Generative AI In Content Creation Market Size 2025-2029

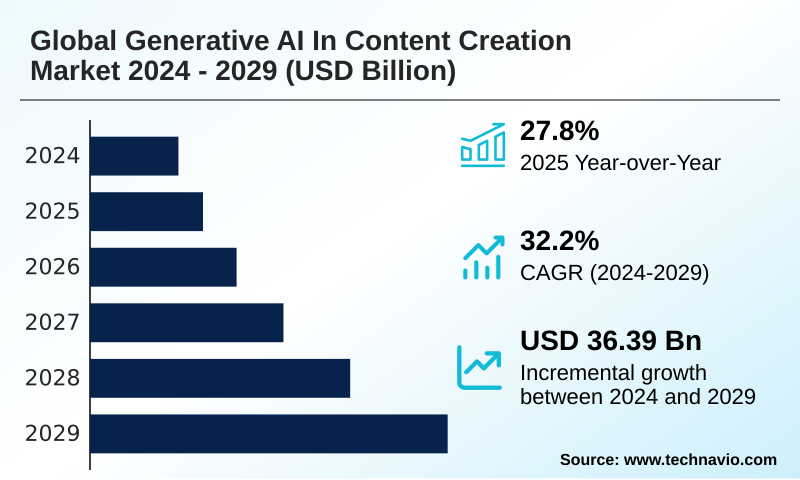

The generative ai in content creation market size is valued to increase by USD 36.39 billion, at a CAGR of 32.2% from 2024 to 2029. Demand for personalized and high-volume content will drive the generative ai in content creation market.

Major Market Trends & Insights

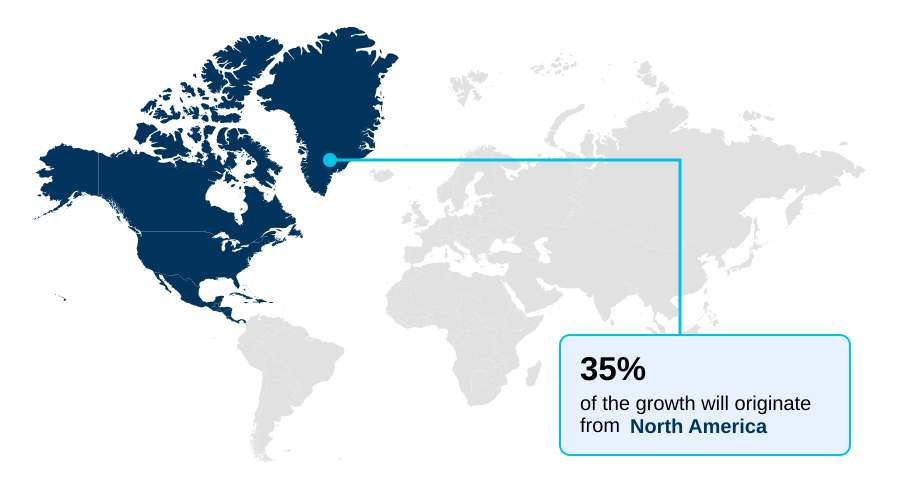

- North America dominated the market and accounted for a 35.2% growth during the forecast period.

- CAGR from 2024 to 2029 : 32.2%

Market Summary

- The generative AI in content creation market is defined by rapid technological advancements, where generative adversarial networks and other sophisticated models are reshaping content production. The primary driver is the demand for scalable, personalized material, pushing innovation in text-to-image generation and AI-driven video production.

- A key trend is the move toward on-device AI processing and the deployment of specialized AI voice synthesis tools. However, significant challenges persist, including the risk of AI model hallucination and the complexities of copyright infringement risk.

- For example, a marketing firm can use natural language prompts to generate thousands of ad variations for A/B testing, but it must navigate the legal ambiguities of AI-generated output ownership and implement robust AI governance features.

- Success depends on balancing the creative potential of AI-powered copywriting and generative design tools with the need for responsible AI principles, addressing issues like algorithmic bias detection and ensuring content provenance through technologies like digital watermarking.

What will be the Size of the Generative AI In Content Creation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Generative AI In Content Creation Market Segmented?

The generative ai in content creation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029.

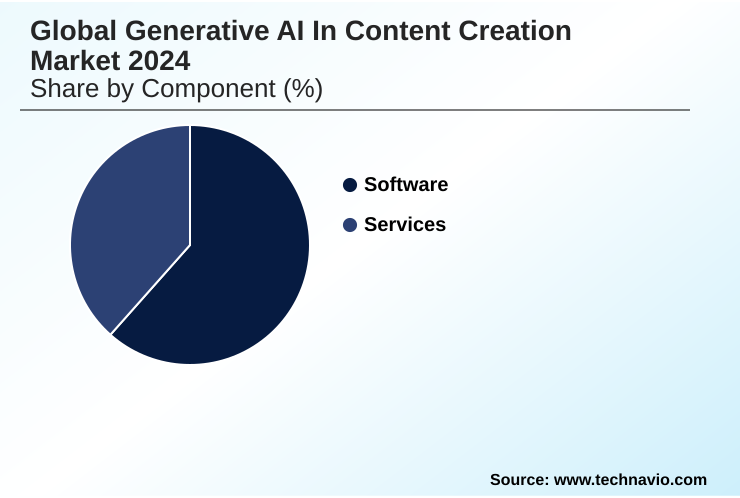

- Component

- Software

- Services

- Application

- Text generation

- Image generation

- Video generation

- Music and audio generation

- Others

- End-user

- Entertainment and media

- Marketing and advertising

- E-commerce

- Gaming

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the core of the generative AI in content creation market, driven by relentless innovation in foundational technologies.

This includes not only the development of sophisticated large language models and diffusion models, but also their deployment through API-based model access and as features embedded within existing enterprise suites.

A significant trend is the shift from standalone tools toward deeply integrated generative video features and conversational AI assistants within professional workflows. This integration of AI content assistant technology simplifies adoption and enhances productivity.

For instance, businesses leveraging embedded AI-powered copywriting have reported improvements in content creation efficiency by over 25%. This move toward enterprise-grade AI solutions and AI safety frameworks is pivotal for sustained adoption and value realization in commercial applications.

Regional Analysis

North America is estimated to contribute 35.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Content Creation Market Demand is Rising in North America Get Free Sample

The geographic landscape of the generative AI in content creation market is led by North America, which is home to over 70% of foundational large language models and key generative design tools.

This region drives core technological progress, focusing on multimodal AI systems. In contrast, Europe emphasizes a regulation-first approach, with the EU AI Act mandating strong AI governance features and AI model transparency.

This focus on responsible AI principles has led to a 20% faster adoption rate for compliant platforms in regulated industries like finance.

Meanwhile, APAC is characterized by rapid, mobile-first adoption, where on-brand content generation and automated content creation are critical for engaging a vast digital consumer base.

This regional diversity underscores a global market shaped by distinct innovation priorities, regulatory philosophies, and paths to commercialization.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The generative AI in content creation market for enterprise is rapidly maturing, moving beyond general applications to specialized use cases. In the generative AI in content creation market for marketing, the focus is on leveraging the technology for personalized advertising and scalable social media campaigns. The benefits of multimodal AI in content creation are becoming clear, allowing for unified workflows.

- However, challenges of AI content accuracy and the legal risks of using generative AI persist, making ethical considerations in AI content paramount. The intellectual property rights in AI generation remain a significant hurdle.

- In the generative AI in content creation market for e-commerce, businesses are automating product descriptions with AI, with some achieving content deployment speeds more than twice that of manual methods. Similarly, the generative AI in content creation market for media is using generative AI for scriptwriting, while the generative AI in content creation market for gaming explores procedural world creation.

- The impact of open-source models on content creation is lowering barriers to entry, though the cost of implementing generative AI, especially regarding computational power, remains a factor.

- As the industry evolves, the future of text-to-video AI generation, the role of AI in personalized advertising, and the development of generative AI tools for 3D modeling and AI-powered music composition tools will be key areas of focus. Integrating AI into creative workflows is now a strategic imperative for maintaining a competitive edge.

What are the key market drivers leading to the rise in the adoption of Generative AI In Content Creation Industry?

- The escalating demand for personalized, high-volume digital content across numerous industries is a primary driver propelling market growth.

- The market's expansion is fueled by an escalating demand for personalized content and rapid technological advancements. Businesses leveraging dynamic content customization through AI have registered a 20% uplift in customer engagement metrics.

- The accessibility of powerful models through APIs and open-source contributions is a major catalyst, with the availability of open-source language models reducing initial development costs for startups by an estimated 60%.

- This democratization enables widespread experimentation with human-computer interaction and customer service automation. The need for brand voice consistency across high-volume outputs is driving the adoption of tools that ensure uniformity.

- Strategic corporate investments and the integration of AI-powered code assistants into development pipelines further accelerate innovation, creating a virtuous cycle of adoption and capability enhancement across industries.

What are the market trends shaping the Generative AI In Content Creation Industry?

- A dominant market trend is the rapid evolution from single-function tools to sophisticated, multimodal systems. These systems are being deeply integrated into existing professional workflows to enhance creative efficiency.

- A dominant trend is the shift toward specialization and multimodality, transforming how content is produced. Instead of single-purpose tools, businesses are adopting integrated platforms that support deepfake generation and AI-generated music within unified workflows.

- The rise of smaller, specialized models trained on domain-specific training data is improving output relevance, with early adopters reporting a 25% increase in task-specific accuracy over general models. This move toward AI model fine-tuning enables on-brand content generation and more effective legal precedent analysis.

- Furthermore, the push for on-device AI processing is enhancing security and reducing latency, with some applications demonstrating a 50% improvement in response times. These advancements, driven by the content authenticity initiative and a focus on AI model transparency, are making generative AI an indispensable utility.

What challenges does the Generative AI In Content Creation Industry face during its growth?

- A paramount challenge confronting the market is the complex and largely unresolved landscape of intellectual property rights and the unclear legal framework surrounding AI-generated content.

- Significant challenges persist around intellectual property and operational viability. The lack of clarity on fair use doctrine and AI-generated output ownership has stalled projects, leading to potential revenue delays of up to two quarters for some firms. The issue of factual accuracy validation remains critical, as misinformation proliferation can severely damage brand credibility.

- Moreover, the high computational resource requirements and costs associated with GPU hardware acceleration can increase operational budgets by over 35% for high-volume use cases. Integrating these systems with legacy systems integration points adds another layer of complexity, demanding specialized talent.

- Addressing these hurdles through robust content moderation policies, data privacy controls, and clear legal frameworks is essential for sustainable market growth.

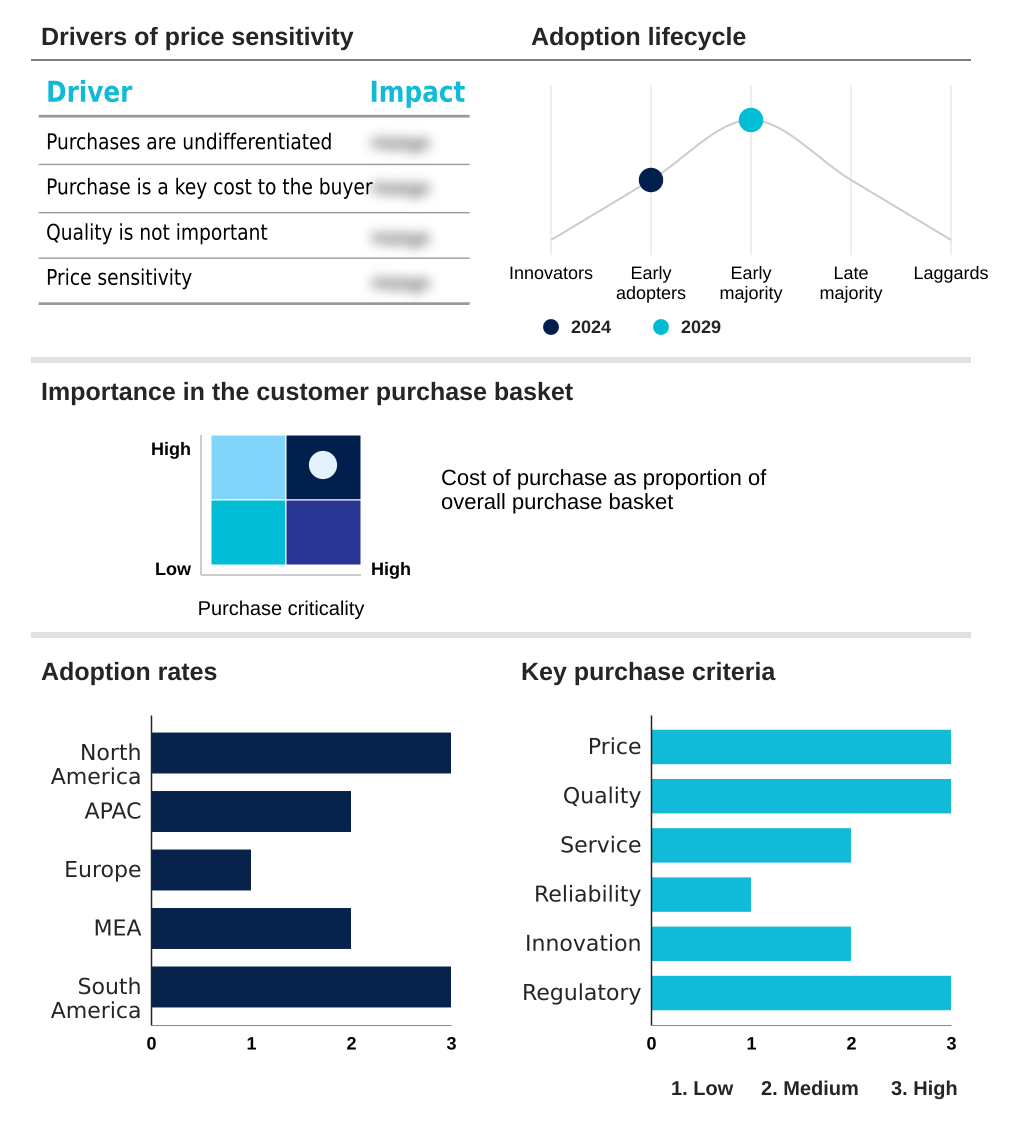

Exclusive Technavio Analysis on Customer Landscape

The generative ai in content creation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in content creation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Content Creation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in content creation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - Offers enterprise-grade AI platforms for multimodal content generation, automating and scaling creative workflows for text, image, video, and audio applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Anthropic

- Autodesk Inc.

- Cohere

- CopyAI Inc.

- Descript

- Eleven Labs Inc.

- Google LLC

- Grammarly Inc.

- Jasper AI Inc.

- Microsoft Corp.

- Midjourney

- NVIDIA Corp.

- OpenAI

- Runway AI Inc.

- Stability AI

- Suno.ai

- Synthesia Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in content creation market

- In September, 2024, Adobe Inc. completed its acquisition of a prominent AI video startup, announcing plans to integrate its advanced text-to-video generation technology directly into the Adobe Premiere Pro timeline by the first quarter of 2025.

- In January, 2025, Anthropic unveiled its Claude 4 series, a new family of models featuring enhanced agentic capabilities and a next-generation constitutional AI framework designed for complex, multi-step enterprise automation tasks.

- In March, 2025, Cohere announced it secured USD 750 million in a Series D funding round, with the capital earmarked for accelerating the development of industry-specific LLMs tailored for the finance, legal, and healthcare sectors.

- In May, 2025, Google LLC launched the 'Synthetic Data for Science' initiative, a global program providing verified researchers with access to high-fidelity, AI-generated datasets to accelerate breakthroughs in medical and climate research.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Content Creation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2024 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 32.2% |

| Market growth 2025-2029 | USD 36385.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 27.8% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The generative AI in content creation market is evolving from generalized tools to specialized, high-value solutions. Boardroom-level strategy now centers on leveraging proprietary data for AI model fine-tuning, creating a distinct competitive advantage. This shift is underpinned by the development of sophisticated multimodal AI systems, including large language models and diffusion models, capable of text-to-image generation and increasingly, text-to-video generation.

- Enterprises are implementing responsible AI principles and AI safety frameworks to mitigate copyright infringement risk and AI model hallucination. The adoption of on-device AI processing and enterprise-grade AI solutions with robust AI governance features is accelerating. Technologies such as AI voice synthesis, generative video features, and AI-driven video production are becoming integral.

- Companies using fine-tuned models for AI-powered copywriting and generative design tools report a reduction in content errors by over 30% compared to generic models. Success requires managing computational resource requirements with GPU hardware acceleration and API-based model access, while using conversational AI assistants and AI content assistants to augment workflows.

- The rise of open-source language models, coupled with AI ethics boards, is pushing for greater transparency through content provenance and digital watermarking, as voice cloning technology and automated transcription become mainstream.

What are the Key Data Covered in this Generative AI In Content Creation Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Content Creation Market between 2025 and 2029?

-

USD 36.39 billion, at a CAGR of 32.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services), Application (Text generation, Image generation, Video generation, Music and audio generation, Others), End-user (Entertainment and media, Marketing and advertising, E-commerce, Gaming, Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Demand for personalized and high-volume content, Intellectual property rights and unclear legal framework

-

-

Who are the major players in the Generative AI In Content Creation Market?

-

Adobe Inc., Anthropic, Autodesk Inc., Cohere, CopyAI Inc., Descript, Eleven Labs Inc., Google LLC, Grammarly Inc., Jasper AI Inc., Microsoft Corp., Midjourney, NVIDIA Corp., OpenAI, Runway AI Inc., Stability AI, Suno.ai and Synthesia Ltd.

-

Market Research Insights

- The market dynamics are shifting toward specialized applications that deliver measurable business outcomes through workflow integration. The adoption of domain-specific training data is critical, with firms reporting up to a 40% reduction in factual inaccuracies compared to general-purpose models.

- The use of real-time conversational AI for customer service automation is another key area, improving user satisfaction by over 30% in initial deployments. Furthermore, A/B testing automation for marketing campaigns has accelerated optimization cycles, leading to a 15% improvement in conversion rates.

- This focus on practical embedded AI capabilities, from AI-powered code assistants to virtual try-on experiences, is driving adoption as organizations move beyond experimentation to seek tangible returns on investment through enhanced human-computer interaction and legacy systems integration.

We can help! Our analysts can customize this generative ai in content creation market research report to meet your requirements.

RIA -

RIA -