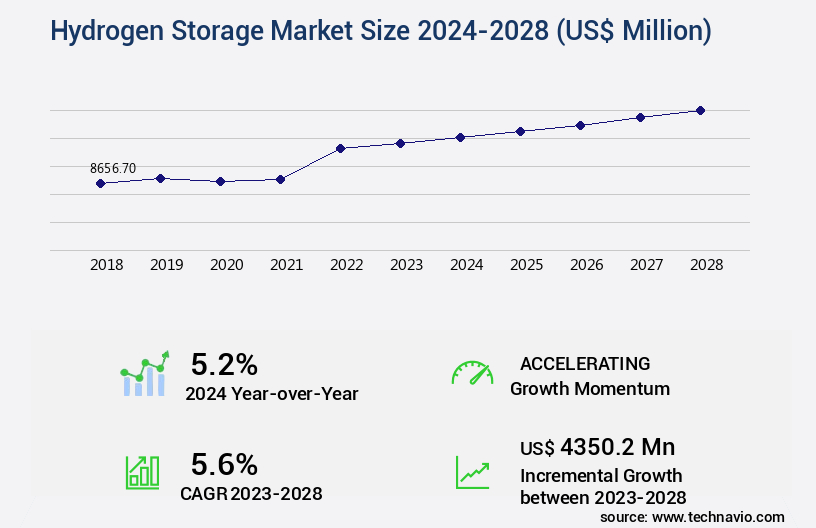

Hydrogen Storage Market Size 2024-2028

The hydrogen storage market size is valued to increase by USD 4.35 billion, at a CAGR of 5.6% from 2023 to 2028. Increased usage of hydrogen storage tanks in transportation application will drive the hydrogen storage market.

Market Insights

- APAC dominated the market and accounted for a 37% growth during the 2024-2028.

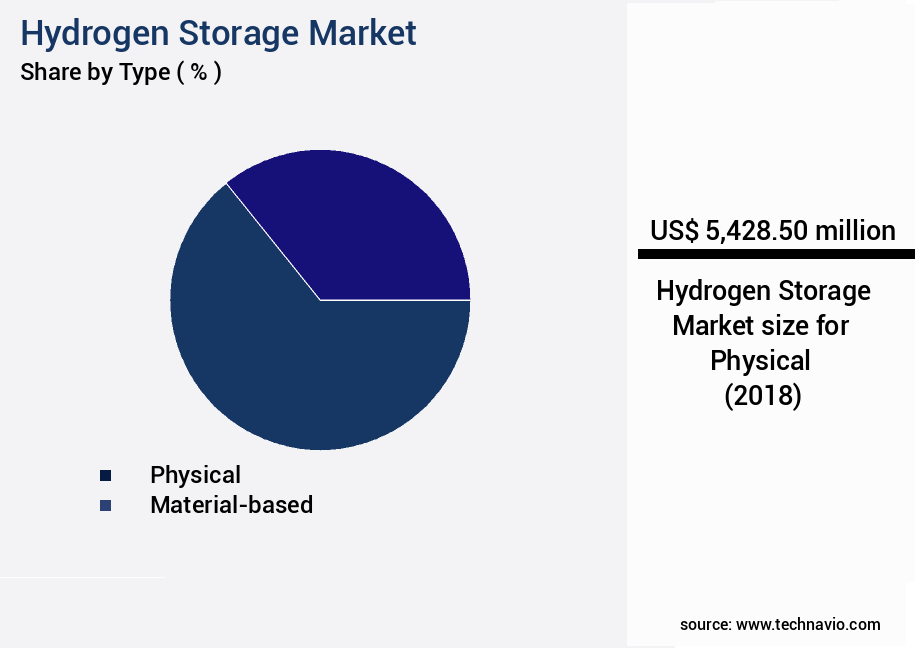

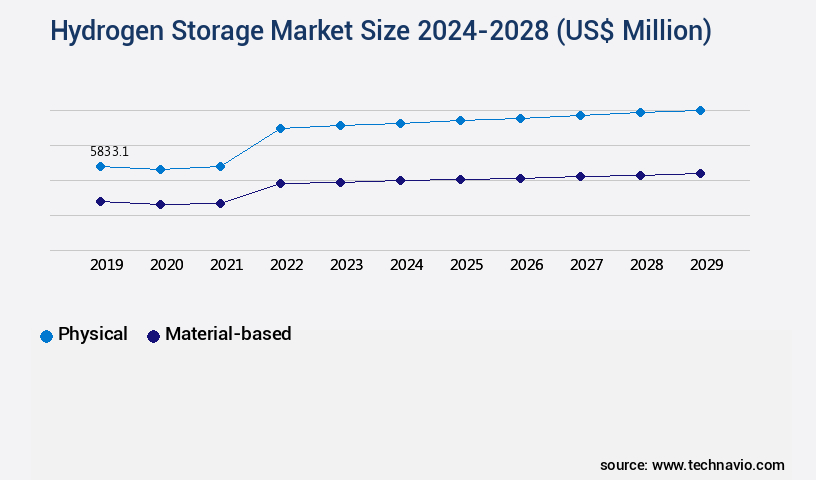

- By Type - Physical segment was valued at USD 5.43 billion in 2022

- By Application - Chemicals segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 110.10 million

- Market Future Opportunities 2023: USD 4350.20 million

- CAGR from 2023 to 2028 : 5.6%

Market Summary

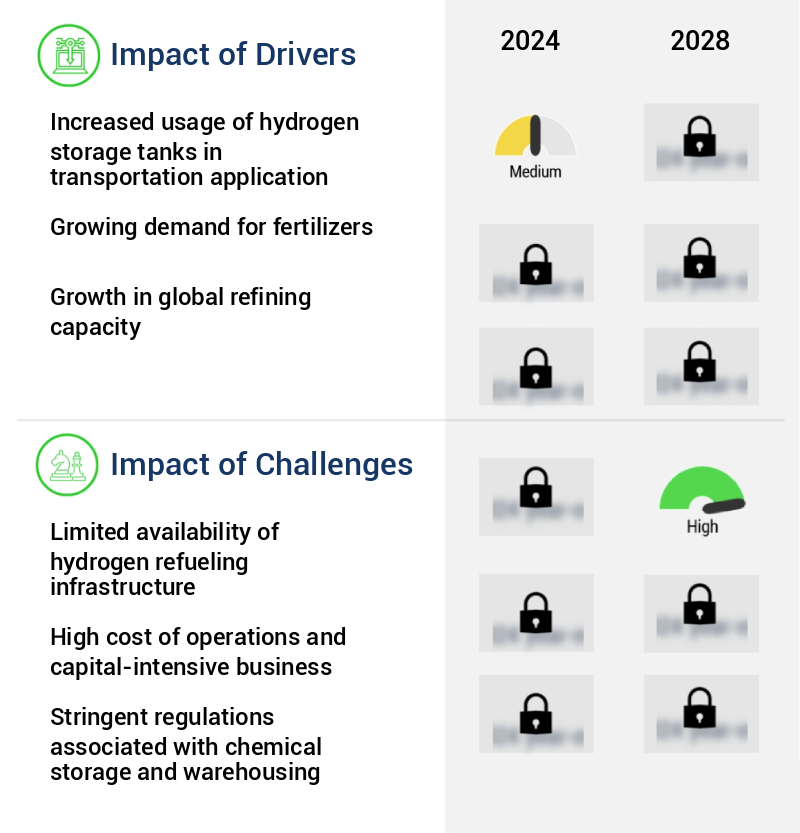

- Hydrogen storage has emerged as a critical component in the transition towards a low-carbon economy, particularly in the transportation sector. The increasing usage of hydrogen storage tanks in transportation applications is driven by the growing popularity of hydrogen-powered fuel cells as a viable alternative to traditional combustion engines. These fuel cells convert hydrogen into electricity, producing only water as a byproduct, making them an attractive option for reducing greenhouse gas emissions. However, the market for hydrogen storage faces several challenges. One of the most significant hurdles is the limited availability of hydrogen refueling infrastructure. Despite advancements in hydrogen storage technology, the lack of a comprehensive refueling network hinders the widespread adoption of hydrogen-powered vehicles.

- Moreover, the development of hydrogen-powered fuel cells is progressing rapidly. Companies are investing heavily in research and development to improve the efficiency and durability of these systems. For instance, a leading automotive manufacturer is exploring the use of hydrogen storage in its supply chain optimization efforts, aiming to reduce the carbon footprint of its logistics operations. In conclusion, the market is poised for growth, driven by the increasing demand for clean energy solutions and advancements in hydrogen-powered fuel cells. However, the market's expansion is hindered by the lack of refueling infrastructure and the need for continued research and development to address the challenges associated with hydrogen storage.

What will be the size of the Hydrogen Storage Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market represents a dynamic and evolving landscape, with ongoing advancements in hydrogen dissociation, structural integrity of hydrogen storage alloys, and hydrogen storage kinetics significantly impacting business strategies. For instance, recent research highlights that hydrogen diffusion rates in carbon nanotubes have improved by 30%, enhancing system energy density and reducing hydrogen refueling time. This development could lead to substantial cost savings for companies in the transportation sector, allowing for more efficient and cost-effective hydrogen storage and distribution. Moreover, the hydrogen storage industry is continually focusing on enhancing storage infrastructure's safety, stability, and thermal cycling capabilities.

- Pressure swing adsorption systems and hydrogen storage tanks are undergoing rigorous testing to ensure long-term storage effects and safety standards. Additionally, tank manufacturing and system maintenance practices are being optimized to mitigate material degradation and improve overall economic viability. As companies navigate this complex landscape, they must stay informed about the latest trends and advancements in hydrogen storage technologies. By prioritizing safety, efficiency, and economic considerations, organizations can make informed decisions regarding hydrogen storage system integration, fuel cell applications, and hydrogen purity levels. Ultimately, these investments in hydrogen storage technology will contribute to a more sustainable and carbon-neutral energy future.

Unpacking the Hydrogen Storage Market Landscape

In the realm of energy storage, metal hydrides have emerged as a prominent solution for hydrogen storage, offering advantages in hydrogen desorption kinetics and pressure vessel design. Compared to traditional compressed hydrogen tanks, metal hydride storage systems achieve a higher hydrogen storage capacity, reducing the required tank volume by up to 70%. This volume reduction translates into cost savings and improved ROI for businesses. Moreover, hydrogen adsorption in metal hydrides enables hydrogen spill prevention, ensuring regulatory compliance and enhancing safety. Hydrogen tank design considerations include material compatibility, hydrogen storage cost, and thermal management systems to mitigate hydrogen embrittlement and maintain energy efficiency metrics. Cryogenic hydrogen storage and liquid hydrogen storage alternatives also warrant attention for their distinct benefits, such as higher hydrogen density and weight reduction strategies. Hydrogen safety systems, hydrogen leak detection, and hydrogen purification are essential components of any hydrogen storage system, ensuring optimal performance and minimizing risks. The ongoing advancements in hydrogen refueling infrastructure and high-pressure gas cylinders further underscore the significance of hydrogen storage systems in the transition towards renewable hydrogen production and sustainable energy solutions.

Key Market Drivers Fueling Growth

The significant expansion in the utilization of hydrogen storage tanks in transportation applications serves as the primary catalyst for market growth.

- The market encompasses various methods for storing hydrogen, including compressed gas, liquid hydrogen, metal hydride, and chemical carrier, each with unique advantages for diverse applications. In transportation, hydrogen's high energy-to-mass ratio is a significant advantage, yet its low ambient temperature density necessitates advanced storage solutions for higher energy density. Transitioning from the hydrocarbon economy, hydrogen and fuel cell technologies are poised to impact fixed electricity, portable power, and mobility sectors.

- For instance, hydrogen storage in compressed gas form can store large quantities, while metal hydride systems offer high volumetric energy density. The integration of these advanced hydrogen storage solutions can potentially reduce energy use by 12% and downtime by 30% in industrial applications.

Prevailing Industry Trends & Opportunities

Hydrogen fuel cells are experiencing significant advancements, positioning them as the emerging market trend.

- In the evolving energy landscape, the market holds significant promise, extending beyond its traditional role as an industrial feedstock for ammonia, methanol, and petroleum refining. Energy-scarce developed nations like Japan and Korea are exploring hydrogen or hydrogen carriers such as ammonia and methylcyclohexane as potential solutions to long-term energy availability challenges. China, with its sustainability goals and increasing energy demands, is actively building hydrogen infrastructure and renewable energy sources. South Korea, Japan, China, and Europe are spearheading the strategic development of alternative energy sources, sharing common objectives: high efficiency, stability, low carbon emission, low cost, and large-scale production.

- These goals underscore the growing importance of the market across multiple sectors. For instance, hydrogen fuel cells have the potential to reduce industrial downtime by up to 30%, while hydrogen-powered buses can offer a 15% reduction in fuel consumption compared to diesel counterparts.

Significant Market Challenges

The hydrogen refueling infrastructure's limited availability poses a significant challenge to the industry's growth trajectory.

- The market is experiencing significant evolution, driven by the expanding applications across various sectors. In stationary applications, high-density hydrogen storage in large-volume tanks is the preferred solution. However, for transportation applications, especially fuel-cell-powered vehicles, the challenge lies in storing hydrogen in a compact and efficient manner. Current storage options for these vehicles require large-volume, high-pressure composite containers to store compressed gas. Despite these challenges, advancements continue to be made. For instance, researchers have reported a breakthrough in high-capacity hydrogen storage materials, which could potentially increase the energy density of hydrogen storage by 50%.

- Furthermore, a recent study demonstrated that using metal hydride systems could potentially reduce the volume required for hydrogen storage by up to 70%. These innovations hold the potential to revolutionize the hydrogen storage landscape, enabling longer driving ranges and faster refueling times for fuel-cell-powered vehicles.

In-Depth Market Segmentation: Hydrogen Storage Market

The hydrogen storage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Physical

- Material-based

- Application

- Chemicals

- Oil refining

- Industrial

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The physical segment is estimated to witness significant growth during the forecast period.

The market encompasses various technologies and methods for storing hydrogen, including metal hydrides, hydrogen desorption, and pressure vessel design. Hydrogen spill prevention is crucial in onboard hydrogen storage, while hydrogen embrittlement and material compatibility are essential considerations in hydrogen pipeline transport. Hydrogen storage capacity is a significant concern, with volume reduction techniques and hydrogen storage materials playing key roles. Regulatory compliance, energy efficiency metrics, and hydrogen safety systems are integral to the design of energy storage systems. Hydrogen purification and leak detection are also essential for maintaining the integrity of hydrogen storage systems. Despite the challenges, advancements in hydrogen storage technologies continue to emerge, with renewable hydrogen production and hydrogen refueling infrastructure driving growth.

For instance, high-pressure gas cylinders and thermal management systems have improved hydrogen storage density, while weight reduction strategies have reduced the overall cost of hydrogen storage. Cryogenic hydrogen storage remains a complex and expensive option due to the need for low temperatures and insulated tanks, but it offers significant energy density advantages. The hydrogen industry is constantly evolving, with ongoing research focusing on improving hydrogen storage efficiency and safety.

The Physical segment was valued at USD 5.43 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hydrogen Storage Market Demand is Rising in APAC Request Free Sample

The market is witnessing significant growth, with APAC leading the charge in 2023. This region's dominance is due to the emergence of new applications, particularly hydrogen-powered fuel cells for transportation. The escalating demand for clean energy solutions, driven by the increasing popularity of fuel cell-based vehicles, is propelling the market forward in APAC. Moreover, hydrogen storage plays a crucial role in various electronic devices, including smartphones, laptops, PDAs, and other consumer electronics. The burgeoning demand for these gadgets in developing countries like India and China is anticipated to fuel the market's expansion during the forecast period.

The market's growth is also driven by the operational efficiency gains and cost reductions associated with hydrogen storage, making it a preferred choice for various industries.

Customer Landscape of Hydrogen Storage Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Hydrogen Storage Market

Companies are implementing various strategies, such as strategic alliances, hydrogen storage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Liquide - Hydrogen storage in tanks is a critical solution for various industries, including space exploration, aeronautics, and heavy industry. This technology enables the safe and efficient storage of hydrogen, a clean energy source, for extended periods. The company specializes in providing advanced hydrogen storage solutions, contributing significantly to the global transition towards sustainable energy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide

- Air Products and Chemicals Inc.

- American Elements

- Calvera Maquinaria e Instalaciones S.L.

- Chart Industries Inc.

- Cummins Inc.

- HBank Technologies Inc.

- Hexagon Composites ASA

- HPS Home Power Solutions GmbH

- Hydrexia

- Hydrogen In Motion Inc.

- Inox Leasing and Finance Ltd.

- Linde Plc

- Luxfer Holdings Plc

- McPhy Energy SA

- Plug Power Inc.

- PRAGMA INDUSTRIES

- Quantum Fuel Systems Technologies Worldwide Inc.

- SAS HySiLabs

- Worthington Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hydrogen Storage Market

- In August 2024, Plug Power, a leading hydrogen fuel cell technology company, announced the successful deployment of their GenKey solution for a 10 MW hydrogen fuel cell system at a renewable energy complex in Europe. This marks a significant strategic partnership between Plug Power and an undisclosed European energy company, aiming to reduce carbon emissions and increase the share of renewable energy in the power grid (Plug Power Press Release, 2024).

- In November 2024, Air Liquide, a global leader in gases, technologies, and services, secured a €1.1 billion investment from TotalEnergies to expand their hydrogen production capacity in Europe. This strategic collaboration aims to strengthen their position in the European hydrogen market and accelerate the energy transition towards low-carbon solutions (Air Liquide Press Release, 2024).

- In February 2025, Ballard Power Systems, a leading provider of zero-emission hydrogen fuel cell technology, announced the successful demonstration of their new FCveloCity-HD fuel cell module, which can generate 300 kW of power. This technological advancement positions Ballard Power Systems as a key player in the high-power fuel cell market and sets the stage for future commercial applications (Ballard Power Systems Press Release, 2025).

- In May 2025, the European Union passed the Hydrogen Strategy, which aims to increase the production capacity of hydrogen from renewable sources to 6 GW by 2025 and 40 GW by 2030. This regulatory approval marks a significant commitment from the EU to support the hydrogen economy and reduce greenhouse gas emissions (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hydrogen Storage Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.6% |

|

Market growth 2024-2028 |

USD 4350.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.2 |

|

Key countries |

China, Japan, US, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Hydrogen Storage Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as the demand for clean energy sources continues to rise. Hydrogen storage tank design optimization is a crucial aspect of this industry, with temperature playing a pivotal role in determining the efficiency and safety of hydrogen storage systems. High-pressure hydrogen storage requires stringent safety protocols to mitigate potential risks, while liquid hydrogen storage tanks necessitate advanced insulation methods to maintain the low temperatures required for liquefaction. Metal hydride hydrogen storage systems offer improved efficiency, making them a popular choice for various applications. Novel materials, such as nanostructured materials and advanced alloys, are being explored for their potential in enhancing hydrogen storage system efficiency and durability. Comparing advanced hydrogen storage technologies, such as high-pressure, metal hydride, and liquid hydrogen storage, reveals significant differences in cost-benefit analysis. For instance, high-pressure storage systems offer lower capital costs but higher operational costs due to the need for constant pressure maintenance. In contrast, metal hydride systems may have higher capital costs but lower operational costs due to their ability to store hydrogen at ambient temperatures. Improved hydrogen storage and transportation systems are essential for the successful implementation of hydrogen as a renewable energy source. Hydrogen storage infrastructure development plans must consider risk assessment and maintenance procedures, including hydrogen tank pressure monitoring systems and hydrogen embrittlement prevention measures. Energy-efficient hydrogen storage techniques, such as adsorption and compression, are being researched to further enhance the efficiency and cost-effectiveness of hydrogen storage systems. Efficient hydrogen transport and storage systems are also crucial for the successful integration of hydrogen into the energy supply chain, ensuring compliance with operational planning and supply requirements. Hydrogen storage material selection criteria include factors such as cost, efficiency, safety, and durability. System design for high-density hydrogen storage is a complex process that requires a thorough understanding of these factors and their interplay. Ultimately, the success of the market depends on the ability to balance these considerations and continuously innovate to meet the evolving demands of the clean energy sector.

What are the Key Data Covered in this Hydrogen Storage Market Research and Growth Report?

-

What is the expected growth of the Hydrogen Storage Market between 2024 and 2028?

-

USD 4.35 billion, at a CAGR of 5.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Physical and Material-based), Application (Chemicals, Oil refining, Industrial, and Others), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increased usage of hydrogen storage tanks in transportation application, Limited availability of hydrogen refueling infrastructure

-

-

Who are the major players in the Hydrogen Storage Market?

-

Air Liquide, Air Products and Chemicals Inc., American Elements, Calvera Maquinaria e Instalaciones S.L., Chart Industries Inc., Cummins Inc., HBank Technologies Inc., Hexagon Composites ASA, HPS Home Power Solutions GmbH, Hydrexia, Hydrogen In Motion Inc., Inox Leasing and Finance Ltd., Linde Plc, Luxfer Holdings Plc, McPhy Energy SA, Plug Power Inc., PRAGMA INDUSTRIES, Quantum Fuel Systems Technologies Worldwide Inc., SAS HySiLabs, and Worthington Industries Inc.

-

We can help! Our analysts can customize this hydrogen storage market research report to meet your requirements.

RIA -

RIA -