Hydraulic Valves Market Size 2024-2028

The hydraulic valves market size is forecast to increase by USD 3.27 billion at a CAGR of 5.15% between 2023 and 2028.

- The market is witnessing significant growth due to the continued emphasis on energy-efficient hydraulic valves. Manufacturers are focusing on developing high-performance hydraulic valves to cater to the increasing demand for power and productivity in various industries. However, the skilled workforce shortage is posing a significant challenge to the market growth. The lack of skilled labor can lead to delays in production and increased costs for end-users. Advanced hydraulic valves, such as electro-hydraulic valves, proportional hydraulic valves, and directional control valves, play a pivotal role in ensuring the functional performance of machinery in severe conditions. In addition, the renewable energy sector and automobile industry also utilize hydraulic systems for fluid control and energy-efficient solutions. Moreover, the trend towards automation and digitalization in manufacturing processes is expected to create new opportunities for the market. The development of advanced technologies, such as smart hydraulic valves and IoT-enabled systems, can help address the workforce shortage and improve overall efficiency in hydraulic systems. In summary, the market is driven by the demand for energy-efficient and high-performance valves, while the skilled workforce shortage and the trend toward automation present significant challenges and opportunities for market growth.

What will be the Size of the Market During the Forecast Period?

- The market encompasses the production and distribution of hydraulic valves used in various industries to control and regulate the flow and pressure of fluids, primarily oil, in hydraulic systems. These systems are integral to powering machinery in sectors such as construction and agriculture, including dump trucks, graders, loaders, excavators, cranes, forklifts, and air seeders. Hydraulic valves facilitate functional performance In these applications by managing fluid flow and pressure in severe conditions. The market's growth is driven by the increasing demand for efficient, reliable, and high-performing hydraulic systems in industries that rely on pressurized fluids for machinery operation. The aging infrastructure In the construction and agriculture sectors, as well as the expanding usage of mobile hydraulic machines, further bolsters market expansion.

- Electro-hydraulic valves are a significant segment within the market, offering advanced functionality and energy efficiency. Overall, the market is poised for steady growth, driven by the continuous need for improved fluid flow and pressure control in various industries.

How is this Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Oil and gas industry

- Water and wastewater industry

- Power industry

- Mining

- Others

- Type

- Control valve

- Servo valve

- Proportional valve

- Others

- Geography

- APAC

- China

- Japan

- Europe

- UK

- France

- North America

- US

- Middle East and Africa

- South America

- APAC

By End-user Insights

- The oil and gas industry segment is estimated to witness significant growth during the forecast period.

The market is driven by the increasing adoption of advanced hydraulic systems in various industries, particularly In the oil and gas sector. These systems require high-performance hydraulic valves to operate efficiently under high-pressure conditions and in harsh environments. The integration of automation and IoT In the oil and gas industry necessitates advanced hydraulic valves for remote monitoring and control, enhancing operational efficiency and safety.

Get a glance at the market report of share of various segments Request Free Sample

The oil and gas industry segment was valued at USD 3.15 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

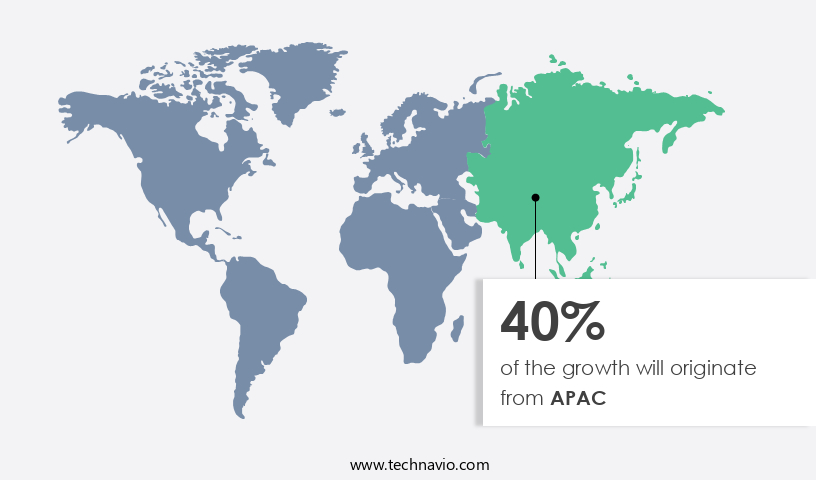

- APAC is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The Asia-Pacific region, particularly countries like China, India, and Southeast Asian nations, are undergoing rapid economic growth and urbanization, leading to increased industrial activities and extensive utilization of hydraulic systems in various industries such as automotive, electronics, machinery, and consumer goods. Furthermore, governments In the region are investing heavily in infrastructure projects, including transportation, energy, water supply, and urban development, which require the use of hydraulic systems in construction machinery and equipment. The construction industry is booming with numerous residential, commercial, and public infrastructure projects, leading to a significant demand for hydraulic systems in construction machinery and equipment. The demand for hydraulic systems is further driven by the need for energy-efficient solutions, automation, and advanced hydraulic valves, including electro-hydraulic valves and proportional hydraulic valves.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Hydraulic Valves Industry?

Continued emphasis on energy-efficient hydraulic valves is the key driver of the market.

- Hydraulic valves play a pivotal role in various industries, including manufacturing, mining, construction, automotive, and aerospace, by providing directional control, flow, and pressure regulation for hydraulic power systems. These systems rely on pressurized fluids to operate machinery, such as dump trucks, graders, loaders, excavators, and bulldozers, under severe conditions. Energy efficiency is a significant concern In these industries, with hydraulic valves accounting for a substantial portion of energy consumption. Advanced hydraulic valves, such as electro-hydraulic and proportional valves, offer energy savings through precise fluid control and minimal energy loss. In the manufacturing sector, for instance, these valves optimize production processes by ensuring accurate positioning and flow control.

- In the renewable energy sector, hydraulic valves are essential for pumping water from natural reservoirs for energy production and impurity filtration in industrial wastewater disposal. The mining industry, particularly in surface and underground mining, requires hydraulic valves for various applications, including fire protection systems, pump stations, and material handling equipment. These are also crucial In the oil and gas industry for drilling pipelines, hydraulic fracturing operations, and offshore drilling rigs. In the agriculture and forestry sector, these are used in farming machinery, such as tractors, shock absorbers, and drive systems. In the automotive sector, hydraulic valves are employed in brakes, power steering, and suspension systems.

What are the market trends shaping the Hydraulic Valves Industry?

Development of high-performance hydraulic valves is the upcoming market trend.

- High-performance hydraulic valves are essential components in hydraulic power systems, providing flow and pressure control for various industries. These valves are engineered to ensure superior functional performance in severe conditions, making them suitable for applications in construction and mining, oil and gas, agriculture and forestry, aerospace and defense, and heavy equipment. Advanced materials, such as stainless steel, alloys, and composites, are used In their manufacturing to enhance durability and resistance to wear and corrosion. Anti-corrosion and anti-wear coatings further extend their lifespan, reducing maintenance costs and ensuring reliable operation in harsh environments. High-performance valves are designed to operate at higher pressures and flow rates, catering to the demands of heavy-duty applications.

- They are capable of precise control of fluid flow and actuator movement, which is crucial for directional control valves, fluid flow, and pressure control valves in various industries. Electrical signals are used to control proportional valves, cartridge valves, check valves, relief valves, and other hydraulic components, ensuring efficient and accurate operation. In the renewable energy sector, it plays a pivotal role in pump stations, mine sites, and other downstream equipment, where precise control of fluid flow and pressure is necessary. These valves are designed to operate in critical fluid systems, such as those involving impurities in water production and industrial wastewater disposal, where contamination and environmental pollution are concerns.

What challenges does the Hydraulic Valves Industry face during its growth?

Skilled workforce shortage impacts market and end-user industries is a key challenge affecting the industry growth.

- The market is a critical component of hydraulic power systems, which utilize both water and oil as pressurized fluids for flow and pressure control in machinery and energy-efficient solutions. It plays a pivotal role in various industries, including construction and mining, oil and gas, agriculture and forestry, aerospace and defense, and heavy equipment. In the hydraulic systems of construction machinery such as dump trucks, graders, loaders, and excavators, hydraulic valves ensure functional performance under severe conditions. In the automobile sector, hydraulic systems are used in pivotal systems like shock absorbers, drive systems, brakes, and power steering. The integration of advanced technologies like electro-hydraulic valves, proportional hydraulic valves, and automation in hydraulic systems necessitates a skilled workforce for installation, maintenance, and repair.

- The shortage of skilled labor is a significant challenge for the market, affecting production, innovation, and customer support in end-user industries. The market caters to diverse applications, including water production, industrial wastewater disposal, contamination control, natural reservoirs, and fluid control in various industries. Key applications include directional control valves, actuator movement, positioning, flow control valves, and pressure control valves. These valves respond to electrical signals, enabling precise fluid flow and actuator movement. These are essential for various industries, including oil and gas, agriculture and forestry, and mining. In the oil and gas sector, these are used in offshore drilling rigs, pipeline systems, hydraulic fracturing operations, and downstream equipment.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bermad CS Ltd.

- Curtiss Wright Corp.

- Danfoss AS

- Eaton Corp. Plc

- Emerson Electric Co.

- Enerpac Tool Group Corp.

- Flowserve Corp.

- HYDAC International GmbH

- Ingersoll Rand Inc.

- Kawasaki Heavy Industries Ltd.

- Parker Hannifin Corp.

- Versa Networks Inc.

- CBF SRL

- Daikin Industries Ltd.

- Duplomatic MS S.p.A.

- HAWE Hydraulik SE

- Helios Technologies Inc.

- Oilgear

- Robert Bosch GmbH

- Roquet Hydraulics S.L.

- Woodward Inc.

- HYLOC HYDROTECHNIC PVT. LTD.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Hydraulic power systems play a crucial role in various industries by converting mechanical energy from a fluid into useful work. The fluid, typically oil or water, is pressurized and circulated through a network of pipes and components, including hydraulic valves. These valves regulate the flow and pressure of the fluid to control actuator movement and positioning in machinery. Energy-efficient solutions, such as electro-hydraulic and proportional hydraulic valves, have gained popularity due to their ability to optimize energy consumption. Advanced hydraulic valves offer improved functional performance in severe conditions, making them essential in industries like construction and mining, oil and gas, agriculture and forestry, aerospace and defense, and heavy equipment.

In addition, these are integral to the operation of machinery in numerous sectors. In the renewable energy sector, they are used in pump stations and hydroelectric power plants. In industrial applications, they are employed for water production and industrial wastewater disposal, ensuring efficient and effective contamination control. In construction and mining, they are essential for directional control valves in excavating and earthmoving equipment. The market is driven by the increasing demand for hydraulic systems in various industries. The market is diverse, with applications ranging from construction machinery like dump trucks, graders, and loaders, to vehicles, automobile sector components like shock absorbers, drive systems, and brakes, and industrial equipment like bulldozers, tractor scrapers, and cranes.

Furthermore, the market is subject to several factors influencing its growth. These include process parameters, piping systems, pressure fluctuations, and refining procedures in industries like chemicals & petrochemicals and energy & power. The aging infrastructure In these industries necessitates target market expansion and the replacement of conventional old equipment with high-quality hydraulic valves. The market also caters to niche applications, such as fire protection systems and mine sites. In deep mines, hydraulic valves help manage harmful gaseous substances and ensure the safe operation of critical fluid systems. In the automobile sector, hydraulic valves contribute to fuel efficiency and emissions reduction, making them essential components in vehicles.

In addition, hydraulic valves are available in various types, including flow control valves, pressure control valves, relief valves, check valves, cartridge valves, and proportional valves. These valves are designed to meet specific application requirements and operate under various conditions, from low-pressure drop to high-pressure environments.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

188 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.15% |

|

Market growth 2024-2028 |

USD 3.27 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.27 |

|

Key countries |

US, China, Japan, UK, and France |

|

Competitive landscape |

Leading Companies, market growth and forecasting, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the ndustry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -