Hydraulic Fluid Connectors Market Size 2026-2030

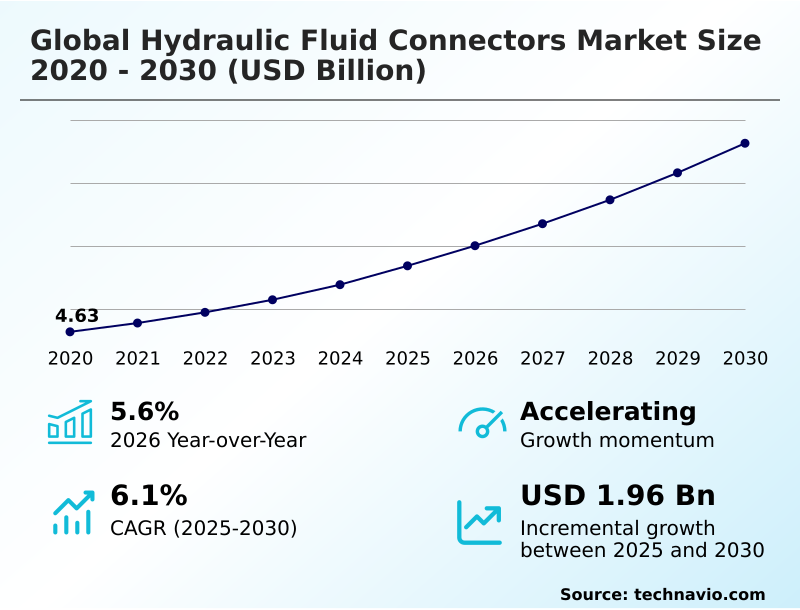

The hydraulic fluid connectors market size is valued to increase by USD 1.96 billion, at a CAGR of 6.1% from 2025 to 2030. Escalating infrastructure development and construction activities will drive the hydraulic fluid connectors market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 36.6% growth during the forecast period.

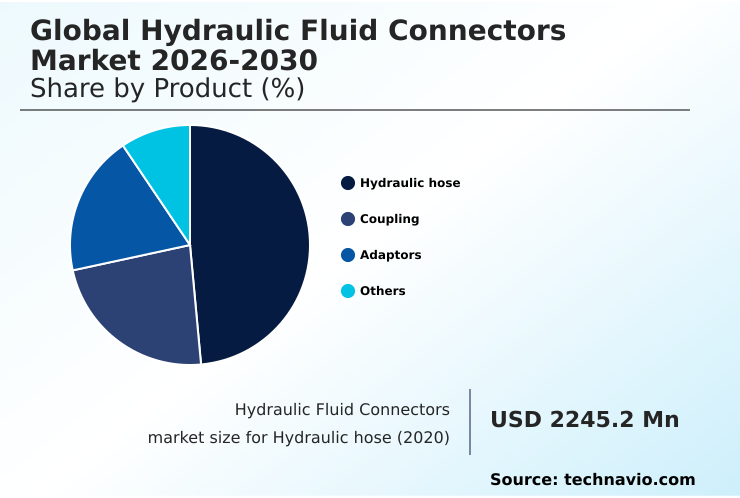

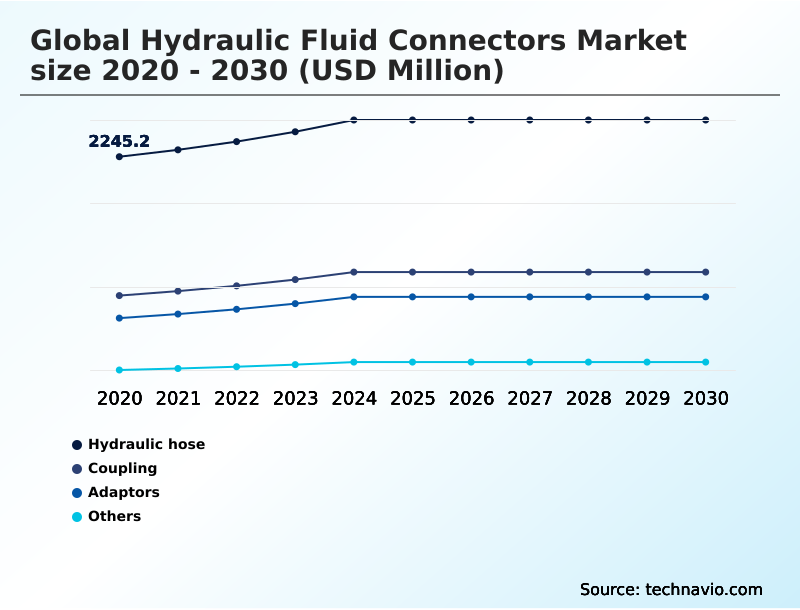

- By Product - Hydraulic hose segment was valued at USD 2.56 billion in 2024

- By Material - Steel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.01 billion

- Market Future Opportunities: USD 1.96 billion

- CAGR from 2025 to 2030 : 6.1%

Market Summary

- The hydraulic fluid connectors market is integral to the functionality of modern industrial and mobile machinery, where ensuring secure fluid power transmission is paramount. Growth is driven by the expansion of industrial automation and major infrastructure projects, which demand robust components like high-pressure tube fittings and steel tube fittings capable of withstanding rigorous operational cycles.

- A significant trend is the integration of smart technologies, with components featuring iot-enabled hydraulic monitoring systems becoming more prevalent. These advancements support predictive maintenance strategies, enabling operators to anticipate failures and optimize schedules. For instance, a heavy equipment OEM can leverage data from smart fittings to proactively replace parts, significantly reducing costly field failures and enhancing overall equipment reliability.

- However, the market also navigates challenges from raw material price volatility and intense competition, which push manufacturers toward innovations in corrosion-resistant coatings and more efficient hydraulic circuit designs. The focus remains on enhancing performance through advancements in leak-free sealing technology and materials like advanced rubber compounds.

What will be the Size of the Hydraulic Fluid Connectors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Hydraulic Fluid Connectors Market Segmented?

The hydraulic fluid connectors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Hydraulic hose

- Coupling

- Adaptors

- Others

- Material

- Steel

- Stainless steel

- Aluminum

- Brass

- Others

- Application

- Manufacturing

- Oil and gas

- Automotive

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Rest of World (ROW)

- North America

By Product Insights

The hydraulic hose segment is estimated to witness significant growth during the forecast period.

The hydraulic hose segment is foundational to fluid power transmission, with demand shaped by evolving industrial requirements.

A key trend is the adoption of advanced materials like thermoplastic hydraulic hose and sophisticated synthetic rubber compounds, often featuring high-tensile steel wire braiding for reinforcement.

These innovations deliver superior temperature and chemical resistance, which is critical in heavy-duty industrial applications.

The integration of predictive maintenance sensors into these components aligns with Industry 4.0 objectives, enabling operators to monitor hydraulic system integrity and reduce unplanned downtime by over 25%.

This shift toward intelligent, durable fluid conveyance systems, including high-pressure hose assembly, is essential for optimizing the operational efficiency metrics of modern industrial automation machinery and mobile hydraulic applications.

The Hydraulic hose segment was valued at USD 2.56 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 36.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hydraulic Fluid Connectors Market Demand is Rising in APAC Get Free Sample

The global market landscape is characterized by diverse regional dynamics. APAC is poised to be the primary growth engine, projected to contribute over 36% of the market’s incremental growth, fueled by massive infrastructure development and industrial expansion.

This contrasts with mature markets in North America and Europe, where growth is driven by technological upgrades and modernization.

For example, stringent European regulations drive adoption of systems using flat-face couplings that improve fluid leakage prevention by over 15%, enhancing environmental compliance.

Meanwhile, developing economies in South America and the Middle East and Africa show steady demand linked to the mining equipment systems and offshore drilling equipment sectors.

The need for reliable fluid power components in these regions supports the market for corrosion-resistant hydraulic adapters and hydraulic workover rigs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the hydraulic fluid connectors market hinge on a detailed analysis of application-specific requirements and total lifecycle costs. For OEMs, selecting between high-pressure vs low-pressure hydraulic fittings is a fundamental design choice, while the debate over flat face vs threaded quick couplers often centers on balancing connection speed with system integrity.

- In harsh environments, the benefits of corrosion-resistant hydraulic adapters and stainless steel quick connect couplings become paramount for ensuring longevity and safety. The commitment to a leak-free hydraulic hose assembly process is no longer optional, as it directly impacts both operational expenses and environmental compliance.

- For instance, OEMs using pre-tested hydraulic tube assembly for manufacturing report assembly line error rates that are half those of companies sourcing individual parts, significantly improving production throughput. The demand for compact hydraulic fittings for mobile equipment continues to grow, pushing innovation in materials and design.

- This focus on specialization is also evident in the need for custom hydraulic solutions for oems and high-impulse hydraulic hose applications. Ultimately, optimizing a hydraulic system's energy efficiency and understanding the hydraulic component lifecycle cost analysis are critical for maintaining a competitive edge.

- Educating end-users through resources like a hydraulic fitting thread identification guide is crucial for ensuring proper maintenance and performance across sectors, from systems for renewable energy to vibration-resistant fittings for heavy machinery.

What are the key market drivers leading to the rise in the adoption of Hydraulic Fluid Connectors Industry?

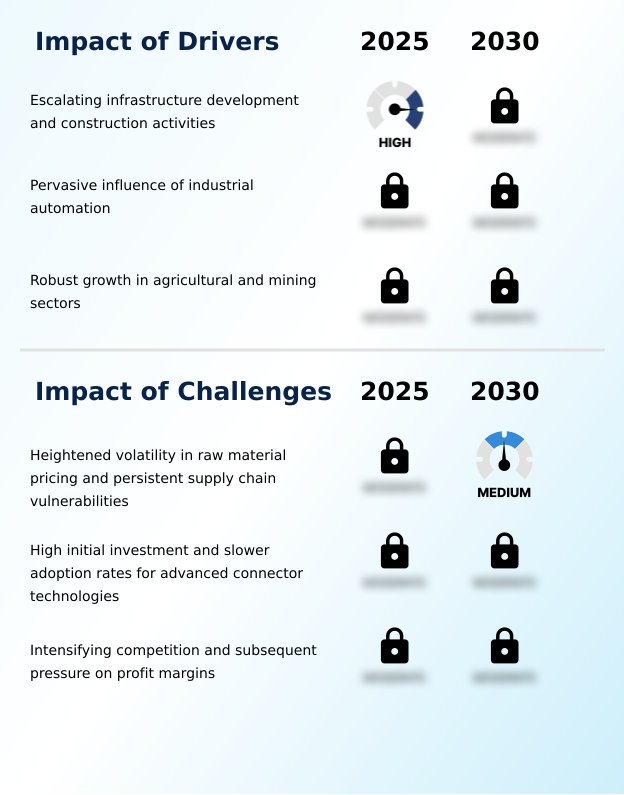

- Escalating infrastructure development and a corresponding rise in construction activities are key drivers propelling market growth.

- Market growth is fundamentally driven by expansion across key industrial sectors. Sustained investment in heavy construction equipment for global infrastructure projects creates continuous demand for robust fluid power components.

- The pervasive influence of industrial automation has led to a 20% increase in the need for high-performance hydraulic actuator control systems in production line automation and automotive manufacturing robotics.

- In parallel, the modernization of agriculture and mining stimulates demand for specialized machinery. Advanced agricultural machinery hydraulics, integral to precision agriculture technology, can improve crop yields by over 10%.

- This mechanization trend, coupled with growth in the mining equipment systems sector, ensures a strong and growing need for reliable hydraulic connectors capable of functioning in demanding high-pressure applications and contributing to greater high-performance fluid power.

What are the market trends shaping the Hydraulic Fluid Connectors Industry?

- The market is increasingly influenced by the proliferation of smart technologies. This includes deeper integration with Industry 4.0 principles, driving demand for intelligent components.

- Key market trends are reshaping the performance and application of hydraulic fluid connectors. The integration of smart technologies is paramount, with predictive maintenance sensors enabling a reduction in unplanned machinery downtime by up to 30%.

- This shift toward Industry 4.0 is complemented by a strong focus on sustainability, driving demand for biodegradable hydraulic fluids and components with advanced, leak-free sealing technology. Innovations in push-to-connect fittings and high-pressure quick disconnects are enhancing operational efficiency metrics in material handling equipment.

- Concurrently, the use of advanced materials, such as lightweight alloy components and corrosion-resistant coatings, is critical for meeting the demands of aerospace fluid systems and subsea hydraulic systems, where both weight and durability are essential for performance and achieving a lower total cost of ownership.

What challenges does the Hydraulic Fluid Connectors Industry face during its growth?

- Heightened volatility in raw material pricing, coupled with persistent supply chain vulnerabilities, presents a key challenge to industry growth.

- The market faces several persistent challenges that impact profitability and operational planning. Heightened raw material price volatility, particularly for steel and specialized polymers, has caused 15-20% fluctuations in manufacturing costs, directly pressuring margins for aftermarket replacement parts. In tandem, supply chain vulnerabilities continue to pose a risk to production schedules.

- The high initial investment required for advanced technologies, such as smart factory integration, presents a barrier for smaller enterprises, potentially extending the capital recovery period by up to two years.

- Furthermore, intense competition among suppliers forces a focus on oem integration support and cost control, as pricing pressures limit the ability to pass on increased costs to end-users, especially in price-sensitive sectors.

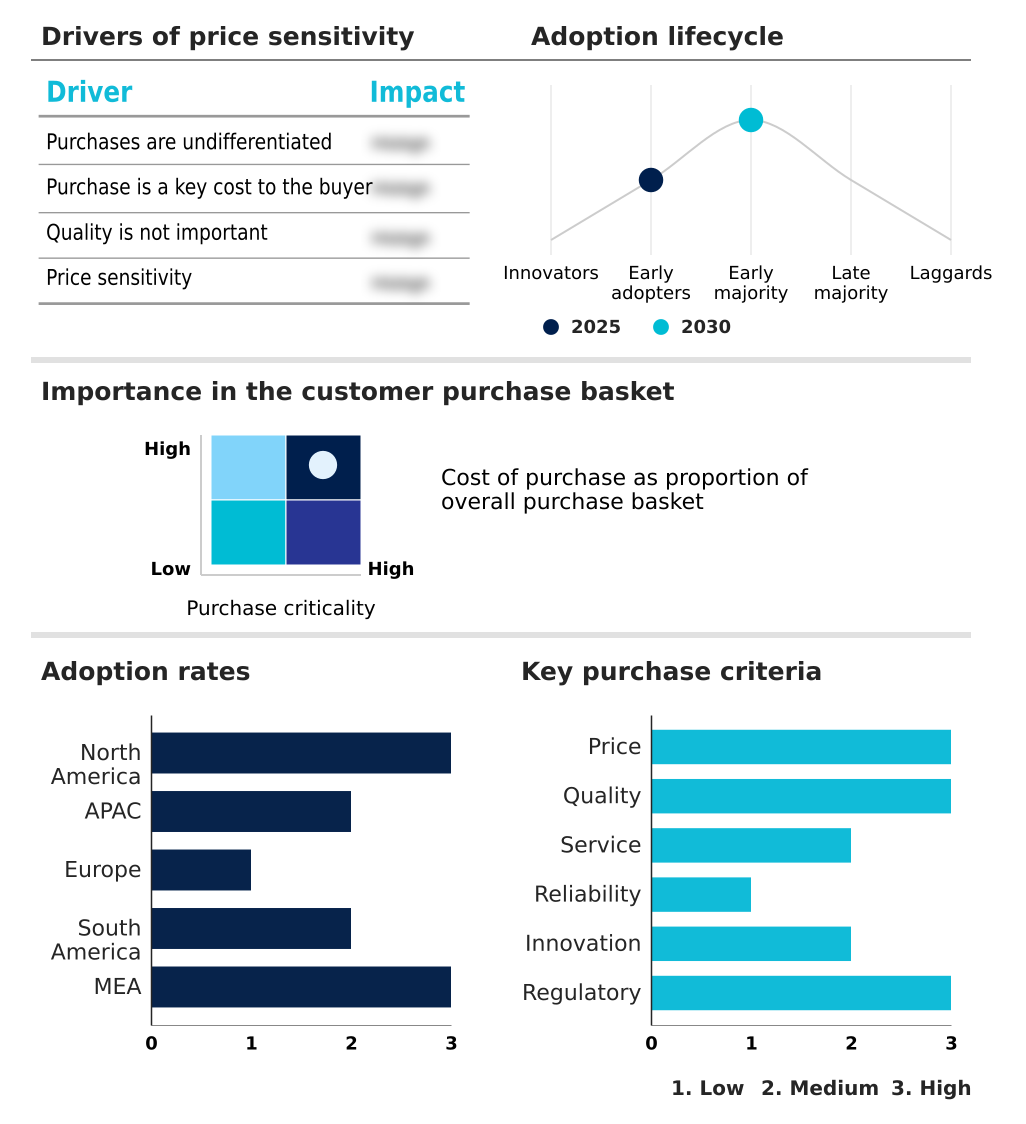

Exclusive Technavio Analysis on Customer Landscape

The hydraulic fluid connectors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hydraulic fluid connectors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hydraulic Fluid Connectors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hydraulic fluid connectors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aerocom Specialty Fittings Inc. - Specialized stainless steel fluid connectors, including custom assemblies, address high-pressure and corrosive environments in critical industrial and aerospace applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aerocom Specialty Fittings Inc.

- Alfa Gomma S.p.A.

- Bosch Rexroth AG

- Eaton Corp. Plc

- Gates Corp.

- Kurt Manufacturing Co.

- Manuli Hydraulics Group

- Parker Hannifin Corp.

- RG Industries Inc.

- RW Connection

- Ryco Hydraulics Pty. Ltd.

- Smiths Group Plc

- Staubli International

- Stauffenberg GmbH and Co. KG

- Swagelok Co.

- VOSS Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hydraulic fluid connectors market

- In August 2025, Parker Hannifin Corp. announced modifications to its compression union and female elbow fittings, a move designed to improve installation efficiency in compact industrial spaces.

- In August 2025, Swagelok Co. introduced new components specifically designed for hydrogen refueling stations, addressing the growing needs of the clean energy sector with high-pressure fluid handling solutions.

- In October 2024, the Manuli Ryco group announced the acquisition of Cardiff Hydraulics Ltd., a strategic move to strengthen its service and distribution capabilities in the United Kingdom.

- In April 2025, an engine supply agreement was established between Kobelco Construction Machinery USA and both Yanmar and Isuzu to facilitate the construction of excavators within North America, signaling sustained demand for heavy machinery and their hydraulic systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hydraulic Fluid Connectors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 1957.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Turkey, South Africa and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The hydraulic fluid connectors market ensures the integrity of fluid power transmission in critical industrial and mobile applications. Its performance is defined by components like din 2353 tube fittings, quick release coupling devices, and high-pressure hose assembly, which must meet stringent standards for reliability.

- The adoption of advanced sealing technology has been shown to extend component service life by up to 40% in high-cycle industrial automation settings. The market's evolution is driven by material science, including the use of thermoplastic hydraulic hose and advanced rubber compounds, along with tools like the hydraulic hose crimper.

- A key trend impacting boardroom-level strategy is the integration of iot-enabled hydraulic monitoring. The decision to invest in these smart systems, which enable predictive maintenance, represents a strategic trade-off between higher initial capital expenditure and long-term ROI from reduced downtime and enhanced hydraulic system integrity.

- This shift towards intelligent, data-driven fluid conveyance systems is reshaping component design and selection criteria across all sectors.

What are the Key Data Covered in this Hydraulic Fluid Connectors Market Research and Growth Report?

-

What is the expected growth of the Hydraulic Fluid Connectors Market between 2026 and 2030?

-

USD 1.96 billion, at a CAGR of 6.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Hydraulic hose, Coupling, Adaptors, and Others), Material (Steel, Stainless steel, Aluminum, Brass, and Others), Application (Manufacturing, Oil and gas, Automotive, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating infrastructure development and construction activities, Heightened volatility in raw material pricing and persistent supply chain vulnerabilities

-

-

Who are the major players in the Hydraulic Fluid Connectors Market?

-

Aerocom Specialty Fittings Inc., Alfa Gomma S.p.A., Bosch Rexroth AG, Eaton Corp. Plc, Gates Corp., Kurt Manufacturing Co., Manuli Hydraulics Group, Parker Hannifin Corp., RG Industries Inc., RW Connection, Ryco Hydraulics Pty. Ltd., Smiths Group Plc, Staubli International, Stauffenberg GmbH and Co. KG, Swagelok Co. and VOSS Group

-

Market Research Insights

- The market's dynamics are shaped by relentless demands for higher operational efficiency and system reliability. The implementation of advanced connectors with non-spill characteristics can reduce fluid loss by over 90%, directly impacting environmental compliance standards and lowering operational costs.

- In parallel, systems utilizing smart fittings with predictive maintenance analytics report a 25% reduction in unplanned downtime compared to those with reactive service schedules, a critical factor for industries focused on maximizing uptime. Furthermore, the adoption of lightweight alloy components in certain mobile hydraulic applications contributes to a 5-7% improvement in fuel efficiency, aligning with sustainability goals.

- These measurable outcomes underscore the strategic importance of component selection in achieving a lower total cost of ownership and improving performance in high-pressure applications.

We can help! Our analysts can customize this hydraulic fluid connectors market research report to meet your requirements.

RIA -

RIA -