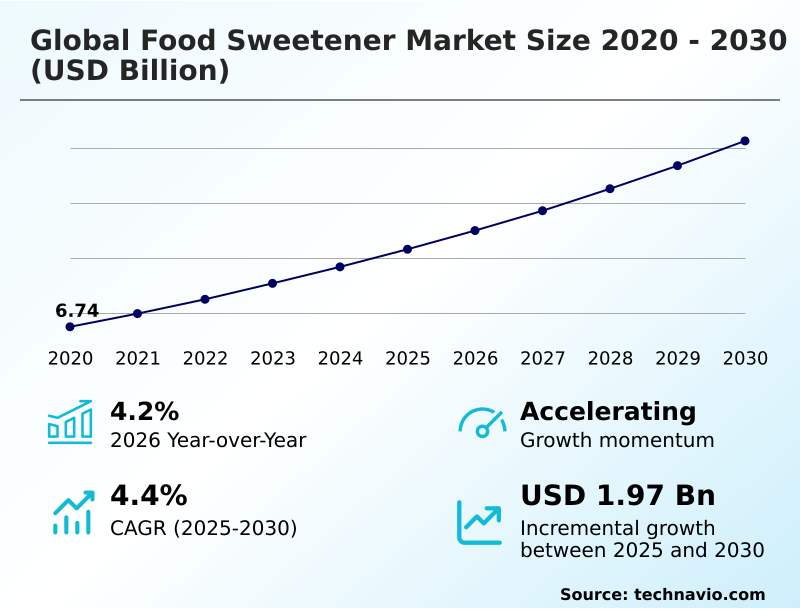

Food Sweetener Market Size 2026-2030

The food sweetener market size is valued to increase by USD 1.97 billion, at a CAGR of 4.4% from 2025 to 2030. Multiple applications of sugar substitutes will drive the food sweetener market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 41.2% growth during the forecast period.

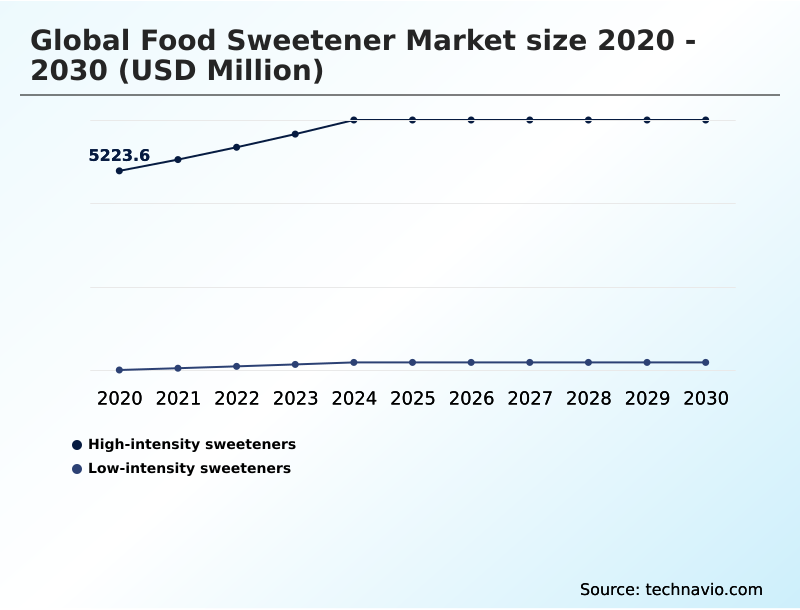

- By Type - High-intensity sweeteners segment was valued at USD 6.17 billion in 2024

- By Application - Bakery and confectionery segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.38 billion

- Market Future Opportunities: USD 1.97 billion

- CAGR from 2025 to 2030 : 4.4%

Market Summary

- The food sweetener market is undergoing a significant transformation, driven by a pronounced consumer shift toward health and wellness. This evolution is compelling manufacturers to innovate beyond traditional sucrose, embracing a diverse portfolio of sugar substitutes.

- Key drivers include the widespread adoption of low-calorie and zero-calorie sweeteners in response to rising metabolic health concerns and regulatory pressures to reduce sugar content in processed foods. A prominent trend is the growing demand for natural and plant-based sweeteners, such as stevia and monk fruit, which align with clean-label preferences.

- For instance, a beverage company might reformulate its flagship product line using a blend of bio-engineered sweeteners and natural extracts to achieve a 30% calorie reduction while maintaining the desired taste profile, thereby appealing to health-conscious consumers.

- However, the market faces challenges related to the sensory attributes of some sugar alternatives, including lingering aftertastes, and the high costs associated with research and development for novel sweetening solutions. Navigating stringent food safety regulations and managing consumer perceptions of artificial sweeteners remain critical for sustained market success.

- This dynamic environment necessitates continuous innovation in food science to balance taste, cost, and health benefits.

What will be the Size of the Food Sweetener Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Food Sweetener Market Segmented?

The food sweetener industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- High-intensity sweeteners

- Low-intensity sweeteners

- Application

- Bakery and confectionery

- Beverages

- Dairy and frozen desserts

- Others

- Source

- Plant-based

- Synthetic

- Bio-engineered

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The high-intensity sweeteners segment is estimated to witness significant growth during the forecast period.

The global food sweetener market segmentation is shaped by the rising adoption of high-intensity sweeteners, driven by consumer demand for low-calorie solutions.

These potent sugar substitutes, including both natural sweeteners and artificial sweeteners, enable significant sugar reduction in food and beverage formulation, addressing health-conscious reformulation goals.

Food and beverage manufacturers leverage these sweetening solutions for their functional properties in finished products, with formulation blends enhancing mouthfeel and texture. Innovations in plant-derived extracts and advanced sweetening systems are critical for maintaining a competitive edge.

This segment is a primary contributor to market expansion, accounting for over 41% of incremental growth by enabling the development of products that meet clean-label requirements without compromising taste.

The High-intensity sweeteners segment was valued at USD 6.17 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Food Sweetener Market Demand is Rising in North America Get Free Sample

The geographic landscape of the food sweetener market is defined by varied regional dynamics and consumer preferences. North America leads in market share, commanding over 35% of the market, driven by strong consumer demand for low-calorie and natural alternatives.

In this region, advanced food technology infrastructure supports the rapid adoption of novel ingredients like sweet proteins and rare sugars. Europe follows, with a mature market focused on clean-label compliance and regulatory-driven sugar reduction.

APAC is the fastest-growing region, with increasing health awareness and rising disposable incomes fueling demand for healthier food options.

Latin America and the Middle East and Africa represent emerging markets with significant growth potential, although adoption is tempered by pricing sensitivities and supply chain complexities.

Across these regions, the successful application of nutritive sweeteners and saccharin alternatives is critical for market penetration and expansion.

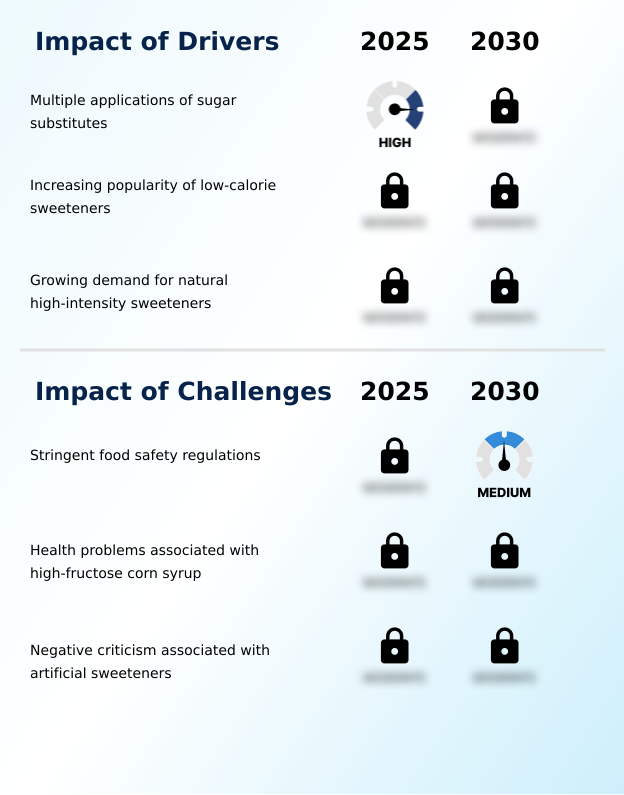

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the food sweetener market requires a deep understanding of complex formulation variables and consumer trends. The high-intensity vs low-intensity sweeteners debate continues to shape product development, with choices impacting both cost and label appeal. Applications of plant-based sweeteners are expanding beyond beverages into bakery and confectionery, demanding new approaches to taste modulation.

- The use of synthetic sweeteners in beverage formulation remains widespread due to cost-effectiveness, but it faces scrutiny over clean-label perceptions. Simultaneously, manufacturers face significant challenges in bio-engineered sweetener production, particularly in achieving scale and cost parity. A key focus area is steviol glycoside taste profile improvement to mitigate bitter off-notes.

- The role of polyols in confectionery is well-established for texture and bulk, but formulators are exploring novel blends. Furthermore, clean label sweetener sourcing strategies are becoming integral to brand identity and consumer trust. Formulating with rare sugars like allulose offers benefits but requires navigating regulatory hurdles and supply chain constraints.

- The exploration of sweet protein stability in food processing is a frontier of innovation, promising high-intensity sweetness with a clean taste. Finally, a thorough grasp of the non-nutritive sweetener regulatory landscape is essential for global market access.

- Companies that effectively integrate these considerations into their operational planning often achieve a 15% faster product launch cycle compared to competitors with siloed R&D and regulatory teams.

What are the key market drivers leading to the rise in the adoption of Food Sweetener Industry?

- The increasing use of sugar substitutes across multiple applications is a key driver for the market.

- The market's growth is primarily driven by the rising global focus on health and wellness, which is accelerating the adoption of low-calorie sweeteners and alternative sweetening agents.

- The increasing prevalence of lifestyle-related health conditions has prompted food and beverage companies to actively pursue sugar-reduction strategies, incorporating everything from bulk sweeteners to high-fructose corn syrup alternatives.

- Innovations that enhance the sweet taste perception while minimizing off-notes have improved product acceptance, with reformulated products achieving up to a 20% higher repeat purchase rate.

- Furthermore, the versatility of sweeteners in diverse applications, from beverages to baked goods, expands market opportunities.

- Regulatory support for sugar reduction initiatives also acts as a significant catalyst, encouraging manufacturers to innovate with ingredients like sugar beet molasses and other plant-derived options, thereby driving sustained market expansion.

What are the market trends shaping the Food Sweetener Industry?

- The growing demand for organic food sweeteners is an emerging trend, driven by a heightened consumer focus on health, wellness, and clean-label products.

- Key trends in the food sweetener market are driven by consumer demand for healthier options and technological advancements in ingredient science. The focus on sugar-like taste and clean-label compliance is pushing innovation in high-intensity natural sweeteners and novel sweetening ingredients.

- For example, advancements in fermentation technology have led to the development of sweeteners with improved sensory attributes, showing a 30% reduction in undesirable aftertaste compared to earlier versions. Furthermore, the trend toward non-GMO and organic sweetening solutions is gaining momentum, with brands that adopt these standards reporting an average 15% increase in consumer loyalty.

- The development of functional sweeteners that offer added health benefits, such as prebiotic effects, is another significant trend shaping the competitive landscape. This shift compels manufacturers to invest in R&D to create products that deliver both sweetness and wellness advantages.

What challenges does the Food Sweetener Industry face during its growth?

- Stringent food safety regulations present a key challenge that impacts the growth of the industry.

- The food sweetener market faces significant challenges related to regulatory complexities and consumer perceptions. Navigating the intricate web of global food safety regulations for ingredients like acesulfame-k and various polyols demands substantial investment in compliance and testing, with regulatory approval processes sometimes extending product development timelines by up to 18 months.

- Another major hurdle is overcoming the negative consumer sentiment associated with certain artificial and synthetic sweeteners. Formulators must also address technical difficulties such as ensuring solubility in beverage systems and achieving the desired texture in food products.

- These challenges are compounded by supply chain vulnerabilities for natural ingredients, which can lead to price volatility and impact production costs, thereby constraining market growth despite strong underlying demand for sugar alternatives.

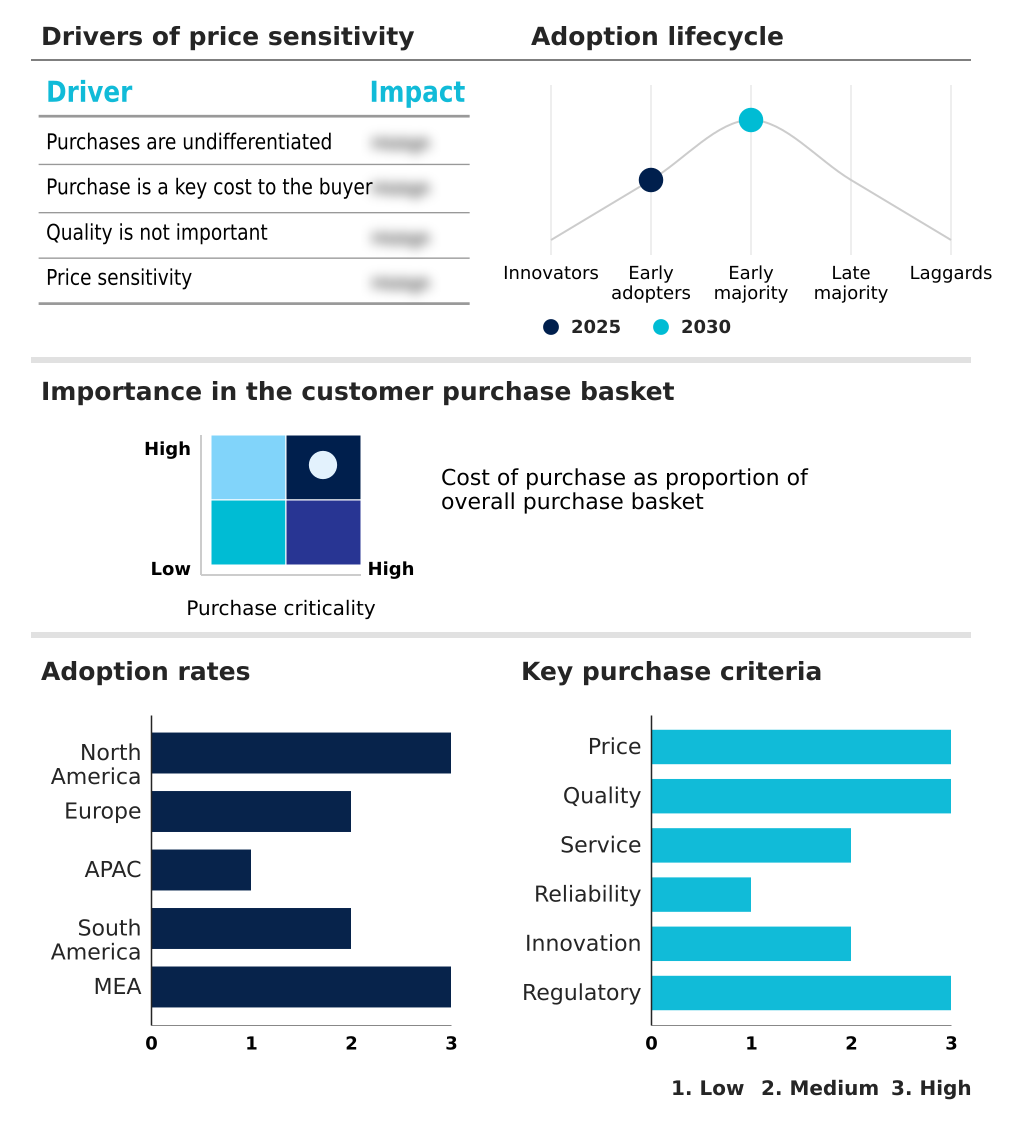

Exclusive Technavio Analysis on Customer Landscape

The food sweetener market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food sweetener market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Food Sweetener Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, food sweetener market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - The company provides a portfolio of sweetener solutions, including nutritive and non-nutritive options, catering to diverse industrial food and beverage formulation requirements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Archer Daniels Midland Co.

- Cargill Inc.

- Celanese Corp.

- Dohler GmbH

- DuPont de Nemours Inc.

- Foodchem International Corp.

- GLG Life Tech Corp.

- Ingredion Inc.

- International Flavors Inc.

- Kerry Group Plc

- Roquette Freres SA

- Tate and Lyle Plc

- Tereos Participations

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food sweetener market

- In September 2025, Cargill's precision-fermented stevia sweetener, EverSweet, was named a finalist in the Global Good Awards for Game Changing Innovation of the Year, highlighting the market's focus on sustainable and healthier sweetening solutions.

- In July 2025, the U.S. Food and Drug Administration (FDA) finalized regulatory updates to revoke outdated standards for certain artificially sweetened canned fruit and vegetable products, signaling evolving oversight in the sweetener industry.

- In June 2025, Layn Natural Ingredients launched its plant-based sweetener SteviUp M2, a high-purity steviol glycoside designed to offer improved solubility and a sugar-like taste for various food and beverage applications.

- In February 2025, Oobli announced a strategic partnership with Ingredion, following an $18 million funding round, to accelerate the commercialization of its sweet protein-based systems for sugar reduction.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Sweetener Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.4% |

| Market growth 2026-2030 | USD 1969.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food sweetener market is advancing through intense innovation focused on health, functionality, and sustainability. The sector is moving beyond simple sucrose replacement to embrace sophisticated high-fructose corn syrup alternatives and next-generation sugar alcohol variants. A key industry dynamic is the development of bioconversion-derived sweeteners and fermentation-based formulations, which offer improved taste profiles and cleaner labels.

- The application of high-potency sweeteners, including advanced stevia leaf extracts and monk fruit concentrate, is expanding across categories. Innovations such as sweet molecule engineering and precision fermentation sweeteners are enabling the creation of novel sweetening compounds with specific functional benefits. For example, the use of brazzein sweet protein is gaining traction for its clean, sugar-like taste.

- Manufacturers are also focused on flavor modification technologies and bitterness blocking agents to overcome sensory challenges. This technical progress is critical, as companies using synergistic sweetener blends have demonstrated a 20% improvement in formulation cost-efficiency.

- The market's evolution is defined by the interplay between consumer demand for naturalness, regulatory pressures for sugar reduction, and the scientific pursuit of the perfect sugar substitute.

What are the Key Data Covered in this Food Sweetener Market Research and Growth Report?

-

What is the expected growth of the Food Sweetener Market between 2026 and 2030?

-

USD 1.97 billion, at a CAGR of 4.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (High-intensity sweeteners, and Low-intensity sweeteners), Application (Bakery and confectionery, Beverages, Dairy and frozen desserts, and Others), Source (Plant-based, Synthetic, and Bio-engineered) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Multiple applications of sugar substitutes, Stringent food safety regulations

-

-

Who are the major players in the Food Sweetener Market?

-

Ajinomoto Co. Inc., Archer Daniels Midland Co., Cargill Inc., Celanese Corp., Dohler GmbH, DuPont de Nemours Inc., Foodchem International Corp., GLG Life Tech Corp., Ingredion Inc., International Flavors Inc., Kerry Group Plc, Roquette Freres SA, Tate and Lyle Plc, Tereos Participations and Wilmar International Ltd.

-

Market Research Insights

- The food sweetener market is characterized by dynamic shifts as manufacturers align with consumer health priorities. The demand for reduced sugar content is reshaping food formulation science, with a focus on taste profile optimization and sensory experience enhancement. For instance, companies leveraging advanced aftertaste masking technology report a 25% increase in consumer preference scores for reformulated beverages.

- Concurrently, ingredient sourcing transparency has become a competitive differentiator, with clean label requirements driving a 15% uptick in the adoption of plant-derived alternatives. Achieving optimal mouthfeel and stability remains a core challenge, but innovations in solubility improvement methods are enabling broader applications.

- These factors underscore a market where technical proficiency in calorie reduction formulation and sugar reduction strategies is essential for growth and consumer acceptance.

We can help! Our analysts can customize this food sweetener market research report to meet your requirements.

RIA -

RIA -