Enjoy complimentary customisation on priority with our Enterprise License!

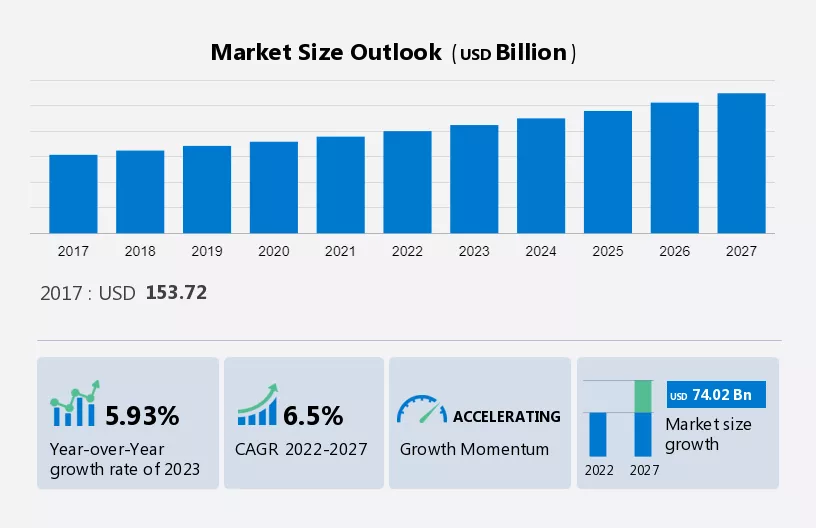

The HVAC market size is estimated to increase by USD 74.02 billion, at a CAGR of 6.5% between 2023 and 2028. The growth rate of the market depends on several factors such as the growing construction sector, the rising preference for condensing boilers, and the increasing refurbishment and replacement demand.

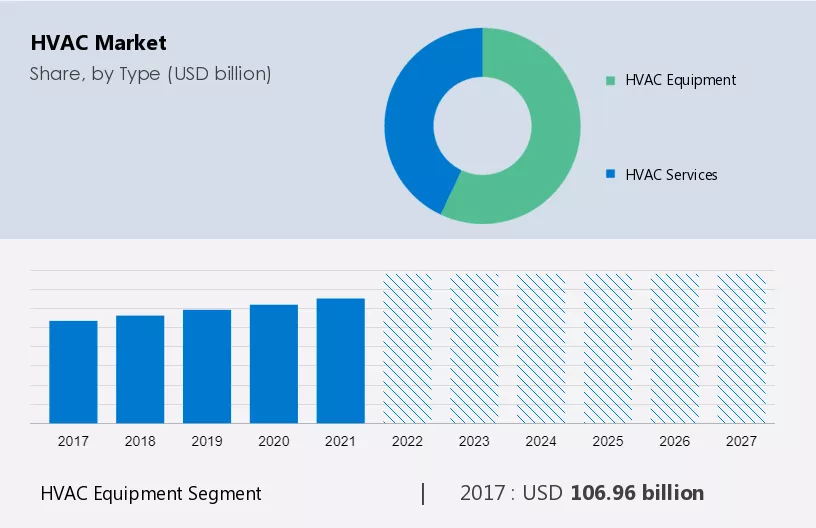

The market trends and analysis report includes a comprehensive outlook on the market, offering forecasts for the industry segmented by Type, which comprises HVAC equipment and HVAC services. Additionally, it categorizes End-user into non-residential and residential and covers Regions, including APAC, Europe, North America, Middle East and Africa, and South America. The market growth analysis report provides market size, historical data spanning from 2018 to 2022, and future projections, all presented in terms of value in USD billion for each of the mentioned segments.

To learn more about this report, Request Free Sample

The construction sector plays a major role in driving the demand for systems. With the increase in the construction of commercial and residential buildings, the demand for equipment and services has been increasing, thereby driving the growth of the market during the forecast period.

Furthermore, ductless systems are highly efficient and flexible. Ductless systems are highly applicable in residential buildings. Most of the countries in APAC prefer ductless air conditioning as it is more economical and consumes less energy than central air-conditioning for the residential sector. Ductless systems can be used to heat and cool the entire house or installed in new room additions, individual rooms, or basements to ensure zoned solutions. Mini split ACs can either be installed in ceilings, walls, or floors. Such development is expected to drive the market growth and trends during the forecast period.

BASs, which control and monitor other facilities of a given building, are embedded with computing and digital communication tools that allow these systems to enhance energy efficiency. The number of integrated BAS installations has increased owing to the rise in the number of construction projects and building retrofits.

Moreover, the energy efficiency ensured by the ever-improving BAS technology enables building owners to enhance facility management with integrated user-friendly solutions. The integration of HVAC controls with access control technologies is one such example. Such benefits are expected to propel the growth of the global market during the forecast period.

The future outlook of the market promises opportunities shaped by technological advancements, notably in the realm of IoT (Internet of Things). Customers increasingly seek smart, energy-efficient solutions, driving innovation in the air conditioning industry. IoT integration allows for enhanced control and automation, optimizing systems for personalized comfort and energy savings. The interconnectivity of devices is reshaping the landscape, offering not just climate control but also predictive maintenance and improved efficiency. As the market embraces these advancements, there's a clear trajectory towards a more responsive, sustainable, and customer-centric industry poised for growth and evolution in the years to come.

The units used in the residential and non-residential segments are made up of various components for the heating and cooling systems. These systems have evolved in the past years to include more software-based and electrical components, along with numerous mechanical components that are necessary for cooling or heat transfer. Due to the increase in the number of components in a unit, the chances of any of these parts failing have also increased.

Thus, failure issues in equipment can lead to an increase in the operating cost of end-users and will encourage them to opt for substitutes, thus impacting the demand for equipment, and hindering the growth of the market during the forecast period.

The HVAC market's regulatory landscape is evolving to address questions surrounding air quality, innovation, and customer satisfaction. With a focus on environmental concerns, regulations impact the construction industry, demanding energy-efficient air conditioners and refrigeration systems. Manufacturers, suppliers, and contractors in the industry are adapting to stringent guidelines, emphasizing regular maintenance and innovative solutions. Ductwork standards play a crucial role in enhancing air quality, while regulations span multiple pages, reflecting the complexity of the industry. As the sector navigates evolving regulations, the commitment to meeting customer needs and advancing technology remains pivotal for all stakeholders in this dynamic market.

The HVAC equipment segment will account for a major share of the market's growth during the forecast period.?The growing population and industrialization, the rise in construction expenditure, the increase in sales of commercial and residential buildings, and the augmented disposable income of the middle-class population are driving the market. Furthermore, the increase in demand for the equipment from the residential and non-residential sectors will drive the market.

Customised Report as per your requirements!

The HVAC equipment segment was valued at USD 106.96 billion in 2018. The growing population and industrialization, the rise in construction expenditure, the increase in sales of commercial and residential buildings, and the augmented disposable income of the middle-class population are driving the market. Heat pumps, air-conditioners (ACs) in rooms, and unitary ACs are likely to witness significant demand in both residential and non-residential buildings.

Non-residential end-users of HVAC equipment are manufacturing facilities, commercial and industrial buildings, retail stores, and healthcare and educational institutions. An increase in the construction of these end-users will drive the growth of the global System Market. HVAC systems, in conjunction with the entire building design, will help significantly reduce energy consumption. Buildings can save nearly 30% of the total energy cost annually by incorporating high-performance systems.

Furthermore, various builders prefer to promote green buildings as a means of differentiation to cope with intense competition in the market. Owing to the adoption of green technology, the demand for units has increased simultaneously as they help in energy savings. The rise in the number of net-zero buildings is the major trend in the construction business. A net-zero building can produce renewable energy to meet its annual energy consumption requirements. This reduces the need for non-renewable energy in the building. The commercial sector has seen growth in terms of the increasing number of office buildings, data centers, and healthcare facilities. Such factors will increase the market growth during the forecast period.

For more insights on the market share of various regions Download Sample PDF now!

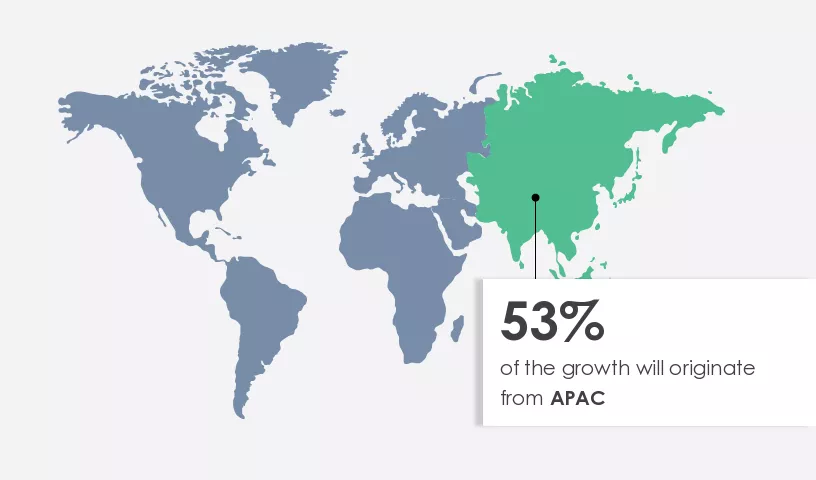

APAC is estimated to contribute 53% to the growth by 2028. Technavio’s analysts have elaborately explained the regional trends, drivers, and challenges that are expected to shape the market during the forecast period. APAC is the largest market for HVAC due to the growing population, climatic conditions, increasing urbanization, and demographic changes in the region. The expanding commercial construction sector is the key driving factor for market growth in countries such as China and India. Regulations and efficiency norms in countries such as India and China will drive the Heating, Ventilation, and Air Conditioning Market in APAC during the forecast period.

Furthermore, an increase in the number of urban high-rise condominium projects will propel the demand for systems. Expansive construction projects in Australia, such as the Queen's Wharf, Howard Smith Wharves, and other significant urban development projects, will propel the demand for systems. The Queen's Wharf will accommodate five major premium hotels, three residential towers, large departmental stores, food and beverage outlets, a Queensland hotel, and other related buildings. Hence, all these projects require HVAC systems, thereby driving the growth of the regional market.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including:

Air Comfort, Alexander Mechanical Inc., Blue Star Ltd., Carrier Global Corp., Daikin Industries Ltd., EMCOR Group Inc., Emerson Electric Co., ENGIE SA, Ferguson plc, Fujitsu Ltd., Ingersoll Rand Inc., J and J Air Conditioning, Johnson Controls International Plc, Lennox International Inc., LG Electronics Inc., Nortek, Samsung Electronics Co. Ltd., Service Logic, and Siemens AG

Technavio's market research and growth report provides an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

The market growth and forecasting report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

|

HVAC Market Scope |

|

|

Market Report Coverage |

Details |

|

Page number |

16 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.5% |

|

Market Growth 2024-2028 |

USD 74.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.93 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 53% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABM Industries Inc., Air Comfort, Alexander Mechanical Inc., Blue Star Ltd., Carrier Global Corp., Daikin Industries Ltd., EMCOR Group Inc., Emerson Electric Co., ENGIE SA, Ferguson plc, Fujitsu Ltd., Ingersoll Rand Inc., J and J Air Conditioning, Johnson Controls International Plc, Lennox International Inc., LG Electronics Inc., Nortek, Samsung Electronics Co. Ltd., Service Logic, and Siemens AG |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market condition analysis for the forecast period. |

|

Customization purview |

If our market forecasting report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by End-user

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights