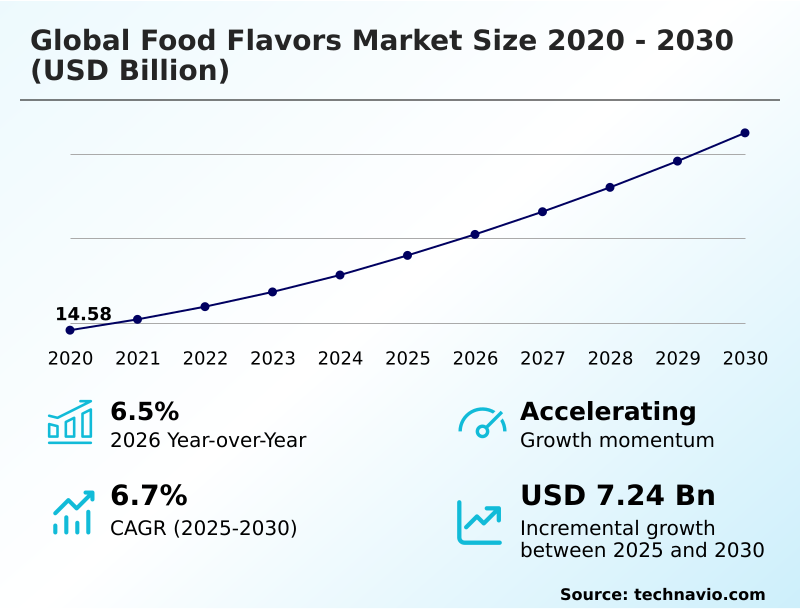

Food Flavors Market Size 2026-2030

The food flavors market size is valued to increase by USD 7.24 billion, at a CAGR of 6.7% from 2025 to 2030. Increasing demand for natural and clean-label ingredients will drive the food flavors market.

Major Market Trends & Insights

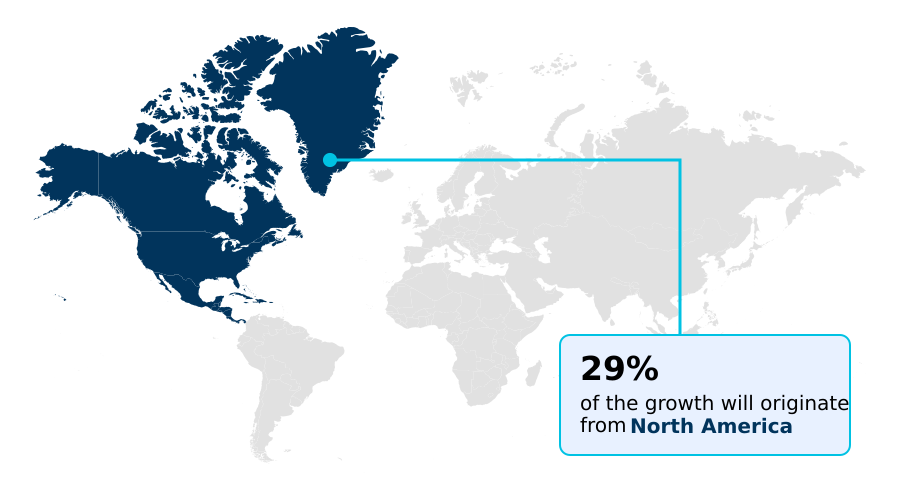

- North America dominated the market and accounted for a 29.2% growth during the forecast period.

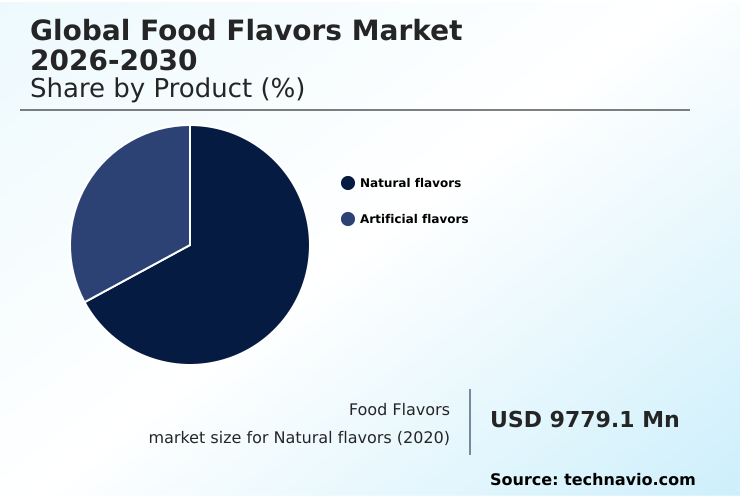

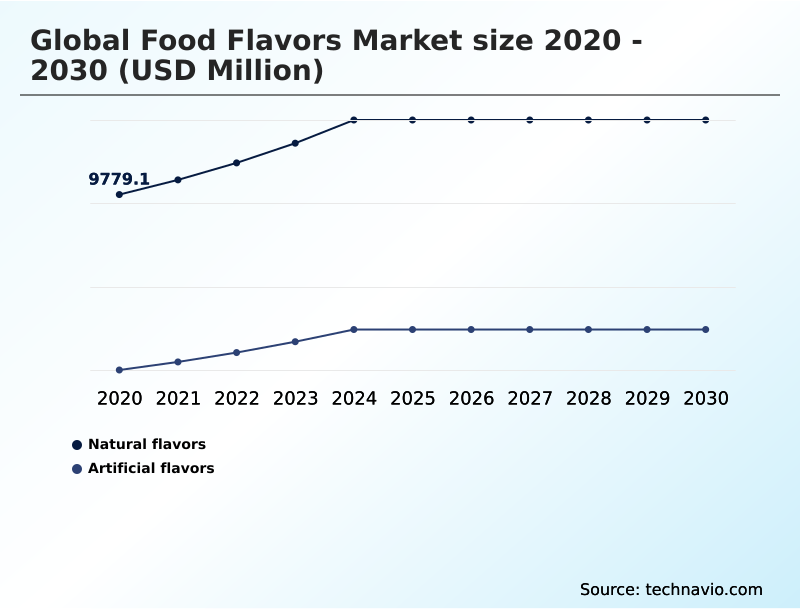

- By Product - Natural flavors segment was valued at USD 11.90 billion in 2024

- By Application - Food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.67 billion

- Market Future Opportunities: USD 7.24 billion

- CAGR from 2025 to 2030 : 6.7%

Market Summary

- The food flavors market is undergoing a significant transformation, driven by consumer demand for authenticity and wellness. This shift compels a move away from traditional artificial flavor synthesis towards sophisticated natural flavor extraction and biosynthetic flavor molecules produced via precision fermentation.

- Key industry efforts are focused on developing clean-label flavor systems and effective plant-based masking agents to improve the palatability of alternative proteins. A critical business scenario involves optimizing the supply chain for volatile citrus oils, where advanced flavor encapsulation technology is used to prevent oxidation, extending shelf life and reducing product waste by up to 15%.

- Innovations in flavor modulation are also central, enabling the creation of low-sugar products without compromising taste. The global food flavors market 2026-2030 is increasingly defined by the convergence of sensory science and sustainable technology, addressing both consumer preferences and regulatory pressures.

What will be the Size of the Food Flavors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Food Flavors Market Segmented?

The food flavors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Natural flavors

- Artificial flavors

- Application

- Food

- Beverages

- End-user

- Food processing

- Foodservice

- Household

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The natural flavors segment is estimated to witness significant growth during the forecast period.

The natural flavors segment is propelled by a fundamental shift in consumer demand for ingredient transparency. This forces manufacturers to pivot from artificial flavor synthesis toward authentic botanical sources.

Adherence to clean-label standards is now a primary purchasing driver, with advanced flavor encapsulation technology and precision fermentation flavors enabling the development of high-stability products.

For instance, new flavor delivery systems have been shown to improve taste retention in processed foods by over 20%. The industry leverages heat-stable flavor carrier ingredients and effective off-note masking for plant-based applications.

The focus remains on biotechnology in flavor production, particularly for sugar and salt reduction technology, while ensuring synthetic flavor stability and addressing challenges like bitterness masking solutions for functional foods.

The Natural flavors segment was valued at USD 11.90 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 29.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Food Flavors Market Demand is Rising in North America Get Free Sample

The geographic landscape of the food flavors market is diversified, with North America leading incremental growth, contributing over 29% of the global expansion. This region exhibits strong demand for advanced plant-based masking agents and savory flavor profiles for health-oriented products.

In APAC, rapid urbanization is fueling the need for cost-effective umami flavor enhancers and high-intensity natural sweeteners.

Innovations such as cold-press extraction and enzymatic processes are being adopted globally to meet clean-label standards, with some facilities reporting a 15% increase in yield from raw materials through such technologies.

The development of specialized hydrocolloid flavor carriers supports the expansion of the beverage sector in emerging economies by improving the stability of fermented flavor ingredients and natural sweetener applications in diverse climates.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the food flavors market increasingly revolves around a complex set of technical and commercial factors. A thorough cost-benefit of natural vs artificial flavors is essential, especially when formulating clean-label savory snacks.

- Key challenges include overcoming off-notes in plant-based dairy and stabilizing volatile oils in beverages, where the impact of encapsulation on flavor release is a critical performance metric. The role of AI in predicting flavor trends is becoming indispensable, with some platforms reducing development cycles by half compared to traditional methods.

- Firms must also navigate the intricate regulatory compliance for natural flavor claims. Advances in heat-stable baking flavors and technologies for masking protein bitterness are creating new opportunities. Concurrently, the sustainability of precision fermentation flavors and applications for upcycled citrus peel flavors are gaining boardroom attention.

- Understanding flavor solutions for salt reduction and how to develop functional flavors for wellness drinks is paramount for market differentiation.

- Furthermore, creating authentic ethnic flavor profiles and nostalgic flavor profiles requires a deep understanding of consumer psychology, while a cost analysis of synthetic vanillin informs sourcing strategies amid challenges in sourcing vanilla beans and the high costs of clean label flavor masking techniques.

What are the key market drivers leading to the rise in the adoption of Food Flavors Industry?

- The increasing demand for natural and clean-label ingredients is a key driver of the global food flavors market.

- The primary market driver is the consumer-led demand for naturality, pushing the industry toward clean-label flavor systems and sustainable sourcing.

- The adoption of natural flavor extraction techniques using food-grade solvents has become widespread, while the development of sustainable aroma chemicals is a key focus.

- This movement is supported by a significant increase in the use of upcycled flavoring agents and botanical extracts, with some manufacturers reducing raw material waste by over 20%.

- As a result, there is strong growth in non-GMO extracts and products with organic flavor certification.

- The natural flavor formulation process is also evolving, with an emphasis on botanical ingredient sourcing and clean-label ingredient solutions to meet the transparency demanded by consumers.

- This shift not only aligns with consumer values but also opens new avenues for innovation in product formulation.

What are the market trends shaping the Food Flavors Industry?

- The integration of artificial intelligence and hyper-personalization is an emerging market trend, enabling the creation of highly targeted and customized sensory experiences.

- Key market trends are redefining product development, with a strong emphasis on functional and personalized offerings. The application of molecular sensory science, for instance, allows for the creation of targeted mouthfeel enhancers and terpene-rich flavors that deliver specific wellness benefits, with R&D teams reporting a 25% faster path to viable prototypes.

- The use of flavor modulation is critical in achieving these goals, especially for sugar reduction solutions in beverages. As part of this trend, sensory data analytics and AI in flavor creation are being leveraged to predict consumer preferences, improving new product success rates by up to 18%.

- This data-driven approach, combined with advanced sensory panel testing and a focus on unique terpene flavor profiles, enables the development of highly differentiated products that align with the growing demand for customized and health-conscious food and beverage options.

What challenges does the Food Flavors Industry face during its growth?

- Regulatory fragmentation and stringent compliance standards are key challenges affecting the growth of the global food flavors market.

- Navigating the complex global regulatory landscape presents a significant market challenge, particularly concerning the classification of biosynthetic flavor molecules and smoke flavor primary products. Discrepancies in international standards increase compliance costs and can delay market entry, with some companies reporting a 15% increase in regulatory-related expenditures.

- Supply chain volatility for key raw materials like volatile citrus oils and aroma chemicals further complicates operations. The production of halal certified flavors requires stringent oversight, while the cost-competitiveness of biosynthetic vanillin production against natural sources remains a hurdle.

- Ensuring synthetic flavor stability during transport and storage is another technical challenge, demanding careful flavor carrier selection and robust aroma profile analysis to prevent issues such as citrus oil oxidation, which can lead to significant product loss.

Exclusive Technavio Analysis on Customer Landscape

The food flavors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food flavors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Food Flavors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, food flavors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apex Flavors Inc. - Analysis indicates a portfolio focused on custom seasoning blends, compound flavors, and coating systems designed for multinational food manufacturers and foodservice operators.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apex Flavors Inc.

- Archer Daniels Midland Co.

- Bell Flavors and Fragrances Inc.

- DSM Firmenich AG

- Flavorchem and Orchidia Fragrances

- Givaudan SA

- GOLD COAST INGREDIENTS INC.

- Huabao International Holdings Ltd.

- International Flavors Inc.

- Kalsec Inc.

- Kerry Group Plc

- McCormick and Co. Inc.

- Ogawa and Co. Ltd.

- Robertet SA

- Sensient Technologies Corp.

- Symrise Group

- Synergy Flavors Inc.

- T.Hasegawa USA Inc.

- Takasago International Corp.

- TREATT Plc

- V Mane Fils

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food flavors market

- In August 2024, a significant research initiative in the United Kingdom successfully isolated a new series of aromatic compounds from upcycled agricultural waste, providing a sustainable and natural alternative to traditional fruit flavors.

- In October 2024, a partnership between an agricultural technology firm and a flavor house led to the development of a mushroom-based flavor enhancer that utilizes the mycelium grown on agricultural side streams such as corn husks.

- In March 2025, a global flavor leader introduced a revolutionary nano-encapsulation technology that protects volatile citrus oils from oxidation, effectively doubling the shelf life of carbonated beverages in warm climates.

- In May 2025, a specialized chemical engineering firm developed a heat-stable flavor carrier that prevents the degradation of delicate vanilla and cocoa notes during the industrial baking process.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Flavors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.7% |

| Market growth 2026-2030 | USD 7244.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food flavors market is driven by sophisticated technological advancements and a decisive pivot towards naturality. Boardroom decisions are increasingly centered on investing in biosynthetic flavor molecules and precision fermentation flavors to mitigate supply chain volatility associated with traditional botanical extracts. The adoption of advanced natural flavor extraction methods like supercritical CO2 extraction, cold-press extraction, and oleoresin extraction is becoming standard.

- Innovations in flavor delivery systems, including flavor encapsulation technology and hydrocolloid flavor carriers, are critical for product stability. Formulators rely on salt reduction technology, sugar reduction solutions, and various mouthfeel enhancers to create healthier products. Key technologies include heat-stable flavor carriers for baked goods, plant-based masking agents for off-note masking, and the use of food-grade solvents.

- The creation of savory flavor profiles, umami flavor enhancers, and reaction flavors requires deep expertise in molecular sensory science and enzymatic processes. With firms achieving up to a 40% reduction in formulation time using sensory data analytics, the integration of AI is reshaping R&D.

- The market also focuses on specific ingredients like volatile citrus oils, aroma chemicals, non-GMO extracts, smoke flavor primary products, and terpene-rich flavors, alongside a commitment to upcycled flavoring agents and halal certified flavors.

What are the Key Data Covered in this Food Flavors Market Research and Growth Report?

-

What is the expected growth of the Food Flavors Market between 2026 and 2030?

-

USD 7.24 billion, at a CAGR of 6.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Natural flavors, and Artificial flavors), Application (Food, and Beverages), End-user (Food processing, Foodservice, and Household) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for natural and clean-label ingredients, Regulatory fragmentation and stringent compliance standards

-

-

Who are the major players in the Food Flavors Market?

-

Apex Flavors Inc., Archer Daniels Midland Co., Bell Flavors and Fragrances Inc., DSM Firmenich AG, Flavorchem and Orchidia Fragrances, Givaudan SA, GOLD COAST INGREDIENTS INC., Huabao International Holdings Ltd., International Flavors Inc., Kalsec Inc., Kerry Group Plc, McCormick and Co. Inc., Ogawa and Co. Ltd., Robertet SA, Sensient Technologies Corp., Symrise Group, Synergy Flavors Inc., T.Hasegawa USA Inc., Takasago International Corp., TREATT Plc and V Mane Fils

-

Market Research Insights

- The dynamics of the food flavors market are shaped by technological innovation and evolving consumer preferences. The strategic selection of a flavor carrier, for instance, can enhance baking-stable flavors, improving product quality and reducing rework rates by up to 10%.

- Meanwhile, the successful application of bitterness masking solutions in functional beverages has been shown to increase consumer acceptance scores by over 30%. Advances in synthetic flavor stability and microencapsulation of flavors allow for greater product resilience in complex supply chains. As manufacturers seek to meet clean-label demands, the focus on organic flavor certification and halal flavor ingredients intensifies.

- This requires rigorous aroma profile analysis to ensure compliance and authenticity, pushing the industry toward more sophisticated and sustainable production methods.

We can help! Our analysts can customize this food flavors market research report to meet your requirements.

RIA -

RIA -