Friction Products Market Size 2026-2030

The friction products market size is valued to increase by USD 10.13 billion, at a CAGR of 5.9% from 2025 to 2030. Aging fleet of automobiles will drive the friction products market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 45.3% growth during the forecast period.

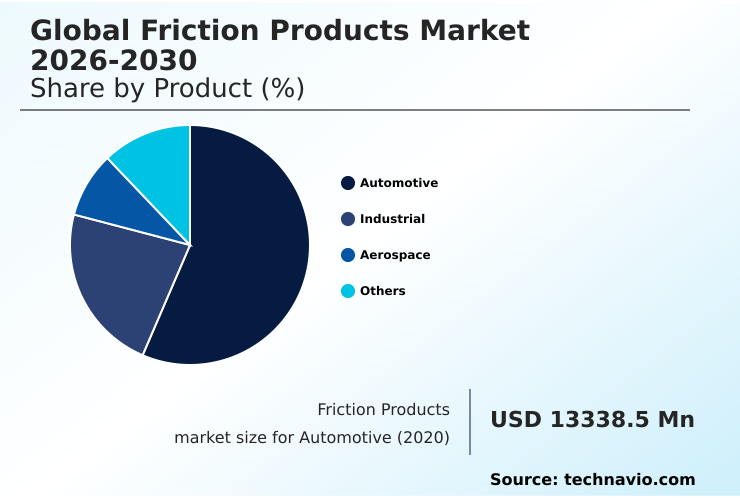

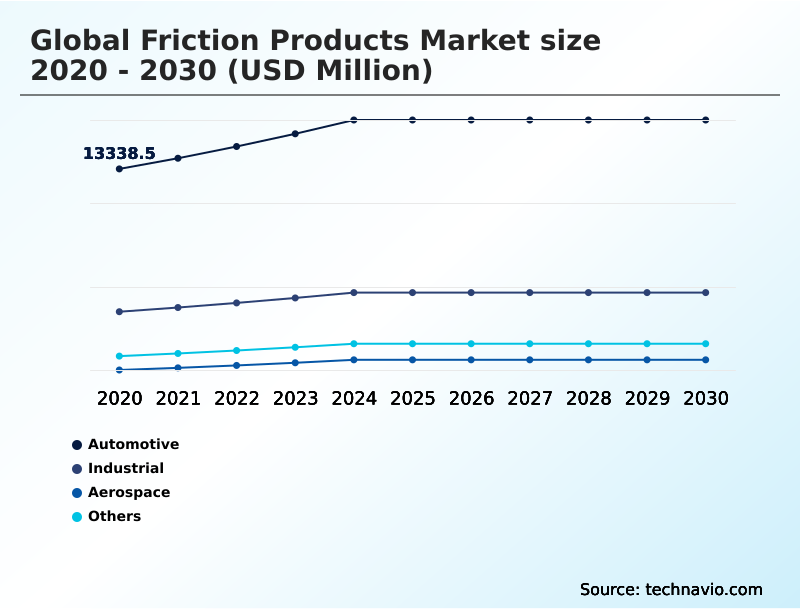

- By Product - Automotive segment was valued at USD 16.08 billion in 2024

- By Material Type - Organic segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 16.77 billion

- Market Future Opportunities: USD 10.13 billion

- CAGR from 2025 to 2030 : 5.9%

Market Summary

- The friction products market is integral to safety and operational efficiency across the automotive, aerospace, and industrial sectors. Growth is propelled by an aging global vehicle fleet, which sustains robust demand for aftermarket components, and the continuous procurement of new aircraft requiring advanced braking technologies.

- A primary trend involves the shift toward lightweight and eco-friendly friction materials, including ceramic and non-asbestos organic formulations, to meet stringent environmental regulations and improve vehicle fuel efficiency. Innovations in material science are enhancing durability, thermal stability, and performance, addressing the demands of high-performance vehicles and electric powertrains with regenerative braking systems.

- For instance, a logistics company can optimize its fleet's total cost of ownership by adopting advanced brake pads that extend service intervals, reducing vehicle downtime and maintenance expenses. However, the market faces challenges from the proliferation of counterfeit products, which threaten revenue streams and brand integrity, alongside slowdowns in manufacturing operations that can disrupt supply chains.

What will be the Size of the Friction Products Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Friction Products Market Segmented?

The friction products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Automotive

- Industrial

- Aerospace

- Others

- Material type

- Organic

- Metallic

- Ceramic

- Distribution channel

- Offline

- Online

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Product Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive segment remains a critical application area, driven by the need for effective motion control systems in passenger and commercial vehicles.

Demand is reinforced by stringent safety regulations mandating advanced technologies and a robust aftermarket serving an aging global fleet.

The transition to electric and hybrid vehicles introduces new requirements for specialized friction materials that can withstand the unique thermal and mechanical stresses of regenerative braking compatibility.

Consequently, there is a focus on brake pad formulations and lightweight braking materials to enhance performance.

These advancements are critical as the automotive sector contributes over 45% of the market's incremental growth, compelling manufacturers to innovate with durable friction components that meet both performance and regulatory standards.

The Automotive segment was valued at USD 16.08 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Friction Products Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is characterized by diverse regional growth dynamics. APAC is set to dominate, projected to account for over 45% of the market's incremental growth, driven by its expanding automotive manufacturing base and industrialization.

The region's market is expanding at a rate approximately 1% higher than Europe, which remains a key market due to its stringent regulatory standards and focus on aerospace braking technology and advanced material adoption.

North America is driven by a large vehicle parc and a strong aftermarket. The region's focus on high-performance clutches and commercial vehicle braking solutions ensures steady demand.

In contrast, emerging markets in South America and the Middle East and Africa show potential, fueled by infrastructure development and a growing need for industrial brake linings.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the friction products market requires a deep understanding of material science and application-specific performance. Evaluating the high temperature stability in ceramic brake pads is critical for luxury and performance vehicle segments, where minimizing brake fade is paramount.

- Concurrently, manufacturers must address the impact of regenerative braking on friction material, a key challenge in the rapidly expanding electric vehicle sector. This has accelerated R&D into lightweight materials for automotive brake systems, which contributes to overall vehicle efficiency. A major industry-wide effort involves developing copper-free materials for environmental regulations, forcing a re-evaluation of traditional formulations.

- Comparative analysis of the wear characteristics of metallic vs. organic pads continues to inform choices for both OEM and aftermarket segments. For heavy-duty applications, friction product solutions for industrial machinery must ensure reliability under extreme loads, while advanced friction materials for aerospace applications must meet unparalleled safety standards.

- In the consumer-facing automotive sector, noise reduction techniques in automotive braking are a key differentiator. The push for sustainability is promoting eco-friendly friction materials for commercial vehicles, while durability testing for heavy-duty brake linings ensures operational safety in logistics. The performance of carbon-ceramic brakes in sports cars sets a benchmark, highlighting the importance of friction coefficient consistency under varying loads.

- For the aftermarket, balancing brake pad quality vs. OEM specifications is a constant focus. Other niche areas include sintered metal brake pads for motorcycles and improving wet braking performance of NAO pads. The role of phenolic resins in brake pad formulation remains crucial for structural integrity, alongside innovations in thermal management in high-performance braking.

- Finally, reducing brake dust from metallic pads and advancements in powder metallurgy for friction parts are key to meeting both consumer expectations and environmental mandates, including challenges in braking systems for electric aircraft.

What are the key market drivers leading to the rise in the adoption of Friction Products Industry?

- A key market driver is the aging global fleet of automobiles, which fuels consistent demand for aftermarket friction products.

- Key drivers propelling the market include the aging global vehicle fleet and increasing aircraft procurement, which sustain demand for both aftermarket brake components and advanced original equipment friction products.

- The continuous need for brake system maintenance fuels a steady revenue stream. Innovations in brake lining composition are critical, with new formulations improving component lifespan by over 20% in certain applications.

- This drive for longevity and performance is also seen in the development of materials with a stable friction coefficient and high wear resistance.

- For instance, the use of aramid fiber reinforcement in non-asbestos organic materials has resulted in a 15% reduction in warranty claims for some manufacturers, underscoring the business impact of material science advancements.

What are the market trends shaping the Friction Products Industry?

- The development of high-performance adaptive braking systems is an upcoming market trend. This innovation is setting new standards for future automotive braking technology.

- The market is witnessing a significant trend toward the development of high-performance adaptive braking systems and the adoption of lightweight materials. Innovations in brake pad materials and clutch facing technology are central, with a focus on enhancing wet braking performance and brake fade resistance.

- The integration of advanced composites has been shown to improve thermal dissipation by up to 25%, a critical factor for performance vehicles. Furthermore, the push for sustainability is accelerating the development of eco-friendly friction materials and copper-free brake pads.

- These advancements in brake disc metallurgy and powder metallurgy processes are enabling manufacturers to create products with superior durability and reduced environmental impact, meeting both regulatory demands and consumer expectations for quieter, more efficient braking.

What challenges does the Friction Products Industry face during its growth?

- The increasing availability of counterfeit products presents a significant challenge to market growth, impacting revenue and brand reputation for legitimate manufacturers.

- The market grapples with significant challenges, including the proliferation of counterfeit products and slowdowns in manufacturing operations, which disrupt supply chains for automotive friction components and industrial brake linings. The need to comply with evolving regulations for heavy-duty friction materials adds complexity, often increasing production costs.

- The integration of advanced features into motion control systems, such as brake system wear indicators, requires higher R&D investment. For example, ensuring regenerative braking compatibility in new brake pad formulations can extend development timelines by up to 30%.

- Furthermore, managing the thermal stability of components under high-energy braking conditions while controlling noise, vibration, and harshness remains a persistent engineering challenge for railway brake blocks and marine clutch systems.

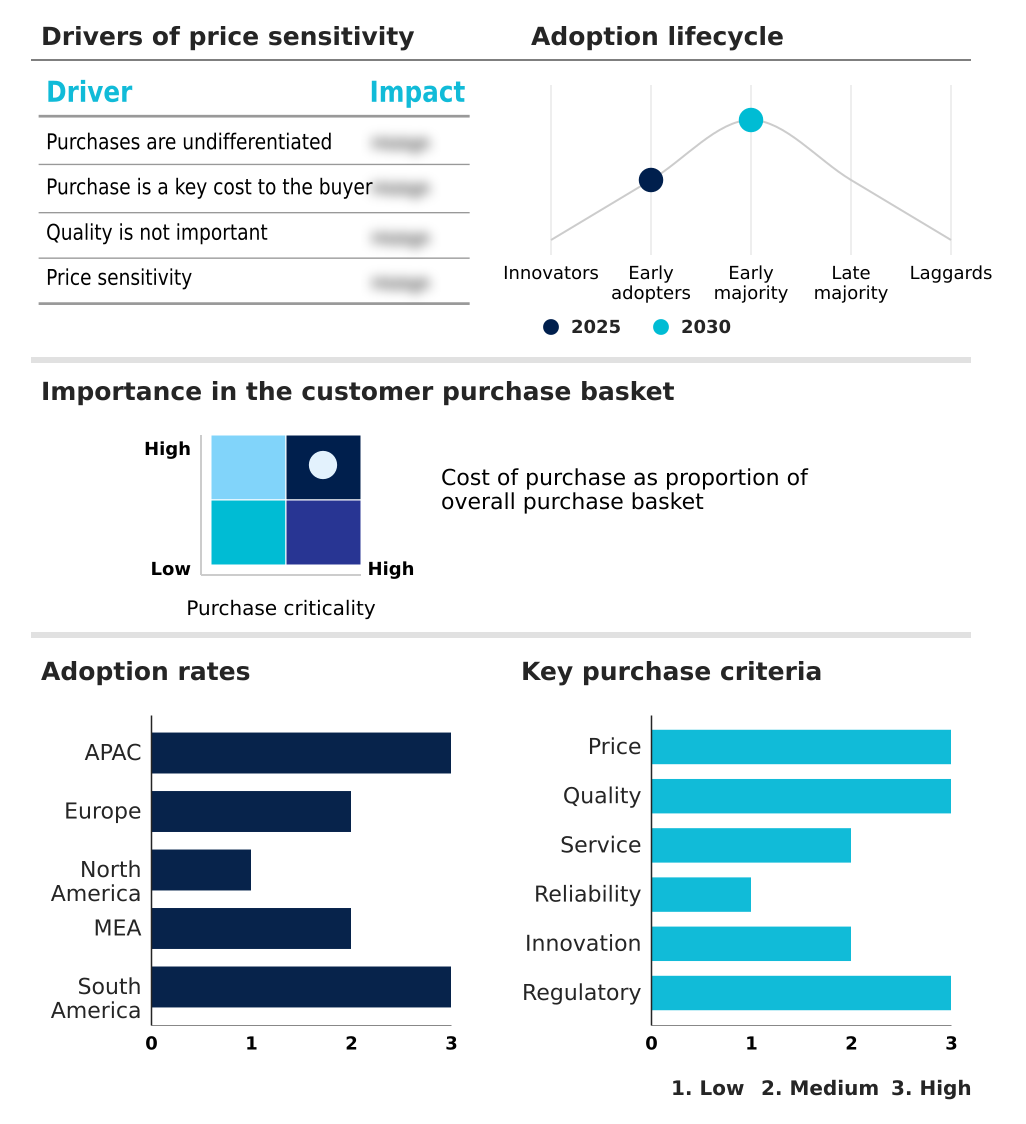

Exclusive Technavio Analysis on Customer Landscape

The friction products market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the friction products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Friction Products Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, friction products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABS Friction Inc. - Key offerings include advanced friction solutions, such as high-performance brake pads and shoes, designed for diverse automotive applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABS Friction Inc.

- AISIN Corp.

- Akebono Brake Industry Co.

- ANAND Group

- ASK Automotive Ltd.

- Brembo Spa

- BREMSKERL Group

- Carlisle Co. Inc.

- EBC Brakes

- General Metals Powder Co.

- Hindustan Composites Ltd.

- Honeywell International Inc.

- Icer Brakes SA

- ITT Inc.

- Knorr Bremse AG

- LUMAG Sp. z o.o.

- Miba AG

- Nisshinbo Holdings Inc.

- Robert Bosch GmbH

- Tenneco Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Friction products market

- In September 2024, Brembo Spa announced the launch of its new 'Greenance Kit,' a line of copper-free brake pads with advanced eco-friendly friction materials, designed to reduce particulate emissions by over 50% for both internal combustion and electric vehicles.

- In November 2024, Robert Bosch GmbH revealed a strategic partnership with a leading European automaker to co-develop a next-generation high-performance adaptive braking system integrated with AI-driven predictive maintenance capabilities for improved safety and reliability.

- In February 2025, ITT Inc. completed its acquisition of a specialized German firm known for its innovations in carbon-ceramic composites, aiming to expand its portfolio of lightweight, high-thermal-stability friction products for the aerospace and high-performance automotive sectors.

- In May 2025, Akebono Brake Industry Co. announced a major expansion of its North American production facility to increase capacity for its advanced electric vehicle brake pads, which feature enhanced noise, vibration, and harshness (NVH) properties.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Friction Products Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.9% |

| Market growth 2026-2030 | USD 10130.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The friction products market is undergoing a significant transformation driven by advancements in material science and evolving end-user requirements. The emphasis is on developing components that offer superior wear resistance and thermal conductivity. For boardroom-level strategy, the push toward regenerative braking compatibility is a critical consideration, directly impacting R&D budgets and future product roadmaps.

- This trend requires a pivot from traditional brake lining composition to advanced materials capable of withstanding different operational stresses. Innovations like high-performance adaptive braking and hydraulic dual-circuit systems are becoming standard. A key performance metric shows that advanced carbon-ceramic composites can improve brake fade resistance by up to 30% in high-demand scenarios compared to conventional materials.

- The industry is also focused on improving wet braking performance and managing noise, vibration, and harshness. The adoption of eco-friendly friction materials, including copper-free brake pads and non-asbestos organic materials, is driven by regulations, while sintered brake pads and clutch facing technology are advancing in specialized applications.

- The underlying science, from aramid fiber reinforcement and phenolic resin binders to brake disc metallurgy and powder metallurgy processes, continues to define the competitive landscape, emphasizing the need for materials with high thermal stability and consistent friction coefficient for high-energy braking scenarios.

What are the Key Data Covered in this Friction Products Market Research and Growth Report?

-

What is the expected growth of the Friction Products Market between 2026 and 2030?

-

USD 10.13 billion, at a CAGR of 5.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Automotive, Industrial, Aerospace, and Others), Material Type (Organic, Metallic, and Ceramic), Distribution Channel (Offline, and Online) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Aging fleet of automobiles, Increasing availability of counterfeit products

-

-

Who are the major players in the Friction Products Market?

-

ABS Friction Inc., AISIN Corp., Akebono Brake Industry Co., ANAND Group, ASK Automotive Ltd., Brembo Spa, BREMSKERL Group, Carlisle Co. Inc., EBC Brakes, General Metals Powder Co., Hindustan Composites Ltd., Honeywell International Inc., Icer Brakes SA, ITT Inc., Knorr Bremse AG, LUMAG Sp. z o.o., Miba AG, Nisshinbo Holdings Inc., Robert Bosch GmbH and Tenneco Inc.

-

Market Research Insights

- Market dynamics are increasingly shaped by the demand for advanced composite brakes and high-performance clutches, particularly in performance vehicle braking and commercial vehicle braking solutions. The integration of brake system wear indicators is becoming standard, improving brake system maintenance protocols.

- This shift toward higher-value original equipment friction products is evident, as their adoption has been shown to reduce component failure rates by up to 25%. Concurrently, the aftermarket brake components segment remains robust, driven by the need for cost-effective yet reliable replacements.

- Suppliers that balance both OE and aftermarket demands are better positioned, especially as innovations tailored for electric vehicle brake pads now account for a growing share of R&D investment, with some advanced formulations reducing wear by 15% in urban driving cycles.

We can help! Our analysts can customize this friction products market research report to meet your requirements.

RIA -

RIA -