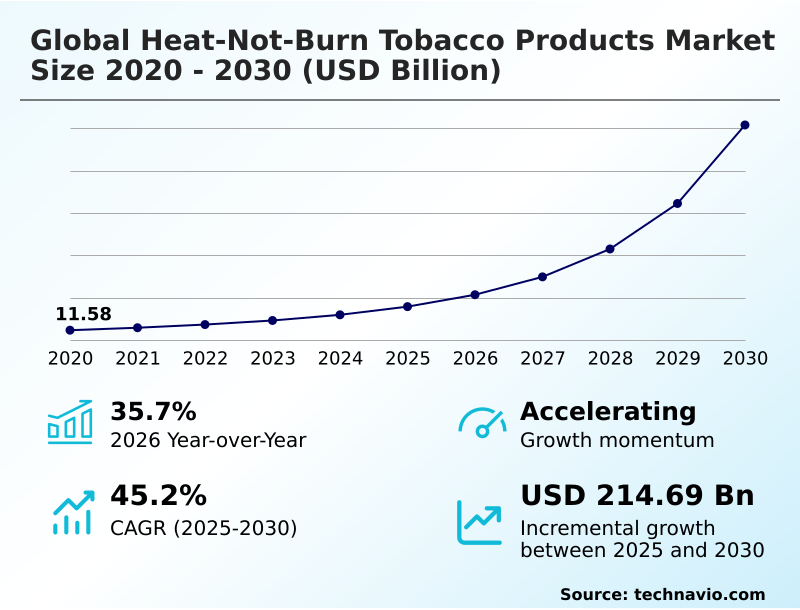

Heat-not-burn Tobacco Products Market Size 2026-2030

The heat-not-burn tobacco products market size is valued to increase by USD 214.69 billion, at a CAGR of 45.2% from 2025 to 2030. Increasing consumer demand for reduced-risk nicotine delivery systems will drive the heat-not-burn tobacco products market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.9% growth during the forecast period.

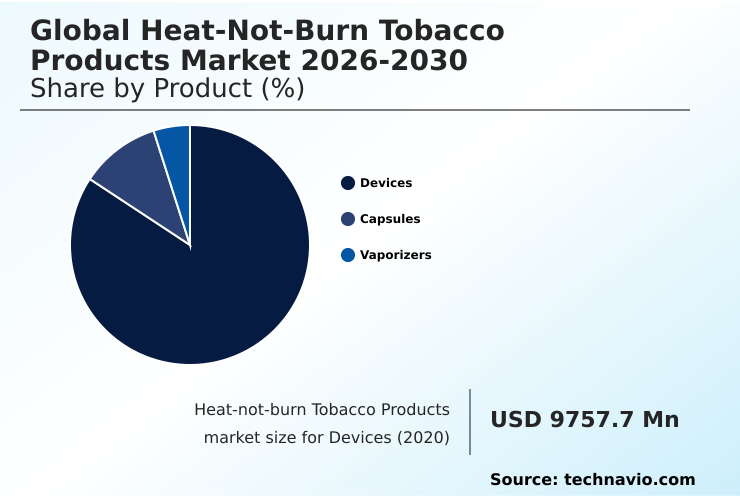

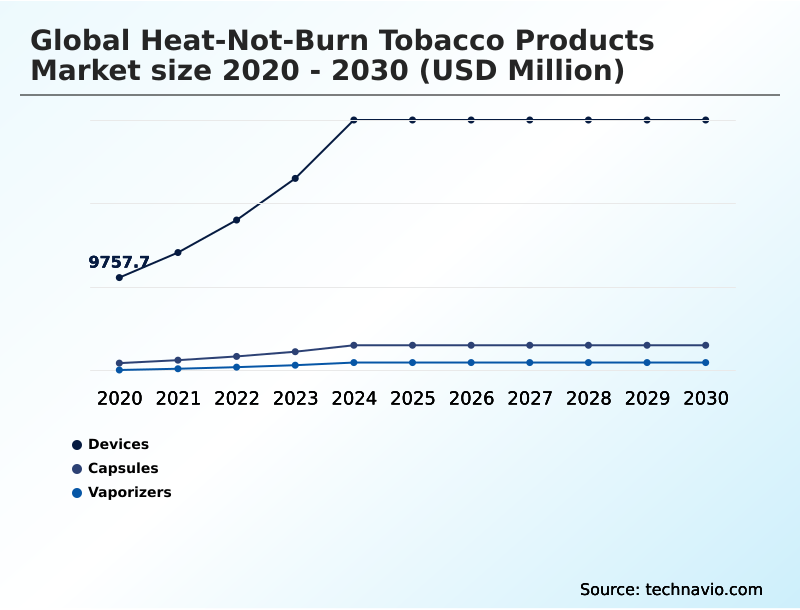

- By Product - Devices segment was valued at USD 25.43 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 242.54 billion

- Market Future Opportunities: USD 214.69 billion

- CAGR from 2025 to 2030 : 45.2%

Market Summary

- The heat-not-burn tobacco products market is undergoing a significant transformation, driven by a consumer shift toward reduced-risk alternatives. These systems utilize advanced technology, including induction heating systems and sophisticated thermal management systems, to generate a nicotine-containing aerosol without combustion, thereby reducing exposure to harmful chemicals. This appeals to a wellness-prioritizing demographic seeking a familiar sensory experience.

- The market dynamics are shaped by key trends such as premiumization, with a focus on artisanal flavor profiles and high-end lifestyle accessories. A critical business scenario involves navigating the complex and fragmented regulatory landscape, where companies must adapt their portfolios to varying regional rules on characterizing flavors and marketing.

- For instance, a firm planning to launch a new device with Bluetooth connectivity and companion mobile applications must ensure compliance with data privacy and tobacco advertising laws, which can differ substantially between markets like Europe and APAC. Success depends on balancing innovation, such as developing biodegradable consumables, with the strategic management of these regulatory and fiscal hurdles.

What will be the Size of the Heat-not-burn Tobacco Products Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Heat-not-burn Tobacco Products Market Segmented?

The heat-not-burn tobacco products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Devices

- Capsules

- Vaporizers

- Distribution channel

- Offline

- Online

- Flavor

- Traditional tobacco

- Mint

- Fruit

- End-user

- Individuals

- Commercial

- Geography

- APAC

- Japan

- South Korea

- China

- Europe

- Italy

- Germany

- UK

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Product Insights

The devices segment is estimated to witness significant growth during the forecast period.

The devices segment is foundational, representing the electronic hardware that facilitates tobacco heating. These units are engineered with high-precision electronic heating elements and advanced temperature regulation to maintain a consistent thermal environment.

Modern designs leverage Bluetooth connectivity and companion mobile applications for a personalized user experience. The market is also seeing a shift towards more sustainable solutions, including the use of biodegradable consumables to improve the overall environmental footprint.

These technological leaps reinforce market dominance, as evidenced by a 38% growth in volumes for certain advanced systems, even in markets with fiscal hurdles like tax adjustments that can increase consumer costs by up to 95%.

This focus on a robust hardware ecosystem is crucial for recurring revenue from compatible capsules.

The Devices segment was valued at USD 25.43 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Heat-not-burn Tobacco Products Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is predominantly led by the APAC region, which is projected to contribute 49.9% of the total incremental growth.

This dominance is driven by early adoption and strong cultural acceptance in countries like Japan, where some systems have already achieved a 14.4% market share.

The region benefits from a large population of adult smokers and an openness to new technology, supported by a robust manufacturing sector for both hardware and consumables.

In Europe, growth is propelled by high excise taxes on traditional cigarettes and a favorable regulatory outlook in key countries.

North America is characterized by a sophisticated regulatory process, while the Middle East and Africa show strong demand for premium products. These regional differences create a complex but opportunity-rich environment for market participants.

Market Dynamics

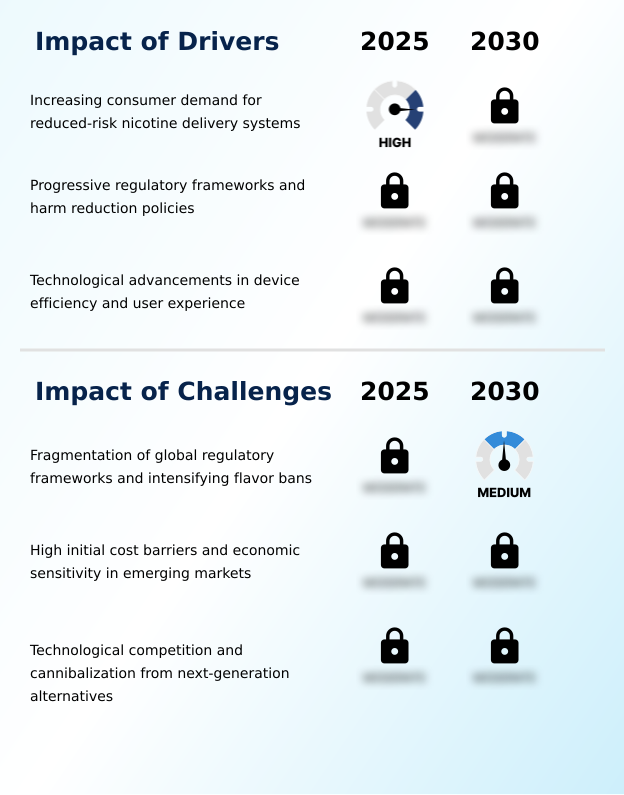

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global heat-not-burn tobacco products market is navigating a complex interplay of technological innovation and regulatory pressures. A key focus is the impact of induction heating on flavor consistency, which represents a significant leap from older technologies. This is complemented by advancements in aerosol delivery optimization and leveraging AI for thermal management optimization to enhance performance.

- The role of companion mobile applications in user tracking has become central to user experience enhancement via smart connectivity. However, companies face significant challenges in managing fragmented regulatory landscapes, particularly concerning compliance challenges with the Tobacco Products Directive and the impact of flavor bans on consumer conversion.

- Strategically, firms are exploring cross-industry collaboration in aroma release technology and developing sustainability trends in heat-not-burn packaging. On the operational front, balancing hardware costs and consumer affordability is crucial, as is developing strategies for overcoming high initial capital expenditure. The competitive landscape is defined by technological competition from next-generation alternatives and the risk of market cannibalization from nicotine pouch products.

- For continued growth, differentiating heat-not-burn from e-vapor systems through superior experience and clear communication is essential, supported by robust e-commerce strategies for online sales channels and efficient supply chain logistics for offline distribution, especially in a market where consumable volumes have shown the potential to increase by over 38% in a single year.

What are the key market drivers leading to the rise in the adoption of Heat-not-burn Tobacco Products Industry?

- A primary market driver is the increasing consumer demand for reduced-risk nicotine delivery systems.

- The primary market driver is a profound consumer shift toward reduced-risk alternatives, driven by a wellness-prioritizing demographic.

- Heat-not-burn technology appeals to this group by generating a nicotine-containing aerosol at temperatures below 350 degrees Celsius, avoiding the combustion process and its associated chemicals.

- This harm reduction approach is increasingly supported by risk-proportionate regulatory frameworks, which encourage the transition to a smoke-free future. Technological advancements, such as improved thermal management systems and cross-industry collaboration on hardware, further propel the market.

- The perception of these products as being less harmful is a decisive factor for more than half of the current user base, highlighting the importance of scientific validation and clear consumer communication in driving adoption.

What are the market trends shaping the Heat-not-burn Tobacco Products Industry?

- The market is witnessing a significant trend toward the integration of advanced induction heating technology, coupled with the incorporation of smart connectivity features in next-generation devices.

- Key trends are reshaping the market, with a strong focus on advanced induction heating systems that ensure a more uniform temperature for a consistent sensory experience. This technological shift is part of a broader premiumization trend, where devices are positioned as lifestyle accessories with high-end finishes.

- As companies pivot toward circular economy models, the development of biodegradable consumables and the reduction of the environmental footprint have become strategic priorities. These initiatives are crucial for gaining a competitive edge, especially in markets where sustainability influences purchasing decisions.

- In some regions, advanced systems have already captured a 14.4% market share, while new product launches have demonstrated the ability to increase consumable volumes by over 38%, underscoring the impact of continuous innovation on consumer adoption.

What challenges does the Heat-not-burn Tobacco Products Industry face during its growth?

- A key challenge affecting industry growth is the fragmentation of global regulatory frameworks and the concurrent intensification of flavor bans.

- The market faces significant headwinds from a fragmented regulatory landscape and intensifying bans on characterizing flavors. This creates logistical and compliance challenges for global firms, forcing them to tailor product portfolios to a patchwork of local laws. For instance, abrupt fiscal and legislative hurdles, such as a tax rate of 95% on the sales price, can stifle market penetration.

- Another challenge is the high initial capital expenditure for consumers, which is a deterrent in price-sensitive regions. This economic tension is exacerbated by competition from other next-generation nicotine delivery systems, leading to risks of market cannibalization.

- Without continuous innovation to offset these challenges, long-term growth could be constrained, as user attrition can be high if devices are perceived as too complex.

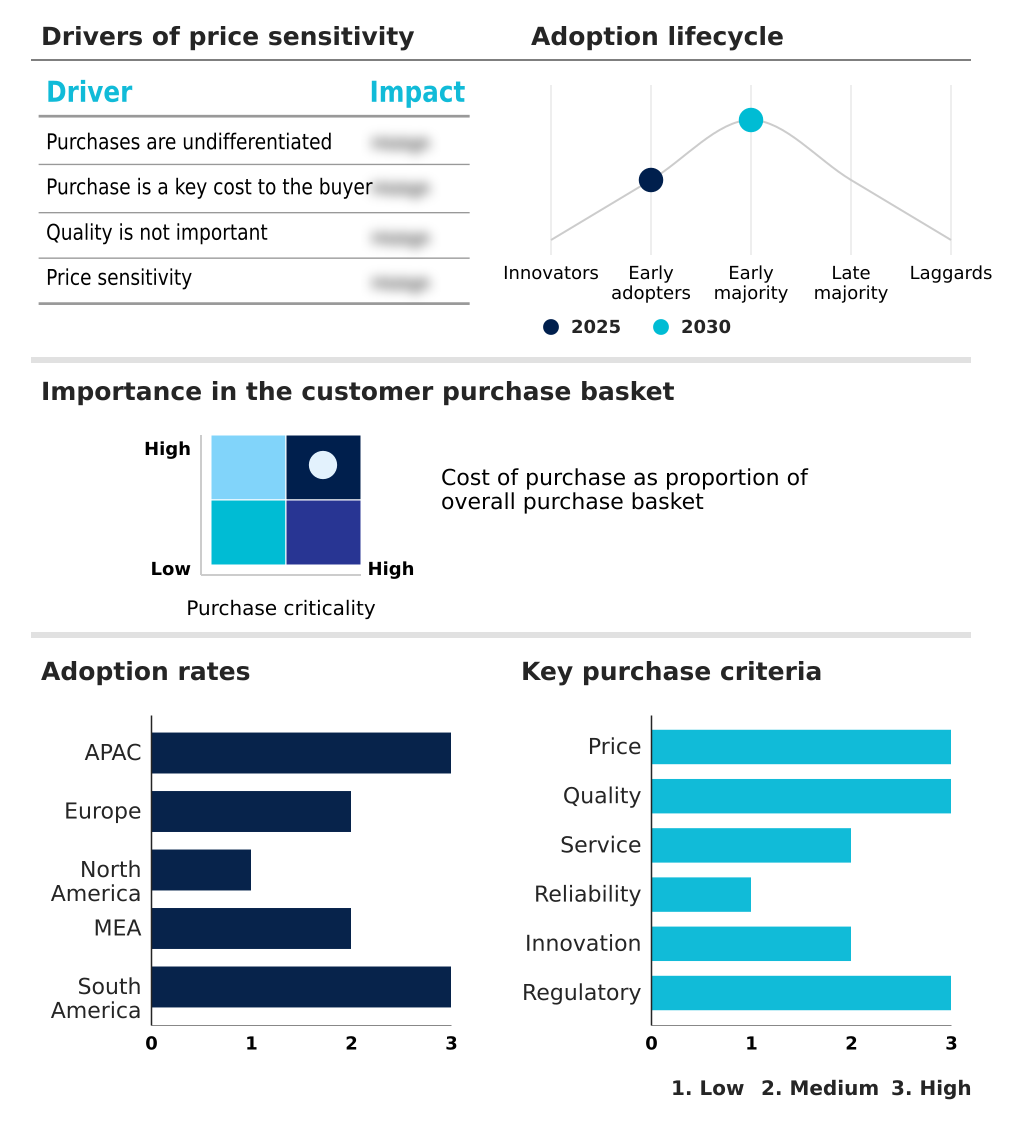

Exclusive Technavio Analysis on Customer Landscape

The heat-not-burn tobacco products market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heat-not-burn tobacco products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Heat-not-burn Tobacco Products Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, heat-not-burn tobacco products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALD Group Ltd - Key offerings include advanced heating technology devices, OEM solutions, and comprehensive vape systems designed for the evolving non-combustible product landscape.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALD Group Ltd

- British American Tobacco Plc

- Buddy Technology Development

- CFU Group

- HiTaste Technology Co Ltd

- Imperial Brands Plc

- ISMODJO Technology Co Ltd

- Japan Tobacco Inc.

- Joecig Technology Co Ltd

- Kamry Technology Co Ltd

- KT and G Corp.

- Lambda Smoke Inc

- Mysmok Electronic Technology

- Philip Morris International

- Pluscig Technology Co Ltd

- Shenzhen Kanger Technology

- SMISS Technology Co. Ltd.

- SMOORE International Holdings

- Xomok Technology Co Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heat-not-burn tobacco products market

- In August 2024, the United States Food and Drug Administration (FDA) issued updated final rules regarding the prohibition of the sale of tobacco products to persons younger than 21.

- In September 2024, The Biden Administration announced an indefinite delay in finalizing the Food and Drug Administration rule that sought to prohibit menthol cigarettes.

- In May 2025, Japan Tobacco International (JTI) acquired a controlling stake in Flavour Warehouse, a leading independent vape company with a strong e-commerce infrastructure.

- In May 2025, British American Tobacco Plc launched glo Hilo, a new premium heated tobacco device in Japan featuring TurboStart technology and connectivity with the myglo app.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heat-not-burn Tobacco Products Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 45.2% |

| Market growth 2026-2030 | USD 214688.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 35.7% |

| Key countries | Japan, South Korea, China, Indonesia, Philippines, Malaysia, Italy, Russia, Germany, UK, Poland, France, US, Canada, Mexico, Saudi Arabia, UAE, South Africa, Turkey, Egypt, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The heat-not-burn tobacco products market is defined by rapid technological advancement and a complex competitive ecosystem. At the core are induction heating systems, which have largely replaced older resistive heating elements to provide a more uniform temperature and consistent nicotine-containing aerosol.

- Boardroom decisions are increasingly focused on the transition to sustainable materials, such as biodegradable filters and advanced cellulose acetate filters, to address regulatory pressures and consumer expectations. Hardware innovation is paramount, with a focus on high-capacity lithium-ion batteries, durable electronic heating elements, and precise temperature regulation.

- Smart features like Bluetooth connectivity and companion mobile applications that use biometrically secured device data allow for enhanced heat management and aerosol delivery. The development of a new matrix-based fragrance carrier for stable aroma release from flavored tobacco sticks showcases the level of sophistication.

- The competitive edge is maintained through a combination of proprietary reconstituted tobacco sheets, single-origin tobacco sticks, and unique flavor-release capsules embedded with menthol-infused thread. Future growth hinges on navigating the Premarket Tobacco Product Application process to secure modified risk claims, a factor that has enabled some platforms to achieve a 14.4% share in key markets.

What are the Key Data Covered in this Heat-not-burn Tobacco Products Market Research and Growth Report?

-

What is the expected growth of the Heat-not-burn Tobacco Products Market between 2026 and 2030?

-

USD 214.69 billion, at a CAGR of 45.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Devices, Capsules, and Vaporizers), Distribution Channel (Offline, and Online), Flavor (Traditional tobacco, Mint, and Fruit), End-user (Individuals, and Commercial) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing consumer demand for reduced-risk nicotine delivery systems, Fragmentation of global regulatory frameworks and intensifying flavor bans

-

-

Who are the major players in the Heat-not-burn Tobacco Products Market?

-

ALD Group Ltd, British American Tobacco Plc, Buddy Technology Development, CFU Group, HiTaste Technology Co Ltd, Imperial Brands Plc, ISMODJO Technology Co Ltd, Japan Tobacco Inc., Joecig Technology Co Ltd, Kamry Technology Co Ltd, KT and G Corp., Lambda Smoke Inc, Mysmok Electronic Technology, Philip Morris International, Pluscig Technology Co Ltd, Shenzhen Kanger Technology, SMISS Technology Co. Ltd., SMOORE International Holdings and Xomok Technology Co Ltd

-

Market Research Insights

- Market dynamics are heavily influenced by the strategic push toward a smoke-free future, with a focus on reduced-risk alternatives and harm reduction policies. Consumer sentiment analysis reveals a strong preference for devices that offer a clean and consistent experience, leading to user attrition rates of over 25% for systems with poor performance.

- The value proposition is challenged by high initial capital expenditure, but this is offset by the long-term benefits of reduced toxicant exposure. In some regions, a risk-proportionate regulatory framework has been adopted, while in others, fiscal and legislative hurdles, such as a 95% tax on sales price, create significant market pressure.

- This fragmented regulatory landscape requires companies to maintain high agility in their go-to-market strategies.

We can help! Our analysts can customize this heat-not-burn tobacco products market research report to meet your requirements.

RIA -

RIA -