Industrial HVAC Market Size 2026-2030

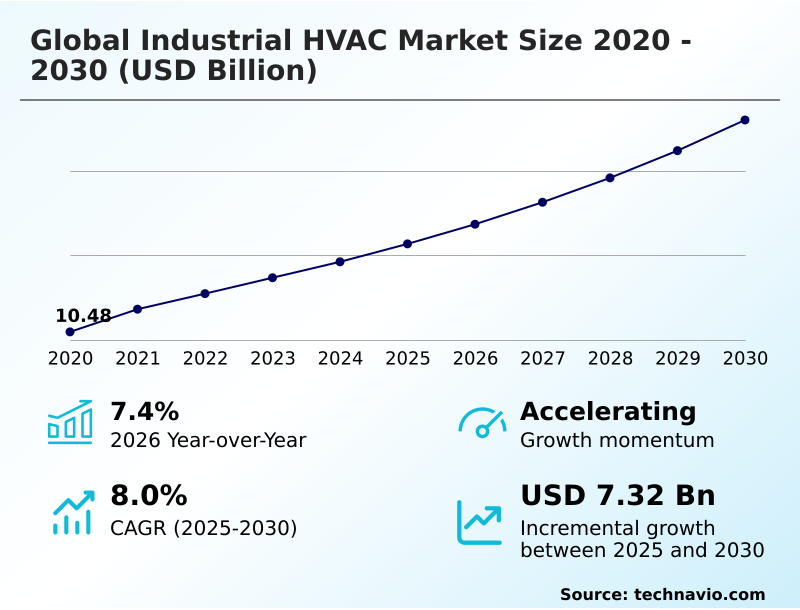

The industrial hvac market size is valued to increase by USD 7.32 billion, at a CAGR of 8% from 2025 to 2030. Accelerated decarbonization and electrification via industrial heat pumps will drive the industrial hvac market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.3% growth during the forecast period.

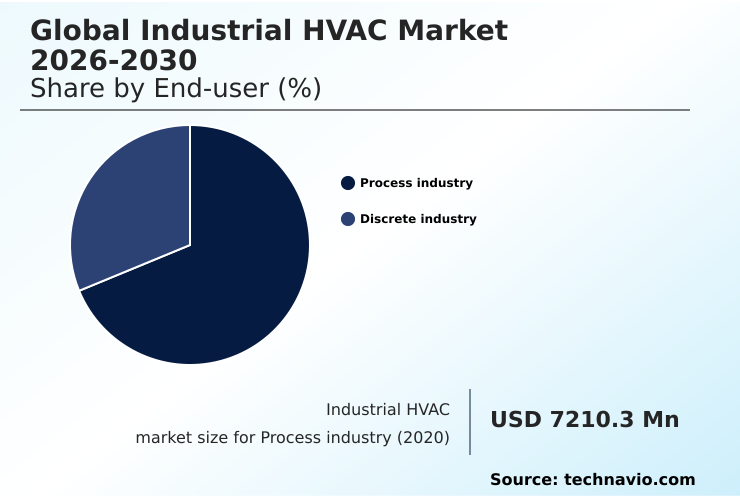

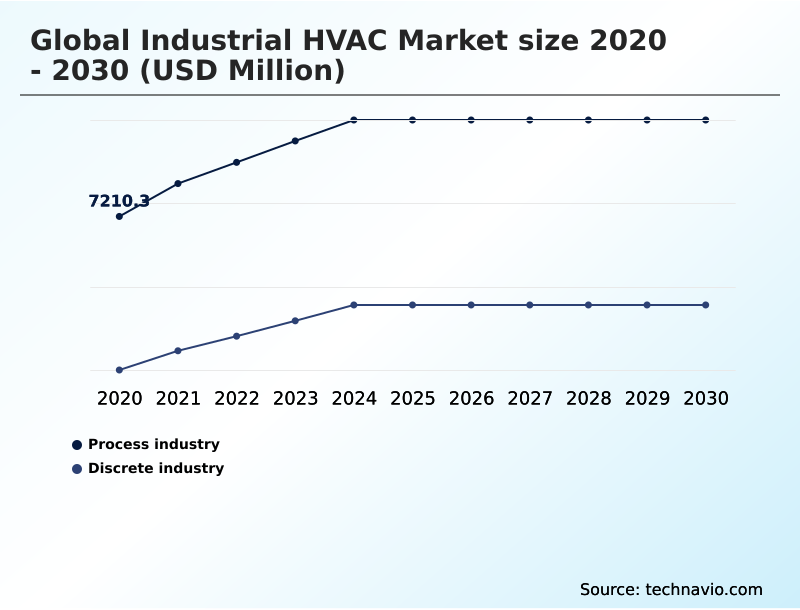

- By End-user - Process industry segment was valued at USD 9.68 billion in 2024

- By Type - HVAC equipment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 12.51 billion

- Market Future Opportunities: USD 7.32 billion

- CAGR from 2025 to 2030 : 8%

Market Summary

- The industrial HVAC market is undergoing a significant transformation, driven by the dual imperatives of decarbonization and digitalization. A primary driver is the expansion of high-performance computing and AI, which has created unprecedented demand for mission-critical cooling systems in hyperscale data centers.

- Concurrently, stringent environmental regulations are compelling a shift toward the electrification of industrial heat, with facilities replacing fossil-fuel boilers with high-capacity heat pumps and exploring low-GWP refrigerants. This transition is enabled by the integration of AI and IoT, which facilitates predictive maintenance and data-driven operational management.

- For instance, a pharmaceutical manufacturer can now deploy smart building ecosystems to maintain sterile conditions with precision air handling, ensuring compliance while optimizing energy consumption. However, this increasing system complexity exacerbates a primary challenge: a structural skilled labor deficit. As experienced technicians retire, the industry grapples with finding qualified professionals to install and service these advanced, interconnected systems.

- This dynamic pushes the market toward more autonomous climate control and modular, easier-to-maintain hardware designs to ensure long-term operational resilience and efficiency across industrial applications.

What will be the Size of the Industrial HVAC Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Industrial HVAC Market Segmented?

The industrial hvac industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Process industry

- Discrete industry

- Type

- HVAC equipment

- HVAC services

- Product type

- Heat pump

- Furnace

- Unitary systems

- Boilers

- Others

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The process industry segment is estimated to witness significant growth during the forecast period.

The process industry segment requires specialized climate control to manage production environments in sectors like chemicals, pharmaceuticals, and food manufacturing.

These facilities are advancing their decarbonization of heating through the adoption of high-capacity heat pumps integrated into hydronic backbone systems, which can recover up to 70% of waste heat from process water.

The growing industrial refrigeration demand is met by systems offering precision air handling and high-efficiency particulate air filtration to maintain sterile conditions.

As part of a broader asset lifecycle management strategy, operators are investing in smart building ecosystems that ensure compliance with a complex low-carbon regulatory landscape, optimizing energy consumption while protecting product integrity and worker safety in these highly controlled settings.

The Process industry segment was valued at USD 9.68 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial HVAC Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the industrial HVAC market is heavily influenced by regional manufacturing and technology priorities.

In APAC, the rapid expansion of semiconductor fabrication and hyperscale data centers fuels demand, with the regional market for data center cooling projected to grow significantly.

This has spurred record adoption of advanced liquid cooling architectures for AI server cluster cooling. In North America, a manufacturing resurgence supported by federal incentives drives investment in mission-critical cooling systems and modular chillers.

The region is also at the forefront of industrial internet of things integration and remote monitoring capabilities for high-density computing workloads.

Across all developed regions, the focus is on energy-efficient data center cooling and the deployment of intelligent hardware to manage the thermal loads of the expanding digital economy, ensuring operational continuity and performance.

Market Dynamics

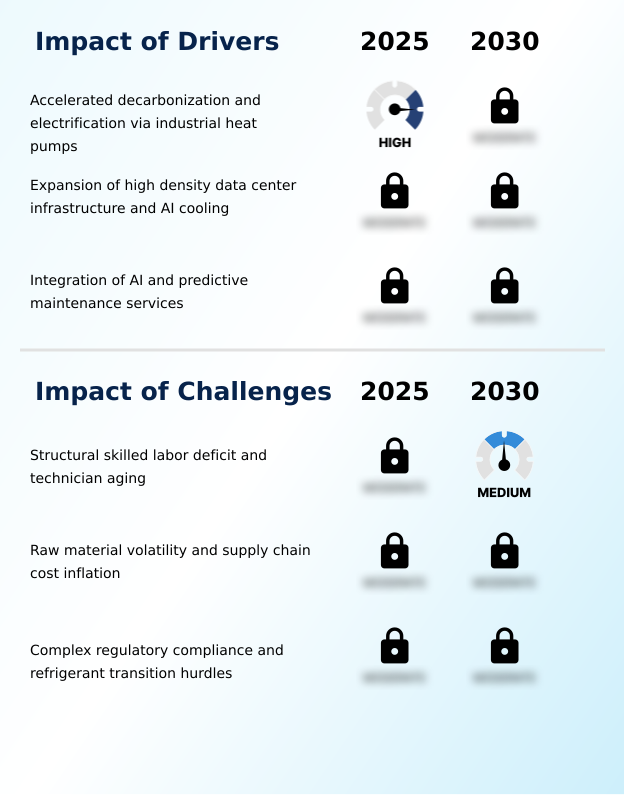

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the industrial HVAC market is shaped by a complex interplay of technological innovation and operational challenges. The benefits of AI-driven HVAC predictive maintenance are becoming clear, with some deployments reducing unexpected equipment breakdowns by over 90% compared to reactive schedules, showcasing a strong business case for investment.

- Simultaneously, the low-GWP refrigerant transition in industrial HVAC presents both regulatory hurdles and opportunities for enhanced system efficiency. Key areas of focus include improving the energy efficiency of industrial heat pumps and developing advanced thermal management for high-density data centers. Smart building integration for HVAC optimization is no longer a niche concept but a core requirement for modern facilities.

- However, the impact of raw material volatility on HVAC manufacturing and a persistent skilled labor shortage in HVAC services remain significant constraints. To navigate this, companies are exploring HVAC-as-a-service models for industrial facilities and investing in digital twin technology in HVAC system design to simulate performance and mitigate risk.

- The role of IoT in industrial climate control is expanding, enabling remote diagnostics for industrial HVAC systems and better management of thermal loads in discrete manufacturing. This digital shift, coupled with specialized hardware like modular chiller platforms and advanced air filtration for pharmaceutical manufacturing, is critical for addressing decarbonization strategies and ensuring regulatory compliance for industrial refrigerants.

What are the key market drivers leading to the rise in the adoption of Industrial HVAC Industry?

- The accelerated decarbonization and electrification of thermal processes through the deployment of industrial heat pumps is a primary market driver.

- Market growth is propelled by digitalization and the push toward net-zero emissions targets.

- The integration of AI into cooling management systems has resulted in a 20% improvement in power usage effectiveness, making it a critical driver for the data center sector's demand for advanced thermal management solutions.

- Concurrently, the shift to proactive, data-driven management through AI-powered predictive maintenance services can reduce emergency repair costs by approximately 38%. This transition is facilitated by smart building automation systems and connected air handling units.

- As facilities adopt more ruggedized HVAC units for decentralized applications, the principles of autonomous climate control are being applied to optimize energy efficiency ratings and ensure reliability across the entire operational footprint, fundamentally redefining performance standards.

What are the market trends shaping the Industrial HVAC Industry?

- A key market trend is the rapid electrification of industrial heat, marked by the increasing adoption of large-scale, reversible heat pump systems.

- Key trends are fundamentally reshaping industrial climate control, with a strong focus on sustainability and advanced performance. The electrification of thermal processes is accelerating, with market data showing heat pumps accounted for approximately 28% of newly installed heating systems in some mature markets. This shift toward circular energy systems involves not just replacing old hardware but rethinking energy flow.

- Innovations in HVAC-as-a-service models and digital twin-based optimization are gaining traction, allowing for performance-based contracts. A breakthrough trend is the integration of thermal energy storage with advanced dehumidification technologies; these hybrid systems can cut peak power demand by over 90%, transforming facilities into grid-interactive buildings.

- This is complemented by hardware advancements like variable refrigerant flow systems and oil-free centrifugal compressors, all while the industry navigates the mandatory transition to low-GWP refrigerants.

What challenges does the Industrial HVAC Industry face during its growth?

- A structural deficit in skilled technical labor, compounded by an aging technician workforce, poses a significant challenge to the industry's growth.

- The industrial HVAC market faces significant operational and economic headwinds that challenge its growth trajectory. The most pressing issue is a structural skilled labor shortage, with estimates indicating that for every five technicians retiring, only two new workers enter the trade, leaving a critical gap.

- This is compounded by persistent supply chain cost inflation, where disruptions have caused air freight rates to increase by as much as 70%. Manufacturers of industrial heat pumps and magnetic-bearing chillers must navigate this volatile environment, often relying on remote diagnostic tools to amplify the efficiency of their existing workforce.

- The push toward a low-carbon regulatory landscape also presents hurdles, as facilities must invest in new infrastructure such as solar-powered HVAC or connect to district heating and cooling networks. These combined pressures strain asset lifecycle management and hinder the adoption of innovations like automated assembly plant cooling.

Exclusive Technavio Analysis on Customer Landscape

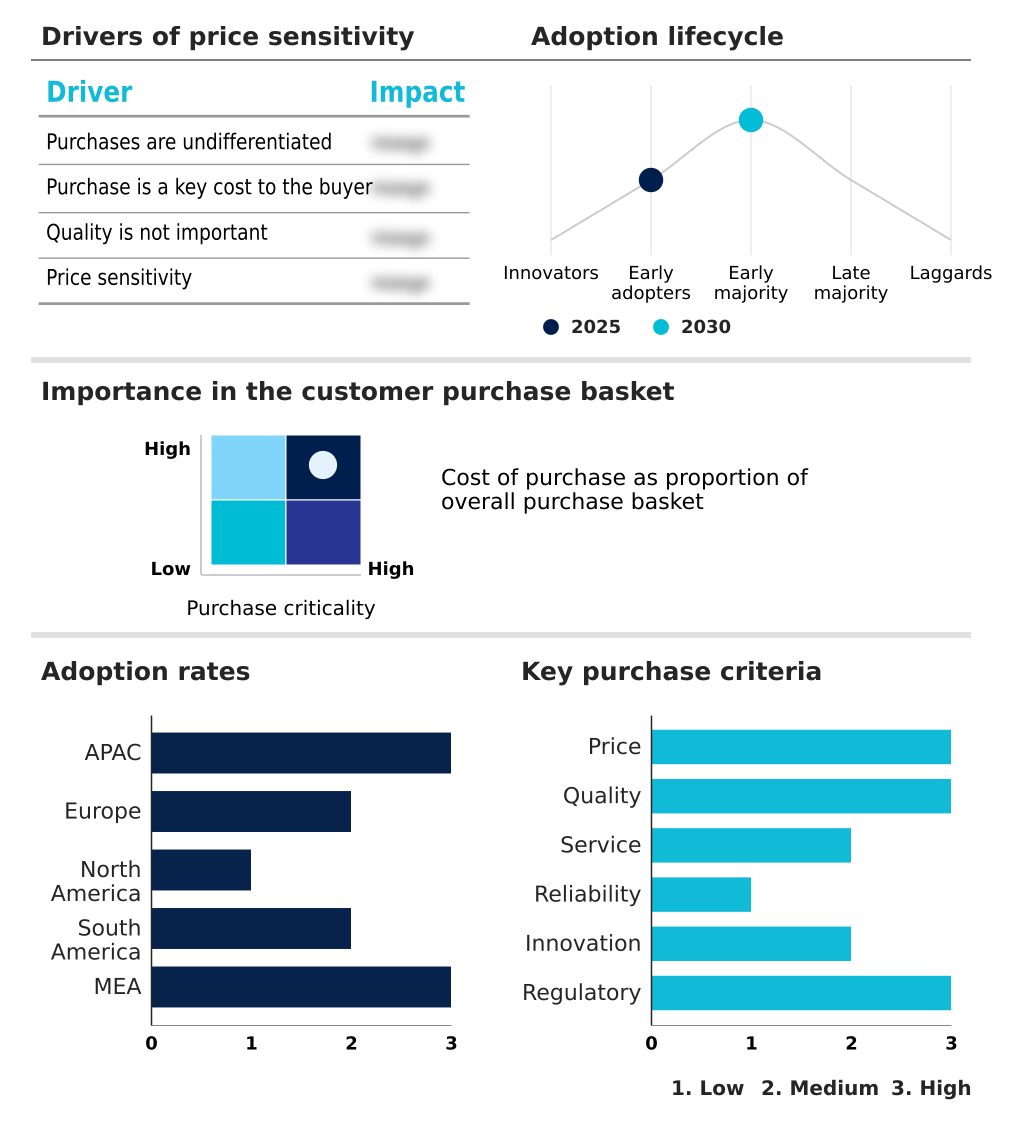

The industrial hvac market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial hvac market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial HVAC Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, industrial hvac market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AAON Inc. - The vendor provides advanced industrial HVAC solutions, including high-capacity chillers and specialized air handling units, engineered for demanding large-scale commercial and industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AAON Inc.

- Alfa Laval AB

- Carrier Global Corp.

- Daikin Industries Ltd.

- Danfoss AS

- FlaktGroup Holding GmbH

- Fujitsu General Ltd.

- Gree Electric Appliances Inc.

- Honeywell International Inc.

- Johnson Controls International

- Lennox International Inc.

- LG Electronics Inc.

- Mitsubishi Electric Corp.

- Munters Group AB

- Nortek Air Solutions LLC

- Panasonic Holdings Corp.

- Siemens AG

- Systemair AB

- Trane Technologies Plc

- Zehnder Group AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial hvac market

- In August 2025, Daikin Applied acquired DDC Solutions, a firm specializing in artificial intelligence-driven cooling technologies, to expand its mission-critical portfolio for data centers.

- In December 2025, Daikin Applied committed $163 million to establish a high-technology research and development laboratory focused on testing large-scale HVAC innovations for industrial applications.

- In February 2026, Carrier Global Corp. announced its commercial orders experienced nearly 50% growth, driven by major contract wins in the global data center sector.

- In April 2026, Johnson Controls acquired Nantum AI to integrate advanced energy optimization and autonomous control features into its OpenBlue service platform.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial HVAC Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8% |

| Market growth 2026-2030 | USD 7320.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.4% |

| Key countries | China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Turkey and Qatar |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industrial HVAC market is defined by a technological convergence aimed at decarbonization and extreme efficiency. At the core, industrial heat pumps are enabling facilities to reduce primary energy consumption by up to 70% compared to traditional systems.

- The architecture of modern facilities now includes high-capacity heat pumps and often integrates with district heating and cooling as part of a larger energy strategy. For specialized, high-load environments, thermal management solutions are critical, with liquid cooling architectures becoming standard for AI server cluster cooling and data center cooling.

- The hardware evolution is evident in the deployment of modular chillers and high-performance magnetic-bearing chillers, which offer superior energy efficiency ratings. On a micro-level, precision air handling and high-efficiency particulate air filtration are non-negotiable in sectors like pharmaceuticals. The entire ecosystem is managed through sophisticated building automation systems that enable predictive maintenance services and remote diagnostic tools.

- This shift is also driving new business structures, such as HVAC-as-a-service models, and technological approaches, including oil-free centrifugal compressors, variable refrigerant flow, solar-powered HVAC, and integration with district cooling networks, all while navigating the mandatory transition to low-GWP refrigerants.

What are the Key Data Covered in this Industrial HVAC Market Research and Growth Report?

-

What is the expected growth of the Industrial HVAC Market between 2026 and 2030?

-

USD 7.32 billion, at a CAGR of 8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Process industry, and Discrete industry), Type (HVAC equipment, and HVAC services), Product Type (Heat pump, Furnace, Unitary systems, Boilers, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated decarbonization and electrification via industrial heat pumps, Structural skilled labor deficit and technician aging

-

-

Who are the major players in the Industrial HVAC Market?

-

AAON Inc., Alfa Laval AB, Carrier Global Corp., Daikin Industries Ltd., Danfoss AS, FlaktGroup Holding GmbH, Fujitsu General Ltd., Gree Electric Appliances Inc., Honeywell International Inc., Johnson Controls International, Lennox International Inc., LG Electronics Inc., Mitsubishi Electric Corp., Munters Group AB, Nortek Air Solutions LLC, Panasonic Holdings Corp., Siemens AG, Systemair AB, Trane Technologies Plc and Zehnder Group AG

-

Market Research Insights

- The industrial HVAC market is shifting from reactive maintenance to proactive, data-driven management, a trend underscored by key performance metrics. The integration of AI into cooling management systems has demonstrated a 20% improvement in power usage effectiveness, a critical factor for data center operators.

- Similarly, AI-driven predictive maintenance has been shown to reduce emergency repair costs by approximately 38% by identifying component degradation weeks before failure. This move toward autonomous climate control and intelligent asset lifecycle management allows industrial clients to transition to guaranteed performance outcomes rather than just owning physical assets.

- Such advancements in proactive data-driven management redefine reliability standards, ensuring that long-term asset value is maximized while minimizing total cost of ownership for facility operators globally.

We can help! Our analysts can customize this industrial hvac market research report to meet your requirements.

RIA -

RIA -