Function As A Service Market Size 2024-2028

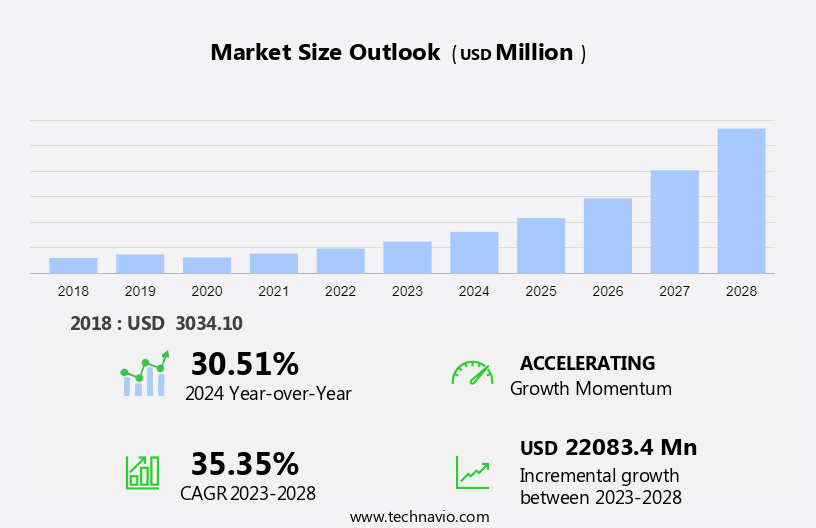

The function as a service market size is estimated to grow by USD 22.08 billion at a CAGR of 35.35% between 2023 and 2028. Serverless computing is an emerging technology that has gained significant traction in the tech industry. One of its key offerings is the ability to build and run applications without the need to manage infrastructure. This results in increased developer productivity and faster development time as the focus shifts from managing servers to writing code. Moreover, the robust dependency on IoT (Internet of Things) devices is driving the adoption of serverless computing. With IoT, data is generated in real-time and needs to be processed and analyzed instantly. Serverless computing provides the flexibility and scalability to handle this data deluge effectively, making it an ideal solution for IoT applications. In summary, serverless computing offers numerous benefits, including faster development time, increased productivity, and effective handling of IoT data, making it a must-have technology for modern-day businesses.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Request Free Sample

Market Dynamics and Customer Landscape

Function-as-a-Service (FaaS) is a deployment model in the cloud computing landscape where the cloud provider runs the code provided by the user, and manages the underlying infrastructure. This model is based on the serverless computing concept, where the cloud provider manages the servers and the infrastructure, allowing users to focus on writing and deploying code. FaaS is available in various deployment models, including public, private, and hybrid cloud. Large enterprises and medium enterprises across industries such as IT & telecom, healthcare, manufacturing, and technology are increasingly adopting FaaS for its agility, cost-effectiveness, and ease of deployment. Cloud providers offer various Hybrid Cloud Deployment models for FaaS, allowing users to maintain control over their data security while leveraging the benefits of cloud infrastructure. FaaS is often used in conjunction with Microservices and Infrastructure-as-a-Service (IaaS) to build and deploy complex applications. Hybrid infrastructure services, such as Colocation, are also used to extend on-premises infrastructure to the cloud for seamless integration with FaaS. With IT investments in cloud computing continuing to grow, FaaS is poised to play a significant role in the future of application development and deployment. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The growing shift to serverless computing is notably driving market growth. The market is experiencing significant growth due to the increasing adoption of serverless computing and the flexibility it offers to businesses. This shift towards cloud-based solutions enables organizations to scale their operations efficiently and manage multiple platforms with ease. Large enterprises are increasingly investing in FaaS to automate various tasks and optimize small services, thereby enhancing productivity and overall business performance. The trend towards serverless architecture is particularly prevalent among large corporations, driven by the demand for cloud automation and the ability to handle large volumes of data. This market is expected to continue its growth trajectory during the forecast period as more businesses recognize the benefits of FaaS in terms of scalability, cost savings, and agility. Thus, such factors are driving the growth of the market during the forecast period.

Significant Market Trends

The increasing adoption of cloud computing services is the key trend in the market. Businesses are increasingly shifting towards cloud adoption, seeking the advantages of both on-premises and off-premises services through a hybrid approach. Small and medium enterprises (SMEs) are particularly embracing cloud computing due to its cost-effective nature, which eliminates the need for upfront infrastructure setup costs and offers on-demand IT services. Hybrid cloud services cater to the requirements of businesses by providing improved workload management, enhanced security and compliance, and seamless integration across development teams. Furthermore, this solution offers the flexibility to transition between on-premises and cloud environments or even between different clouds. The scalability of hybrid cloud services enables businesses to gain a competitive edge in the market. This trend is expected to continue, contributing significantly to the expansion of the hybrid cloud services market. Thus, such trends will shape the growth of the market during the forecast period.

Major Market Challenge

The increase in cyberattacks is the major challenge that affects the growth of the market. Cloud Function-as-a-Service (FaaS) market is witnessing significant growth due to its ability to enhance business agility and efficiency, enabling on-demand resource utilization and reducing operational costs. However, the increasing volume of corporate data migration to the cloud and the resulting digital transformation initiatives expose businesses to an escalating threat landscape. Cyberattacks, such as Specter and Meltdown, cloud malware, account or service takeovers, and man-made attacks, pose significant risks to corporate data. These threats can lead to substantial losses and potential business closures. Consequently, the increasing prevalence of cyberattacks may hinder the expansion of the global FaaS market during the forecast period. Despite these challenges, FaaS providers are continually investing in advanced security measures to mitigate risks and ensure data protection. Hence, the above factors will impede the growth of the market during the forecast period.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amazon.com Inc. - The company offers Function as a Service such as AWS Fargate and AWS Lambda.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphabet Inc.

- Amazon.com Inc.

- Bronze.io Dba Iron.io Inc.

- Cloudflare Inc.

- Ekinops SA

- Flowgear

- Infosys Ltd.

- International Business Machines Corp.

- Manjrasoft Pty Ltd.

- Microsoft Corp.

- Netlify Inc.

- Oracle Corp.

- TIBCO Software Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

By Deployment

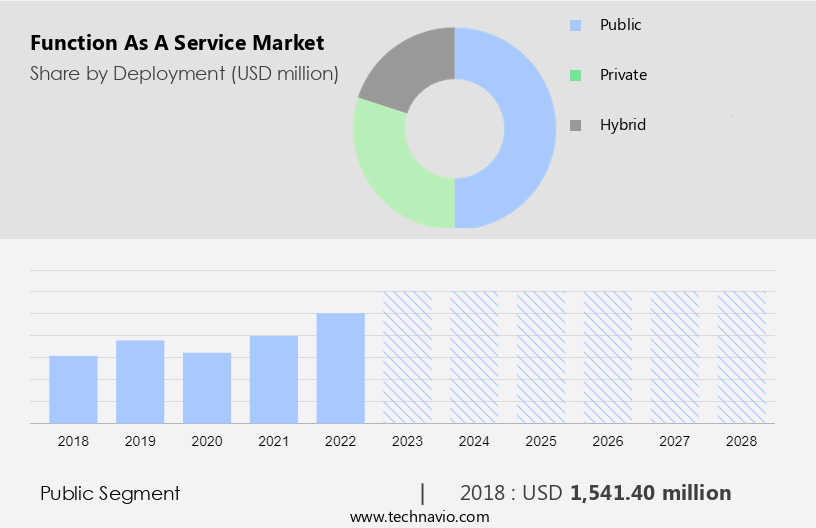

The public segment is estimated to witness significant growth during the forecast period. The market encompasses deployment models, including public, private, and hybrid clouds, which cater to the varying needs of businesses. In 2023, the public cloud segment held the largest market share due to its numerous benefits, such as faster deployment, scalability, and business agility. DevOps solutions, which are increasingly being adopted by businesses, play a significant role in this trend.

Get a glance at the market share of various regions Download the PDF Sample

The public segment accounted for USD 1.54 billion in 2018. By using these tools, companies can streamline their operations, reduce costs, and ensure regulatory compliance. The shift towards serverless computing model, microservices, and cloud providers' offerings, such as Infrastructure-as-a-Service (IaaS), colocation and hosting, and hybrid cloud deployment, is driving the growth of the FaaS market. Industries like IT & telecom, healthcare, manufacturing, media & entertainment, e-commerce, and communication service providers are investing heavily in FaaS technology. Telecom companies are moving towards operator-centric and developer-centric models, while hyper-scale cloud providers are focusing on edge computing and 5G technology to expand their offerings. Additionally, emerging technologies like IoT, blockchain, artificial intelligence, and autonomous driving are expected to further fuel the growth of the FaaS market. Overall, the FaaS market is poised for significant growth due to its ability to provide cost savings, flexibility, and improved operational efficiency.

Regional Analysis

For more insights on the market share of various regions Download PDF Sample now!

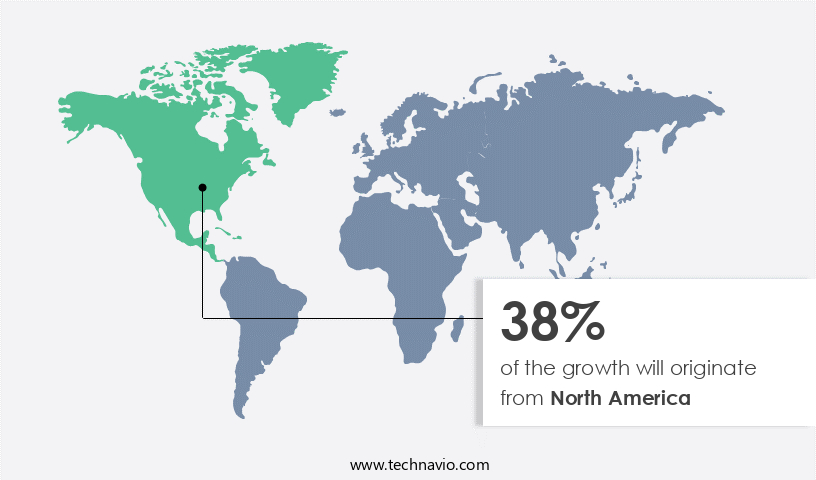

North America is estimated to contribute 38% to the growth of the global market during the market forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market refers to the deployment of hosted services in the cloud computing landscape, where technology providers manage the infrastructure and handle the execution of code in response to events or requests. This deployment model, a part of serverless computing, enables businesses to focus on their core competencies without managing the underlying infrastructure. FaaS is available on public, private, and hybrid cloud platforms, catering to large enterprises in IT & telecom, healthcare, manufacturing, media & entertainment, e-commerce, and other industries. Operator-centric and developer-centric businesses alike benefit from this model's cost-effective expenses and on-demand access to resources. Cloud providers, including hyper-scale and communication service providers, offer FaaS as part of their Infrastructure-as-a-Service (IaaS) and Platform-as-a-Service (PaaS) offerings. FaaS is increasingly adopted for emerging technologies like 5G technology, autonomous driving, IoT, blockchain, artificial intelligence, and edge computing, enhancing business agility and driving digital transformation. Colocation and hosting facilities further support the FaaS market's growth, ensuring data security and compliance for various industries.

Segment Overview

The market report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment Outlook

- Public

- Private

- Hybrid

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- South America

- Argentina

- Brazil

- Chile

- North America

You may also be interested in:

- Middleware as a Service (MWAAS) Market Analysis North America, Europe, APAC, South America, Middle East and Africa - US, China, Japan, UK, Germany - Size and Forecast

- Cloud Managed Services Market Analysis North America, Europe, APAC, South America, Middle East and Africa - US, China, Germany, Japan, UK - Size and Forecast

- Network Function Virtualization (Nfv) Market Analysis North America, Europe, APAC, Middle East and Africa, South America - US, China, Germany, Canada, UK - Size and Forecast

Market Analyst Overview

Function-as-a-Service (FaaS) is a deployment model under the serverless computing umbrella, where technology providers run and manage the underlying infrastructure and developers focus on writing and deploying code. FaaS allows businesses to pay only for the resources they use, making it an economical choice for IT investments. This deployment model is gaining popularity in various industries, including large enterprises in IT & telecom, healthcare, manufacturing, media & entertainment, e-commerce, and more. FaaS is available on public, private, and hybrid clouds, catering to operator-centric and developer-centric needs. Cloud providers offer FaaS as part of their Infrastructure-as-a-Service (IaaS) offerings, enabling businesses to scale their operations with ease. Hybrid Cloud Deployment, which combines public and private cloud resources, is particularly beneficial for data security and regulatory compliance. FaaS is also driving innovation in emerging technologies like 5G technology, autonomous driving, IoT, blockchain, artificial intelligence, and edge computing. By allowing developers to focus on writing code without worrying about infrastructure, FaaS fosters business agility and faster time-to-market for new applications and services. Cloud providers like telecom companies and hyper-scale cloud providers are investing heavily in FaaS to meet the growing demand for flexible, cost-effective, and secure IT solutions. The future of FaaS looks promising, with its potential to revolutionize the way businesses deploy and manage applications and services.

|

Industry Scope |

|

|

Report Coverage |

Details |

|

Page number |

141 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 35.35% |

|

Market growth 2024-2028 |

USD 22.08 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

30.51 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 38% |

|

Key countries |

US, China, Germany, Italy, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Alphabet Inc., Amazon.com Inc., Bronze.io Dba Iron.io Inc., Cloudflare Inc., Ekinops SA, Flowgear, Infosys Ltd., International Business Machines Corp., Manjrasoft Pty Ltd., Microsoft Corp., Netlify Inc., Oracle Corp., and TIBCO Software Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behavior

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

RIA -

RIA -