Food Storage Container Market Size 2024-2028

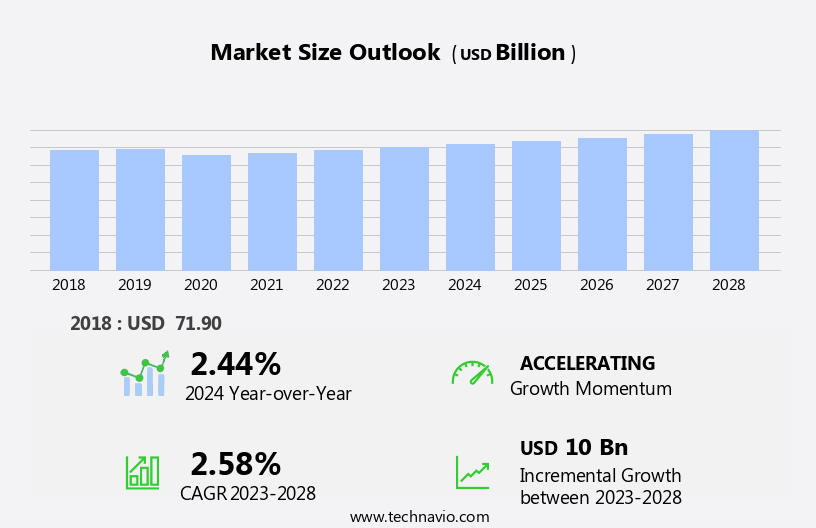

The food storage container market size is forecast to increase by USD 10 billion at a CAGR of 2.58% between 2023 and 2028.

What will be the Size of the Food Storage Container Market During the Forecast Period?

How is this Food Storage Container Industry segmented and which is the largest segment?

The food storage container industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Material

- Plastic

- Metal

- Glass

- Paper

- Type

- Rigid packaging

- Flexible packaging

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

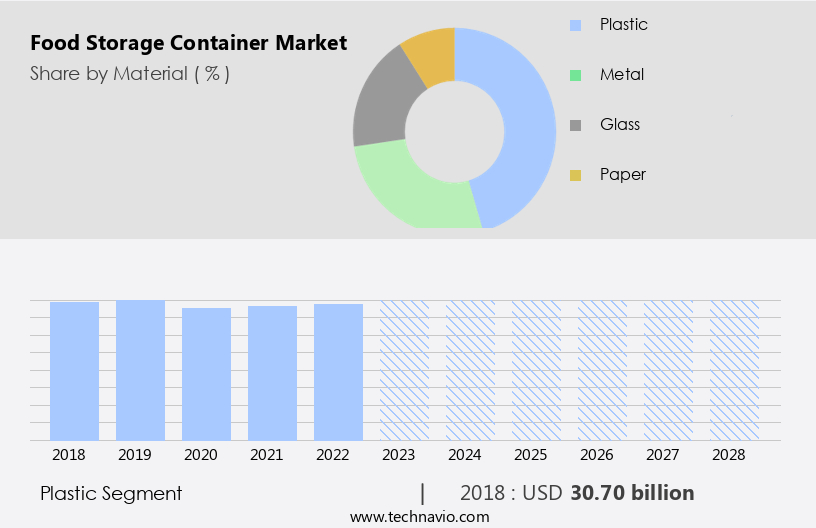

By Material Insights

The plastic segment is estimated to witness significant growth during the forecast period. Plastic containers have gained significant popularity In the food storage market due to their versatility, affordability, and convenience. The lightweight nature of plastic containers makes them easy to transport, stack, and store, making them an ideal choice for consumers with busy lifestyles. Plastic containers offer various advantages, including being shatterproof, which reduces the risk of breakage and subsequent food wastage. They come in various shapes, sizes, and styles, catering to diverse consumer needs. Reusable containers with locking mechanisms preserve leftovers, while disposable plastic containers are suitable for food delivery or takeout. Glass and metal containers, paperboard, bags and pouches, and bottles, jars, bags, cups, tubs, and semi-rigid containers also have their place In the market.

Visual appeal, freshness preservation, portability, and quick meals are essential factors driving the demand for food storage containers. With the increasing consumption of convenience food, the market for food storage containers is expected to grow significantly. Sustainability issues and environmental challenges are key concerns, leading to the development of eco-friendly and biodegradable containers. Food packaging plays a crucial role in maintaining food quality and preserving freshness and nutrition. E-commerce and online food sales have also contributed to the growth of the market. Rigid and flexible containers, including plastic bags, pouches, wraps, fruits and vegetables, meat products, and dairy goods, bakery products, and grain mill products, are in high demand.

Get a glance at the market report of various segments Request Free Sample

The Plastic segment was valued at USD 30.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

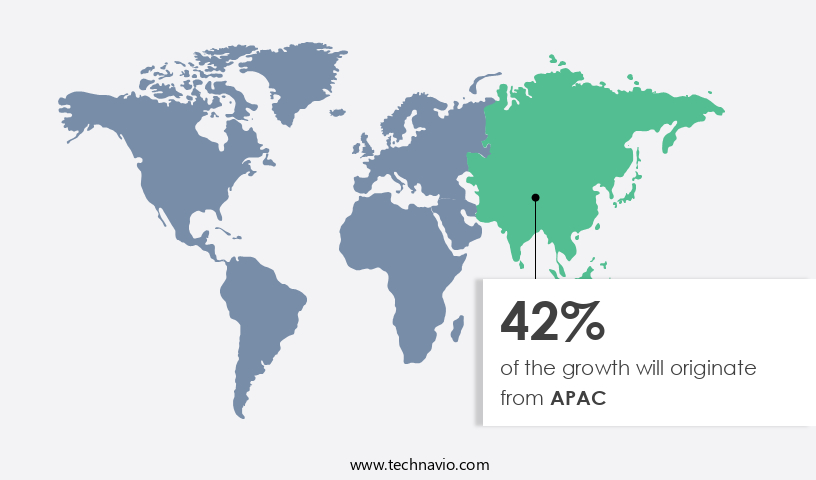

APAC is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in Asia Pacific (APAC) is characterized by a high level of fragmentation due to the presence of numerous companies. To gain a competitive edge, companies offer customized solutions to cater to diverse consumer needs. Key growth drivers include changing consumer preferences towards convenience and an increasing focus on sustainable packaging. The market encompasses various types of containers, including plastic, glass, metal, paperboard, and flexible packaging such as bags and pouches. These containers cater to various food categories, including convenience foods, fruits and vegetables, meat products, dairy goods, bakery products, and beverages. The market is further segmented into rigid and flexible containers, with the latter gaining popularity due to their portability and lightweight nature.

Sustainability issues and environmental challenges are significant concerns, leading to the adoption of eco-friendly materials and innovative packaging designs. Online food sales and the rise of quick meals, particularly among the tech-savvy Generation Z, are further fueling market growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Food Storage Container Industry?

- Growing preference for durable and lightweight containers is the key driver of the market.The market In the US has experienced significant growth due to the changing lifestyles and busy schedules of consumers. In 2023, the urban population accounted for 83.3% of the total population, leading to an increase in spending on food at food service establishments and supermarkets. This trend has influenced market growth, as top companies strive to maintaIn the brand image and value of their products. Moreover, the organized retail segment's expansion has altered consumers' shopping habits, driving demand for various food storage container types, such as plastic, glass, metal, paperboard, bags and pouches, bottles, jars, bags, cups, tubs, and semi-rigid containers.

These containers cater to the need for convenience, portability, and freshness preservation, making them suitable for quick meals and fast food containers. Food quality, freshness, and nutrition are essential factors for consumers, and food packaging plays a crucial role in maintaining these aspects. Aesthetics, affordability, and versatility are also essential considerations for consumers, particularly among younger generations like Generation Z. Sustainability issues and environmental challenges are becoming increasingly important, leading to the development of eco-friendly and recyclable containers. The market for food storage containers is dynamic, with rigid and flexible containers, such as plastic bags, pouches, wraps, and bottles, catering to various consumer needs.

The market encompasses a wide range of products, including fruits and vegetables, meat products, dairy goods, bakery products, grain mill products, and beverages. Food contamination is a significant concern, and high-grade materials and manufacturing processes are essential to ensure food safety.

What are the market trends shaping the Food Storage Container market?

- Growing importance of sustainable containers is the upcoming market trend.The market is witnessing significant growth due to the increasing consumption of convenience food and changing lifestyles. With busy schedules becoming the norm, the demand for portable and quick meal solutions is on the rise. This trend is driving the market for food storage containers, including plastic, glass, metal, paperboard, bags, and pouches. Manufacturers are focusing on visual appeal, freshness preservation, and food quality to cater to consumers' demands. They are investing in innovative technologies to create versatile containers that are eco-friendly, temperature-resistant, and suitable for various end-users, such as dairy goods, bakery products, grain mill products, and meat products.

However, the market is facing sustainability issues and environmental challenges. Strict regulations and consumer preferences are limiting the potential for conventional plastic containers, especially in developed countries. As a result, companies are exploring alternatives, such as semi-rigid and flexible containers, bottles, jars, bags, cups, tubs, and cans made from sustainable materials. The market for food storage containers is also influenced by online food sales and e-commerce. The convenience of ordering food online and having it delivered to one's doorstep has led to an increase in demand for containers that can maintaIn the freshness and nutrition of the food during transportation.

The market is expected to continue growing, with trends such as twin pouches, gussets, corner spouts, stand-up pouches, and flat pouches gaining popularity among consumers, especially among the tech-savvy Generation Z. Despite the challenges, the market for food storage containers remains an attractive investment opportunity due to their affordability, versatility, and lightweight nature. The market is expected to continue evolving as companies focus on improving the functionality and design of their products to meet the evolving needs of consumers.

What challenges does the Food Storage Container Industry face during its growth?

- Issues regarding health and environmental safety is a key challenge affecting the industry growth.In the dynamic food industry, convenience and preservation are key factors driving the demand for food storage containers In the US market. With changing lifestyles and busy schedules, consumers increasingly rely on quick meals and ready-to-eat options. Plastic, glass, metal, paperboard, bags, and pouches are popular container choices, each offering unique benefits. Plastic containers ensure visual appeal, portability, and freshness preservation, while glass and metal containers prioritize food quality and freshness. Flexible containers like paperboard bags, pouches, and wraps offer versatility and lightweight nature, making them suitable for fruits, vegetables, meat products, and various food categories. Food contamination is a significant concern, and regulations, such as the Federal Food, Drug and Cosmetic Act (FDCA), mandate manufacturers to obtain approval from the FDA or USDA to ensure food safety.

This includes additives used in plastic containers, which, if not approved, can pose health risks due to potential toxic release. The food packaging market, encompassing rigid and flexible containers, bottles, jars, bags, cups, tubs, and semi-rigid containers, caters to various food categories like Grain Mill Products, Dairy Goods, and Bakery Products. As online food sales continue to grow, e-commerce platforms require sustainable, affordable, and versatile packaging solutions to maintaIn the freshness and nutrition of food items. Generation Z consumers prioritize sustainability issues and environmental challenges, making eco-friendly and reusable containers increasingly popular. This trend is expected to shape the future of food packaging, focusing on aesthetics, affordability, and functionality.

Exclusive Customer Landscape

The food storage container market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food storage container market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, food storage container market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Accent-Fairchild Group - Accent Home Products, a division of the company, provides a range of food storage containers. These containers cater to the growing demand for convenient, airtight, and space-efficient solutions for food preservation. The market continues to expand due to increasing consumer awareness of food waste reduction and healthier eating habits. Accent Home Products' offerings align with this trend, featuring various sizes and materials to accommodate diverse food types and consumer preferences. The company's commitment to quality and innovation ensures that its food storage containers meet the evolving needs of modern households.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accent-Fairchild Group

- Amcor Plc

- Anchor Glass Container Corp.

- Berry Global Inc.

- Crown Holdings Inc.

- Graham Packaging Co. LP

- Graphic Packaging Holding Co.

- Hamilton Housewares Pvt. Ltd.

- Newell Brands Inc.

- Nilkamal Ltd.

- O I Glass Inc.

- Pactiv Evergreen Inc.

- Plastipak Holdings Inc.

- Printpack Inc.

- RING Container Technologies

- S.C. Johnson and Son Inc.

- Shantou Mandun Plastic Co. Ltd.

- Sonoco Products Co.

- Sterilite Corp.

- Tupperware Brands Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of products designed to accommodate various types of food items, catering to the evolving consumption patterns brought about by changing lifestyles and busy schedules. Convenience has become a significant driving force In the food industry, leading to the increased popularity of containers that offer freshness preservation, portability, and visual appeal. Plastic containers, glass containers, metal containers, paperboard bags and pouches, and various types of boxes, clamshells, cans, and jars are among the most common options available In the market. Each material offers unique advantages, such as freshness preservation, food quality maintenance, and affordability.

Plastic containers are known for their lightweight nature, versatility, and affordability. They are widely used for storing a variety of food items, including fruits and vegetables, meat products, dairy goods, bakery products, and grains. However, concerns regarding sustainability issues and environmental challenges have led to a growing demand for alternatives to plastic containers. Glass containers and jars, on the other hand, offer superior aesthetics and are often used for storing high-end food items or for display purposes. They are ideal for preserving the freshness and nutrition of food, making them a popular choice for consumers seeking to maintain food quality.

Metal containers, particularly cans and tins, are commonly used for storing canned goods, such as fruits, vegetables, and meats. Their airtight seals help preserve the freshness of the contents, making them a practical choice for long-term storage. Flexible containers, including plastic bags, pouches, wraps, and stand-up pouches, offer the advantage of portability and ease of use. They are widely used for storing a variety of food items, including snacks, dried fruits, and powdered beverages. Gussets and corner spouts are popular features that enhance the functionality of these containers. The rise of e-commerce and online food sales has led to an increased demand for food packaging solutions that cater to the unique requirements of the digital marketplace.

Rigid containers, such as boxes and clamshells, are commonly used for shipping perishable food items, while flexible containers, such as flat pouches, are ideal for online sales of dry goods and snacks. Generation Z consumers, who prioritize convenience and sustainability, are driving the demand for innovative food storage solutions. Twin pouches, for instance, offer the convenience of two separate compartments for storing different food items, while also addressing sustainability concerns by reducing the amount of packaging waste. Food contamination is a significant concern In the market, leading to the increasing popularity of high-grade materials and advanced preservation technologies.

The use of antimicrobial agents and vacuum sealing technologies are among the strategies being employed to ensure food safety and extend the shelf life of stored food items. In conclusion, the market is a dynamic and evolving industry that caters to the diverse needs of consumers. The market is driven by factors such as changing lifestyles, convenience, freshness preservation, portability, and sustainability concerns. The use of various materials, such as plastic, glass, and metal, as well as innovative designs, such as gussets and corner spouts, are shaping the future of food storage solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.58% |

|

Market growth 2024-2028 |

USD 10 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.44 |

|

Key countries |

US, China, India, Germany, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Food Storage Container Market Research and Growth Report?

- CAGR of the Food Storage Container industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the food storage container market growth of industry companies

We can help! Our analysts can customize this food storage container market research report to meet your requirements.

RIA -

RIA -