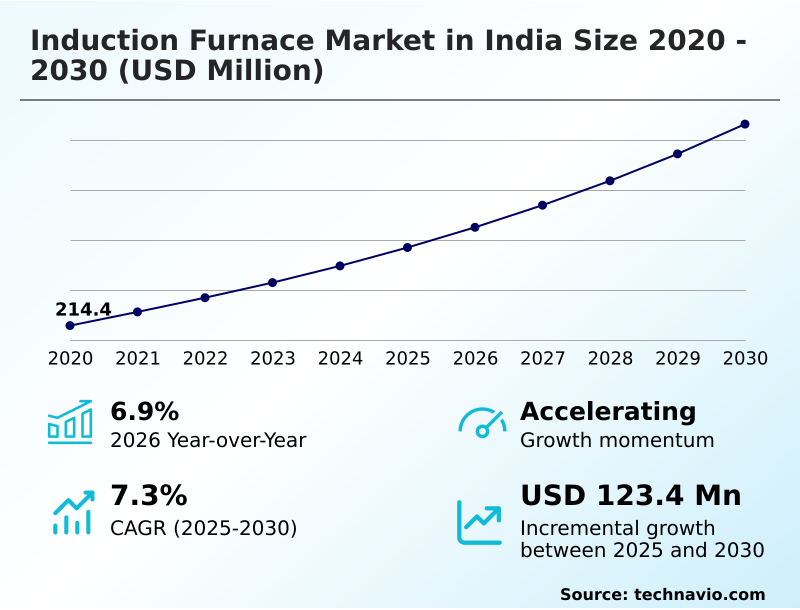

India Induction Furnace Market Size 2026-2030

The india induction furnace market size is valued to increase by USD 123.4 million, at a CAGR of 7.3% from 2025 to 2030. Expansion of secondary steelmaking and infrastructure development will drive the india induction furnace market.

Major Market Trends & Insights

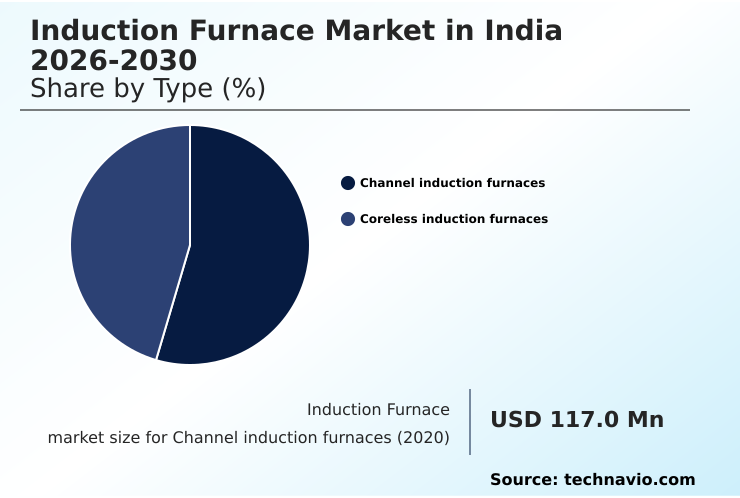

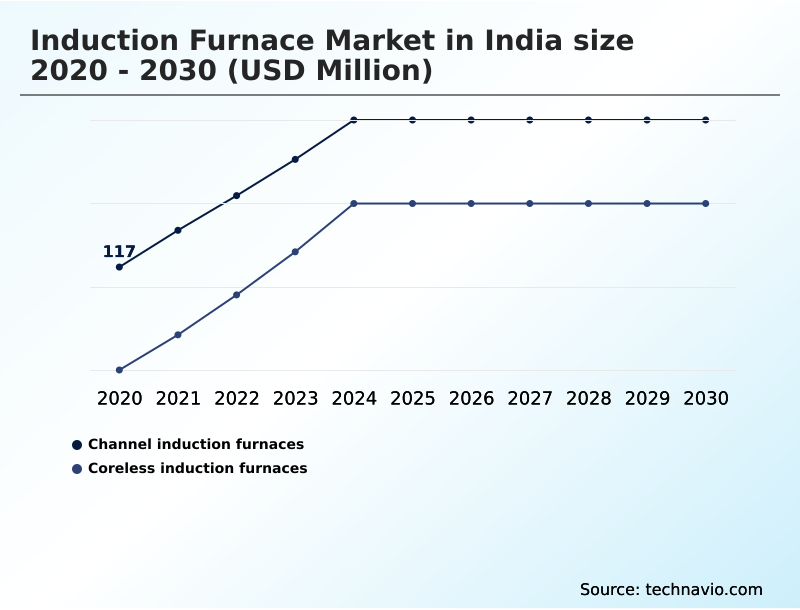

- By Type - Channel induction furnaces segment was valued at USD 145 million in 2024

- By End-user - Steel industry segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 201.5 million

- Market Future Opportunities: USD 123.4 million

- CAGR from 2025 to 2030 : 7.3%

Market Summary

- The induction furnace market in India is central to the nation's industrial strategy, underpinning the production of steel, iron, and non-ferrous alloys. This technology, which uses electromagnetic induction for heating and melting, is favored for its efficiency, precise temperature control, and lower emissions compared to conventional methods.

- The market's momentum is tied to infrastructure growth and the automotive sector's demand for high-quality materials. For instance, a foundry supplying automotive components leverages induction melting to produce complex castings that meet strict metallurgical purity and tolerance standards, ensuring product reliability and performance. This capability is crucial for competing in a landscape where quality is non-negotiable.

- As manufacturers increasingly prioritize energy efficiency and sustainability, the adoption of advanced induction systems integrated with automation and digital monitoring is becoming a key differentiator. However, the high initial capital investment and dependency on a stable power supply and consistent raw material quality remain significant operational considerations for businesses across the sector.

What will be the Size of the India Induction Furnace Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the India Induction Furnace Market Segmented?

The india induction furnace industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Channel induction furnaces

- Coreless induction furnaces

- End-user

- Steel industry

- Copper industry

- Aluminum industry

- Zinc industry

- Capacity

- More than 100 ton

- Upto 1 ton

- Geography

- APAC

- India

- APAC

By Type Insights

The channel induction furnaces segment is estimated to witness significant growth during the forecast period.

The channel induction furnace segment is crucial for large-scale casting and holding, particularly in secondary metallurgical operations that support industrial decarbonization. These systems excel at maintaining large volumes of molten metal at precise temperatures, a key function for continuous casting.

This precise metallurgical control, enhanced by digital temperature feedback loops, minimizes thermal variations and prevents melt batch loss. Integrating automated tilt pouring further refines the process, reducing manual intervention.

The technology is indispensable for high-volume foundries producing inputs for applications like billet heating furnaces, ladle refining furnaces, and various heat treatment furnace processes, where maintaining consistent quality over extended periods is critical for operational success.

The Channel induction furnaces segment was valued at USD 145 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic adoption of advanced technologies is reshaping the operational framework of the induction furnace market in India. A key focus is on induction furnace refractory lining thickness monitoring to preempt failures and extend equipment life, which has been shown to improve operational uptime by more than 15% compared to reactive maintenance schedules.

- The application of AI for induction furnace energy optimization is critical, with intelligent algorithms adjusting power cycles in real-time. This is often paired with a digital twin for induction furnace simulation, allowing operators to model melt cycles and train staff in a virtual environment.

- For sustainability, the induction furnace integration with renewable energy is becoming a priority for achieving green steel objectives. In terms of process control, medium-frequency coreless induction furnace stirring techniques are refined to enhance melt homogeneity, complemented by smart melt cycle evaluation and monitoring. Predictive temperature monitoring for induction furnace systems prevents overheating and ensures metallurgical consistency.

- The market also sees growth in specialized applications, including induction heating for forging applications and vacuum induction melting for specialty alloys. From large-scale secondary steel production to the induction melting furnace for aluminum recycling and coreless furnace for small-scale casting, the emphasis is on efficiency and quality.

- The use of an automated charging system for induction furnace operations and mitigating induction furnace power supply harmonic distortion are further areas of innovation defining the competitive landscape.

What are the key market drivers leading to the rise in the adoption of India Induction Furnace Industry?

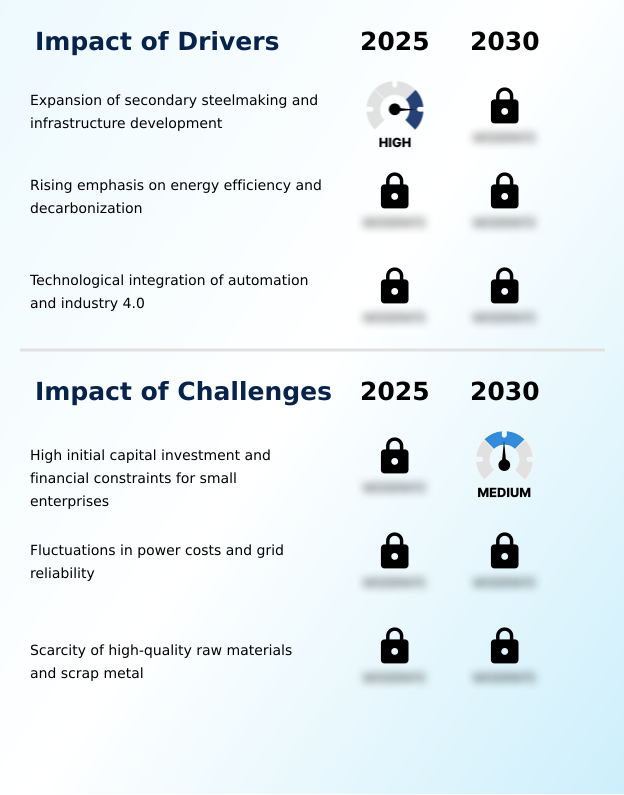

- The expansion of secondary steelmaking, driven by significant infrastructure development, is a primary factor fueling market growth.

- The market's growth is primarily propelled by the expansion of secondary steelmaking and the national push toward sustainability.

- The adoption of green steelmaking practices is a major driver, with induction furnaces being a core technology due to their compatibility with captive renewable energy parks and green energy corridors.

- This shift is also a strategic response to potential carbon border adjustment mechanisms in export markets. Advanced solid-state power electronics have significantly improved furnace efficiency, with modern systems achieving electrical efficiency levels exceeding 90%.

- Furthermore, the integration of AI-enabled diagnostics for induction melting and innovations in forging induction systems and continuous casting machines are enhancing productivity.

- These technological advancements support the national goal of achieving a three hundred million tonne crude steel capacity while aligning with industrial decarbonization targets.

What are the market trends shaping the India Induction Furnace Industry?

- The adoption of digital twin technology and real-time process simulation is an emerging trend. This allows for the creation of virtual replicas of physical assets to optimize performance and predict maintenance needs.

- Key market trends are centered on digitalization and advanced process control. The adoption of digital twin technology is a significant development, allowing for real-time process simulation that can predict thermal stress on refractory linings and optimize melting scenarios. This innovation has been shown to reduce alloy homogenization times by up to 10%.

- Paired with a cloud-based analytical platform, operators gain insights for autonomous process optimization and improved energy optimization. The integration of an FPGA based control architecture is enhancing the precision of these systems, particularly in advanced applications like the plasma induction furnace, which is crucial for high-purity metal production.

- This move toward data-centric manufacturing improves operational efficiency and allows foundries to achieve a higher degree of precision in metallurgical outputs, enhancing process consistency by over 15%.

What challenges does the India Induction Furnace Industry face during its growth?

- The substantial initial capital investment required for advanced systems presents a significant financial challenge, particularly for small and medium-sized enterprises.

- Persistent challenges in the market revolve around high upfront costs and operational variables. The initial investment in high-frequency induction units, advanced pollution control equipment, and specialized copper induction coils remains a significant barrier for many smaller enterprises, with equipment costs recently rising by approximately 15% due to supply chain pressures.

- Furthermore, the reliance on a consistent supply of quality raw materials, such as ferrous and non-ferrous scrap, is a critical issue. Inconsistent quality can decrease final product yield by up to 5%. This has spurred the adoption of AI-driven power demand forecasting and scrap quality categorization to optimize input and energy use.

- Proactive energy demand forecasting and induction coil fault detection are becoming essential to manage fluctuating power costs and prevent costly failures.

Exclusive Technavio Analysis on Customer Landscape

The india induction furnace market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india induction furnace market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Induction Furnace Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india induction furnace market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Electro Power Enterprise - Analysis reveals a focus on advanced induction melting, heating, and metal processing systems designed for diverse industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Electro Power Enterprise

- Eltech Electrodesigns

- Foster Induction Heating

- H K Malvi Industries

- Heatcon Sensors Pvt. Ltd.

- Indotherm Furnace Pvt. Ltd.

- Induction Furnace India

- Inductotherm Group

- Jyoti CNC Automation Ltd.

- Magnalenz

- Megatherm Electronics Pvt. Ltd.

- Microtech Inductions Pvt. Ltd.

- Naksh Induction

- Nutrotherm Induction Pvt Ltd

- Orbit Induction

- Oritech Engineering

- Plasma Induction India Pvt. Ltd

- Priyanka Induction Supermelt

- Shapet Induction Company

- Srishtech India Pvt Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India induction furnace market

- In September 2025, Electrotherm announced that a 60 ton 32 MW induction melting furnace project is currently under execution, integrating advanced digital controls and AI-enabled diagnostics.

- In February 2026, the Ministry of Steel inaugurated a specialized greenfield cluster in eastern India, incentivizing the use of high-capacity induction melting units integrated with renewable energy grids.

- In March 2026, the Indian Ministry of Micro, Small, and Medium Enterprises initiated a review of credit guarantee schemes to address the high costs of industrial machinery, including high-frequency induction units.

- In April 2026, Megatherm Induction Limited initiated the construction of its fourth production facility to scale its transformer and large-scale induction furnace manufacturing capacity to meet growing global orders.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Induction Furnace Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 183 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.3% |

| Market growth 2026-2030 | USD 123.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The induction furnace market in India is driven by the strategic imperative of industrial decarbonization and the expansion of secondary steelmaking. Widespread adoption is seen in systems like the coreless induction furnace and the channel induction furnace, which are fundamental to producing high-purity metal production.

- The technological landscape is evolving with innovations in solid-state power electronics, which enhance efficiency to levels exceeding 90%, and the integration of digital twin technology for real-time process simulation. Boardroom decisions are increasingly influenced by the push toward green steelmaking, necessitating investments in systems compatible with renewable energy.

- This involves not only the furnace itself, from billet heating furnace to ladle refining furnace models, but also ancillary components like copper induction coils, robust refractory linings, and advanced pollution control equipment. The use of an FPGA based control architecture and automated charging systems is becoming standard.

- For specialized needs, technologies such as vacuum induction melting, plasma induction furnace systems, and those for specific forging induction systems or heat treatment furnace applications are gaining traction. Managing the supply chain for raw materials like ferrous and non-ferrous scrap, heavy melting scrap, and sponge iron remains a critical operational focus.

What are the Key Data Covered in this India Induction Furnace Market Research and Growth Report?

-

What is the expected growth of the India Induction Furnace Market between 2026 and 2030?

-

USD 123.4 million, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Channel induction furnaces, and Coreless induction furnaces), End-user (Steel industry, Copper industry, Aluminum industry, and Zinc industry), Capacity (More than 100 ton, and Upto 1 ton) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Expansion of secondary steelmaking and infrastructure development, High initial capital investment and financial constraints for small enterprises

-

-

Who are the major players in the India Induction Furnace Market?

-

Electro Power Enterprise, Eltech Electrodesigns, Foster Induction Heating, H K Malvi Industries, Heatcon Sensors Pvt. Ltd., Indotherm Furnace Pvt. Ltd., Induction Furnace India, Inductotherm Group, Jyoti CNC Automation Ltd., Magnalenz, Megatherm Electronics Pvt. Ltd., Microtech Inductions Pvt. Ltd., Naksh Induction, Nutrotherm Induction Pvt Ltd, Orbit Induction, Oritech Engineering, Plasma Induction India Pvt. Ltd, Priyanka Induction Supermelt, Shapet Induction Company and Srishtech India Pvt Ltd

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of operational excellence through advanced technology. The integration of AI-driven power demand forecasting allows operators to synchronize melting cycles with grid loads, mitigating the impact of peak-hour tariffs. Predictive maintenance and AI-enabled diagnostics for induction melting are becoming standard, reducing unplanned downtime.

- Innovations in digital power management units, coupled with harmonic filters and voltage-boosted power supplies, enhance grid compatibility and deliver electrical efficiency levels exceeding 90%. Moreover, the adoption of micro-processor-controlled induction systems allows for the implementation of digital temperature feedback loops, improving process consistency by over 15%.

- These intelligent systems support autonomous process optimization, transforming furnaces into self-regulating assets that consistently deliver high-purity metal production.

We can help! Our analysts can customize this india induction furnace market research report to meet your requirements.

RIA -

RIA -