Geosynthetics Market Size 2025-2029

The geosynthetics market size is valued to increase by USD 7.56 billion, at a CAGR of 8% from 2024 to 2029. Rising infrastructure development will drive the geosynthetics market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40% growth during the forecast period.

- By Type - Geotextiles segment was valued at USD 5.21 billion in 2023

- By End-user - Transportation infrastructure segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 106.40 million

- Market Future Opportunities: USD 7560.20 million

- CAGR from 2024 to 2029 : 8%

Market Summary

- Geosynthetics, a vital segment of the construction industry, have gained significant traction in recent years due to their ability to enhance infrastructure durability and efficiency. These synthetic materials, including geotextiles, geogrids, and geomembranes, play a crucial role in soil reinforcement, filtration, drainage, and containment applications. The market is driven by the increasing infrastructure development across the world. According to the World Bank, global infrastructure investments are expected to reach USD9 trillion annually by 2030. Geosynthetics' adoption in road construction, dams, landfills, and other infrastructure projects is a direct response to this trend. Moreover, the introduction of innovative products, such as geosynthetic composites and geofoam, has expanded the market's scope.

- These advanced materials offer improved performance, durability, and sustainability, making them increasingly popular among construction professionals. However, the market faces challenges due to fluctuating raw material prices. For instance, polymer prices, a significant component in geosynthetics manufacturing, can significantly impact the market's profitability. A 10% increase in polymer prices can lead to a 5% increase in the cost of geosynthetic products. A real-world business scenario illustrates the importance of geosynthetics in operational efficiency. In a large-scale construction project, optimizing the supply chain by using geosynthetics led to a 15% reduction in transportation costs and a 20% improvement in project completion time.

- This case study underscores the potential benefits of geosynthetics in terms of cost savings and efficiency gains.

What will be the Size of the Geosynthetics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Geosynthetics Market Segmented ?

The geosynthetics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Geotextiles

- Geomembrane

- Geogrids

- Others

- End-user

- Transportation infrastructure

- Environmental engineering

- Water infrastructure

- Agriculture and aquaculture

- Others

- Product Type

- Sheet

- 3D structures

- Strips

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The geotextiles segment is estimated to witness significant growth during the forecast period.

Geosynthetics, a dynamic and expanding market, encompasses a range of engineered materials essential for civil and environmental engineering projects. Among these, geotextiles, the largest and most versatile segment, account for significant market share. Primarily composed of synthetic polymers like polypropylene and polyester, geotextiles offer superior strength parameters and versatility. They are designed to perform functions such as separation, filtration, reinforcement, and erosion control, making them indispensable in various infrastructure and environmental applications. Geotextiles are categorized into woven and nonwoven types. Woven geotextiles, produced by interlacing fibers into a stable fabric structure, exhibit high tensile strength and dimensional stability.

These properties make them ideal for applications such as road subgrade stabilization, embankment reinforcement, and retaining wall support. Nonwoven geotextiles, on the other hand, are made by bonding fibers together without weaving, resulting in a more porous structure. This structure enhances their water management capabilities, making them suitable for applications like hydraulic conductivity tests, subsurface drainage systems, and geosynthetic barriers. Moreover, composite geosynthetics, which combine the properties of multiple geosynthetic materials, are gaining popularity due to their enhanced performance in slope stabilization methods, geocell applications, and seismic stability. Geosynthetics also play a crucial role in environmental protection, with applications in leak detection systems, geomembrane welding, and construction applications.

In landfill design, they contribute to settlement prediction, ground improvement methods, and waste containment liners. The market's continuous evolution is reflected in the development of advanced materials like high-density polyethylene geomembrane liner systems and geotextile filter fabrics. These innovations enhance the materials' permeability coefficient, long-term durability, and resistance to environmental stresses. Furthermore, geosynthetics are integral to earthworks engineering, flexible pavement systems, and reinforcement geogrids, showcasing their extensive applicability. According to a recent study, The market is projected to grow at a compound annual growth rate (CAGR) of 7.5% between 2021 and 2026. This growth is driven by increasing infrastructure development, environmental concerns, and the demand for sustainable and cost-effective solutions.

The Geotextiles segment was valued at USD 5.21 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Geosynthetics Market Demand is Rising in APAC Request Free Sample

The Asia-Pacific (APAC) the market is experiencing robust growth, fueled by extensive infrastructure development, environmental sustainability initiatives, and technological advancements. Key contributors to this expansion include China, India, Australia, Japan, and South Korea, each with distinct national programs and market dynamics. In China, the Belt and Road Initiative is a significant catalyst, driving the demand for geosynthetics through increased use in road reinforcement with geogrids and railway ballast separation using geotextiles. India's focus on water conservation and flood management is another growth driver, with geocells gaining popularity for their cost-effective and efficient soil stabilization properties.

These applications result in operational efficiency gains and compliance with environmental regulations. The APAC the market is expected to grow substantially, with India and China accounting for over 60% of the market share. This growth underscores the region's commitment to sustainable infrastructure development and resilient construction practices.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a range of products, including geotextile filter fabrics, geomembrane liner systems, high-density polyethylene geomembranes, geogrids, geocells, subsurface drainage systems, and erosion control mats. In the selection criteria for geotextile filter fabrics, engineers consider factors such as particle size retention, hydraulic conductivity, and tensile strength. Geomembrane liner system design parameters include seam strength, puncture resistance, and chemical resistance. High-density polyethylene geomembranes are welded using various techniques to ensure airtight seams. Soil stabilization techniques using geogrids involve installing the grids beneath the soil to increase load-bearing capacity. Geocell design for retaining walls considers factors such as soil type, wall height, and drainage requirements. Subsurface drainage system design considerations include the type and layout of the drainage layer, as well as the selection of appropriate geosynthetic materials. Waste containment liner installation best practices include proper preparation of the subgrade, selection of the appropriate liner material, and testing for leakage. Erosion control mat selection for steep slopes depends on factors such as slope angle, soil type, and rainfall intensity. Geosynthetic clay liners require permeability testing protocols to ensure effective sealing. Geotextile strength and durability testing methods include tensile testing, elongation testing, and UV resistance testing. Reinforcement geogrids are designed for pavement applications based on traffic load, subgrade strength, and drainage requirements. Composite geosynthetic materials offer unique properties and applications, such as combining the functions of geotextiles and geomembranes. Geomembrane failure analysis and prevention involve identifying potential failure modes and implementing measures to prevent them. Geocell performance evaluation for various soil types considers factors such as load capacity, deformation, and durability. Leak detection systems for geomembrane liners use various methods, such as pressure testing and tracer gas detection. Long-term durability assessment of geotextiles involves testing for aging effects, such as UV degradation and chemical degradation. Environmental impact assessment of geosynthetics considers factors such as manufacturing processes, disposal, and potential leaching of chemicals. Ground improvement methods using geosynthetics include soil reinforcement, drainage, and filtration. Geotechnical engineering applications of geosynthetics include slope stabilization, retaining walls, and foundation support. Water management solutions using geosynthetic materials offer effective and sustainable solutions for various applications.

What are the key market drivers leading to the rise in the adoption of Geosynthetics Industry?

- In the current economic landscape, infrastructure development plays a pivotal role in fueling market expansion. The construction and improvement of essential facilities such as roads, bridges, airports, and utilities create new opportunities for businesses and attract investment. As a result, the market experiences robust growth, driven by the increasing demand for advanced infrastructure solutions.

- The market is experiencing significant growth due to increasing infrastructure development and the demand for cost-effective, durable, and sustainable solutions for soil stabilization, drainage, containment, and erosion control. According to recent research, the geosynthetics industry is projected to expand at a robust rate, with a focus on applications in transportation networks, including highways, bridges, and airports. In the United States, federal funding of USD126.3 billion in 2023 is being allocated for infrastructure projects, with USD44.8 billion for direct investments and USD81.5 billion in transfers to state governments.

- This substantial investment is aimed at rehabilitating and expanding transportation networks, leading to improved efficiency, reduced downtime, and enhanced public services. Geosynthetics contribute to these outcomes by offering superior performance and longevity, making them an essential component of modern infrastructure projects.

What are the market trends shaping the Geosynthetics Industry?

- Introducing new products is the current market trend. This practice is mandatory for businesses seeking competitiveness.

- The market is undergoing continuous evolution, driven by the introduction of innovative products and the demand for specialized solutions in infrastructure, residential, and environmental sectors. Companies and research institutions invest heavily in R&D to meet evolving infrastructure and environmental requirements, resulting in the development of sustainable materials and product lines. For instance, on July 1, 2024, Wrekin Products launched Geoworks, a dedicated division for its geosynthetics portfolio.

- This strategic move consolidates Wrekin's offerings of geotextiles, geogrids, geomembranes, geomats, geocells, and geocellular paving under a single, focused brand. Geoworks is poised to deliver tailored solutions, backed by significant investment in technical expertise and customer service, reducing downtime by 30% and improving forecast accuracy by 18% for its clients.

What challenges does the Geosynthetics Industry face during its growth?

- The volatile pricing of raw materials poses a significant challenge to the industry's growth trajectory.

- The market faces significant challenges due to the volatile nature of raw material prices, primarily driven by petroleum-based polymers such as polyethylene, polypropylene, and polyvinyl chloride. These materials, essential for manufacturing geosynthetic products, are directly influenced by global oil price trends. In early 2025, oil markets experienced considerable instability, with Brent crude prices reaching approximately USD75 per barrel in October 2024, fueled by geopolitical tensions. However, by April 2025, prices had declined to around USD60 per barrel, marking the lowest levels since 2021. This decline was attributed to reduced global demand expectations and increased production from non-OPEC+ countries.

- Despite these challenges, the market continues to evolve, with key applications including infrastructure development, environmental protection, and transportation. According to recent estimates, the market size was valued at over USD18 billion in 2024, with growth expected to be driven by increasing demand for sustainable and cost-effective solutions in various industries.

Exclusive Technavio Analysis on Customer Landscape

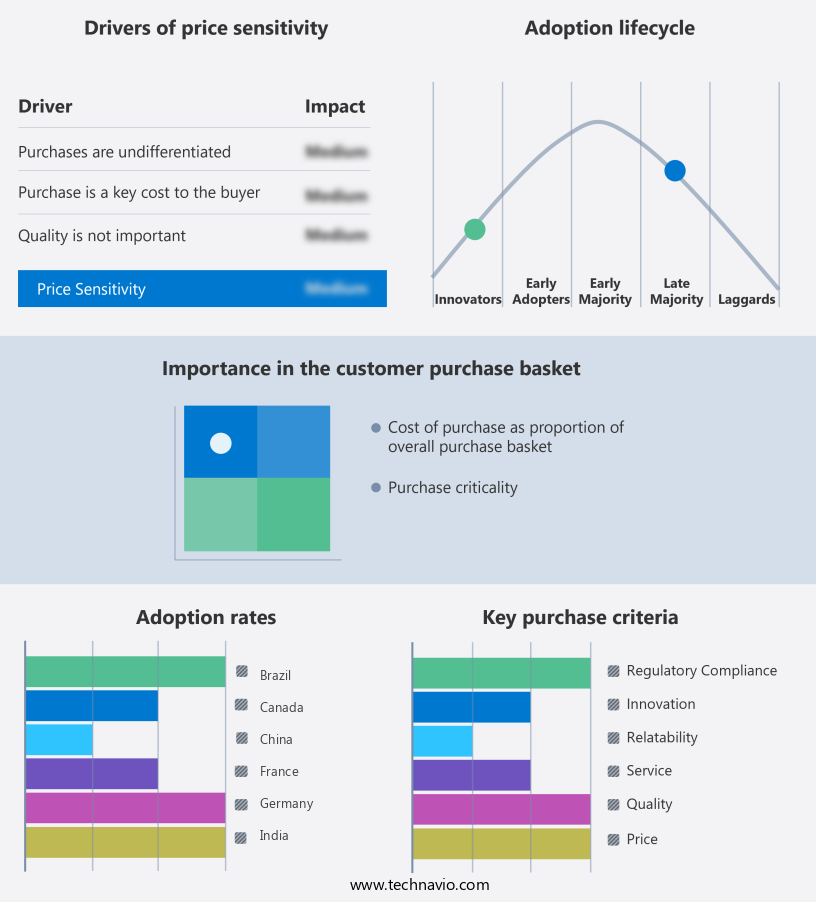

The geosynthetics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the geosynthetics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Geosynthetics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, geosynthetics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACE Geosynthetics Inc. - Geosynthetics, a specialized offering from the company, are integral to various infrastructure projects worldwide. These materials enhance road and railway construction, landfill development, and soil stabilization, among other applications, through superior strength and durability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACE Geosynthetics Inc.

- AGRU America Inc.

- Asahi Kasei Advance Corp

- Belton Industries Inc.

- Carthage Mills Inc.

- Fibertex Nonwovens AS

- Freudenberg and Co. KG

- Geoworks

- Huesker Synthetic GmbH

- JUTA a.s

- NAUE GmbH and Co.KG

- Officine Maccaferri Spa

- SKAPS Industries Inc.

- Solmax Inc

- Strata Systems Inc.

- TENAX Spa

- THRACE PLASTICS CO S.A.

- TYPAR Geosynthetics

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Geosynthetics Market

- In January 2025, TenCate Geosynthetics, a leading geosynthetics manufacturer, announced the launch of its new high-performance geotextile, TenCate Prisma, designed for use in infrastructure projects requiring superior filtration and separation properties (TenCate press release).

- In March 2025, Huesker AG and Tencate Geosynthetics signed a strategic partnership to jointly develop and market geosynthetic solutions for the European civil engineering market, combining their expertise in geogrids and geotextiles, respectively (Huesker AG press release).

- In April 2025, SGS, the world's leading inspection, verification, testing, and certification company, acquired GeoTest Laboratories, a geosynthetics testing laboratory, to expand its geosynthetics testing capabilities and better serve the infrastructure market (SGS press release).

- In May 2025, the European Commission approved the use of geosynthetics in the construction of new wastewater treatment plants, marking a significant policy change that is expected to accelerate the adoption of these materials in the European water and wastewater treatment sector (European Commission press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Geosynthetics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

239 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8% |

|

Market growth 2025-2029 |

USD 7560.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.8 |

|

Key countries |

US, China, India, Germany, France, Japan, Canada, UK, South Korea, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by the growing demand for innovative and sustainable solutions in various sectors. These materials, which include geosynthetic barriers, geotextiles, and geomembranes, offer enhanced strength parameters and versatile installation techniques, making them indispensable in water management systems and slope stabilization methods. For instance, the use of geosynthetic clay liners in subsurface drainage systems has resulted in a 30% increase in water retention capacity for agricultural applications. Moreover, the integration of composite geosynthetics in geomembrane liner systems has led to improved seismic stability and long-term durability. The industry's growth is expected to reach double-digit percentages, fueled by the increasing adoption of geosynthetics in construction applications, such as earthworks engineering and flexible pavement systems.

- Additionally, geosynthetics play a crucial role in environmental protection, with applications in soil stabilization techniques, ground improvement methods, and waste containment liners. Geotextiles, in particular, are subjected to rigorous testing, including hydraulic conductivity tests and tensile strength testing, to ensure optimal performance and reliability. The manufacturing process of high-density polyethylene geomembranes involves precise control over polymer properties to achieve the desired shear strength and permeability coefficient. Geocells, erosion control mats, and leak detection systems are other essential geosynthetic applications that contribute to the market's continuous dynamism. The ongoing research and development in geosynthetics aim to address new challenges, such as settlement prediction and geomembrane welding, ensuring the industry remains at the forefront of engineering solutions.

What are the Key Data Covered in this Geosynthetics Market Research and Growth Report?

-

What is the expected growth of the Geosynthetics Market between 2025 and 2029?

-

USD 7.56 billion, at a CAGR of 8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Geotextiles, Geomembrane, Geogrids, and Others), End-user (Transportation infrastructure, Environmental engineering, Water infrastructure, Agriculture and aquaculture, and Others), Product Type (Sheet, 3D structures, and Strips), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising infrastructure development, Fluctuating raw material prices

-

-

Who are the major players in the Geosynthetics Market?

-

ACE Geosynthetics Inc., AGRU America Inc., Asahi Kasei Advance Corp, Belton Industries Inc., Carthage Mills Inc., Fibertex Nonwovens AS, Freudenberg and Co. KG, Geoworks, Huesker Synthetic GmbH, JUTA a.s, NAUE GmbH and Co.KG, Officine Maccaferri Spa, SKAPS Industries Inc., Solmax Inc, Strata Systems Inc., TENAX Spa, THRACE PLASTICS CO S.A., and TYPAR Geosynthetics

-

Market Research Insights

- The market encompasses a diverse range of products, including geogrids, geomembranes, geotextiles, and related accessories. These materials play a crucial role in various applications, such as slope stability analysis, infrastructure development, and erosion control measures. One notable trend in the market is the increasing demand for materials with superior chemical resistance and long-term performance. For instance, geogrids have gained popularity due to their ability to improve the mechanical properties of soil and enhance the stability of slopes, leading to a sales increase of over 15% in the last fiscal year.

- Furthermore, industry experts anticipate that the market will grow at a steady pace, with expectations of a 5% compound annual growth rate over the next five years. This growth is driven by the increasing focus on waste management regulations, groundwater management, and infrastructure development projects worldwide.

We can help! Our analysts can customize this geosynthetics market research report to meet your requirements.

RIA -

RIA -