Home Theater Market Size 2025-2029

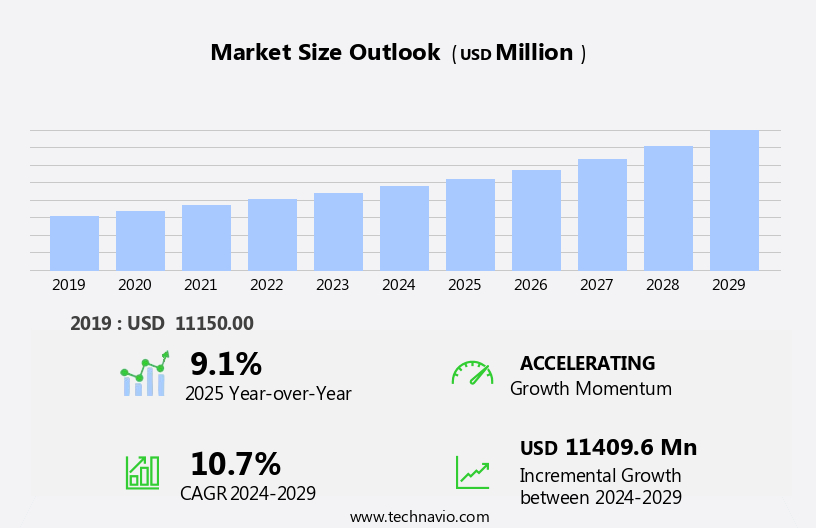

The home theater market size is forecast to increase by USD 11.41 billion at a CAGR of 10.7% between 2024 and 2029.

- The market is experiencing significant growth due to several key trends. One of the primary factors driving market expansion is the increase in disposable income, enabling consumers to invest in premium home entertainment systems. The integration of Bluetooth and Wi-Fi connectivity in home entertainment systems has enabled seamless streaming of audio and video content. Another trend is the rising demand for customized home theater systems, as consumers seek personalized experiences in their entertainment spaces. However, the high cost of home theater systems remains a challenge for some potential buyers. Despite this, the market is expected to continue its growth trajectory, offering opportunities for manufacturers and suppliers to innovate and cater to evolving consumer preferences.

What will be the Size of the Home Theater Market During the Forecast Period?

- The market encompasses a range of home entertainment-related devices, including high-definition television sets, projectors, soundbars, and home theater in a box (HTIB) systems. These technologies continue to evolve, integrating smart home capabilities, Bluetooth and Wi-Fi connectivity, and cloud services. Home theaters increasingly offer access to video streaming platforms, such as Netflix and Disney Plus, and audio content in various formats. Lamp-less technology and surround sound speakers enhance the viewing experience, while sub-woofers provide deep bass. Market growth is driven by advancements in technology, consumer demand for entertainment experiences, and the proliferation of OTT platforms. Home theaters remain a significant investment for consumers seeking to create a cinematic experience in their own homes.

How is this Home Theater Industry segmented and which is the largest segment?

The home theater industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Home theater speakers

- Sound bars

- Distribution Channel

- Offline

- Online

- Connectivity

- Wireless

- Wired

- End-user

- Residential

- Commercial

- Geography

- APAC

- China

- India

- Japan

- South Korea

- North America

- Canada

- US

- Europe

- Germany

- UK

- France

- Italy

- Middle East and Africa

- South America

- APAC

By Product Insights

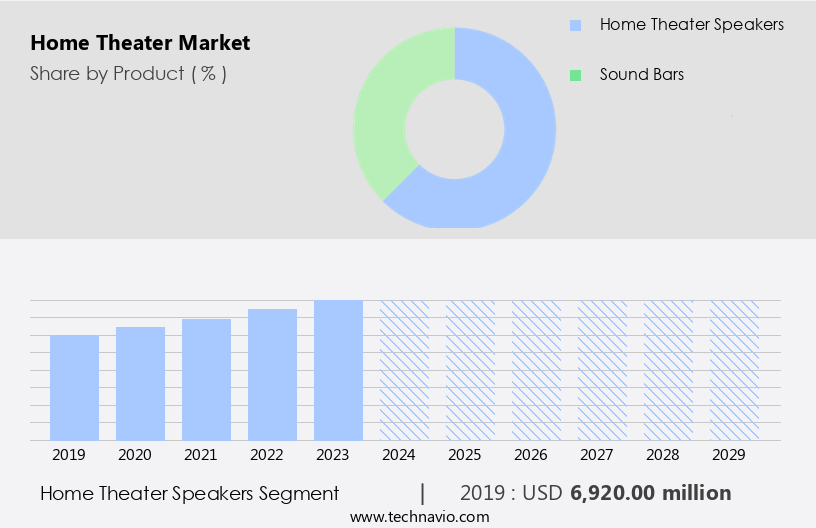

- The home theater speakers segment is estimated to witness significant growth during the forecast period. The market encompasses a range of devices and technologies designed to enhance the in-home entertainment experience. Smart homes, cloud services, video streaming platforms, and audio content are integral components of modern home entertainment systems. Devices such as Bluetooth and Wi-Fi connectivity-enabled soundbars, component systems, wireless subwoofers, and projector screens are popular choices. The sound bar segment is expected to dominate the market due to its affordability and ease of use. Other product types, including component systems and 3D sound systems, cater to niche audiences.

- Installation costs and the availability of counterfeit products may pose challenges for market growth. Despite these hurdles, home theater systems continue to be popular for their surround sound capabilities and theater-like experience. Companies like Bowers and Wilkins, Koninklijke Philips, LG Corporation, and JBL offer a range of high-quality audio equipment. Online retailers and specialty stores are key distribution channels, with platforms like Chromecast and streaming services such as Netflix and Disney Plus driving demand.

Get a glance at the market report of share of various segments Request Free Sample

The home theater speakers segment was valued at USD 6.92 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

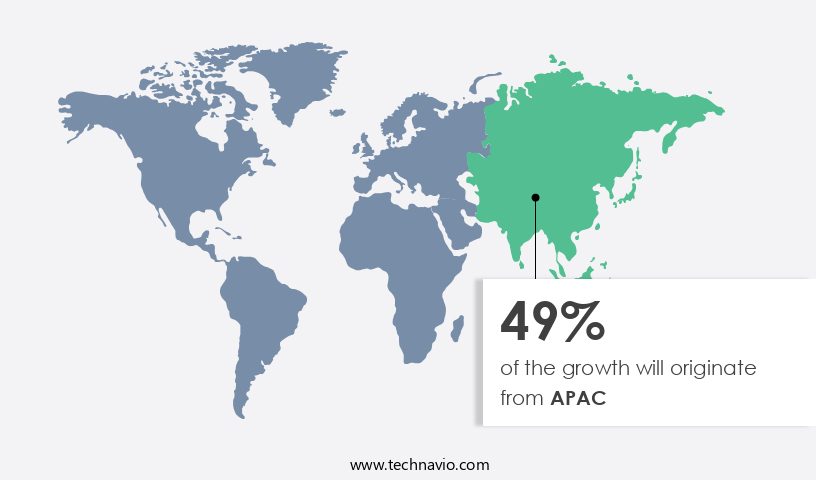

- APAC is estimated to contribute 49% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The market in APAC is experiencing significant growth due to the increasing disposable income of consumers. This financial growth is driving the demand for various media and entertainment devices, particularly home theater systems. Advanced audio devices, such as soundbars and wireless subwoofers, are becoming increasingly popular. China, Japan, and India are expected to be the major contributors to the market in the region. The adoption of online sales channels for purchasing consumer electronic goods is also increasing. Smart homes, equipped with Wi-Fi and Bluetooth connectivity, are becoming more prevalent, leading to the integration of cloud services, video streaming platforms, and OTT content.

For more insights on the market size of various regions, Request Free Sample

Major players in the market include LG Electronics, Harman International Industries, Seiko Epson Corporation, and others. Product types include Home Theater in a Box (HTIB) systems, soundbars, Blu-ray high-definition players, and more. The market is expected to grow due to the rising popularity of 3D sound systems and the increasing affordability of high-quality audio equipment. Installation costs and the availability of stand-alone speakers and smart TVs are also factors influencing market growth.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Home Theater Industry?

- Rise in disposable income is the key driver of the market. The market is experiencing growth due to the increasing disposable income of consumers. According to the Bureau of Economic Analysis, personal income rose by 0.2% in August 2024, with disposable personal income and personal outlays also increasing by the same percentage. This income growth has expanded the purchasing power of consumers, making high-end audio devices more accessible. Home entertainment-related devices, such as soundbars, Bluetooth speakers, and Wi-Fi connectivity, are popular choices for consumers seeking enhanced home theater experiences. Smart homes and cloud services have also influenced the market, with video streaming platforms like Netflix and Disney Plus offering high-definition audio content.

- Products like HTIB systems, component systems, and wireless subwoofers continue to dominate the market. Urbanization and the availability of electronic parts have facilitated the production of these devices. The sound bar segment has seen significant growth due to its affordability and ease of installation. The market dynamics are further influenced by the availability of 3D sound systems, smart TVs, and flat-screen TVs. Consumers are increasingly opting for audio equipment, such as speakers and sub-woofers, to complement their TVs. However, the market also faces challenges from counterfeit products and the rising installation costs of complex home theater systems. Internet connectivity and smart devices have transformed the market, with companies like LG Electronics, Harman International Industries, and Seiko Epson Corporation leading the way.

What are the market trends shaping the Home Theater Industry?

- Demand for customized home theater systems is an upcoming market trend. The market is experiencing growth due to the increasing popularity of home entertainment-related devices and the integration of technology in homes. Smart homes, cloud services, and video streaming platforms are driving the demand for high-quality audio content and video display. Home theater packages, including soundbars, Blu-ray high-definition players, and projector screens, are gaining traction, especially with the advancement of lamp-less technology. The sound bar segment is expected to dominate the market due to its convenience and affordability. Internet connectivity, such as Wi-Fi and Bluetooth, enables seamless integration with other smart devices and OTT platforms like Netflix and Disney Plus.

- Surround sound systems, speakers, sub-woofers, and sound bars are essential components of a home theater system. However, the high cost of home theaters and the lack of return on investment for builders limit their adoption in the middle-income segment. Specialty stores and online retailers offer various home entertainment systems, including A/V receivers, media players, and storage devices. Customized home theaters, although a niche market, are gaining popularity due to their unique offerings. Companies like LG Electronics, Harman International Industries, Seiko Epson Corporation, and others provide various home theater solutions.

- Counterfeit products pose a challenge to the market, and consumers are advised to purchase from reputable sources to ensure product quality and safety. Audio equipment, including speakers, sub-woofers, and sound bars, are essential components of a home theater system. Smart TVs and flat-screen TVs are popular video sources, and Echo and Chromecast enable wireless connectivity for easy use. Installation costs and stand-alone speakers are other factors that impact the market's growth.

What challenges does the Home Theater Industry face during its growth?

- High cost of home theater systems is a key challenge affecting the industry growth. The market encompasses a range of home entertainment-related devices, including soundbars, component systems, and Blu-ray high-definition players. Smart homes and cloud services have significantly influenced market growth, enabling consumers to access video streaming platforms like Netflix and Disney Plus via Wi-Fi or Bluetooth connectivity. Audio content is a key focus, with surround sound systems utilizing speakers and sub-woofers to deliver a good experience. The market comprises various product types, such as Home theatre packages, HTIBs, and sound bars. LG Electronics, Harman International Industries, Seiko Epson Corporation, and other leading players offer innovative solutions. The sound bar segment is gaining popularity due to its compact design and affordability.

- However, the high cost of systems and the availability of inexpensive stand-alone speaker systems pose challenges to market growth. Setting up an equipment requires a substantial investment, with estimates suggesting a budget of nearly USD 17,000-18,000 for a complete system. Consumers consider various factors, such as installation cost and the quality of equipment, when making their purchases. Internet connectivity and smart devices, like Echo and Chromecast, have transformed the experience. The integration of OTT platforms and 3D sound systems adds to the appeal. However, the risk of purchasing counterfeit products online is a concern for consumers.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, home theater market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atlantic Technology Inc. - The company offers home theater systems along with several other products such as soundbars and speakers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AudioQuest

- Bluesound International

- Bose Corp.

- Bowers and Wilkins

- Koninklijke Philips NV

- LG Corp.

- Logitech International SA

- Monitor Audio Ltd.

- NAD Electronics

- Panasonic Holdings Corp.

- Pioneer Corp.

- Samsung Electronics Co. Ltd.

- Sennheiser Electronic GmbH and Co. KG

- Sharp Corp.

- Sonos Inc.

- Sony Group Corp.

- The Rotel Co., Ltd.

- Toshiba Corp.

- Yamaha Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market continues to evolve, with technological advancements and consumer preferences shaping its dynamics. Home entertainment-related devices, including smart homes, cloud services, video streaming platforms, and audio content, are at the forefront of this evolution. Home Theater in a Box (HTIB) systems, soundbars, and projector screens are popular choices for consumers seeking experiences. Lamp-less technology and high-definition displays have revolutionized television sets, offering superior image quality. The adoption of smart homes and IoT devices has expanded the market for home entertainment systems.

Further, consumers can now control using voice commands or smart devices, enhancing convenience and ease of use. Urbanization and the increasing popularity have led to the growth of the market. Manufacturers are focusing on developing innovative products to cater to the evolving needs of consumers. For instance, Harman International Industries and Seiko Epson Corporation are investing in lamp-less technology for projectors, while LG Electronics and JBL are introducing wireless subwoofers. Transcosmos, Echo, and Chromecast are among the companies offering smart home integration and voice control features. The market for home entertainment systems is segmented based on product type, including HTIB systems, sound bars, component systems, and stand-alone speakers.

In addition, the sound bar segment is expected to dominate the market due to its compact design and affordability. The component system segment is expected to witness steady growth due to its superior sound quality. The market is also segmented based on distribution channels, including specialty stores and online retail. Online retail is expected to witness significant growth due to its convenience and wide product selection. OTT platforms, such as Netflix and Disney Plus, are also emerging as key players In the market, offering streaming services for movies and TV shows. The adoption of surround sound and 3D sound systems is expected to drive the growth of the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.7% |

|

Market growth 2025-2029 |

USD 11.41 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.1 |

|

Key countries |

US, China, Japan, India, Canada, South Korea, UK, Germany, Italy, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Home Theater Market Research and Growth Report?

- CAGR of the Home Theater industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the home theater market growth of industry companies

We can help! Our analysts can customize this home theater market research report to meet your requirements.

RIA -

RIA -