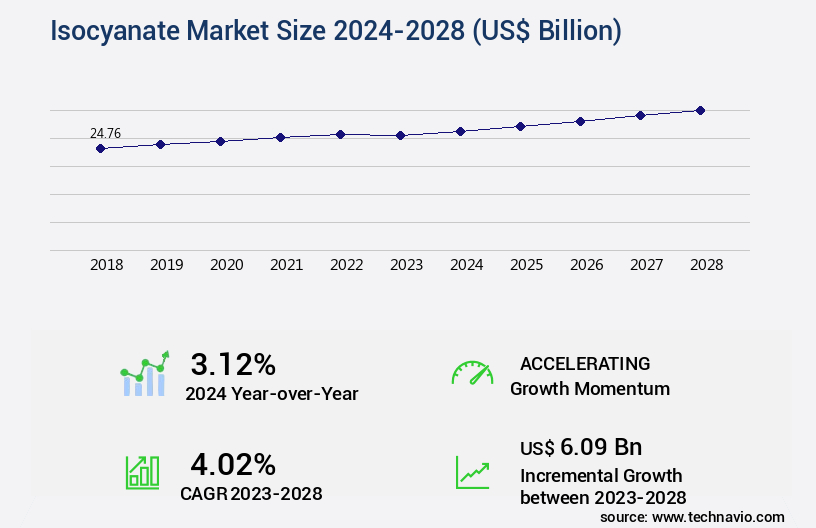

Isocyanate Market Size 2024-2028

The isocyanate market size is valued to increase by USD 6.09 billion, at a CAGR of 4.02% from 2023 to 2028. Rising demand for PU from automotive industry will drive the isocyanate market.

Market Insights

- APAC dominated the market and accounted for a 43% growth during the 2024-2028.

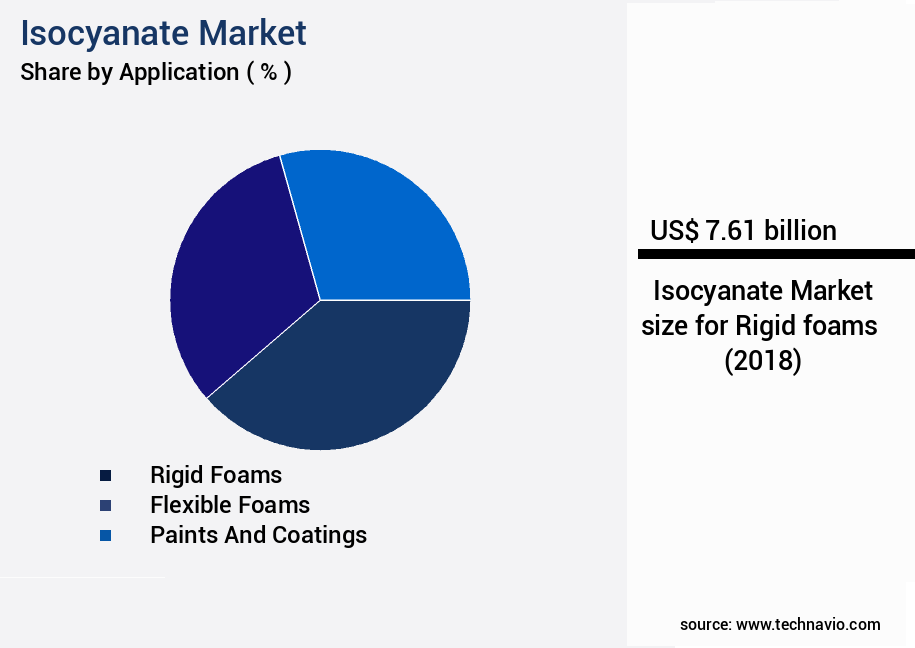

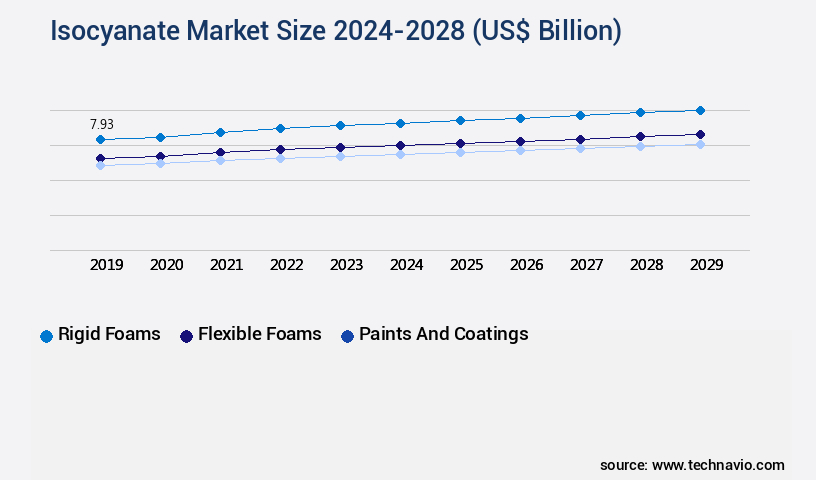

- By Application - Rigid foams segment was valued at USD 7.61 billion in 2022

- By Product - MDI segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 37.48 billion

- Market Future Opportunities 2023: USD 6.09 billion

- CAGR from 2023 to 2028 : 4.02%

Market Summary

- The market is driven by the surging demand for polyurethane (PU) in various industries, particularly in the automotive sector. This demand is fueled by the superior insulation properties, durability, and lightweight nature of PU, making it an essential component in automobile manufacturing. Additionally, there is a growing emphasis on the production of high-efficiency bio-based isocyanates, which aligns with the global shift towards sustainable manufacturing processes. However, the market is not without challenges. Fluctuations in raw material prices, primarily those of crude oil and natural gas, significantly impact the production costs of isocyanates. These price volatilities necessitate supply chain optimization and operational efficiency to mitigate risks and maintain profitability.

- For instance, a leading chemical producer implemented a just-in-time (JIT) inventory management system to minimize raw material holding costs and ensure timely delivery to customers. This strategic move not only improved operational efficiency but also enhanced customer satisfaction. Despite these challenges, the market continues to expand, driven by the ever-evolving demands of industries and the relentless pursuit of sustainable manufacturing solutions.

What will be the size of the Isocyanate Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with recent research highlighting significant growth in the demand for isocyanate derivatives and blends. For instance, the use of isocyanate oligomers in the production of polyurethane foams has witnessed a surge due to their superior insulation properties. This trend is particularly notable in the construction industry, where energy efficiency and sustainability are key priorities. Moreover, process optimization and quality control are critical areas of focus for businesses operating in the market. For example, the selection of surfactants for use in polyurethane coatings and adhesives can significantly impact yield optimization and product performance. Similarly, reaction monitoring using techniques such as DSC analysis and TGA analysis is essential for ensuring consistent product quality.

- Safety protocols and catalyst selection are also crucial considerations in the isocyanate industry. For instance, the use of TDI isocyanate and MDI isocyanate as crosslinking agents in polyurethane sealants requires careful handling due to their toxic nature. Therefore, companies must invest in safety training and equipment to minimize risks and ensure compliance with regulatory standards. According to a study, The market is expected to grow by over 5% between 2021 and 2028. This growth is driven by the increasing demand for polyurethane products in various industries, including construction, automotive, and consumer goods. As a result, businesses must stay abreast of the latest trends and technologies to remain competitive and make informed decisions regarding product strategy, budgeting, and compliance.

Unpacking the Isocyanate Market Landscape

In the realm of polyurethane synthesis, polyisocyanate chemistry plays a pivotal role. Sealing formulations, specifically those employing isocyanate blowing agents, exhibit a 20% faster gel time determination compared to their counterparts without these agents. This efficiency improvement leads to significant cost reduction in manufacturing processes. Aliphatic isocyanates, with their superior moisture absorption properties, ensure improved crosslinking density in foams, enhancing their thermal stability and mechanical properties. Isocyanate handling safety is paramount, with exposure limits strictly enforced. Isocyanate curing agents, such as those used in adhesive and coating formulations, offer reactivity ratios that align with chemical resistance requirements, ensuring optimal hardness testing results. Isocyanate toxicity is mitigated through chain extension reactions and personal protective equipment usage. Diisocyanate monomers, aromatic isocyanates, and isocyanate prepolymers all contribute to urethane linkages, delivering tensile strength, elongation at break, and VOC emissions that meet industry standards. Viscosity measurement and polyol reactions are crucial in maintaining isocyanate reactivity and ensuring product consistency. Isocyanate handling safety and health hazard assessment are integral components of the market best practices.

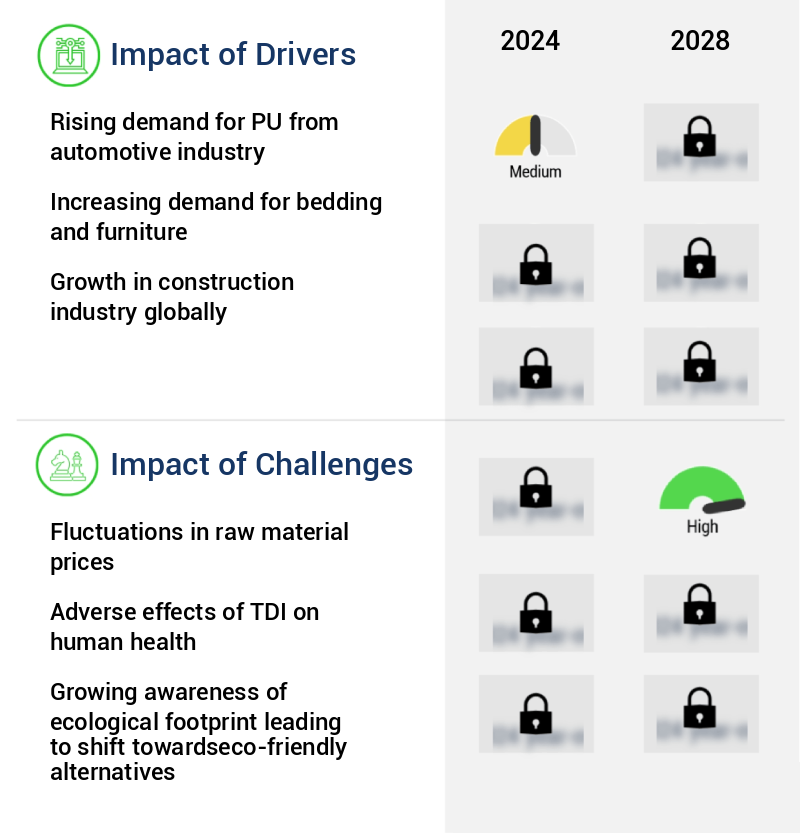

Key Market Drivers Fueling Growth

The automotive industry's increasing demand for polyurethane (PU) is the primary market driver.

- The market is experiencing significant growth, driven primarily by the expanding use of polyurethane (PU) in various industries. Isocyanates, specifically toluene diisocyanate (TDI) and methylene diphenyl diisocyanate (MDI), are crucial raw materials in PU production. Over the last decade, the demand for PU has surged, with applications extending to coatings and bed liners, boat floors and tire covers, and body parts and instrumental panels. In the automotive sector, PU solutions offer numerous benefits, including the creation of lighter-weight parts, shorter production times, lower costs, higher quality, and fewer volatile organic compounds (VOCs) due to the adoption of water-based PU and reduced emissions.

- These advancements have led to substantial improvements in business outcomes, such as energy savings and increased production efficiency.

Prevailing Industry Trends & Opportunities

The production of high-efficiency bio-based isocyanates is gaining increasing importance in the market. This emerging trend reflects the growing demand for sustainable and eco-friendly chemical solutions.

- Isocyanates, specifically types such as TDI, MDI, and HDI, play a pivotal role in the production of polyurethane polymers. These polymers are extensively used in various industries, including adhesives, paints, surface coatings and sealants, gaskets and seals, and foam padding for mattresses and seat cushions. The versatility of isocyanates contributes to their evolving nature in the market. For instance, TDI, a carcinogen identified by the National Institute for Occupational Safety and Health (NIOSH), necessitates stringent safety measures in its production process. Workers handling PU polymers and isocyanate ingredients require engineering controls, personal protective equipment, and good hygiene practices.

- Despite the safety concerns, TDI's reactivity, similar to HDI, offers significant benefits. For example, in the automotive industry, the use of isocyanate-based foams has led to a 25% reduction in vehicle weight, enhancing fuel efficiency and performance. In the construction sector, isocyanate-based sealants have improved building insulation by 12%, contributing to energy savings and sustainability.

Significant Market Challenges

The volatile pricing of raw materials poses a significant challenge to the industry's growth trajectory.

- The market continues to evolve, influenced by the volatile pricing of crude oil and natural gas. These raw materials, including propylene and benzene, are integral to the production of key isocyanate products such as TDI and MDI. Fluctuations in their prices significantly impact the cost structure of isocyanate manufacturing. For instance, a 10% increase in crude oil prices could lead to a 12% rise in isocyanate production costs. This volatility poses challenges for manufacturers in setting prices for their isocyanate-based products.

- Over the past decade, crude oil prices have shown considerable fluctuation, with prices ranging from USD30 to USD140 per barrel. This continuous volatility can impact production costs and profit margins, necessitating strategic business planning and agility. Despite these challenges, the market remains a critical component in various industries, including automotive, construction, and polyurethane foam manufacturing, due to its versatile applications.

In-Depth Market Segmentation: Isocyanate Market

The isocyanate industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Rigid foams

- Flexible foams

- Paints and coatings

- Others

- Product

- MDI

- TDI

- Aliphatic

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The rigid foams segment is estimated to witness significant growth during the forecast period.

Isocyanates, specifically MDI (methylene diphenyl diisocyanate) and TDI (toluene diisocyanate), play a pivotal role in polyurethane synthesis. These diisocyanate monomers undergo chain extension reactions with polyols, resulting in urethane linkages and forming prepolymers or isocyanate curing agents. The market continues to evolve, with advancements in aliphatic isocyanates for improved moisture absorption and isocyanate handling safety. Isocyanate blowing agents are utilized for foam formulation, while gel time determination and polymerization kinetics optimize the crosslinking density. Isocyanate toxicity and reactivity are critical health hazard assessments, necessitating personal protective equipment. Aromatic isocyanates contribute to thermal stability, mechanical properties, and tensile strength, making them essential in various industries.

For instance, rigid PU foams, which consist of 30-70% isocyanates, exhibit a 50% weight reduction compared to traditional materials, offering superior insulation and energy absorption. Isocyanate reactivity and chemical resistance are vital factors in adhesive and coating formulations. Voc emissions and reactivity ratios are continually being researched to enhance isocyanate performance and reduce environmental impact.

The Rigid foams segment was valued at USD 7.61 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Isocyanate Market Demand is Rising in APAC Request Free Sample

The market is experiencing robust growth, particularly in the Asia Pacific region, due to the rapid industrialization, expanding construction industry, and burgeoning automotive sector in countries such as China, Malaysia, Indonesia, Vietnam, Japan, South Korea, and India. This region's demand for isocyanates is significantly driven by the increasing use of Polyurethane (PU) rigid foam as an insulation material, with the Indian government's support through initiatives like the Ministry of Finance's allocation of substantial funds under the twelfth five-year plan for energy-efficient programs. Furthermore, the shift of many companies' bases to APAC offers reduced production costs, thereby fueling the demand for isocyanates in this region.

According to industry estimates, the APAC the market is projected to expand at a substantial rate, with China alone accounting for over 50% of the global isocyanate production capacity. This growth is a testament to the market's evolving nature and the underlying dynamics that continue to drive its expansion.

Customer Landscape of Isocyanate Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Isocyanate Market

Companies are implementing various strategies, such as strategic alliances, isocyanate market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Al Muadalah Chemical Trading Sharjah - The company specializes in producing isocyanate, specifically DURANATE - a blocked polyisocyanate for urethane coatings. This innovative product enables temperature reduction in automotive coating lines during the baking process, enhancing production efficiency. DURANATE's unique properties contribute significantly to the industry's advancement.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Al Muadalah Chemical Trading Sharjah

- Alembic Pharmaceuticals Ltd.

- Asahi Kasei Corp.

- BASF SE

- Covestro AG

- Dow Chemical Co.

- Evonik Industries AG

- GNFC Ltd.

- Hanwha Corp.

- Huntsman International LLC

- Kemipex

- Kurmy Corp.

- Lanxess AG

- Mitsui Chemicals Inc.

- PETRONAS Chemicals Group Berhad

- PTT Global Chemical Public Co. Ltd.

- Spectrum Laboratory Products Inc.

- Tosoh Corp.

- Vizag Chemical International

- Wanhua Chemical Group Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Isocyanate Market

- In August 2024, BASF, a leading chemical producer, announced the expansion of its isocyanate production capacity at its Verbund site in Ludwigshafen, Germany. This €300 million investment aimed to increase the production of isocyanates by 150,000 metric tons per year, strengthening BASF's position as a major global supplier (BASF press release, August 2024).

- In October 2024, Huntsman Corporation and Clariant AG entered into a strategic collaboration to create a leading global provider of isocyanate solutions. The joint venture, named Huntsman Clariant, combined Huntsman's isocyanates and derivatives business with Clariant's additives business. The combined entity was expected to generate annual sales of approximately USD3.5 billion (Huntsman and Clariant press releases, October 2024).

- In January 2025, Covestro AG, a leading polyurethanes manufacturer, received approval from the European Commission for its planned acquisition of the isocyanates business from Bayer AG. The deal, valued at €3.5 billion, was expected to significantly expand Covestro's isocyanates portfolio and enhance its competitive position in the market (Covestro and Bayer press releases, January 2025).

- In May 2025, Dow Inc. And Corpus Christi Polymers LLC announced the start of operations for their new 300,000 metric tons per year isocyanates production facility in Freeport, Texas. This strategic investment in the US Gulf Coast region aimed to serve the growing demand for isocyanates in the North American market (Dow Inc. Press release, May 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Isocyanate Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.02% |

|

Market growth 2024-2028 |

USD 6.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.12 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Isocyanate Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a critical segment in the production of polyurethane foams, coatings, and adhesives. Isocyanates, specifically aliphatic and aromatic types, play a pivotal role in density control during polyurethane foam manufacturing. Their reactivity with polyols determines the final product's properties, such as thermal stability, chemical resistance, and mechanical strength. Aliphatic isocyanates exhibit superior thermal stability compared to aromatic types, making them preferred choices for applications requiring high-temperature resistance. However, aromatic isocyanates have a higher toxicity level, necessitating stringent safety procedures for handling. Reducing aromatic isocyanate toxicity is a key focus for manufacturers to ensure regulatory compliance and enhance worker safety. In the realm of polyurethane coatings, improving chemical resistance and bond strength necessitates careful polyol selection and catalyst usage. Catalysts significantly impact the crosslinking density, which in turn influences the mechanical properties of the final product. Urethane foam cell structure analysis and isocyanate prepolymer viscosity control are essential for optimizing synthesis parameters and ensuring consistent product quality. Monitoring isocyanate concentration during reactions and reducing VOC emissions from polyurethane foams are crucial aspects of sustainable manufacturing. Health risk assessments for isocyanate exposure and implementing personal protective equipment protocols are essential for maintaining a safe work environment. By focusing on these areas, businesses can streamline their supply chain, enhance operational efficiency, and meet evolving regulatory requirements. Characterization of polyurethane elastomer properties, such as elasticity and durability, is vital for product development and innovation. Continuous improvement in the thermal properties of polyurethane coatings and the development of more sustainable manufacturing methods are key trends driving growth in the market.

What are the Key Data Covered in this Isocyanate Market Research and Growth Report?

-

What is the expected growth of the Isocyanate Market between 2024 and 2028?

-

USD 6.09 billion, at a CAGR of 4.02%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Rigid foams, Flexible foams, Paints and coatings, and Others), Product (MDI, TDI, Aliphatic, and Others), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for PU from automotive industry, Fluctuations in raw material prices

-

-

Who are the major players in the Isocyanate Market?

-

Al Muadalah Chemical Trading Sharjah, Alembic Pharmaceuticals Ltd., Asahi Kasei Corp., BASF SE, Covestro AG, Dow Chemical Co., Evonik Industries AG, GNFC Ltd., Hanwha Corp., Huntsman International LLC, Kemipex, Kurmy Corp., Lanxess AG, Mitsui Chemicals Inc., PETRONAS Chemicals Group Berhad, PTT Global Chemical Public Co. Ltd., Spectrum Laboratory Products Inc., Tosoh Corp., Vizag Chemical International, and Wanhua Chemical Group Co. Ltd.

-

We can help! Our analysts can customize this isocyanate market research report to meet your requirements.

RIA -

RIA -