Intravenous (IV) Therapy And Vein Access Market Size 2024-2028

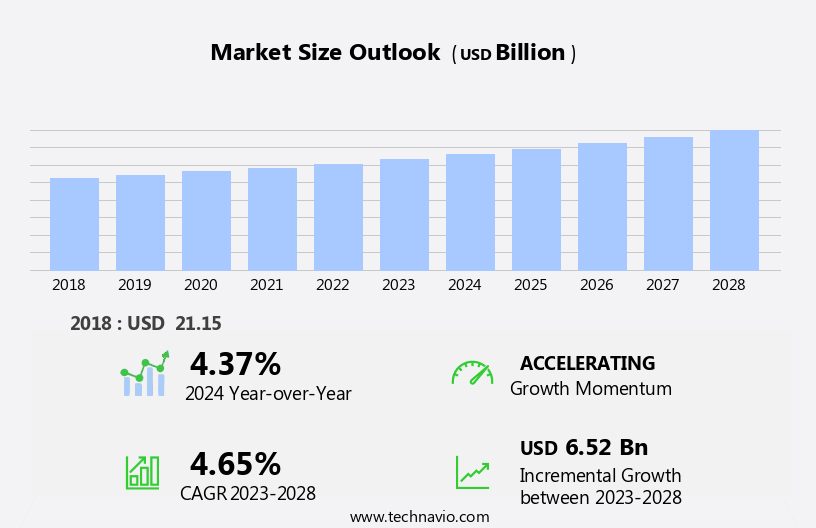

The intravenous (iv) therapy and vein access market size is forecast to increase by USD 6.52 billion at a CAGR of 4.65% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing prevalence of chronic diseases and the resulting demand for efficient and effective IV solutions. Chronic conditions, such as cancer, diabetes, and cardiovascular diseases, require frequent IV therapy for medication administration and nutritional support. This trend is particularly prominent in the US, where the Centers for Disease Control and Prevention (CDC) reports that chronic diseases account for approximately 7 out of 10 deaths and 86% of all healthcare spending. Moreover, technological advancements in IV solutions are driving innovation and improving patient outcomes. For instance, the development of smart infusion pumps, which allow for precise dosing and real-time monitoring, and the use of ultrasound technology for vein visualization and cannulation, are transforming the IV therapy landscape.

- However, the high cost of IV solutions remains a significant challenge for both healthcare providers and patients. The high cost of IV drugs, coupled with the need for specialized equipment and trained personnel, can limit access to IV therapy and increase healthcare costs. Companies seeking to capitalize on market opportunities and navigate these challenges effectively must focus on cost reduction strategies, such as the development of generic IV drugs and the implementation of cost-effective technologies, while ensuring the highest standards of patient safety and clinical efficacy.

What will be the Size of the Intravenous (IV) Therapy And Vein Access Market during the forecast period?

- The market in the US is experiencing significant growth due to the increasing number of ries and the rising prevalence of chronic diseases. IV therapy plays a crucial role in administering essential nutrients, medications, and fluids for various medical procedures, critical care therapies, and nourishment for patients with digestive system disorders. The market's expansion is driven by the growing healthcare expenditure, an aging geriatric population, and the increasing number of trauma cases. IV therapy involves the use of intravenous lines, implantable ports, and vein access devices for medication administration and fluid replenishment. These devices are made from materials such as polyvinyl chloride (PVC) and are free from harmful substances like diethylhexyl phthalate (DEHP).

- The market's size is substantial, with a steady direction, as IV therapy is a vital component of healthcare delivery, particularly in critical care settings. IV therapy is used to administer a range of medications, including artesunate injections, and is essential for the administration of IV drugs and fluids in emergency situations, such as road accidents. The use of IV therapy is not limited to hospitals but is also prevalent in home healthcare settings, further expanding the market's reach. The market's future looks promising, with ongoing research and development in vein access technology and the introduction of innovative products, such as the Minnesota-based startup's NXGENPORT, enhancing the overall efficiency and patient experience.

How is this Intravenous (IV) Therapy And Vein Access Industry segmented?

The intravenous (iv) therapy and vein access industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Clinics

- Ambulatory surgical centers

- Application

- Medication administration

- Blood-based products

- Nutrition and buffer solution

- Volume expander

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Asia

- Japan

- Rest of World (ROW)

- North America

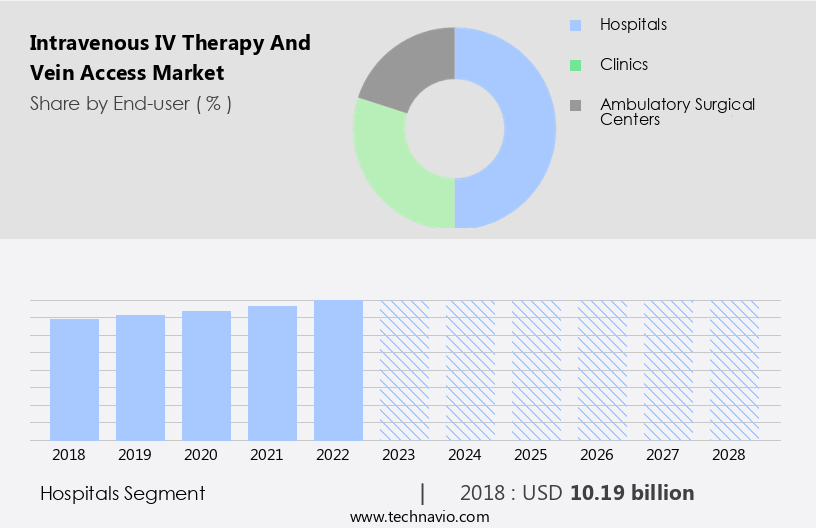

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The IV therapy and vein access market encompasses a range of auxiliary accessories and devices used in the administration of IV medications and fluid replenishment. Hospital pharmacies play a pivotal role in supplying these systems, ensuring their availability for patients in hospital settings. Products in this segment cater to diverse hospital requirements, including infusion pumps, genetic testing for personalized medication administration, and novel catheter designs. Infusion technology advances continue with real-time monitoring capabilities to mitigate complications such as infections and phlebitis. Biodegradable materials and closed-loop medicine preparation systems are gaining traction due to their safety and environmental benefits.

In addition, wearable alternatives like implantable ports and microneedle patches offer convenience for chronic disease management and home healthcare settings. IV therapy is essential for various medical procedures, including diabetes care, critical care therapies, cancer treatments, and trauma cases. The market is driven by technological progress and increasing healthcare expenditure, particularly in ambulatory surgical centers and clinics. Infusion pumps, vein access devices, and IV catheters are integral components of these applications. Innovations like smart catheters, AI-assisted medication administration, and ultrasound guiding systems enhance the efficiency and accuracy of IV therapy. However, concerns regarding materials like polyvinyl chloride (PVC) and diethylhexyl phthalate (DEHP) persist, necessitating the development of safer alternatives.

The market for IV therapy and vein access systems is diverse and dynamic, catering to the needs of hospitals, clinics, and home healthcare settings. The market's growth is fueled by the increasing prevalence of chronic diseases, the aging population, and the ongoing advancements in infusion technology.

Get a glance at the market report of share of various segments Request Free Sample

The Hospitals segment was valued at USD 10.19 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

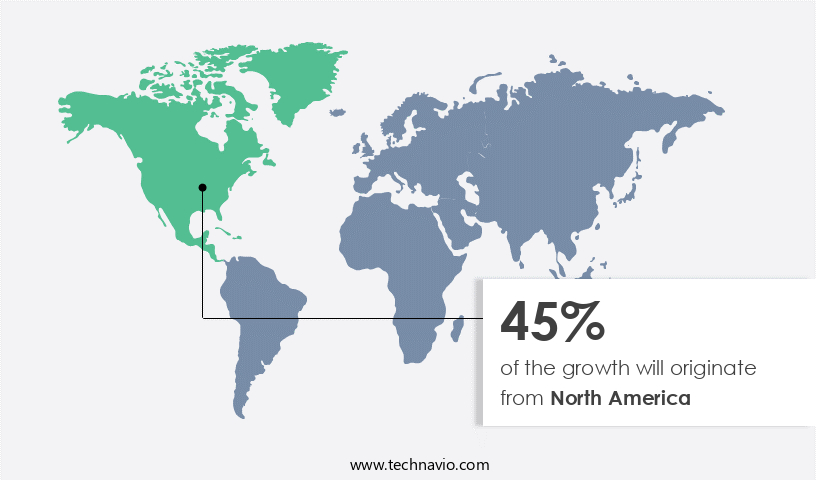

North America is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The IV therapy and vein access market in North America is experiencing substantial growth due to several factors. The rising healthcare expenditure, growing prevalence of chronic diseases, and increasing aged population are significant drivers. Major market players are focusing on emerging markets and expanding healthcare facilities and infrastructure in the region, including Mayo Clinic Hospital, ProMedica Toledo (Ohio), and Brigham and Women's Hospital (Boston). The adoption of advanced infusion technology, such as infusion pumps, smart catheters, and real-time monitoring capabilities, is also contributing to market growth. Additionally, the increasing use of genetic testing and pharmacogenomics in IV drug regimens is driving innovation in the market.

Auxiliary accessories, such as tip locating systems and microneedle patches, are gaining popularity for their convenience and effectiveness in medication administration. The market is further by the rising number of medical procedures, including ries and critical care therapies, requiring IV fluid replenishment and nutrient delivery. The use of biodegradable materials and closed-loop medicine preparation systems is also gaining traction due to their environmental benefits and potential for reducing infections, such as phlebitis. The market for vein access devices, including IV catheters, implantable ports, and arterial catheters, is expected to continue growing due to their essential role in various medical applications, including diabetes care, cancer treatment, and trauma cases.

The market is also witnessing technological progress in the form of AI and machine learning applications, vein imaging methods, and wearable alternatives to IV poles. The market for IV therapy and vein access devices is expected to continue its growth trajectory in the coming years, driven by these and other factors.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Intravenous (IV) Therapy And Vein Access Industry?

- Increasing prevalence of chronic diseases is the key driver of the market.

- The IV therapy and vein access market is experiencing significant growth due to the rising prevalence of chronic diseases, including cancer, diabetes, and cardiovascular conditions. These therapies are essential for treating various medical conditions and delivering fluids, electrolytes, and medications to patients. According to the International Diabetes Federation (IDF), the global diabetes population is projected to reach 700 million by 2045. Diabetes patients require IV therapy and vein access for glucose management, making the increasing prevalence of diabetes a key driver for market growth during the forecast period.

- Chronic diseases necessitate long-term care and frequent hospitalizations, leading to an increased demand for IV therapy and vein access solutions. Additionally, advancements in technology have led to the development of minimally invasive and more efficient vein access devices, further fueling market growth.

What are the market trends shaping the Intravenous (IV) Therapy And Vein Access Industry?

- Technological advancements in IV solutions is the upcoming market trend.

- IV therapy and vein access systems play a vital role in modern medical practice by enabling the direct administration of medications, fluids, and nutrients into the bloodstream. Recent technological advancements have significantly enhanced the efficiency, safety, and efficacy of these systems. One such innovation is the development of smart IV pumps. These devices are designed to improve patient safety and minimize medication errors by automatically adjusting infusion rates based on a patient's weight, age, and medical condition. This technological advancement is a significant driver for the global IV therapy and vein access market.

- Smart IV pumps offer numerous benefits, including improved patient outcomes, reduced healthcare costs, and enhanced clinical workflows. As medical facilities continue to prioritize patient safety and efficiency, the adoption of smart IV pumps and other advanced vein access systems is expected to increase.

What challenges does the Intravenous (IV) Therapy And Vein Access Industry face during its growth?

- High cost of IV solutions is a key challenge affecting the industry growth.

- The IV therapy and vein access market has experienced a consistent rise in costs, a trend that is projected to persist throughout the forecast period. This escalation in costs is attributed to several factors, including the high expense of raw materials, intricate manufacturing processes, and transportation costs. The substantial cost of IV therapy and vein access systems poses challenges for the global market. Primarily, it results in a decline in demand due to the financial constraints of healthcare providers and patients. This challenge is particularly significant in developing countries, where access to affordable healthcare is already limited. Despite these hurdles, the market continues to evolve, driven by advancements in technology and the growing need for efficient and effective healthcare solutions.

Exclusive Customer Landscape

The intravenous (iv) therapy and vein access market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the intravenous (iv) therapy and vein access market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, intravenous (iv) therapy and vein access market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AngioDynamics Inc. - The company specializes in providing advanced intravenous (IV) therapy and vein access solutions, including the LifePort lipid-compatible infusion set. This set ensures optimal patient safety and efficacy through its innovative design, enabling healthcare professionals to administer medications and nutrients efficiently and effectively. By utilizing cutting-edge technology and adhering to stringent quality standards, the company remains at the forefront of the IV therapy industry, delivering superior outcomes for patients worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AngioDynamics Inc.

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Co.

- Cardinal Health Inc.

- Fresenius SE and Co. KGaA

- ICU Medical Inc.

- IRadimed Corp.

- Medtronic Plc

- Poly Medicure Ltd.

- Smith and Nephew plc

- Tekni Plex Inc.

- Teleflex Inc.

- Terumo Corp.

- Vygon SAS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompass a wide range of auxiliary accessories and devices that facilitate the administration of medications and fluids directly into a patient's vein. These devices play a crucial role in various medical procedures, critical care therapies, and healthcare settings, including hospitals, clinics, ambulatory surgical centers, and home healthcare settings. Infusion pumps and IV catheters are two essential components of IV therapy. Infusion pumps regulate the flow rate and pressure of infused fluids, ensuring precise medication administration. IV catheters, on the other hand, provide access to the patient's venous system, allowing for the infusion of drugs, fluids, blood-based products, and nutrients.

The demand for advanced vein access devices continues to grow due to technological progress and the increasing prevalence of chronic diseases, geriatric population, and critical care therapies. Biodegradable materials, smart catheters, and real-time monitoring capabilities are some of the innovative features that enhance the functionality and safety of IV catheters. Infection prevention is a significant concern in IV therapy, as catheter-related bloodstream infections can lead to severe complications. Vein imaging methods, such as ultrasound guiding, help ensure proper catheter placement and reduce the risk of complications. IV therapy is used in various medical applications, including medication administration for trauma cases, diabetes management, cancer treatment, and circulatory support.

In some cases, implantable ports and infusion pumps are used for long-term therapy, such as in chronic diseases and home healthcare settings. The use of IV therapy extends beyond hospitals and clinics. Ambulatory care facilities and home healthcare settings also rely on IV therapy for the administration of medications, fluids, and nutrients. In these settings, wearable alternatives, such as microneedle patches and implanted ports, offer convenience and mobility. Healthcare professionals in various specialties, including emergency medicine, oncology, and critical care, rely on IV therapy and vein access devices to provide optimal patient care. The integration of AI and machine learning in IV therapy has the potential to improve medication administration, reduce errors, and enhance patient outcomes.

The use of IV therapy is not limited to pharmaceuticals. It is also used for fluid replenishment, blood transfusions, and the administration of nutrients and other nourishing substances. The market for IV therapy and vein access devices is expected to grow significantly due to the increasing demand for advanced medical technologies and the expanding range of applications. The cost of IV therapy and vein access devices can be a significant concern for healthcare insurers and providers. Closed-loop medicine preparation and the use of cost-effective materials, such as polyvinyl chloride (PVC) and biodegradable materials, can help reduce the overall cost of IV therapy while maintaining safety and efficacy.

In summary, the IV therapy and vein access market encompasses a diverse range of devices and technologies that play a crucial role in various medical applications. The demand for advanced, safe, and cost-effective IV therapy solutions is expected to grow due to the increasing prevalence of chronic diseases, technological progress, and the expanding range of applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.65% |

|

Market growth 2024-2028 |

USD 6.52 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.37 |

|

Key countries |

US, Germany, Japan, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Intravenous (IV) Therapy And Vein Access Market Research and Growth Report?

- CAGR of the Intravenous (IV) Therapy And Vein Access industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the intravenous (iv) therapy and vein access market growth of industry companies

We can help! Our analysts can customize this intravenous (iv) therapy and vein access market research report to meet your requirements.

RIA -

RIA -