High Power Charger For Electric Vehicle Market Size 2024-2028

The High Power Charger For Electric Vehicle Market size is estimated to grow by USD 117.48 billion, at a CAGR of 58.37% between 2023 and 2028. The market is experiencing significant growth, driven by increasing consumer demand and favorable regulations. This trend is spurring the need for robust and reliable EV charging infrastructure. Key offerings in this space include fast-charging stations, smart charging systems, and wireless charging technology. Favorable standards for electrical connectors, such as the Combined Charging System (CCS) and the Combined Charging System Type 2 (CCS Type 2), ensure compatibility and interoperability between charging stations and EV models. As EV sales continue to rise, the importance of well-built and efficient charging infrastructure becomes increasingly crucial to support the growing number of electric vehicles on the road.

What will be the High Power Charger for Market Size During the Forecast Period?

_market_size_abstract_2023_v1.jpg)

To learn more about this report, Request Free Sample

Market Dynamics

The market is pivotal in accelerating the adoption of Battery Electric Vehicles (BEVs) worldwide. As auto sales transition towards sustainable options, non-renewable energy giants are investing in infrastructure compatible with RFID technology and cloud-computing platforms to enhance electric car charging infrastructure under initiatives like the FAME India Scheme. High Power Chargers play a crucial role in supporting the electric mobility industry, enabling fast-charging systems alongside traditional charging stations to facilitate long-distance travel and ensure mainstream EV adoption. They cater to both the public and private segments, accommodating various connector types, including CHAdeMO, for efficient charging solutions in the sustainable transportation sector, reducing dependence on fossil fuel-dependent cars, and promoting environmental conservation.

Key Market Driver

The increasing EV sales are notably driving market growth. Incentives and subsidies from governments and regulators around the world are driving the growth of the electric vehicles market. Governments in various countries are giving financial incentives to buyers according to battery size. For example, the Sustainable Energy Authority of Ireland (SEAI) is offering buyers up to USD 5,500 to USD 6,000 subsidy, as well as exemption from vehicle registration tax.

In the US, the federal government is giving hefty tax credits for new battery and plug-in hybrid electric vehicles, ranging from USD 2,500 to USD 7,500, depending on the battery capacity. All battery EVs are eligible for the full USD 7,500, but some plug-in hybrid models with smaller batteries qualify for less. In addition, Italian buyers of fully electric or hybrid vehicles are exempt from annual registration tax for five years after vehicle purchase. Five years after that, they could benefit from a 75% reduction in the equivalent tax rate on most petrol cars. Such tax incentives will increase the demand and drive the growth of the market during the forecast period.

Significant Market Trend

Recent developments in high power chargers for EVs are a key trend influencing the market. The market is seeing an increase in new product launches. The addition of new products will encourage more consumers to purchase a variety of high-power chargers according to their needs. Align with market trends and analysis, the increasing number of new product launches also increases competition in the market, leading to innovation and differentiation.

New product launches encourage consumers to try different products, and manufacturers are also focusing on developing new products such as a revolutionary all-in-one (EV) charger that offers end-users the fastest charging experience, the launch of a new Chinese-made V3 supercharger station by Tesla motors, the launch of latest EV charging infrastructure portfolio in New Zealand via a partnership between Siemens and YHI energy. Such developments are expected to boost the growth of the market during the forecast period.

Major Market Challenge

The lack of charging infrastructure in potential markets is challenging the market. Infrastructure plays a key role in selling. Finding a suitable charging infrastructure remains the biggest challenge for owners. Unlike internal combustion engine (ICE) vehicle owners, EV owners do not benefit from standardized refueling facilities. Poor communication of needs and requirements for building easily accessible charging networks is a major concern in the market. For example, finding EV charging infrastructure is the biggest hurdle preventing the mass adoption of EVs in India. Charging infrastructure is either difficult to implement or non-existent in most cities where EVs are the most viable mode of transportation. However, Mahindra and Mahindra Ltd have been unable to grow EV sales in 2022, mainly due to insufficient urban charging infrastructure. Electric bikes could not be sold in India for the same reason. Public awareness campaigns on EV prevalence and required charging infrastructure are needed for public and private companies to better understand EVs in such countries.

Governments play a key role in the development of EV charging infrastructure. Governments around the world offer tax breaks and subsidies for the purchase. However, their focus on developing and deploying better-charging infrastructure is marginal. For example, Norway, the Netherlands, and Denmark are making rapid progress in subsidizing EV sales and developing EV charging infrastructure, while countries such as Germany and the United Kingdom have seen a significant increase in infrastructure investment compared to total EV sales per year. There are not yet enough subsidies to drive development. These factors will, therefore, challenge the growth of the market during the forecast period.

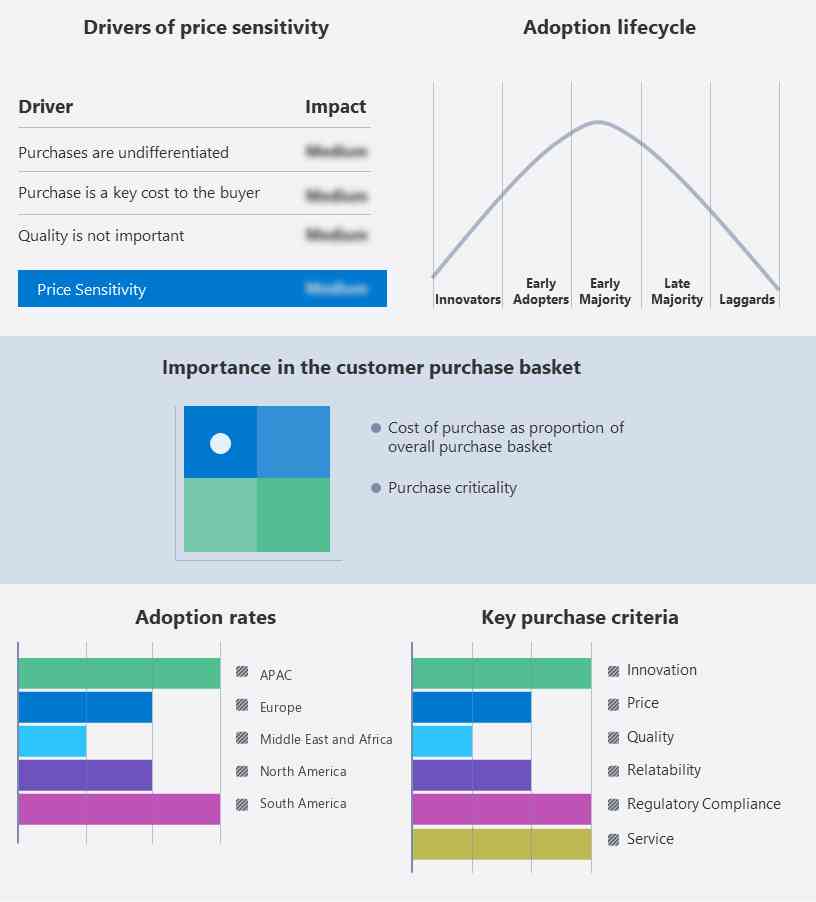

Key Market Customer Landscape

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Who are the Major Market companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ABB Ltd: The company provides a control room, charging infrastructure, and industrial software solutions along with that it also provides low-voltage products and systems.

The market analysis and report also includes detailed analyses of the competitive landscape of the market growth and forecasting and information about 15 market companies, including:

- Blink Charging Co.

- BorgWarner Inc.

- Chargemaster NZ

- ChargePoint Inc.

- ClipperCreek Inc.

- EV Safe Charge Inc.

- EVBox BV

- FLO Services USA Inc.

- Hyundai Motor Co.

- Infineon Technologies AG

- Leviton Manufacturing Co. Inc.

- Robert Bosch GmbH

- Shenzhen Shenghong Electric Co. Ltd.

- Siemens AG

- Tesla Inc.

- VOLTERIO GmbH

- WiTricity Corp.

- Zhejiang Benyi Electrical Co. Ltd.

- Tata Motors Ltd.

Qualitative and quantitative analysis of vendors has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize vendors as dominant, leading, strong, tentative, and weak.

Market Segmentation

By Type

The market share growth by the 50 KW-less than 150 KW segment will be significant during the forecast period. Vendors mainly use high-power chargers for their PHEV or BEV electric vehicles to ensure higher performance. High-power chargers are used in these vehicles to provide fast charging capabilities. Popular PHEVs or BEVs with high-performance engines include the BMW i3 (125 KW), BMW i8 (98 KW), GM Spark EV (105 KW), GM Bolt EV (150 KW), Mercedes-Benz E- B-class drive (132 KW). As the demand increases, so does the need for high-performance chargers. These chargers can provide more than 50kW of charge to EVs and are typically used to charge EVs with a range of 150km or less. High-power chargers are typically found at public charging stations and can charge in minutes.

_market_segments_abstract_2023_v2.jpg)

Get a glance at the market contribution of various segments Request a PDF Sample

The 50 KW-less than 150 KW segment was valued at USD 1.75 billion in 2018. Using a high-capacity charger has several advantages. First, drivers can quickly charge their car batteries. This is especially useful while traveling long distances. Second, high-power chargers can significantly reduce the time required to charge. And third, it can extend the range by providing higher charging rates. These factors will drive the segment of the High Power Charger For EV Market to grow from HE 50KW to below 150KW during the forecast period.

By Region

_market_regions_abstract_2023_geo_v2.jpg)

For more insights on the market share of various regions Request PDF Sample now!

APAC is estimated to contribute 43% to the growth of the market during the forecast period. Technavio’s analysts have elaborately explained the regional market growth and trends that shape the market during the forecast period. China will have the most EVs deployed in 2022 and is expected to produce the most EVs in APAC in 2027. China, Japan, and South Korea are three countries in Asia that are world leaders in the field of this and electromobility. South Korea is technologically strong, but Japan and China hold strong positions in terms of production and market size. The market for high-capacity EV chargers growing in China, where the world's largest number of EVs are sold. In addition to electric cars and private cars, public transport in China is also electrified. Such deployment of electric buses by governments for private or public transport, fueled by the growing need to reduce air pollution in countries across APAC, will result in large-capacity vehicles. Demand for chargers is expected to spur the growth of the Market in APAC during the forecast period.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion " for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type Outlook

- 50 KW-less than 150 KW

- 150 KW-350 KW

- 350 KW and above

- Application Outlook

- Plug-in hybrid electric vehicle

- Battery electric vehicle

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in the below market reports

-

Electric Vehicle Charger Market: Analysis APAC, North America, Europe, South America, Middle East and Africa - US, Canada, China, Germany, UK - Size and Forecast

-

Electric Vehicle (EV) Charging Station Market: Analysis APAC, Europe, North America, South America, Middle East and Africa - China, Germany, UK, France, US - Size and Forecast

-

Electric Vehicle (EV) Charging Infrastructure Market: Analysis APAC, North America, Europe, South America, Middle East and Africa - US, China, Japan, Germany, UK - Size and Forecast

Market Analyst Overview

The market is rapidly evolving with advancements in vehicle electrification and stringent safety norms driving demand for advanced technology solutions. Catering to the 50-150 kW charger category, innovations like the Velion DC Fast Charger and Level 3 DC Fast Chargers from Hitachi Industrial Products are pivotal in expanding electric vehicle infrastructure worldwide. These chargers address high-power technology needs while overcoming space constraints and optimizing energy management with competitive power tariffs. As consumer sentiment shifts toward environmental awareness and reducing environmental pollution and greenhouse gases, the market emphasizes green energy solutions and biofuels integration supported by regulatory bodies like the California Air Resources Board promoting zero-emission vehicles. Integrated battery diagnostic systems such as E-HEALTH Charge and E-CHARGE 20 battery charger enhance reliability and efficiency, positioning the DC fast charging system sector for robust growth in the global EV battery charger market.

The introduction of EV fast-charging systems supported by Cloud-Computing Platform marks a significant step towards reducing carbon emissions in urban and transportation planning. As advancements in battery technology and smart grid technology improve, addressing range anxiety and accommodating GB/T standard connector types become priorities. This aligns with government legislation and initiatives by energy providers and infrastructure developers to promote eco-friendly transportation through renewable energy sources. The market introduction of these systems not only impacts the public and private segments but also underscores the industrial impact on achieving environmental goals and fostering environmental consciousness. This integrated approach is pivotal in transitioning away from internal combustion engine vehicles towards sustainable mobility solutions, shaping the future of urban landscapes and global transportation networks. The Level 3 DC Fast Charger integrates high energy capabilities with advanced energy management technologies, enhancing electric motor efficiency while supporting battery diagnostic system and promoting respiratory health through reduced emissions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 58.37% |

|

Market growth 2024-2028 |

USD 117.48 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

41.79 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 43% |

|

Key countries |

China, US, Germany, France, and The Netherlands |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABB Ltd., Blink Charging Co., BorgWarner Inc., Chargemaster NZ, ChargePoint Holdings Inc., ClipperCreek Inc., EV Safe Charge Inc., EVBox BV, FLO Services USA Inc., Hyundai Motor Co., Infineon Technologies AG, Leviton Manufacturing Co. Inc., Robert Bosch GmbH, Sinexcel, Siemens AG, Tata Motors Ltd., Tesla Inc., VOLTERIO GmbH, WiTricity Corp., and Zhejiang Benyi Electrical Co. Ltd. |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting of the market between 2024 and 2028

- Precise estimation of the size of the market size and its contribution to the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Growth of the market industry across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough market growth analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

We can help! Our analysts can customize this report to meet your requirements. Get in touch

RIA -

RIA -