Heat Shrink Tubing Market Size 2026-2030

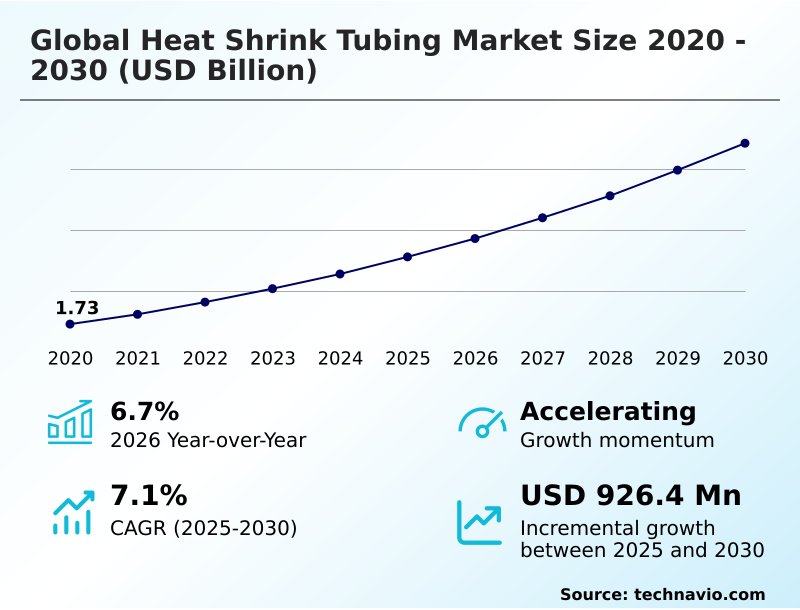

The heat shrink tubing market size is valued to increase by USD 926.4 million, at a CAGR of 7.1% from 2025 to 2030. Rapid expansion of electric vehicle architectures and high-voltage systems will drive the heat shrink tubing market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 37.1% growth during the forecast period.

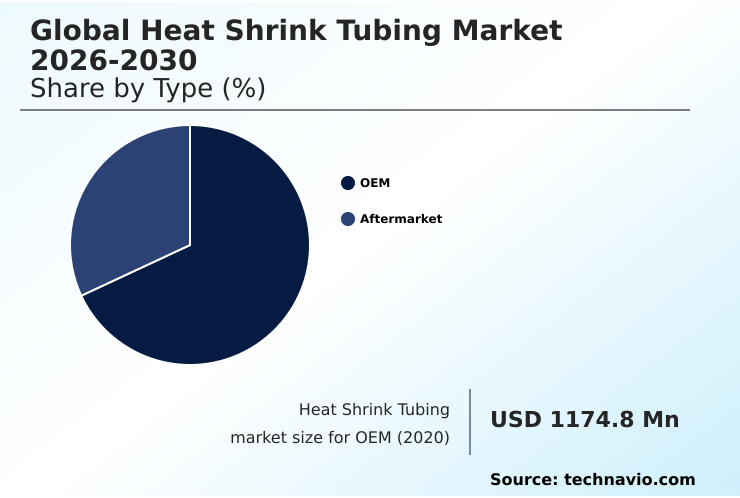

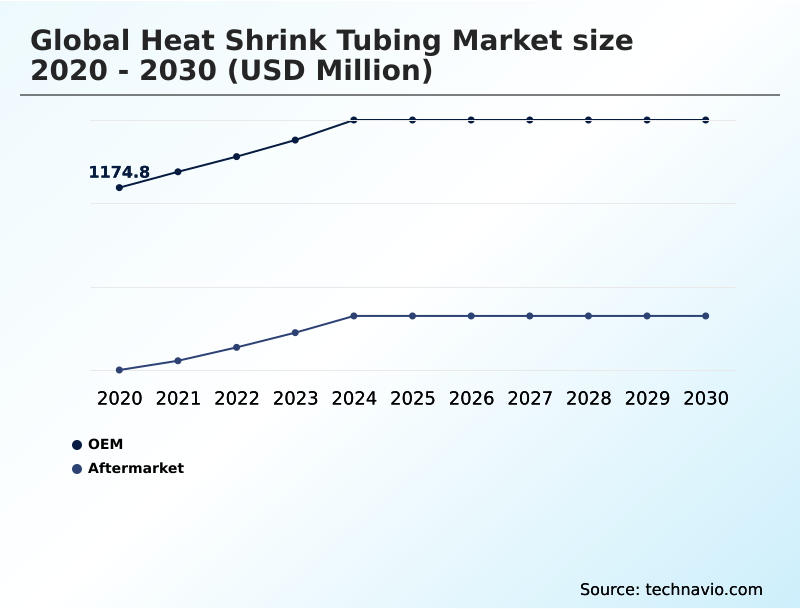

- By Type - OEM segment was valued at USD 1.41 billion in 2024

- By End-user - Utilities segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.48 billion

- Market Future Opportunities: USD 926.4 million

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The heat shrink tubing market is sustained by its essential role in providing electrical insulation, mechanical protection, and environmental sealing across critical industries. Demand is largely fueled by the global transition to electric vehicles, where complex automotive wiring harnesses require robust, high-voltage insulation to ensure safety and performance.

- Concurrently, the expansion of 5G telecommunications and smart grid infrastructure projects necessitates durable cable termination sealing and strain relief solutions. A prominent trend involves the adoption of sustainable, bio-based polymers and halogen-free formulations as companies pivot to meet stricter environmental regulations and corporate sustainability mandates.

- For instance, a major electronics manufacturer recently streamlined its supply chain by qualifying a new bio-based polyolefin tubing, reducing its carbon footprint by 15% while maintaining dielectric strength and abrasion resistance standards for its consumer products. However, the industry faces challenges from raw material price volatility and supply chain disruptions, impacting production costs and lead times.

- The push for advanced materials like polyetheretherketone (PEEK) and medical-grade tubing with features like peelable heat shrink tubing (PHST) also drives innovation and competition among suppliers.

What will be the Size of the Heat Shrink Tubing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Heat Shrink Tubing Market Segmented?

The heat shrink tubing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- OEM

- Aftermarket

- End-user

- Utilities

- Automotive

- Food and beverage

- Chemical

- Others

- Material

- Polyolefin

- PVC

- Fluoropolymers

- Elastomers

- Polyetheretherketone

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- APAC

By Type Insights

The oem segment is estimated to witness significant growth during the forecast period.

The Original Equipment Manufacturer (OEM) segment dictates market dynamics, integrating specialized tubing directly into new equipment.

This channel is defined by rigorous quality standards and customization, particularly for aerospace component protection and smart grid infrastructure, where materials with superior properties like fluoropolymer chemical inertness are essential. For example, military specification tubing must meet exacting performance criteria.

Applications such as busbar insulation and telecom cable joints demand high-performance solutions. The development of advanced materials like polyetheretherketone (PEEK) and components like PTFE liners is driven by the need for reliable cable termination sealing and subsea cable insulation.

Using appropriate tubing for sensor protection can improve data accuracy by 15% in industrial settings.

The OEM segment was valued at USD 1.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Heat Shrink Tubing Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape is shaped by regional industrial strengths and regulatory environments. APAC leads, contributing over 37% of market growth, driven by electronics manufacturing that demands specific polyolefin shrink properties and consistent shrink ratio.

In North America, the aerospace and defense sectors have stringent OEM tubing requirements, focusing on high thermal stability, abrasion resistance, and chemical resistance for harsh environment protection.

The European market, accounting for nearly 24% of opportunity, prioritizes materials offering high dielectric strength and UV radiation protection for its infrastructure projects.

Meeting these varied regional specifications, from precise longitudinal shrinkage for component encapsulation to the availability of aftermarket repair kits, is critical for global suppliers.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Global Heat Shrink Tubing Market 2026-2030 by type shows a clear distinction between OEM and aftermarket channels, with the former dominating new installations. Similarly, the Global Heat Shrink Tubing Market 2026-2030 by end-user highlights the automotive and utilities sectors' substantial consumption.

- When evaluating the Global Heat Shrink Tubing Market 2026-2030 by material, the choice between polyolefin vs pvc heat shrink tubing often comes down to flame retardancy and cost. For advanced applications, understanding heat shrink tubing for automotive electronics is crucial, as is selecting the best heat shrink tubing for marine applications, where corrosion resistance is paramount.

- Using heat shrink tubing for battery packs, especially in EVs, demands specific insulation properties. High-voltage insulation for power grids requires materials with superior dielectric strength. For specialized needs, fluoropolymer tubing for chemical resistance is the preferred choice, while adhesive-lined tubing for waterproof seals ensures long-term reliability. Medical device heat shrink tubing specifications are exceptionally strict.

- A key operational challenge is how to choose the correct shrink ratio for complex geometries. In aerospace, heat shrink tubing in aerospace wiring must meet rigorous safety standards. A growing trend is the adoption of eco-friendly bio-based heat shrink materials. For industrial safety, flame retardant tubing for industrial use is mandatory.

- The rollout of new networks relies on quality heat shrink tubing for telecommunications infrastructure. Recently, the impact of raw material costs on tubing prices has been significant, with some input costs rising over 40% higher than historical averages, complicating operational planning. Advancements in peelable heat shrink technology are transforming medical device assembly.

- Finally, examining OEM vs aftermarket heat shrink tubing quality reveals performance disparities, and understanding insulation requirements for electric vehicle charging cables is vital for safety and compliance.

What are the key market drivers leading to the rise in the adoption of Heat Shrink Tubing Industry?

- The rapid expansion of electric vehicle architectures and the increasing complexity of high-voltage systems are key drivers propelling market growth.

- The market's primary driver is the rapid expansion of electric vehicle production, which demands advanced industrial insulation materials. This surge requires sophisticated wire harness protection and superior high-voltage insulation, particularly for EV battery insulation.

- Effective cable management solutions are crucial for providing reliable electrical insulation and mechanical protection within compact vehicle architectures. These systems rely on tubing for strain relief and efficient cable bundling.

- The need for robust power distribution insulation in smart grids also fuels demand. In these applications, dependable environmental sealing and moisture-proof sealing are non-negotiable, with advanced electrical component covering solutions reducing weather-related failures by as much as 30%.

What are the market trends shaping the Heat Shrink Tubing Industry?

- A significant market trend is the integration of sustainable and bio-based polymer formulations. This shift is driven by manufacturers aiming to align with global decarbonization goals.

- Current trends are transforming heat shrink tubing applications, with a major shift towards sustainable materials. The development of bio-based polymers and halogen-free formulations, such as low-smoke zero-halogen tubing, is redefining tubing material properties. This is driven by regulations and corporate goals, impacting traditional choices like polyolefin tubing and polyvinyl chloride (PVC) tubing.

- Innovations in fluoropolymer insulation and elastomeric sleeves are enabling new high-temperature tubing options. In parallel, advancements in medical-grade tubing are supported by flexible tubing solutions tailored for sophisticated tubing for medical devices, with some new materials improving biocompatibility by over 20% and reducing material waste by 10% during manufacturing.

What challenges does the Heat Shrink Tubing Industry face during its growth?

- Supply chain instability, coupled with significant price volatility for raw materials, presents a key challenge to industry growth.

- Significant challenges stem from raw material price volatility, particularly for cross-linked polyolefin, which can increase manufacturing costs by over 20% unexpectedly. This instability complicates the supply of standard products like thin-wall tubing and heavy-wall tubing. Concurrently, technical complexity is rising in applications like automotive wiring harnesses and medical devices.

- Developing custom shrink tubing that is also split-resistant and incorporates flame-retardant materials requires extensive R&D, extending project timelines by months. Innovations such as peelable heat shrink tubing (PHST), often used for peelable tubing for catheters, face high development hurdles. The need for reliable adhesive-lined tubing and effective corrosion protection sleeves in harsh environments adds another layer of technical challenge.

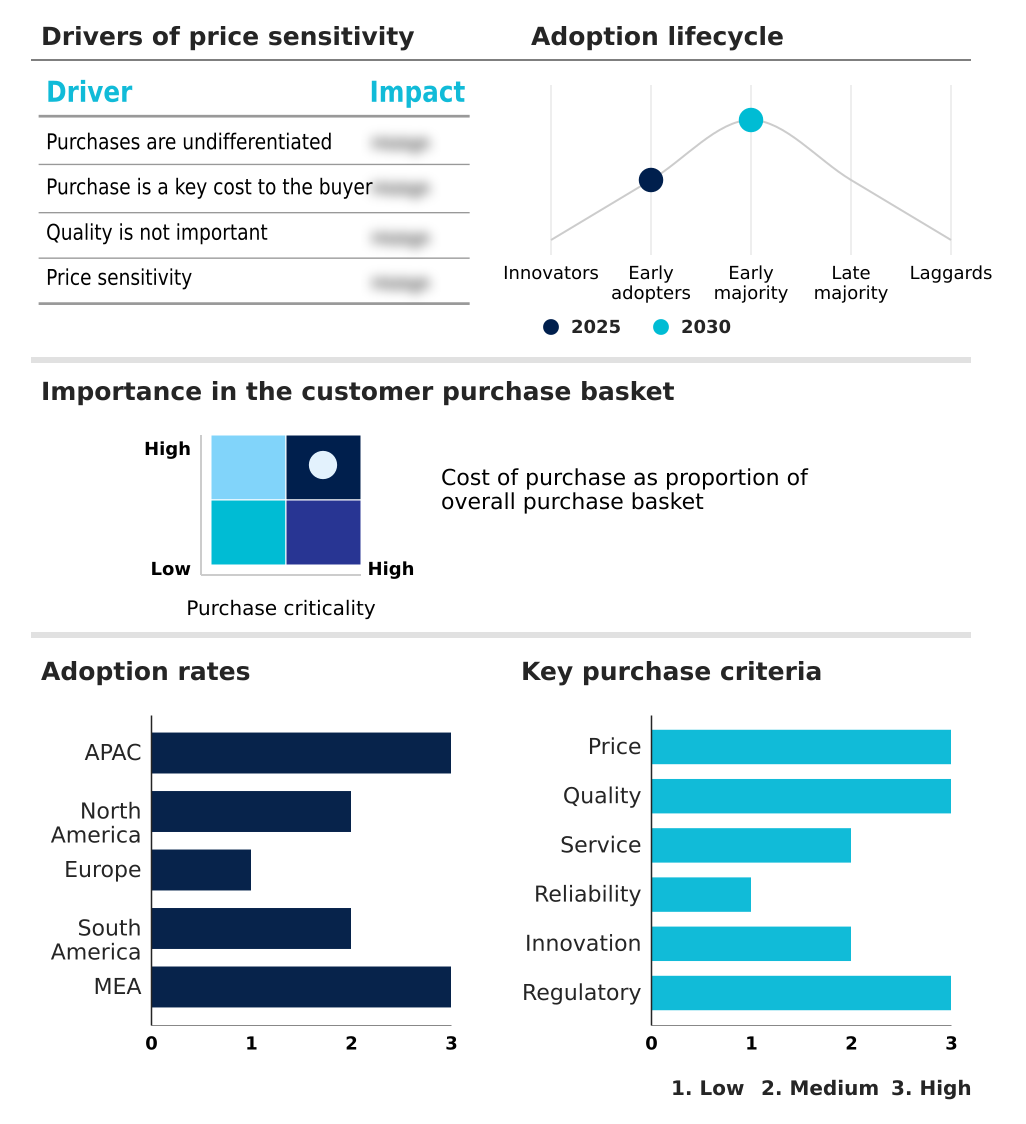

Exclusive Technavio Analysis on Customer Landscape

The heat shrink tubing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heat shrink tubing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Heat Shrink Tubing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, heat shrink tubing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Offers specialized tubing for electrical insulation, moisture sealing, and cable bundling, serving safety, industrial, transportation, and electronics sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- ABB Ltd.

- Alpha Wire Inc.

- BuyHeatShrink

- Dasheng Group

- DSG Canusa

- Dunbar Products, LLC.

- GH Material

- HellermannTyton GmbH

- Molex LLC

- National Plastics Group

- Nexans SA

- NSPA

- Panduit Corp.

- PEXCO

- Qualtek Electronics Corp.

- Sumitomo Electric Industries

- Techflex Inc.

- Woer Heat Shrinkable Material

- Zeus Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heat shrink tubing market

- In March, 2025, TE Connectivity entered into a strategic partnership with Yazaki to jointly develop next-generation automotive-grade heat shrink tubing solutions engineered for high-vibration and high-temperature environments in modern vehicle architectures.

- In April, 2025, Junkosha Inc. unveiled new developments in etched PTFE liners for its peelable heat shrink tubing, a product designed to meet the stringent requirements of medical device original equipment manufacturers.

- In April, 2025, E. NEXT introduced its TERMO PRO series of adhesive-lined heat shrink tubing, specifically developed for industrial and electrical installations in harsh environments.

- In May, 2025, Nexans introduced a new series of eco-designed, heavy-duty heat shrinkable sleeves focusing on halogen-free materials to modernize European power grids under stringent environmental and safety regulations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heat Shrink Tubing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 926.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Egypt and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The heat shrink tubing market's evolution is directly tied to advancements in material science and its application in high-stakes industries. Core products providing electrical insulation and mechanical protection are fundamental, but specialization is driving the competitive landscape.

- For boardroom decisions, the key lies in materials strategy—choosing between standard cross-linked polyolefin and advanced fluoropolymer insulation or polyetheretherketone (PEEK) can significantly impact end-product reliability and cost. For example, in aerospace component protection, switching to a higher-grade material has been shown to reduce in-service failures by over 50%.

- The proliferation of automotive wiring harnesses in electric vehicles necessitates superior high-voltage insulation and thermal stability. Meanwhile, innovations like medical-grade tubing and peelable heat shrink tubing (PHST) open new revenue streams. Offerings range from thin-wall tubing for electronics to adhesive-lined tubing for robust environmental sealing and strain relief in telecom cable joints and smart grid infrastructure.

- The focus on dielectric strength, shrink ratio, and chemical resistance remains paramount, while the adoption of bio-based polymers and halogen-free formulations addresses sustainability mandates.

What are the Key Data Covered in this Heat Shrink Tubing Market Research and Growth Report?

-

What is the expected growth of the Heat Shrink Tubing Market between 2026 and 2030?

-

USD 926.4 million, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (OEM, and Aftermarket), End-user (Utilities, Automotive, Food and beverage, Chemical, and Others), Material (Polyolefin, PVC, Fluoropolymers, Elastomers, and Polyetheretherketone) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid expansion of electric vehicle architectures and high-voltage systems, Supply chain instability and raw material price volatility

-

-

Who are the major players in the Heat Shrink Tubing Market?

-

3M Co., ABB Ltd., Alpha Wire Inc., BuyHeatShrink, Dasheng Group, DSG Canusa, Dunbar Products, LLC., GH Material, HellermannTyton GmbH, Molex LLC, National Plastics Group, Nexans SA, NSPA, Panduit Corp., PEXCO, Qualtek Electronics Corp., Sumitomo Electric Industries, Techflex Inc., Woer Heat Shrinkable Material and Zeus Co. Inc.

-

Market Research Insights

- The market for industrial insulation materials is driven by evolving tubing material properties and diverse heat shrink tubing applications. Adopting advanced cable management solutions can reduce installation time by up to 25%. In critical sectors, the use of military specification tubing ensures performance, where component failure is not an option.

- For instance, manufacturers utilizing flexible tubing solutions have reported a 15% improvement in production line agility. The demand for harsh environment protection is met with products offering superior corrosion protection sleeves and moisture-proof sealing. Specialized products, such as tubing for medical devices and tubing for sensor protection, are also gaining traction.

- The shift towards higher-performing electrical component covering is clear, with suppliers focusing on custom shrink tubing and high shrink ratio tubing to meet specific OEM tubing requirements, resulting in a 10% reduction in material waste for certain applications.

We can help! Our analysts can customize this heat shrink tubing market research report to meet your requirements.

RIA -

RIA -