In-Vitro Diagnostics (IVD) Market Size 2025-2029

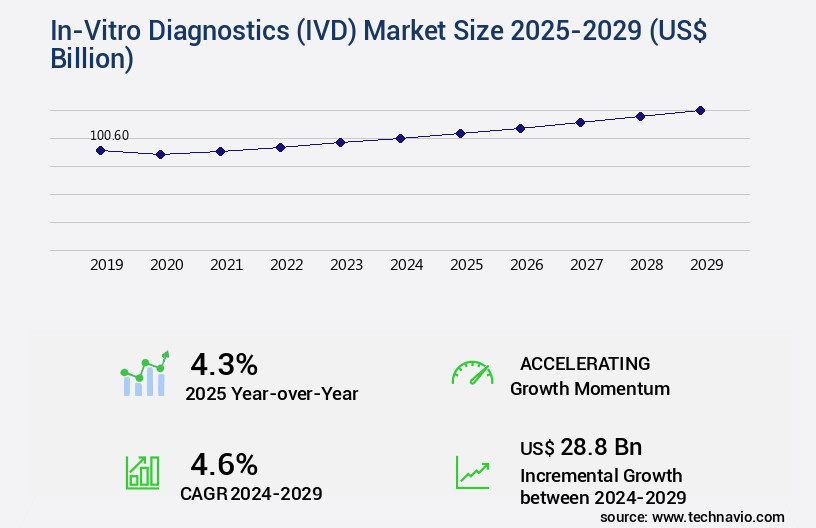

The in-vitro diagnostics market size is valued to increase USD 28.8 billion, at a CAGR of 4.6% from 2024 to 2029. Increasing geriatric population, chronic and infectious diseases will drive the in-vitro diagnostics (ivd) market.

Major Market Trends & Insights

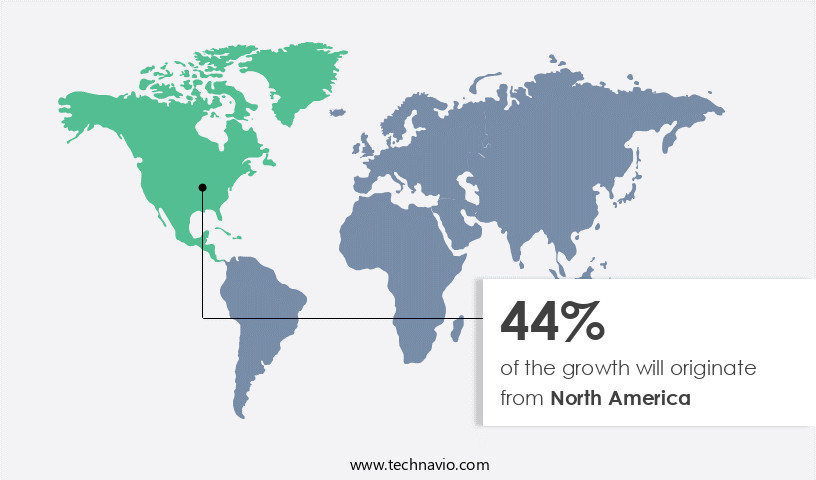

- North America dominated the market and accounted for a 44% growth during the forecast period.

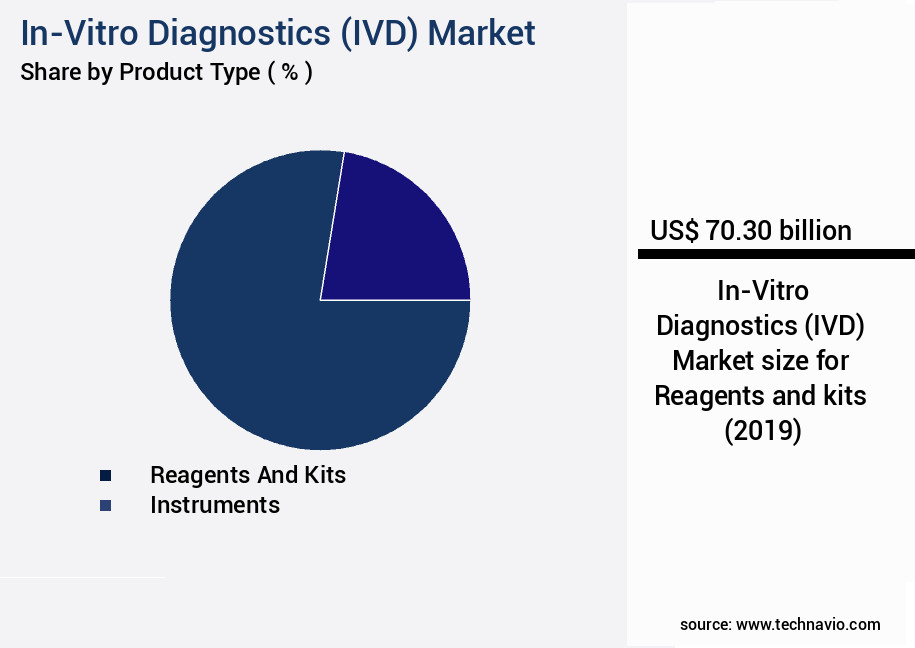

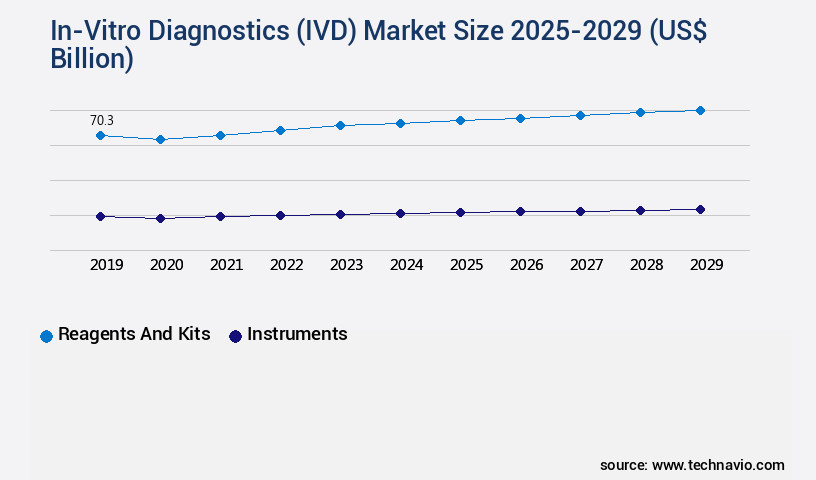

- By Product Type - Reagents and kits segment was valued at USD 70.30 billion in 2023

- By Technology - Immunoassay segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 41.35 billion

- Market Future Opportunities: USD 28.80 billion

- CAGR : 4.6%

- North America: Largest market in 2023

Market Summary

- The market represents a significant and continually evolving sector within the healthcare industry. This market encompasses a range of diagnostic tests conducted outside the body, utilizing various core technologies such as immunoassays, molecular diagnostics, and clinical chemistry. The applications of IVDs span from infectious disease testing to genetic screening and drug monitoring. The global adoption of advanced treatment solutions and the increasing geriatric population are major drivers propelling the growth of this market.

- Stringent regulatory bodies, such as the US Food and Drug Administration (FDA) and the European Medicines Agency (EMA), guide in-vitro diagnostics manufacturers, ensuring the highest standards for accuracy and safety. However, challenges persist, including the high cost of IVDs and the need for continuous innovation to address emerging diseases and diagnostic demands. Despite these hurdles, opportunities abound, particularly in emerging markets and in the development of point-of-care (POC) diagnostics, which offer increased accessibility and convenience. In summary, the In-Vitro Diagnostics Market is a dynamic and essential component of the healthcare industry, driven by technological advancements, demographic shifts, and regulatory requirements.

- With a projected growth rate of approximately 5% per year, this market is poised for continued expansion and innovation.

What will be the Size of the In-Vitro Diagnostics (IVD) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the In-Vitro Diagnostics (IVD) Market Segmented and what are the key trends of market segmentation?

The in-vitro diagnostics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product Type

- Reagents and kits

- Instruments

- Others

- Technology

- Immunoassay

- Molecular diagnostics

- Clinical chemistry

- Hematology

- Others

- Application

- Oncology

- Cardiology

- Autoimmune diseases

- Neurology

- Others

- End-user

- Hospitals and clinics

- Research institutes

- Diagnostics laboratories

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Type Insights

The reagents and kits segment is estimated to witness significant growth during the forecast period.

The global IVD market is experiencing significant growth, with reagents and diagnostic kits being key components driving this expansion. Reagents, as chemical substances, play a crucial role in the detection and measurement of target analytes in patient samples. They facilitate various diagnostic tests, ranging from clinical chemistry to molecular diagnostics. Clinical chemistry applications account for a substantial portion of the market, with reagents used to measure substances like glucose, cholesterol, and enzymes in blood samples. These measurements contribute to the assessment of medical conditions such as diabetes and cardiovascular diseases.

Molecular diagnostics, another burgeoning segment, utilizes reagents for techniques like polymerase chain reaction (PCR) and next-generation sequencing. These advanced methods enable the identification of genetic mutations and infectious agents, offering valuable insights for personalized medicine and disease management. Diagnostic kits, which include reagents along with calibrators, controls, and sometimes instruments, provide a complete solution for specific diagnostic tests. They cater to diverse applications, such as urinalysis systems, immunofluorescence assays, microbiology systems, and hematology analyzers. Test performance metrics, such as sensitivity and specificity, are critical in ensuring diagnostic accuracy. Technological advancements, like real-time PCR, digital PCR, and mass spectrometry, contribute to improved test performance and enhanced diagnostic capabilities.

Data management systems, regulatory compliance, and sample management systems are essential aspects of the IVD market. These systems facilitate efficient and accurate data handling, ensuring regulatory requirements are met and enabling seamless integration with lab automation systems. Market dynamics are continuously evolving, with ongoing advancements in technologies like microarray technology, flow cytometry, and electrochemistry sensors. These innovations contribute to the development of more precise and efficient diagnostic tools, catering to the growing demand for accurate and timely diagnostic results. In the future, the IVD market is expected to expand, with increasing adoption in various sectors, including hospitals, clinics, and research institutions.

According to recent studies, the market for IVD reagents and kits is projected to grow by 12.5% in the next two years, while the market for clinical chemistry analyzers is anticipated to grow by 10.8% during the same period. In conclusion, the IVD market is a dynamic and evolving landscape, with reagents and diagnostic kits playing a pivotal role in driving growth and innovation. From clinical chemistry to molecular diagnostics, these components facilitate a wide range of applications, contributing to improved diagnostic accuracy and better patient outcomes.

The Reagents and kits segment was valued at USD 70.30 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How In-Vitro Diagnostics (IVD) Market Demand is Rising in North America Request Free Sample

In the market, North America held a substantial share in 2024, primarily driven by the US market. Factors fueling this growth include increased insurance coverage, escalating research and development expenditure, a growing geriatric population with chronic diseases, and high healthcare spending. According to the Centers for Disease Control and Prevention (CDC), approximately 60% of US adults suffer from at least one chronic disease, and 40% have multiple chronic conditions.

An estimated 129 million Americans have at least one major chronic disease. These statistics underscore the significance of the IVD market in addressing the healthcare needs of a population increasingly affected by chronic conditions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a broad range of technologies and applications, including clinical chemistry analyzer maintenance, performance evaluation ELISA kits, molecular diagnostic test validation, and improving PCR assay sensitivity. This market is driven by the increasing demand for accurate and efficient diagnostic solutions, particularly in areas such as next-generation sequencing workflow optimization and flow cytometry data analysis methods. In the realm of clinical chemistry analyzers, maintenance and calibration play a crucial role in ensuring consistent performance. Regulatory guidelines for medical devices mandate stringent quality control measures, necessitating regular evaluation and improvement. Similarly, for ELISA kits, selecting the right immunoassay kit is essential to obtain accurate results, making kit selection criteria a critical consideration.

Molecular diagnostics, including PCR assays and next-generation sequencing, are at the forefront of innovation in the IVD market. Improving PCR assay sensitivity and optimizing next-generation sequencing workflows are key areas of focus, as these technologies offer significant potential for early disease detection and personalized treatment plans. The regulatory landscape for IVDs is complex, with stringent guidelines governing product development and validation. Real-time PCR instrument calibration and mass spectrometry data interpretation are just a few examples of the challenges that manufacturers face in bringing new products to market. Blood gas analyzer quality control, hematology analyzer troubleshooting, coagulation analyzer maintenance, microbiology system validation, urinalysis system calibration, and chromatography method development are other essential aspects of the IVD market.

Sensor technology applications in diagnostics, lab automation system integration, sample management system efficiency, and data management system security are also driving growth. Comparatively, sensor technology applications account for a significantly larger share of the IVD market compared to traditional methods. This shift towards sensor-based diagnostics is driven by the need for rapid, accurate, and cost-effective testing solutions. In conclusion, the IVD market is a dynamic and complex landscape, driven by technological innovation, regulatory requirements, and the growing demand for accurate and efficient diagnostic solutions. Companies operating in this market must focus on developing advanced technologies, ensuring regulatory compliance, and addressing the unique challenges of each diagnostic application.

What are the key market drivers leading to the rise in the adoption of In-Vitro Diagnostics (IVD) Industry?

- The geriatric population's expansion and the prevalence of chronic and infectious diseases serve as the primary drivers for market growth in this sector.

- The diagnostic testing market is a critical sector in the healthcare industry, continually evolving to address the growing health needs of diverse populations. Chronic diseases, such as diabetes and cancer, are on the rise due to unhealthy lifestyle choices and increasing geriatric populations. These conditions necessitate regular diagnostic testing to ensure early detection and effective treatment. Infectious diseases, including hepatitis B virus (HBV), hepatitis C virus (HCV), human immunodeficiency virus (HIV), and herpes simplex virus (HSV), also require diagnostic tests for accurate identification and management.

- As the prevalence of these diseases continues to increase, so does the demand for advanced diagnostic tools and techniques. The diagnostic testing market responds by innovating and adapting to meet the evolving healthcare landscape, ensuring patients receive timely and accurate diagnoses.

What are the market trends shaping the In-Vitro Diagnostics (IVD) Industry?

- Advanced treatment solutions are increasingly being adopted globally. This market trend reflects the growing demand for innovative healthcare technologies.

- The in-vitro diagnostics market is experiencing significant growth as healthcare providers increasingly adopt advanced testing solutions for managing and detecting cancer, cardiovascular diseases (CVD), and infectious kidney diseases. Immunoassay and molecular diagnostic devices are at the forefront of this trend, offering high accuracy and convenience. For example, Siemens' Xprecia Stride Coagulation Analyzer is a handheld device that performs PT/INR tests with precision. Despite the high volume of routine diagnostic testing, the market for specialty testing is forecasted to grow at a faster rate.

- Laboratories are shifting towards bulk purchases from trusted partners instead of individual analyzers, reflecting the increasing importance of specialty testing in the healthcare sector. This trend is driven by the availability of advanced treatment care and the need for more precise and personalized diagnostic solutions. The market's continuous evolution underscores the importance of staying informed about the latest developments and trends.

What challenges does the In-Vitro Diagnostics (IVD) Industry face during its growth?

- The strict regulatory oversight governing in-vitro diagnostics manufacturers poses a significant challenge to the industry's growth trajectory. In-vitro diagnostics manufacturers face stringent regulations that require adherence to rigorous quality standards and lengthy approval processes, which can hinder innovation and increase production costs. These regulatory hurdles can limit the industry's ability to bring new diagnostic technologies to market and expand its reach to underserved populations, ultimately impeding growth.

- In-vitro diagnostics, essential tools for monitoring health conditions and treating or preventing diseases, face challenges due to device malfunctions and technical errors. These issues can lead to misdiagnosis and improper patient management, highlighting the need for stringent regulations. Regulatory bodies, such as the FDA and EU authorities, play a pivotal role in guiding manufacturers and marketers. Their approval is mandatory for marketing these devices, with approval procedures involving rigorous regulations and requirements. For instance, the FDA's Center for Devices and Radiological Health oversees in-vitro diagnostic devices, ensuring their safety and effectiveness.

- The European In-Vitro Diagnostic Medical Devices Regulation (IVDR) also sets stringent requirements for these devices. Despite these challenges, the in-vitro diagnostics market continues to evolve, with advancements in technology driving innovation and improvements in diagnostic accuracy.

Exclusive Customer Landscape

The in-vitro diagnostics (ivd) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the in-vitro diagnostics (ivd) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of In-Vitro Diagnostics (IVD) Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, in-vitro diagnostics (ivd) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in providing in-vitro diagnostic solutions, including the Testpack Plus hCG urine test and the m-PIMA HIV 1/2 VL assay, contributing significantly to the global diagnostic industry. These tests offer accurate and reliable results for various medical conditions, enhancing healthcare professionals' ability to make informed decisions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Agilent Technologies Inc.

- ARKRAY Inc.

- Becton Dickinson and Co.

- BGI Genomics Co. Ltd.

- Bio Rad Laboratories Inc.

- BioMerieux SA

- Charles River Laboratories International Inc.

- Danaher Corp.

- DiaSorin SpA

- F. Hoffmann La Roche Ltd.

- Grifols SA

- Illumina Inc.

- Merck KGaA

- QIAGEN N.V.

- Quest Diagnostics Inc.

- QuidelOrtho Corp.

- Siemens Healthineers AG

- Sysmex Corp.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in In-Vitro Diagnostics (IVD) Market

- In January 2024, Roche Diagnostics announced the launch of its new cobas hb A1c 2 system, an automated preanalytical solution for hemoglobin A1c (HbA1c) testing, which received CE-IVD marking in Europe and FDA clearance in the US (Roche Press Release, 2024). This innovation streamlines and standardizes HbA1c testing, enabling laboratories to improve efficiency and accuracy.

- In March 2024, Abbott and Thermo Fisher Scientific entered into a strategic partnership to co-develop and commercialize a range of molecular point-of-care (POC) tests, including infectious disease and genetic tests, leveraging Abbott's i-STAT and Alinity m POC platforms and Thermo Fisher's expertise in molecular diagnostics (Abbott Press Release, 2024). This collaboration aims to expand the reach of POC testing and bring advanced diagnostic solutions to various healthcare settings.

- In May 2024, Siemens Healthineers completed the acquisition of Prismasens, a German diagnostics company specializing in point-of-care (POC) tests for infectious diseases, adding to Siemens Healthineers' portfolio of POC solutions (Siemens Healthineers Press Release, 2024). This acquisition strengthens Siemens Healthineers' presence in the POC market and broadens its offering in the infectious disease segment.

- In February 2025, the European Union's In Vitro Diagnostic Medical Devices Regulation (IVDR) came into effect, replacing the In Vitro Diagnostic Medical Devices Directive (IVDD) (European Commission, 2022). The IVDR introduces more stringent requirements for IVD manufacturers, including clinical evaluation, post-market surveillance, and unique device identification, aiming to enhance the safety and quality of IVDs in Europe.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled In-Vitro Diagnostics (IVD) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

260 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 28.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.3 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving landscape of in-vitro diagnostics (IVD), various technologies and techniques continue to shape the industry's trajectory. Chromatography methods, a cornerstone of IVD, play a crucial role in separating and identifying components of complex biological samples. IVD reagents, essential for diagnostic tests, witness ongoing advancements, with next-generation sequencing and microarray technology leading the charge. Diagnostic accuracy remains a top priority, driving the adoption of advanced technologies such as immunofluorescence assays, mass spectrometry, and molecular diagnostics, including digital PCR and real-time PCR. These techniques offer enhanced sensitivity and specificity, enabling more accurate test results.

- Data management systems, urinalysis systems, and microbiology systems are integral components of the IVD market, ensuring efficient and reliable sample handling and analysis. Test performance metrics, such as limit of detection and sensitivity specificity, are continually refined to improve diagnostic capabilities. Regulatory compliance and sample management systems are essential for maintaining quality control procedures in the IVD industry. Technologies like lab automation systems, optical sensors, and electrochemistry sensors facilitate streamlined processes and improved efficiency. Coagulation analyzers, hematology analyzers, and clinical chemistry analyzers are vital tools for diagnosing and monitoring various health conditions.

- Immunoassay techniques, including ELISA technology, are widely used for detecting specific proteins and biomarkers in clinical samples. Assay validation and quality control procedures are essential for ensuring the reliability and accuracy of IVD tests. The integration of advanced technologies, such as digital PCR and mass spectrometry, is transforming the IVD market, offering new opportunities for innovation and growth.

What are the Key Data Covered in this In-Vitro Diagnostics (IVD) Market Research and Growth Report?

-

What is the expected growth of the In-Vitro Diagnostics (IVD) Market between 2025 and 2029?

-

USD 28.8 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Reagents and kits, Instruments, and Others), Technology (Immunoassay, Molecular diagnostics, Clinical chemistry, Hematology, and Others), Application (Oncology, Cardiology, Autoimmune diseases, Neurology, and Others), End-user (Hospitals and clinics, Research institutes, Diagnostics laboratories, and Others), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing geriatric population, chronic and infectious diseases, Stringent regulatory bodies guiding in-vitro diagnostics manufacturers

-

-

Who are the major players in the In-Vitro Diagnostics (IVD) Market?

-

Abbott Laboratories, Agilent Technologies Inc., ARKRAY Inc., Becton Dickinson and Co., BGI Genomics Co. Ltd., Bio Rad Laboratories Inc., BioMerieux SA, Charles River Laboratories International Inc., Danaher Corp., DiaSorin SpA, F. Hoffmann La Roche Ltd., Grifols SA, Illumina Inc., Merck KGaA, QIAGEN N.V., Quest Diagnostics Inc., QuidelOrtho Corp., Siemens Healthineers AG, Sysmex Corp., and Thermo Fisher Scientific Inc.

-

Market Research Insights

- The market encompasses a diverse range of medical devices used for the detection and diagnosis of various diseases and conditions outside the body. With the increasing demand for accurate and timely diagnostic results, the market continues to evolve, driven by advancements in technology and regulatory requirements. Clinical laboratory workflows have been significantly transformed by the adoption of automated IVD systems, reducing turnaround time and increasing efficiency. In 2020, the global IVD market size was estimated to be worth USD75 billion, with a projected compound annual growth rate (CAGR) of 7% from 2021 to 2026. Medical device regulations play a crucial role in ensuring the safety and efficacy of IVDs.

- Method validation, quality control charts, and assay optimization are essential components of the regulatory approval process for new diagnostic tests. Infection diagnostics and cancer diagnostics are two major segments of the market, accounting for significant revenue shares. Infection diagnostics, driven by the growing prevalence of infectious diseases, is projected to grow at a CAGR of 8% from 2021 to 2026. On the other hand, cancer diagnostics, with its high clinical utility and significant patient impact, is expected to grow at a CAGR of 6% during the same period. Molecular assays, endocrine diagnostics, neurological diagnostics, and genetic testing are other key segments of the IVD market, each with unique challenges and opportunities.

- Performance characteristics, such as analytical sensitivity and clinical utility, are critical factors in the development and adoption of new diagnostic tests. Quality assurance protocols and patient data privacy are essential considerations in the IVD market, ensuring accurate results and protecting sensitive patient information. Regulatory approval and result interpretation are also crucial aspects of the diagnostic test development process. Cardiovascular diagnostics, drug development testing, and serological tests are additional segments of the IVD market, each contributing to the overall growth and evolution of the industry. Disease biomarkers play a significant role in the development of new diagnostic tests, enabling earlier and more accurate detection and diagnosis.

We can help! Our analysts can customize this in-vitro diagnostics (IVD) market research report to meet your requirements.

RIA -

RIA -