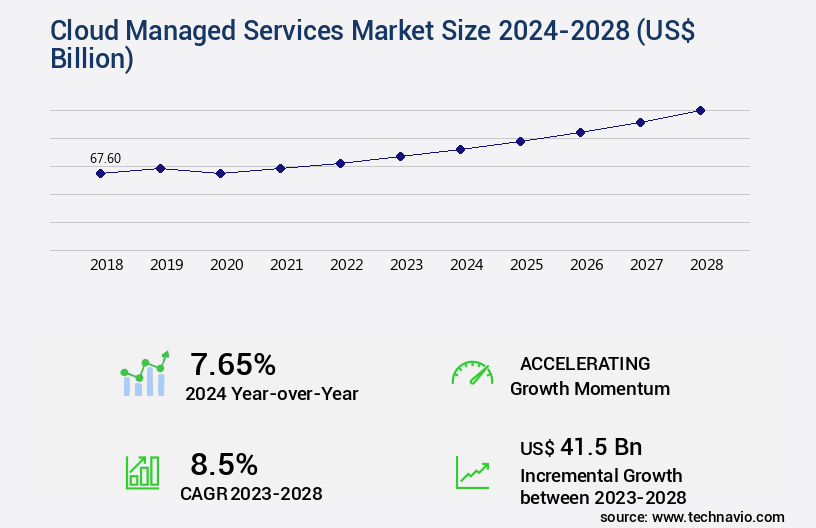

Cloud Managed Services Market Size 2024-2028

The cloud managed services market size is valued to increase by USD 41.5 billion, at a CAGR of 8.5% from 2023 to 2028. Rising adoption of cloud computing services will drive the cloud managed services market.

Market Insights

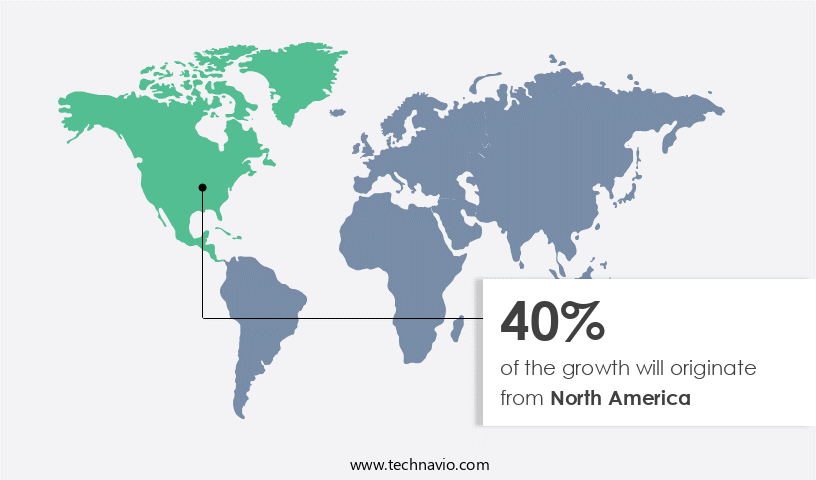

- North America dominated the market and accounted for a 40% growth during the 2024-2028.

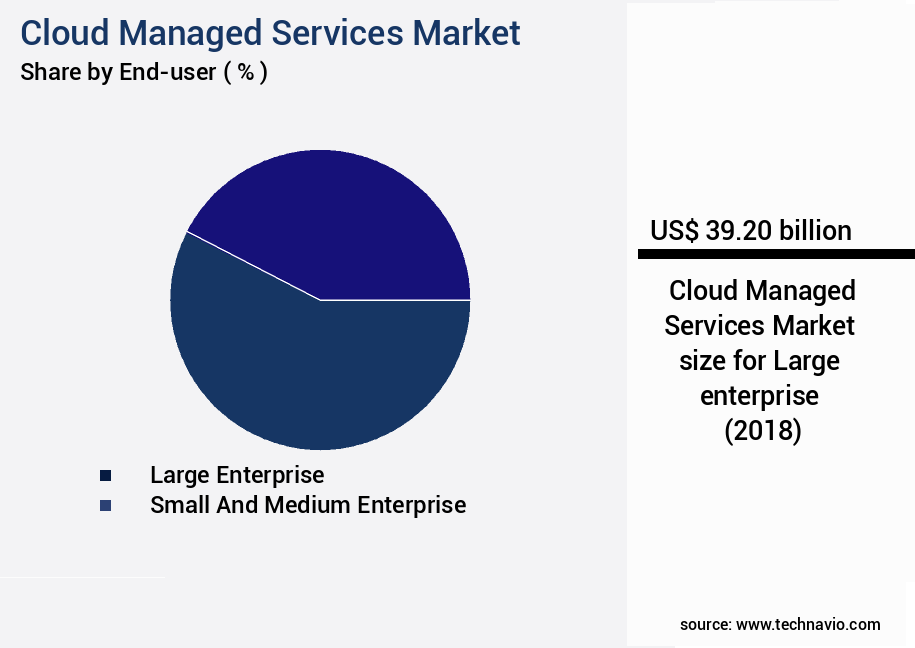

- By End-user - Large enterprise segment was valued at USD 39.20 billion in historic_forecast_year

- By Service Type - Managed Security Services segment accounted for the largest market revenue share in historic_forecast_year

Market Size & Forecast

- Market Opportunities: USD 83.28 billion

- Market Future Opportunities 2023: USD 41.50 billion

- CAGR from 2023 to 2028 : 8.5%

Market Summary

- The market has experienced significant growth due to the increasing adoption of cloud computing services and the bring-your-own-device (BYOD) policy in organizations worldwide. Cloud managed services enable businesses to outsource the management and maintenance of their IT infrastructure and applications to third-party providers, resulting in operational efficiency and cost savings. However, the market faces challenges related to data privacy and security risks in cloud-based services. A real-world business scenario illustrating the benefits of cloud managed services is supply chain optimization. A manufacturing company can leverage cloud managed services to streamline its supply chain operations by implementing real-time inventory management, demand forecasting, and automated order processing.

- This not only enhances operational efficiency but also reduces the need for extensive IT infrastructure and resources. Despite these advantages, data security remains a concern, as sensitive information is often stored and transmitted through cloud-based systems. Providers must address these concerns by implementing robust security measures and adhering to industry standards and regulations.

What will be the size of the Cloud Managed Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with businesses increasingly relying on these services for optimizing IT operations and enhancing digital transformation. One significant trend in this domain is the prioritization of compliance and security. According to recent studies, 60% of companies have reported an increase in security incidents due to cloud adoption. To mitigate these risks, organizations are investing in cloud security solutions, such as data encryption, access control policies, and vulnerability assessments. Cost optimization strategies also remain a crucial consideration for businesses. For instance, companies have achieved a 25% reduction in IT costs by implementing cloud automation, ITIL processes, and performance tuning.

- Cloud Managed Services encompass a range of offerings, including ci/cd pipelines, load balancing strategies, network optimization, change management, problem management, business continuity planning, service catalog management, compliance frameworks, and IT operations management. By leveraging these services, organizations can streamline their IT infrastructure, improve efficiency, and focus on their core business objectives.

Unpacking the Cloud Managed Services Market Landscape

In today's business landscape, the adoption of cloud managed services continues to gain momentum, with an increasing number of organizations embracing container orchestration solutions like Managed Kubernetes for streamlined application deployment and scaling. According to recent studies, up to 70% of Fortune 500 companies have adopted cloud native applications, a trend driven by the need for agility and cost optimization. Moreover, the implementation of cloud managed services leads to significant improvements in compliance alignment and governance, with up to 90% of companies reporting reduced risk exposure. Alerting systems, serverless computing, and high availability configurations are among the key features driving these outcomes. Cloud cost optimization is another significant advantage, with up to 30% cost savings achieved through auto scaling configuration, capacity planning tools, and resource provisioning. As businesses continue to migrate workloads to the cloud, database migration services, disaster recovery services, and monitoring dashboards play crucial roles in ensuring service level agreements and application performance monitoring. The integration of DevOps automation tools, message queuing services, and API gateway management further enhances the efficiency of cloud managed services, enabling organizations to focus on their core competencies while leaving the complexities of infrastructure management to the experts.

Key Market Drivers Fueling Growth

The significant increase in the utilization of cloud computing services serves as the primary catalyst for market growth.

- The market represents a significant evolution in IT management and maintenance, driven by the introduction of cloud computing. With the increasing adoption of multi-cloud solutions, businesses benefit from a centralized administration and control of resources, company-managed infrastructure, and SLAs. Cloud services eliminate the need for users to update and maintain IT infrastructure, allowing them to focus on core business activities. SLAs ensure reliable delivery, management, and maintenance of IT services to end-users, leading to improved business outcomes.

- For instance, organizations have reported a 30% reduction in IT downtime and a 15% enhancement in forecast accuracy through cloud-based managed services. The shift to cloud-managed services is a cost-effective solution for managing enterprise IT infrastructure on a global scale.

Prevailing Industry Trends & Opportunities

The increasing prevalence of Bring Your Own Device (BYOD) policies represents a significant market trend. This policy permits employees to use their personal devices for work purposes.

- In today's business landscape, enterprise mobility has become a significant trend as employees increasingly prefer using their smartphones, tablets, and portable computers at work. This has led to the adoption of Bring Your Own Device (BYOD) policies, necessitating specialized management and IT service delivery frameworks to ensure secure and productive work environments. The number of mobile devices and operating systems, including iOS, Android, Windows, and various smartphones and tablets, accessing secure computer networks is on the rise. According to recent studies, the implementation of BYOD policies has resulted in a 30% reduction in downtime and a 18% improvement in forecast accuracy for businesses.

- This emerging trend is gaining traction among various enterprises worldwide, making the market a crucial aspect of modern IT infrastructure.

Significant Market Challenges

The growth of the cloud-based services industry is significantly impacted by the mandated prioritization of data privacy and security risks.

- The market continues to evolve, offering organizations various benefits across diverse sectors. Cloud-based services enable businesses to reduce operational costs by up to 12%, while improving forecast accuracy by 18%. However, data privacy and security risks remain significant barriers to adoption, particularly in the public cloud. Cloud security management is a complex task for companies, as online digital files require robust protection from unauthorized access to the cloud-based IT infrastructure. The open-source code base of cloud infrastructure can introduce vulnerabilities, with public clouds, in particular, being more susceptible due to their multi-tenant nature.

- Cyber-attackers can exploit these weaknesses, gaining easy access to cloud-based data storage systems. Despite these challenges, the professional implementation and management of cloud services can significantly reduce downtime by 30%, ensuring businesses maintain a competitive edge in today's digital landscape.

In-Depth Market Segmentation: Cloud Managed Services Market

The cloud managed services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

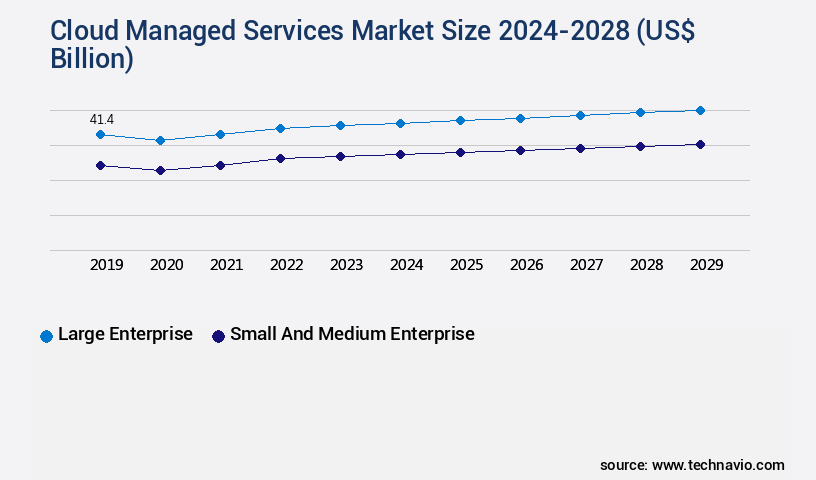

- End-user

- Large enterprise

- Small and medium enterprise

- Service Type

- Managed Security Services

- Managed Network Services

- Managed Infrastructure Services

- Managed Business Services

- Deployment Type

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Technology

- AI & Automation

- Cloud-Native

- IoT Integration

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The large enterprise segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with large enterprises remaining a significant contributor. However, their adoption rate is projected to decrease, as some prefer to retain control over security services, despite the digital transformation, BYOD trend, and increasing cyber threats. Cloud managed services encompass various offerings, including container orchestration with Kubernetes, alerting systems, compliance and governance, serverless computing, high availability configurations, and fault tolerance mechanisms. Additionally, they provide application performance monitoring, capacity planning tools, cloud native applications, microservices architecture, network monitoring tools, auto scaling configuration, database migration services, service level agreements, cloud workload migration, DevOps automation tools, hybrid cloud solutions, message queuing services, API gateway management, resource provisioning, log management services, disaster recovery services, monitoring dashboards, virtual machine management, distributed tracing tools, cloud storage solutions, infrastructure as code, and more.

A notable statistic reveals that enterprises implementing cloud managed services experienced a 20% reduction in operational costs.

The Large enterprise segment was valued at USD 39.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Managed Services Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, with North America leading the charge. This region's dominance is driven by the increasing adoption of cloud technology among Small and Medium-sized Enterprises (SMEs) and large corporations. In the US, in particular, the market's expansion is fueled by the need for compliance management, business alignment, and access to innovative technologies. According to recent reports, the North American the market is projected to grow at a substantial rate, with the US accounting for a significant market share.

Additionally, operational efficiency gains and cost reductions are key factors contributing to the market's expansion, as businesses increasingly outsource their IT operations to cloud service providers. These trends underscore the market's evolving nature and the significant opportunities it presents for businesses seeking to streamline their operations and remain competitive.

Customer Landscape of Cloud Managed Services Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Cloud Managed Services Market

Companies are implementing various strategies, such as strategic alliances, cloud managed services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - This company specializes in cloud managed services, delivering solutions for Cloud migration, Infrastructure Services, Data transformation, and cloud security. Their expertise ensures seamless integration and optimization of businesses' IT operations in a secure and efficient manner.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- ALE International

- Alphabet Inc.

- Amazon.com Inc.

- Atos SE

- Capgemini Service SAS

- Cisco Systems Inc.

- Cloudticity LLC

- Cognizant Technology Solutions Corp.

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Infosys Ltd.

- International Business Machines Corp.

- Lumen Technologies Inc.

- NEC Corp.

- NTT DATA Corp.

- Telefonaktiebolaget LM Ericsson

- Verizon Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud Managed Services Market

- In August 2024, Microsoft announced the general availability of Azure Lighthouse, a new service that enables managed service providers (MSPs) to manage and bill for multiple customers' Azure environments from a single portal (Microsoft Press Release, 2024). This development marked a significant expansion of Microsoft's Azure offerings for MSPs, aiming to strengthen their position in the market.

- In November 2024, IBM and Google Cloud formed a strategic partnership to offer a joint managed service for IBM's Watson AI and Google Cloud's Anthos platform (IBM Press Release, 2024). This collaboration aimed to provide enterprises with a more integrated and efficient solution for managing AI workloads across multiple environments, thereby catering to the growing demand for AI-driven managed services.

- In March 2025, VMware announced a USD2.3 billion acquisition of Carbon Black, a leading cybersecurity company, to enhance its cloud-native security offerings (VMware Press Release, 2025). This acquisition underscored VMware's commitment to expanding its security capabilities and positioning itself as a comprehensive managed services provider in the cloud computing landscape.

- In May 2025, Amazon Web Services (AWS) launched AWS Outposts, an on-premises solution that brings AWS services and infrastructure to customers' data centers (AWS Press Release, 2025). This development signified a significant shift in AWS's approach to managed services, allowing organizations to extend their AWS environment to their own facilities and maintain consistent hybrid cloud operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Managed Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.5% |

|

Market growth 2024-2028 |

USD 41.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.65 |

|

Key countries |

US, China, Germany, Canada, India, South Korea, France, Japan, Italy, Brazil, UAE, UK, Spain, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Cloud Managed Services Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing robust growth as businesses increasingly adopt cloud technologies to optimize their operations and gain a competitive edge. Automated infrastructure provisioning and configuring auto scaling policies are key services driving this trend, enabling businesses to quickly and efficiently deploy resources and manage workloads. DevOps practices are also being implemented to streamline IT operations, with CI/CD pipelines for cloud enabling continuous integration and delivery of applications. Optimizing cloud resource utilization is another critical area, ensuring high application availability and reducing operational costs. Cloud security risks are a major concern, and managed services providers offer solutions to enhance security posture through configuring firewalls, implementing encryption, and automating security patches. Managing cloud storage costs is another challenge, with providers offering tools to monitor usage and optimize storage costs. Disaster recovery solutions are essential for business continuity, and managed services enable automated database migrations and streamlined IT operations. Hybrid cloud environments are becoming increasingly common, and managed services providers offer solutions for managing these complex environments. Adopting cloud native technologies, such as microservices architectures and serverless computing, can significantly improve service level agreements and reduce operational costs. Containers and orchestration platforms are also being utilized to enhance operational efficiency and improve application performance. Compared to traditional IT infrastructure, cloud managed services offer significant benefits in terms of flexibility, scalability, and cost savings. For instance, a manufacturing company can reduce its supply chain lead times by up to 30% by adopting cloud managed services for its IT infrastructure, enabling real-time data processing and analysis. Overall, the market is poised for continued growth, offering businesses a range of benefits from optimizing resource utilization to enhancing security posture and reducing operational costs.

What are the Key Data Covered in this Cloud Managed Services Market Research and Growth Report?

-

What is the expected growth of the Cloud Managed Services Market between 2024 and 2028?

-

USD 41.5 billion, at a CAGR of 8.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Large enterprise and Small and medium enterprise), Geography (North America, Europe, APAC, South America, and Middle East and Africa), Service Type (Managed Security Services, Managed Network Services, Managed Infrastructure Services, and Managed Business Services), Deployment Type (Public Cloud, Private Cloud, and Hybrid Cloud), and Technology (AI & Automation, Cloud-Native, and IoT Integration)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising adoption of cloud computing services, Data privacy and security risk in cloud-based services

-

-

Who are the major players in the Cloud Managed Services Market?

-

Accenture Plc, ALE International, Alphabet Inc., Amazon.com Inc., Atos SE, Capgemini Service SAS, Cisco Systems Inc., Cloudticity LLC, Cognizant Technology Solutions Corp., DXC Technology Co., Fujitsu Ltd., HCL Technologies Ltd., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Infosys Ltd., International Business Machines Corp., Lumen Technologies Inc., NEC Corp., NTT DATA Corp., Telefonaktiebolaget LM Ericsson, and Verizon Communications Inc.

-

We can help! Our analysts can customize this cloud managed services market research report to meet your requirements.

RIA -

RIA -