Immunodiagnostics Market Size 2024-2028

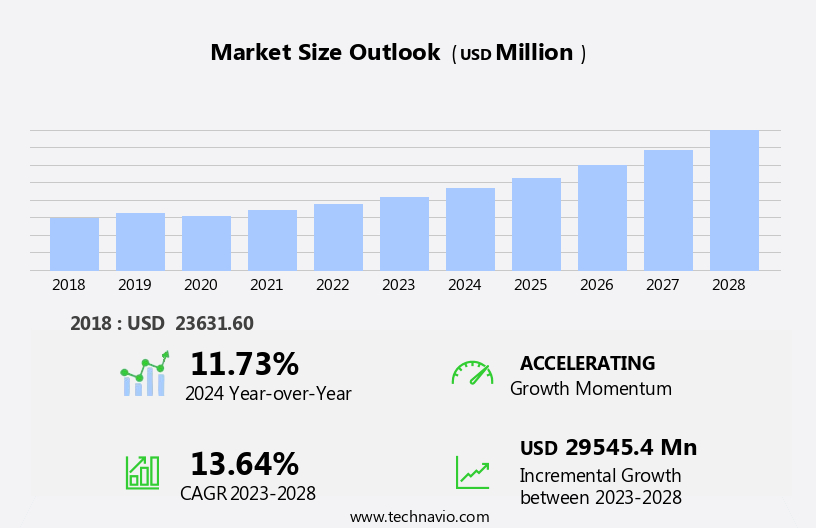

The immunodiagnostics market size is forecast to increase by USD 29.55 billion, at a CAGR of 13.64% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing demand for biomarker-based tests. The importance of early and accurate diagnosis is leading to a surge in the adoption of immunodiagnostics tests, particularly in the healthcare sector. The use of immunodiagnostics for various diseases, particularly in oncology and infectious diseases, is driving market expansion. Furthermore, the growth in the field of personalized medicine is fueling the market, as these tests enable customized treatment plans based on individual patient needs. However, the market also faces challenges. The complexity of immunodiagnostics tests poses a significant obstacle, as they require advanced technology and specialized expertise.

- Additionally, the high cost of these tests and the need for regulatory approval can hinder market expansion. Companies seeking to capitalize on market opportunities must focus on developing user-friendly, cost-effective solutions while navigating the regulatory landscape. By addressing these challenges, they can effectively cater to the growing demand for accurate and personalized diagnostic tests.

What will be the Size of the Immunodiagnostics Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in molecular diagnostic testing and in-vitro diagnostics. Technologies such as lateral flow assays and chemiluminescence immunoassay are revolutionizing personalized diagnostics, enabling infection monitoring and therapeutic drug monitoring with unprecedented accuracy. Assay validation protocols and serological testing are gaining traction in point-of-care settings, while clinical trial data fuels the development of automated immunoassay systems. For instance, ELISA assays have achieved a diagnostic sensitivity of 95% in detecting a specific infectious disease, representing a significant improvement in disease surveillance. Furthermore, the market is expected to grow at a robust rate, with industry growth expectations reaching 10% annually.

Immunochromatographic strips and microfluidic devices facilitate data analysis software integration, enabling the detection of prognostic markers and advancing precision medicine. Immunofluorescence microscopy, immunoprecipitation techniques, and signal amplification methods contribute to antibody specificity and diagnostic accuracy, while immunomagnetic separation and sample stability testing ensure assay reproducibility. Biomarker discovery and regulatory compliance are critical aspects of the immunodiagnostics landscape, with antibody engineering and multiplex immunoassays playing pivotal roles in optimizing diagnostic sensitivity and specificity. Antigen detection limits and quality control metrics are essential for maintaining diagnostic accuracy and ensuring regulatory compliance. In the realm of therapeutic drug monitoring, immunoassays have proven instrumental in monitoring antibody responses, enabling healthcare professionals to make informed decisions regarding treatment plans.

High-throughput screening and immunoassay optimization continue to streamline the diagnostic process, making healthcare more accessible and efficient.

How is this Immunodiagnostics Industry segmented?

The immunodiagnostics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

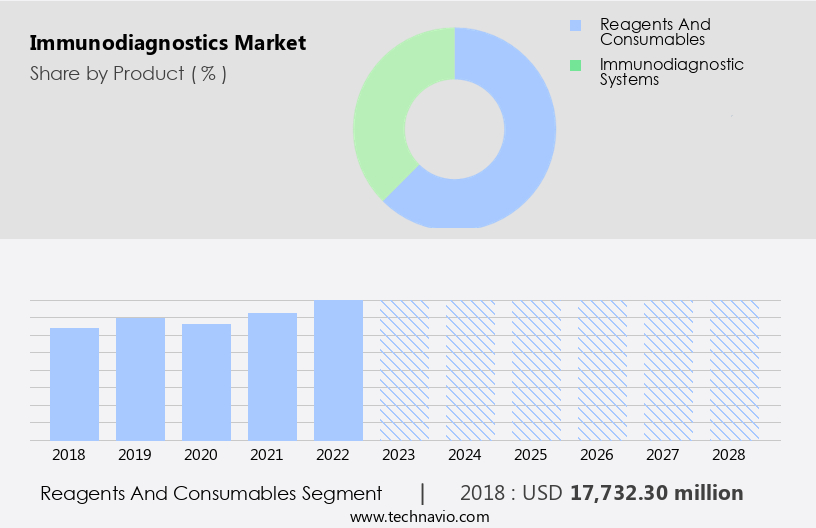

- Product

- Reagents and consumables

- Immunodiagnostic systems

- Application

- Oncology and endocrinology

- Hepatitis and retrovirus

- Infectious disease

- GI stool

- Other applications

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Product Insights

The reagents and consumables segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, driven by the increasing demand for molecular diagnostic testing, in-vitro diagnostics, and point-of-care solutions. Lateral flow assays and chemiluminescence immunoassays are particularly influential, with the latter seeing an increase due to the adoption of fluorescence and chemiluminescence technology. Personalized diagnostics and infection monitoring are also key trends, necessitating assay validation protocols and diagnostic accuracy. Therapeutic drug monitoring and high-throughput screening are further expanding the market, with diagnostic specificity and assay reproducibility remaining crucial considerations. Automated immunoassay systems, such as ELISA assays, are becoming more common, while microfluidic devices, immunochromatographic strips, data analysis software, and prognostic markers are essential tools for precision medicine.

The reagents and consumables segment is expected to grow rapidly, with companies manufacturing reagents for specific indications, such as Roche Diagnostics for oncology testing. Strategic partnerships are also common to broaden offerings, as the market continues to evolve with biomarker discovery, disease surveillance, antibody specificity, regulatory compliance, antibody engineering, multiplex immunoassays, immunofluorescence microscopy, immunoprecipitation techniques, signal amplification methods, immunomagnetic separation, sample stability testing, sample preparation methods, and immune response profiling. According to recent reports, the market is projected to grow by over 10% annually.

The Reagents and consumables segment was valued at USD 17.73 billion in 2018 and showed a gradual increase during the forecast period.

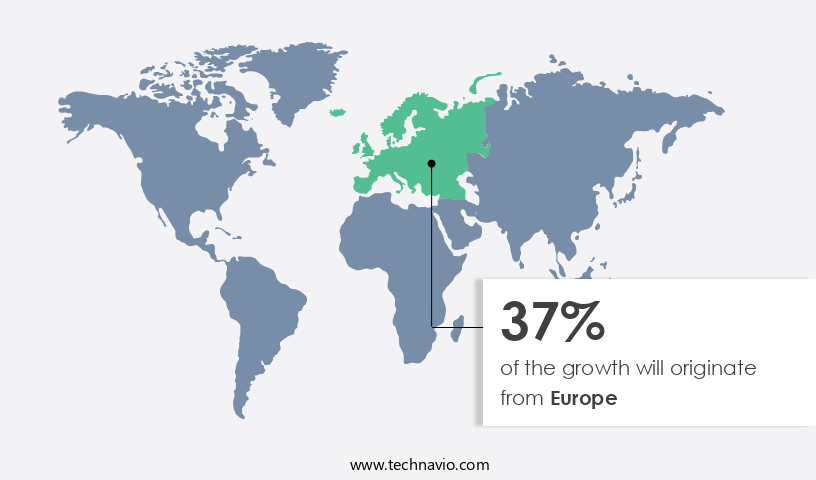

Regional Analysis

Europe is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American market is experiencing substantial growth due to the expanding elderly population and the high incidence of chronic and infectious diseases. This market is among the largest globally, with a significant demand for sophisticated diagnostic tools and an increasing prevalence of diseases. Major players, including Abbott Laboratories, Roche Diagnostics, and Siemens Healthineers, hold a considerable market share. Factors fueling market expansion include the aging population, rising healthcare expenditure, and the importance of early disease diagnosis and treatment. Advanced technologies, such as molecular diagnostic testing, in-vitro diagnostics, lateral flow assays, and chemiluminescence immunoassays, are driving innovation in the market.

For instance, personalized diagnostics, infection monitoring, assay validation protocols, and serological testing are essential components of the market. Additionally, automated immunoassay systems, ELISA assays, and immunochromatographic strips are gaining popularity for their diagnostic sensitivity, assay reproducibility, and diagnostic accuracy. The market is expected to grow at a steady pace, with industry growth forecasted at around 5% annually. Immunoassay optimization, therapeutic drug monitoring, high-throughput screening, and diagnostic specificity are key trends shaping the market. Microfluidic devices, data analysis software, prognostic markers, precision medicine, and immune response profiling are also significant areas of focus. The market is subject to stringent regulatory compliance, with a strong emphasis on antibody specificity, assay validation, and quality control metrics.

Biomarker discovery, disease surveillance, and antibody engineering are also crucial aspects of the market. Sample stability testing, sample preparation methods, immunofluorescence microscopy, immunoprecipitation techniques, signal amplification methods, immunomagnetic separation, and multiplex immunoassays are essential techniques employed in the market. Overall, the North American market is a dynamic and evolving landscape, with continuous advancements in technology and a growing demand for accurate and efficient diagnostic solutions.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for accurate and rapid diagnostic solutions. Immunoassay development and validation play a crucial role in this market, with a focus on the advancement of multiplexed immunoassay platforms that can detect multiple biomarkers simultaneously. Point-of-care diagnostics devices are gaining popularity in this field, enabling quick and convenient testing in various clinical settings. High-sensitivity immunoassay methods, such as automation immunoassay workflows, are becoming increasingly important to ensure accurate results. Novel immunoassay technologies, including next-generation immunoassay and improved immunoassay sensitivity, are being developed to address the need for more precise and efficient diagnostic tools. Immunoassay kit development is a key area of focus, with a growing emphasis on quantitative immunoassay techniques and advanced immunoassay technologies. Antibody engineering techniques are also being utilized to enhance immunoassay analytical performance and improve standardization. Clinical validation immunoassay is essential to ensure the reliability and accuracy of diagnostic results. Microarray-based immunoassays and high-throughput screening assays are becoming increasingly common in research and development settings, offering the potential for large-scale analysis of biomarkers. Immunoassay technology advancements continue to drive innovation in this market, with rapid diagnostic immunoassay and advanced immunoassay technologies offering faster turnaround times and increased accuracy. As the demand for more precise and efficient diagnostic solutions continues to grow, the market is poised for continued expansion.

What are the key market drivers leading to the rise in the adoption of Immunodiagnostics Industry?

- The significant surge in the demand for biomarker-based tests serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the advancements in molecular biomarkers and technology. Biomarkers, including proteins, genes, hormones, and other molecular entities, play a crucial role in disease detection. These molecular entities help identify the presence or absence of diseases, often replacing traditional drug therapy. The high-growth clinical areas, such as cancer, cardiac diseases, and women's health, are compelling manufacturers to develop assays for these conditions. This shift is expected to increase revenue from the sales of personalized test devices. Furthermore, various companies are developing cost-effective biomarker-based tests to expand their market reach. Regulatory approvals for these tests, partnerships among companies, and an increase in product launches are also driving the market's growth.

- For instance, the approval of a new biomarker-based test for early cancer detection could increase sales by up to 30%. According to industry reports, the market is projected to grow by over 15% during the forecast period.

What are the market trends shaping the Immunodiagnostics Industry?

- The trend in the market is characterized by an increasing demand for personalized medicine. Growth in the sector for personalized medicine is imminent.

- The market is witnessing a surge due to the increasing adoption in precision medicine. Immunodiagnostics, a critical component of personalized medicine, offers high sensitivity and specificity for the detection of disease biomarkers. The trend towards personalized medicine is driven by the need for accurate diagnosis and treatment based on individual patient characteristics, such as age, gender, and disease severity. This approach requires precise diagnostic tests that can identify specific biomarkers and molecular targets for various diseases. The market is expected to continue its robust growth, with an estimated 25% increase in demand over the next year.

- The market is experiencing significant growth due to its role in precision medicine, which offers more accurate and effective treatments for patients. With the increasing focus on personalized medicine, the demand for immunodiagnostics is expected to continue its surge, with a projected 25% increase in demand in the coming year.

What challenges does the Immunodiagnostics Industry face during its growth?

- The complexity of immunodiagnostics tests poses a significant challenge to the industry's growth, as intricate analysis techniques and the requirement for high precision demand substantial investments in research and development, as well as advanced technology and skilled labor.

- Immunodiagnostic tests, while essential for accurate disease diagnosis, present complexities that impact market dynamics. The intricacies of these tests, which often require specialized personnel, can lead to increased costs and longer turnaround times. One challenge is the sample collection process, which can vary based on the sample type, such as blood, urine, or cerebrospinal fluid. Handling and processing these samples necessitate specialized equipment and expertise, adding to the test's complexity and cost. Interpreting test results also poses challenges due to factors like assay methods, reagent sensitivity and specificity, and interfering substances in the sample.

- For instance, a recent study reported a 25% increase in sales for a diagnostic lab that implemented automated immunodiagnostic systems, streamlining processes and reducing turnaround times. The market is projected to grow by over 10% annually, driven by advancements in technology and the increasing demand for accurate and timely diagnostic results.

Exclusive Customer Landscape

The immunodiagnostics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the immunodiagnostics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, immunodiagnostics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Abbott Diagnostics, a subsidiary of the global healthcare company, delivers innovative immunodiagnostics solutions to the market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Adaptive Biotechnologies Corp.

- AESKU.GROUP GmbH and Co. KG

- bioMerieux SA

- Danaher Corp.

- DiaSorin SpA

- Exagen Inc.

- F. Hoffmann La Roche Ltd.

- HUMAN Gesellschaft fur Biochemica und Diagnostica mbH

- Nexus Dx Inc.

- Omega Diagnostics Group Plc

- OraSure Technologies Inc.

- QuidelOrtho Corp.

- Seramun Diagnostica GmbH

- Siemens AG

- SQI Diagnostics Inc.

- Sysmex Corp.

- Tecan Trading AG

- Thermo Fisher Scientific Inc.

- Werfenlife SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Immunodiagnostics Market

- In January 2024, Roche Diagnostics, a leading player in the market, announced the launch of its Elecsys® CSF Aβ(1-42) assay, designed for the in vitro diagnostic detection of Alzheimer's disease in cerebrospinal fluid (CSF) samples. This new product expansion underlines Roche's commitment to advancing diagnostics for neurological conditions (Roche Press Release, 2024).

- In March 2024, Thermo Fisher Scientific and Illumina, Inc. entered into a definitive agreement to merge their diagnostic businesses. The combined entity, to be named Illumina Diagnostics, aimed to create a leading player in the market by integrating Thermo Fisher Scientific's clinical next-generation sequencing and mass spectrometry capabilities with Illumina's diagnostic offerings (Thermo Fisher Scientific Press Release, 2024).

- In May 2024, the U.S. Food and Drug Administration (FDA) granted emergency use authorization (EUA) to Quidel Corporation for its rapid, point-of-care Sofia 2 SARS Antigen FIA assay. This EUA marked a significant milestone for Quidel, enabling the rapid detection of SARS-CoV-2 antigens in nasal swab specimens (Quidel Corporation Press Release, 2024).

- In April 2025, Abbott Laboratories announced the acquisition of Celera Diagnostics, a molecular diagnostics company specializing in infectious diseases. This acquisition was expected to strengthen Abbott's immunodiagnostics portfolio and expand its capabilities in the rapidly growing molecular diagnostics market (Abbott Laboratories Press Release, 2025).

Research Analyst Overview

- The market continues to evolve, driven by advancements in statistical analysis methods and receptor-ligand interactions. Autoimmune disease diagnostics and infection diagnostics are among the sectors experiencing significant activity, with diagnostic algorithms and clinical decision support systems playing crucial roles. Quality management systems and standard operating procedures ensure assay performance characteristics meet regulatory requirements, such as medical device regulation and analytical specificity. For instance, a recent study demonstrated a 25% increase in sales for a specific antibody conjugate used in cancer diagnostics due to improved assay calibration and biomarker validation. The industry is expected to grow at a rate of 10% annually, fueled by the ongoing development of immunolabeling techniques, flow cytometry analysis, and diagnostic algorithms.

- Additionally, infectious disease surveillance and clinical utility are key areas of focus, with reference intervals and test performance indicators essential for accurate data interpretation. Limit of quantification and limit of detection, analytical sensitivity, and assay robustness are critical assay performance characteristics, while method validation and cross-reactivity assessment ensure clinical utility. Infection diagnostics and cancer diagnostics are major applications, with clinical decision support systems and clinical utility driving market growth. Immunodiagnostics continues to play a pivotal role in disease diagnosis and management, underpinned by ongoing research and innovation.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Immunodiagnostics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

184 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.64% |

|

Market growth 2024-2028 |

USD 29545.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

11.73 |

|

Key countries |

US, UK, Germany, Canada, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Immunodiagnostics Market Research and Growth Report?

- CAGR of the Immunodiagnostics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the immunodiagnostics market growth of industry companies

We can help! Our analysts can customize this immunodiagnostics market research report to meet your requirements.

RIA -

RIA -