Homeland Security Market Size 2026-2030

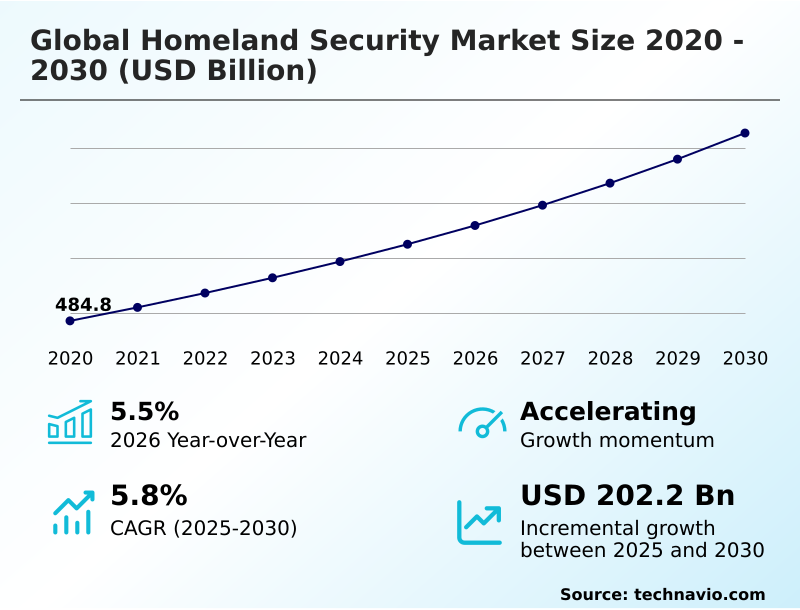

The homeland security market size is valued to increase by USD 202.2 billion, at a CAGR of 5.8% from 2025 to 2030. Escalation of cyber warfare and necessity for digital sovereignty will drive the homeland security market.

Major Market Trends & Insights

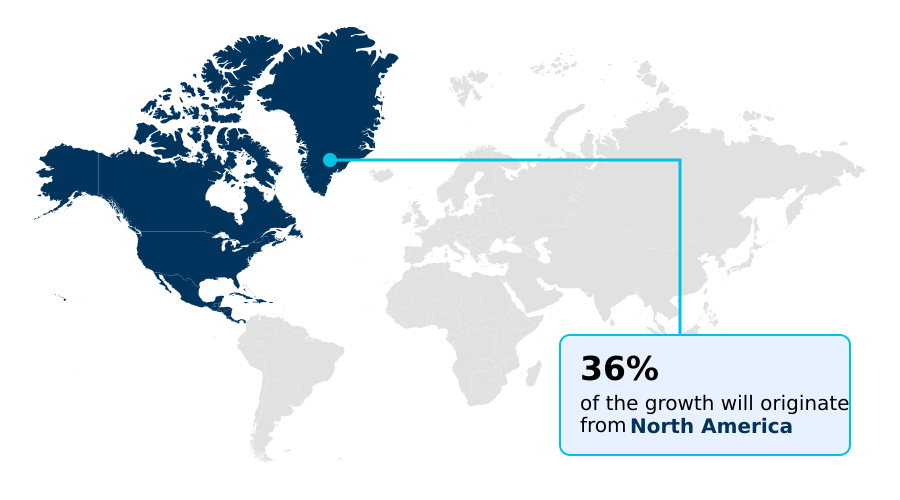

- North America dominated the market and accounted for a 35.7% growth during the forecast period.

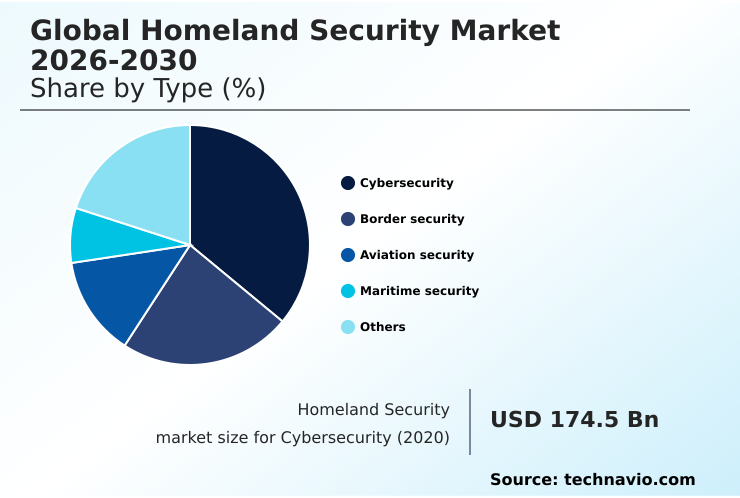

- By Type - Cybersecurity segment was valued at USD 214.6 billion in 2024

- By Component - Hardware segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 341.5 billion

- Market Future Opportunities: USD 202.2 billion

- CAGR from 2025 to 2030 : 5.8%

Market Summary

- The homeland security market is undergoing a significant transformation, moving beyond conventional physical defense toward integrated, intelligence-driven frameworks. This evolution is driven by the need to counter a broadening spectrum of threats, from sophisticated cyber warfare targeting critical infrastructure to asymmetric threats leveraging commercial-off-shelf technologies.

- A key trend is the integration of AI and edge analytics for predictive threat assessment, enabling proactive rather than reactive security postures. For instance, a public-private partnership managing a national power grid utilizes a unified operational view combining data from surveillance systems and grid-stability sensors.

- This allows for predictive modeling to identify vulnerabilities before they are exploited, reducing potential downtime by up to 40%. The market also emphasizes the modernization of border security with biometric identification and autonomous surveillance, balancing national safety with the facilitation of legitimate global commerce.

- However, challenges related to the ethical use of facial recognition and the interoperability of legacy systems with new zero-trust architectures persist, shaping procurement strategies and demanding innovative, adaptable solutions from technology providers.

What will be the Size of the Homeland Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Homeland Security Market Segmented?

The homeland security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

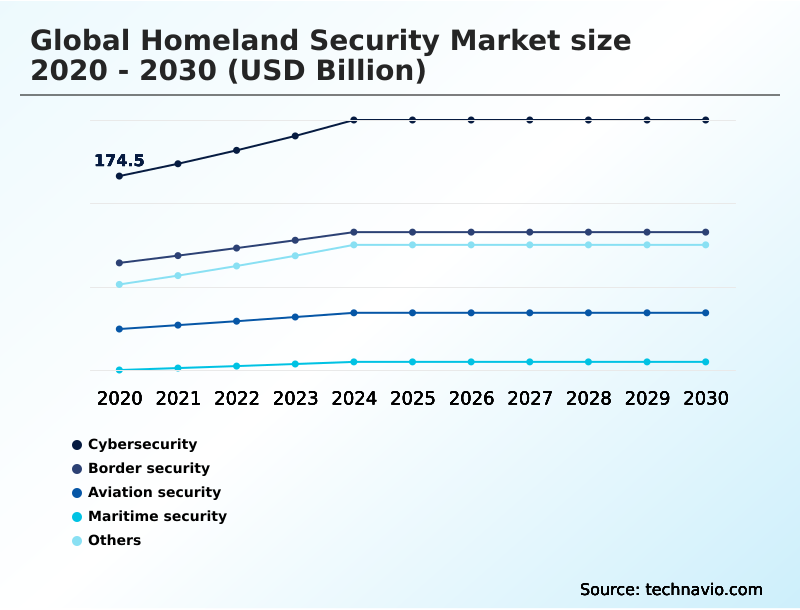

- Type

- Cybersecurity

- Border security

- Aviation security

- Maritime security

- Others

- Component

- Hardware

- Software

- Services

- End-user

- Public sector

- Private sector

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Type Insights

The cybersecurity segment is estimated to witness significant growth during the forecast period.

The cybersecurity segment is pivotal, focusing on protecting national digital infrastructure against sophisticated electronic warfare. This involves a strategic shift toward zero-trust architecture, where continuous verification is mandatory, rendering the traditional network perimeter obsolete.

Core to this is safeguarding the digital supply chain to prevent infiltration via third-party software vulnerabilities.

The deployment of advanced cybersecurity defensive software within sovereign cloud environments is critical for defending against advanced persistent threats and maintaining the integrity of sovereign information.

Integrating AI-powered forensic analysis into command and control platforms enhances the real-time identification of anomalous network behavior, improving breach detection rates by over 30%.

This data-centric approach ensures a resilient digital environment capable of defending a nation's expanding digital attack surface.

The Cybersecurity segment was valued at USD 214.6 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Homeland Security Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is diverse, with regional priorities shaping technology adoption. In North America, the focus is on critical infrastructure protection and securing the digital supply chain.

APAC is a high-growth region, driven by investments in maritime security and smart city initiatives that leverage extensive surveillance systems and data-centric governance. In this region, enhanced maritime domain awareness has improved incident response times by over 25%.

Europe navigates a complex regulatory environment, balancing border security needs with stringent privacy laws, which fosters innovation in privacy-preserving technologies like federated learning. Coordinated disinformation campaigns are a global concern, prompting cross-regional collaboration among financial intelligence units.

Key technologies like facial recognition and iris scanning are being deployed globally, but their application is tailored to regional legal frameworks, creating a fragmented but opportunity-rich market.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- An analysis of the global homeland security market reveals distinct growth patterns influenced by several factors. The market's structure, defined by the global homeland security market by type and the global homeland security market by component, shows a clear shift toward software and service-based solutions.

- Key global homeland security market growth drivers include persistent geopolitical instability and the need to protect critical national assets, while significant global homeland security market challenges stem from ethical debates over public surveillance and the high cost of overhauling legacy systems. Recent global homeland security market developments indicate a focus on AI integration, as highlighted by major players.

- The global homeland security market's key trends, such as the move toward zero-trust architecture for government agencies and the use of autonomous systems for border management, are reshaping operational strategies. Regionally, the global homeland security market in North America leads in spending, while the global homeland security market in APAC exhibits the fastest growth.

- The global homeland security market in Europe contends with strict data privacy regulations affecting biometric implementation in homeland security. Specific segments like the aviation security screening systems market and the maritime security surveillance technologies market are seeing rapid innovation.

- The expanding role of cloud computing in homeland security is undeniable, yet interoperability issues in security systems remain a primary concern for procurement officers, with organizations reporting that integration challenges can increase project timelines by more than 30% compared to greenfield deployments.

What are the key market drivers leading to the rise in the adoption of Homeland Security Industry?

- The escalation of cyber warfare and the corresponding necessity for digital sovereignty are key drivers propelling the market's growth.

- Market growth is significantly propelled by the dual pressures of escalating cyber warfare and the critical need for digital sovereignty.

- Nations are building a resilient digital environment to protect sovereign information from advanced persistent threats that exploit an ever-expanding digital attack surface. This has led to the widespread adoption of zero-trust architectures, ensuring resilient connectivity and robust digital perimeter protection.

- Modernization of border management is another key driver, with the deployment of advanced biometric processing systems accelerating traveler verification by up to 60%. These systems, along with unmanned aerial vehicles, form a layered defense strategy.

- Concurrently, protecting critical national infrastructure with technologies like grid-stability sensors enhances the national resilience framework, enabling effective threat prioritization against both physical and digital disruptive forces.

What are the market trends shaping the Homeland Security Industry?

- The proliferation of artificial intelligence for predictive threat assessment is emerging as a significant market trend. This development enables proactive security measures by identifying potential hazards before they manifest.

- Key market trends are centered on the integration of intelligent and automated technologies to create a proactive security posture. The adoption of zero-trust models is becoming standard, moving beyond traditional perimeter defenses to a framework of continuous verification that limits lateral movement, reducing breach impact by over 60%.

- This is complemented by the proliferation of autonomous surveillance, where swarm drones and other unmanned systems provide persistent monitoring. Such systems, particularly for autonomous border surveillance, expand coverage by fivefold compared to manual patrols.

- Central to these trends is the use of high-performance computing and edge analytics for predictive threat assessment and modeling, which allows for the identification of behavioral deviations before they escalate. These technologies are creating a digital fence that provides a unified operational view, enhancing overall situational awareness and enabling more effective security responses.

What challenges does the Homeland Security Industry face during its growth?

- Ethical considerations and legal barriers associated with biometric implementation present a key challenge affecting the industry's growth trajectory.

- The market faces significant challenges from the rapid evolution of asymmetric threats and the technologies that enable them. Adversaries are leveraging commercial-off-shelf technologies, leading to a constant need for innovation in asymmetric threats neutralization. The rise of high-fidelity synthetic media and deepfake detection has become a critical concern, requiring the development of advanced synthetic media detection algorithms.

- This cat-and-mouse game demands continuous investment in countermeasures like signal jamming equipment. Furthermore, the use of encrypted communication by non-state actors complicates monitoring efforts by financial intelligence units.

- Addressing these challenges necessitates a move toward privacy-preserving technologies that can be deployed without violating ethical and legal norms, ensuring that security measures do not compromise civil liberties while effectively countering threats from illegal logging to coordinated disinformation campaigns.

Exclusive Technavio Analysis on Customer Landscape

The homeland security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the homeland security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Homeland Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, homeland security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Key offerings include integrated intelligence systems, secure communications, and specialized aircraft for comprehensive border and maritime surveillance operations, enhancing national security frameworks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Axon Enterprise Inc.

- BAE Systems Plc

- Booz Allen Hamilton Corp.

- CACI International Inc.

- Elbit Systems Ltd.

- General Dynamics Corp.

- Honeywell International Inc.

- IDEMIA France SAS

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Motorola Solutions Inc.

- NEC Corp.

- Northrop Grumman Corp.

- Palantir Technologies Inc.

- RTX Corp.

- Smiths Detection Group Ltd.

- Thales Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Homeland security market

- In August 2025, Cisco Systems launched a comprehensive zero-trust security architecture tailored for national critical infrastructure, integrating physical sensor data with network traffic analysis to prevent lateral movement by malicious actors.

- In September 2025, the Australian Home Affairs Department implemented a new automated biometric processing system for international maritime arrivals to streamline the identification process and enhance coastal security.

- In October 2025, the European Data Protection Board issued a restrictive guideline that further limited the use of real-time biometric identification in public spaces by law enforcement agencies.

- In November 2025, General Electric Vernova introduced a new series of advanced grid-stability sensors designed to protect power distribution networks from physical sabotage and electromagnetic interference.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Homeland Security Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.8% |

| Market growth 2026-2030 | USD 202.2 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.5% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The homeland security market is evolving from siloed defense mechanisms toward integrated, intelligence-driven ecosystems. This strategic shift is driven by the dual needs of countering sophisticated asymmetric threats and achieving digital sovereignty.

- Central to this transformation is the adoption of zero-trust models, a boardroom-level decision that forces a complete re-evaluation of cybersecurity budgets, moving investment from perimeter security to continuous verification. The deployment of autonomous surveillance, powered by edge analytics, is reshaping border security and critical infrastructure protection.

- For instance, leveraging edge computing in surveillance systems has demonstrated an ability to reduce data transmission costs by over 60% while accelerating real-time threat detection. Technologies such as biometric identification, command and control platforms, and predictive modeling are no longer standalone tools but are integral components of a cohesive defense posture.

- This integration is essential for managing an expanding digital attack surface and ensuring a resilient digital environment against persistent cyber warfare.

What are the Key Data Covered in this Homeland Security Market Research and Growth Report?

-

What is the expected growth of the Homeland Security Market between 2026 and 2030?

-

USD 202.2 billion, at a CAGR of 5.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Cybersecurity, Border security, Aviation security, Maritime security, and Others), Component (Hardware, Software, and Services), End-user (Public sector, and Private sector) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalation of cyber warfare and necessity for digital sovereignty, Ethical and legal barriers to biometric implementation

-

-

Who are the major players in the Homeland Security Market?

-

Airbus SE, Axon Enterprise Inc., BAE Systems Plc, Booz Allen Hamilton Corp., CACI International Inc., Elbit Systems Ltd., General Dynamics Corp., Honeywell International Inc., IDEMIA France SAS, L3Harris Technologies Inc., Leidos Holdings Inc., Leonardo S.p.A., Lockheed Martin Corp., Motorola Solutions Inc., NEC Corp., Northrop Grumman Corp., Palantir Technologies Inc., RTX Corp., Smiths Detection Group Ltd. and Thales Group

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for digital perimeter protection and enhanced situational awareness. The adoption of autonomous border surveillance has improved threat detection efficiency in remote terrains by over 40%, optimizing personnel deployment.

- Concurrently, the implementation of zero-trust architectures is a critical response to advanced persistent threats, with early adopters reporting up to a 70% reduction in lateral movement by malicious actors post-breach. A focus on resilient connectivity and threat prioritization is driving investment in platforms that offer a unified operational view.

- Furthermore, sovereign cloud integration is becoming standard for government agencies, ensuring data integrity while mitigating risks associated with foreign software dependencies. These shifts underscore a move toward proactive, data-centric security models.

We can help! Our analysts can customize this homeland security market research report to meet your requirements.

RIA -

RIA -