Labels Market Size 2026-2030

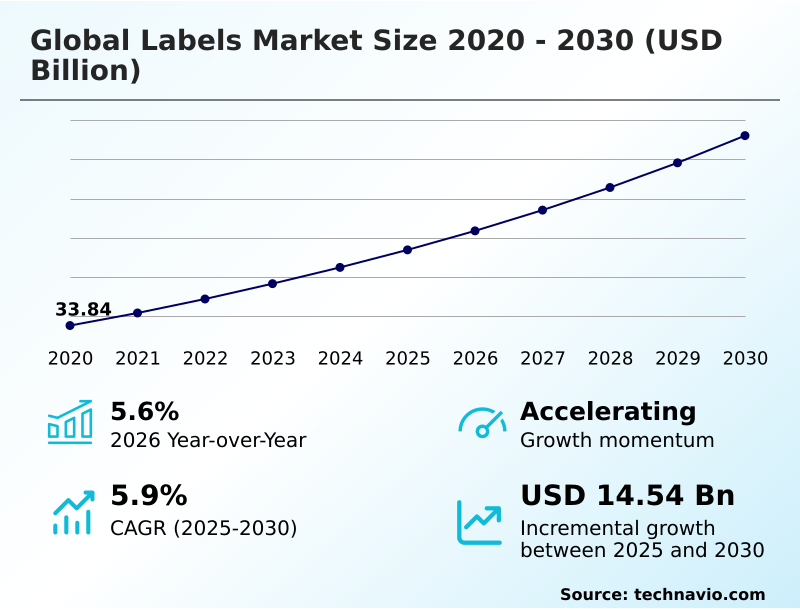

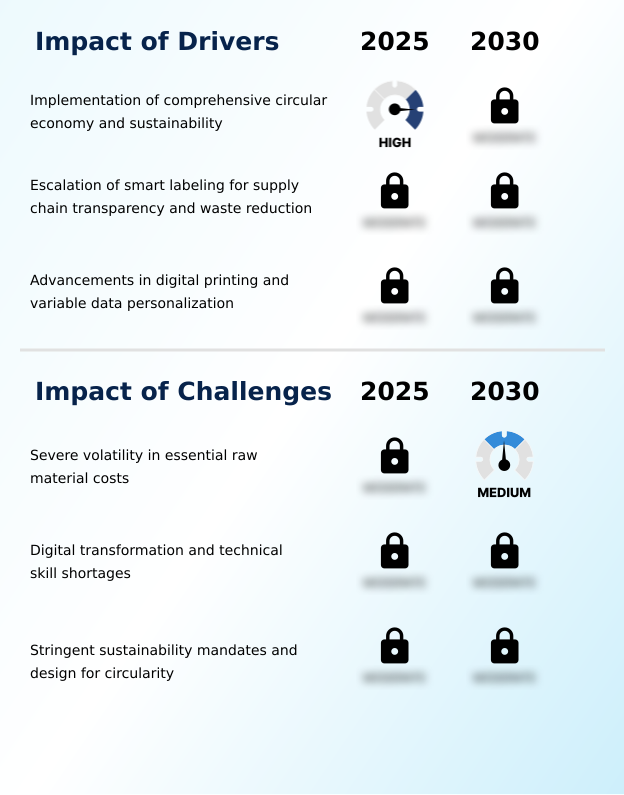

The labels market size is valued to increase by USD 14.54 billion, at a CAGR of 5.9% from 2025 to 2030. Implementation of comprehensive circular economy and sustainability will drive the labels market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 48.7% growth during the forecast period.

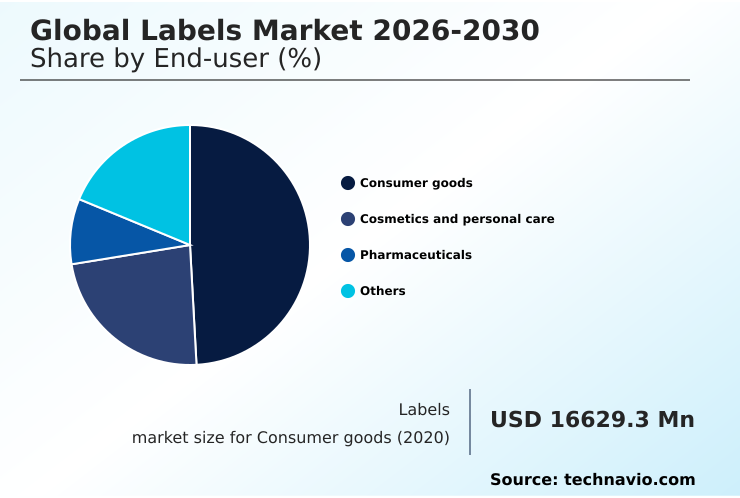

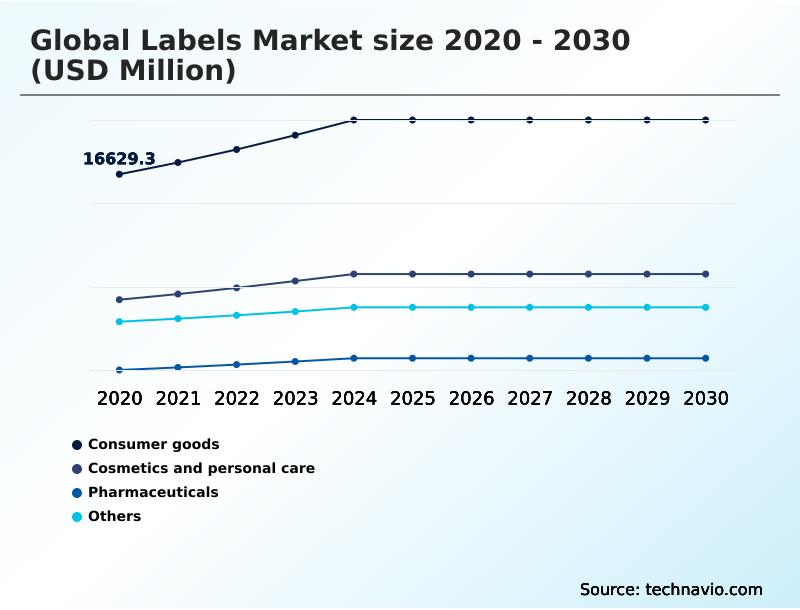

- By End-user - Consumer goods segment was valued at USD 20.41 billion in 2024

- By Type - Pressure-sensitive label segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 24.16 billion

- Market Future Opportunities: USD 14.54 billion

- CAGR from 2025 to 2030 : 5.9%

Market Summary

- The labels market is undergoing a significant transformation, driven by the dual forces of digitalization and sustainability. The expansion of e-commerce necessitates robust logistics labels capable of supporting high-speed automated sorting systems, while consumer demand for eco-friendly products fuels innovation in materials science. This includes the development of compostable face stocks and wash-off adhesives that facilitate recycling.

- A key trend is the integration of smart technologies, such as radio frequency identification and near field communication, which convert passive labels into active data carriers. For instance, a pharmaceutical company can leverage serialized security labels with integrated sensors for cold chain monitoring, ensuring vaccine efficacy from production to patient administration.

- This provides end-to-end supply chain transparency, enhances brand protection technology, and ensures regulatory compliance. However, the industry grapples with challenges like raw material price volatility and the need for significant capital investment in digital printing technology to support short-run, personalized packaging requirements. The market's trajectory is defined by this balance between technological advancement and environmental responsibility.

What will be the Size of the Labels Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Labels Market Segmented?

The labels industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Consumer goods

- Cosmetics and personal care

- Pharmaceuticals

- Others

- Type

- Pressure-sensitive label

- Glue-applied label

- Sleeve label

- In-mold labels

- Material

- Plastic and film

- Paper

- Metal foil

- Fabric

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The consumer goods segment is estimated to witness significant growth during the forecast period.

The consumer goods segment is a primary end-user, where labels are a critical interface for brand differentiation and information delivery.

The proliferation of digital printing technology enables extensive use of variable data printing for mass personalization campaigns, while the integration of radio frequency identification allows for superior inventory accuracy systems.

As brands pursue aggressive sustainability targets, the adoption of liner-less labels is gaining momentum, with some companies reporting a reduction in operational waste by over 20% in high-volume settings.

The demand for high-resolution graphics and a premium shelf appeal continues to drive innovation in decorative finish options.

This is complemented by a move towards sustainable labeling solutions, which has become a key purchasing criterion for major consumer goods companies aiming for ethical production standards.

The Consumer goods segment was valued at USD 20.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 48.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Labels Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by robust growth in APAC, which is poised to contribute nearly 49% of the market's incremental growth.

This expansion is fueled by rapid industrialization, the formalization of retail, and the rise of a large consumer base in countries like China and India.

Strong demand from the manufacturing, e-commerce, and pharmaceutical sectors requires high-volume, cost-effective industrial identification labels and packaging.

The region is seeing a significant shift toward digital inkjet systems, with adoption rates leading to a 25% improvement in production throughput for brands needing regionalized packaging with high-resolution graphics.

While cost remains a factor, there is growing adoption of premium solutions like tamper-evident features and sustainable labeling solutions to meet both local and export standards, reflecting a maturing market focused on brand protection technology.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the labels market is increasingly defined by the impact of digital printing on labels market, which enables unprecedented agility. This technological shift complements the urgent need for sustainable materials for pressure-sensitive labels, forcing innovation in recyclable and compostable options.

- In high-value sectors, RFID technology in pharmaceutical labeling is becoming standard for traceability, working alongside advancements in tamper-evident label technology to ensure product safety. Businesses are navigating the challenges of implementing circular economy in labels by adopting solutions like wash-off adhesives for PET bottle recycling, which are critical to the success of the circular model.

- The role of mono-material construction in sustainability is equally vital, simplifying end-of-life processing. Concurrently, smart labeling for supply chain optimization, utilizing tools such as QR code applications in food traceability and NFC labels for enhanced consumer engagement, is transforming logistics.

- The transition from legacy methods, highlighted by the flexographic to digital printing transition benefits, has been shown to reduce job changeover waste by over 50%. This flexibility allows for effective variable data printing for personalized marketing and the use of expanded content labels for regulatory compliance.

- Other key considerations include the cost-effectiveness of glue-applied versus sleeve labels, the adoption of liner-less labels for waste reduction in logistics, and the implementation of digital product passport requirements and solutions.

- Material science is also advancing with bio-based polymers in flexible packaging labels and the use of in-mold labeling for durable consumer goods, while security labels for brand protection strategies now often incorporate sophisticated holographic features for anti-counterfeiting.

What are the key market drivers leading to the rise in the adoption of Labels Industry?

- The implementation of comprehensive circular economy principles and a heightened focus on sustainability serve as primary drivers propelling innovation and adoption within the market.

- Key market drivers are centered on digitalization and sustainability mandates that reshape production and compliance.

- The widespread adoption of digital printing technology, including advanced digital inkjet systems, facilitates on-demand label production, cutting time-to-market for new products by an average of 30%. This agility is crucial for personalized packaging and agile marketing support.

- Furthermore, stringent environmental regulations are compelling a shift toward eco-friendly packaging design. Proactive adoption of solutions like mono-material construction and liner-less labels not only supports packaging waste reduction goals but also mitigates compliance risk, helping companies avoid significant fines.

- This regulatory push makes technologies like the digital product passport an essential component for ensuring supply chain transparency and meeting extended producer responsibility requirements.

What are the market trends shaping the Labels Industry?

- The evolution toward intelligent and connected labeling solutions represents a significant market trend, driven by the increasing need for enhanced supply chain visibility and interactive consumer engagement.

- The market is rapidly evolving toward intelligent and sustainable solutions, driven by regulatory pressures and supply chain demands. The adoption of smart labeling solutions incorporating technologies like near field communication and digital watermarking has been shown to reduce inventory shrinkage by up to 40% in high-value retail sectors.

- Concurrently, advancements in sustainable materials, such as compostable face stocks and recycled content substrates, are becoming standard. For instance, the use of specialized wash-off adhesives improves PET recycling yields by over 15%, aligning with circular economy in packaging goals.

- This pivot to intelligent packaging provides enhanced food traceability and supports lean manufacturing principles, transforming labels into functional assets that improve both efficiency and brand trust.

What challenges does the Labels Industry face during its growth?

- Severe volatility in the cost of essential raw materials, including paper pulps and plastic resins, presents a key challenge affecting profitability and price stability across the industry.

- The market faces significant challenges from raw material volatility and a growing technical skills gap. Severe price fluctuations in essential inputs like bio-based polymers and high-performance adhesives, with swings of over 18% in a single quarter, directly impact profit margins and complicate financial forecasting. This requires sophisticated predictive maintenance in printing operations to minimize waste.

- Simultaneously, the digital transformation demands a workforce proficient in operating complex systems for variable data printing and automated quality control.

- The current skills shortage increases technician training and onboarding time by an estimated 30%, delaying ROI on capital investments in new technologies like radio frequency identification and creating a barrier for smaller firms aiming to achieve pharmaceutical serialization or other advanced tracking capabilities.

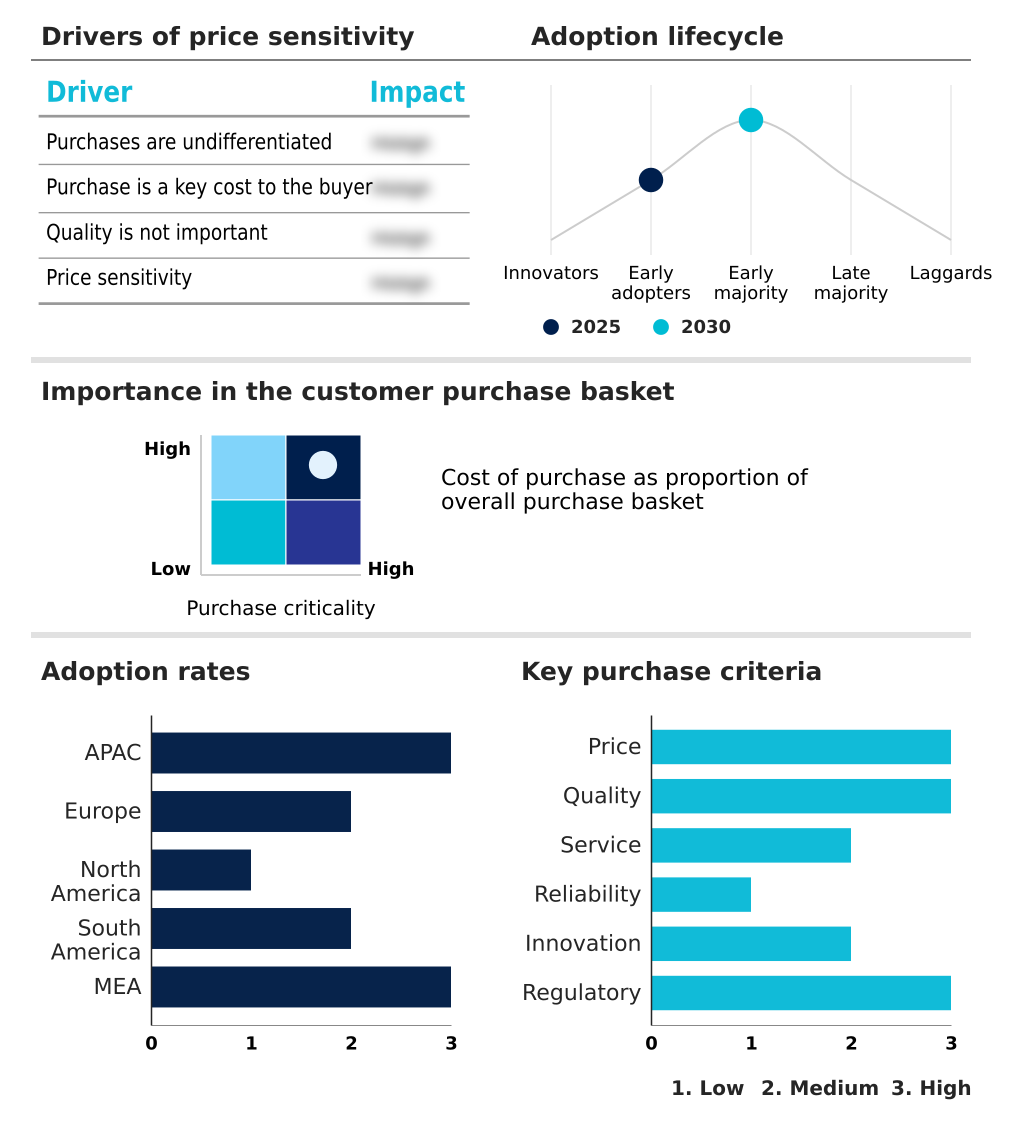

Exclusive Technavio Analysis on Customer Landscape

The labels market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the labels market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Labels Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, labels market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Offers a comprehensive range of labeling solutions, including pressure-sensitive, shrink sleeve, and wrap-around formats, tailored for diverse consumer and industrial packaging applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Avery Dennison Corp.

- Brady Corp.

- CCL Industries Inc.

- Cenveo Worldwide Ltd.

- Consolidated Label Co.

- Denny Bros Ltd.

- Essentra Components

- Fuji Seal International Inc.

- HERMA GmbH

- Multi Color Corp.

- OPM Group

- Resource Label Group LLC

- SATO Holdings Corp.

- Schreiner Group GmbH and Co. KG

- UPM Kymmene Corp.

- Yorkshire Labels Ltd

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Labels market

- In January 2025, Avery Dennison South Asia announced the launch of a new premium labels range designed to enhance consumer experience with unique textures and surface patterns, targeting the high-end consumer goods sector.

- In January 2025, the European Medicines Agency mandated the use of the IRIS platform for Article 61(3) notifications, streamlining the process for updating labeling information for centrally authorized pharmaceutical products.

- In February 2025, the European Union's Packaging and Packaging Waste Regulation entered a new phase, introducing stricter labeling and reuse requirements compelling cosmetic brands to adopt mono-material packaging and wash-off adhesives.

- In February 2025, Polytag launched its QR Squared service, a QR code analytics platform providing brands with detailed performance data, which enhances tracking and inventory management in industrial and transportation contexts.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Labels Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.9% |

| Market growth 2026-2030 | USD 14536.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Boardroom-level decisions are increasingly focused on the strategic integration of labeling technologies to drive efficiency and compliance. The modern labels ecosystem combines various formats, including the pressure-sensitive label, glue-applied label, sleeve label, and in-mold labels, with advanced printing methods like digital printing technology and legacy flexographic printing.

- The shift toward digital inkjet systems and thermal transfer labels facilitates variable data printing, a stark contrast to older methods. Smart labeling is now a cornerstone, utilizing radio frequency identification, near field communication, and QR code technology embedded in RFID labels and barcode labels to power electronic tracking systems.

- For security, tamper-evident features, holographic security features, and specialized security labels are critical. Sustainability mandates are driving the adoption of wash-off adhesives, mono-material construction, compostable face stocks, thin-gauge liners, and liner-less labels made from recycled content substrates or bio-based polymers.

- This pivot away from traditional synthetic labels has achieved a 30% reduction in compliance-related processing time for companies in regulated markets. Material choices now span self-adhesive label materials with specialized release liners and high-performance adhesives, while applications range from industrial identification labels to expanded content labels with a premium decorative finish.

What are the Key Data Covered in this Labels Market Research and Growth Report?

-

What is the expected growth of the Labels Market between 2026 and 2030?

-

USD 14.54 billion, at a CAGR of 5.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Consumer goods, Cosmetics and personal care, Pharmaceuticals, and Others), Type (Pressure-sensitive label, Glue-applied label, Sleeve label, and In-mold labels), Material (Plastic and film, Paper, Metal foil, and Fabric) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Implementation of comprehensive circular economy and sustainability, Severe volatility in essential raw material costs

-

-

Who are the major players in the Labels Market?

-

Amcor Plc, Avery Dennison Corp., Brady Corp., CCL Industries Inc., Cenveo Worldwide Ltd., Consolidated Label Co., Denny Bros Ltd., Essentra Components, Fuji Seal International Inc., HERMA GmbH, Multi Color Corp., OPM Group, Resource Label Group LLC, SATO Holdings Corp., Schreiner Group GmbH and Co. KG, UPM Kymmene Corp., Yorkshire Labels Ltd and Zebra Technologies Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by the need for enhanced operational intelligence and consumer interaction. The integration of intelligent packaging for real-time asset tracking has been shown to improve inventory accuracy systems by over 98% for early adopters in the retail sector, drastically reducing stock-outs and waste.

- Concurrently, the use of consumer engagement platforms, accessed via QR code technology on labels, has boosted repeat purchase rates by up to 15% in targeted campaigns by providing detailed product provenance and sustainability information. This shift toward data-driven functionality is compelling a move to on-demand label production, offering greater flexibility for agile marketing support and reducing obsolescence.

- The ability to provide these value-added services is becoming a critical differentiator, transforming labels from a simple component into a strategic asset for achieving food traceability and supply chain transparency.

We can help! Our analysts can customize this labels market research report to meet your requirements.

RIA -

RIA -