Land Based Smart Weapons Market Size 2024-2028

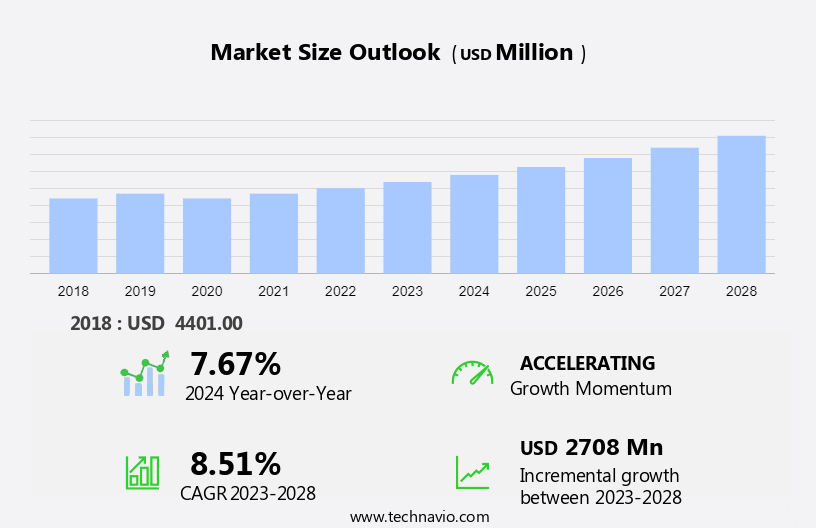

The land based smart weapons market size is forecast to increase by USD 2.71 billion, at a CAGR of 8.51% between 2023 and 2028.

- The market is witnessing significant growth due to several key factors. The development and procurement of advanced technologies are driving market growth as militaries worldwide invest in intelligent weapons systems to enhance their operational capabilities. Another trend influencing market growth is the increasing digitization of battlefields, which necessitates the use of smart weapons for precise and effective targeting. The integration of AI, machine learning, and sensor technologies in these weapons systems enables higher target accuracy and mission success rates, reducing collateral damage and increasing the effectiveness of precision strikes. Strict regulatory norms are also playing a role in market growth as governments prioritize the safety and security of their troops and civilians, leading to increased demand for smart weapons that minimize collateral damage.

What will be the Size of the Land Based Smart Weapons Market During the Forecast Period?

- The land-based smart weapons market encompasses the production and deployment of advanced weapon systems designed to enhance operational capabilities and minimize civilian casualties. These weapons, which include precision missiles and munitions, leverage sensor technologies to ensure target accuracy and mission success rates. The market's growth is driven by the increasing demand for conventional weapons with enhanced capabilities to counter evolving threats.

- Sensor technologies continue to advance, enabling more precise strikes and improved defense systems. Regulations play a significant role in shaping the market, ensuring the ethical use of these advanced weapons. The market's size is substantial, with continuous investment in research and development to maintain a technological edge. Platforms such as artillery, multiple launch rocket systems, and surface-to-air missiles are key areas of focus within the land-based smart weapons market.

How is this Land Based Smart Weapons Industry segmented and which is the largest segment?

The land based smart weapons industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Missiles

- Ammunition

- Others

- Geography

- North America

- US

- APAC

- China

- Europe

- Germany

- UK

- France

- Middle East and Africa

- South America

- North America

By Product Insights

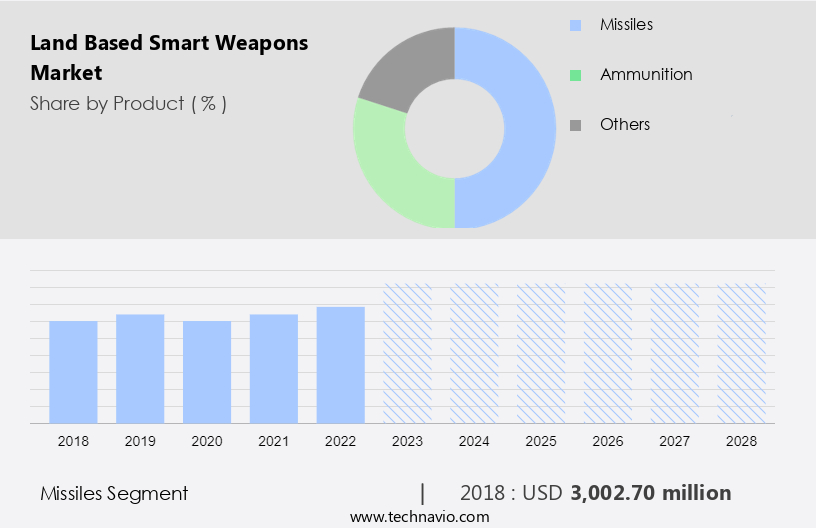

- The missiles segment is estimated to witness significant growth during the forecast period.

The market is primarily driven by the missiles segment due to the increasing demand for advanced weapon systems in modern warfare. Technological advancements, such as radio-frequency identification (RFID) technology, are used In the production of smart land-based missiles, enhancing their precision and operational capabilities. However, the high cost of development, maintenance, and technology obsolescence pose challenges to market growth. Militaries worldwide are investing in land-based smart weapons to counteract maritime threats and enhance their defense systems. The market is expected to experience growth due to the increasing pressure to minimize civilian casualties and the need for conventional weapons to be replaced with more advanced systems. Navies and air forces are also integrating smart anti-airfield weapons into their arsenals to counteract adversaries' threats.

Get a glance at the Land Based Smart Weapons Industry report of share of various segments Request Free Sample

The missiles segment was valued at USD 3 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

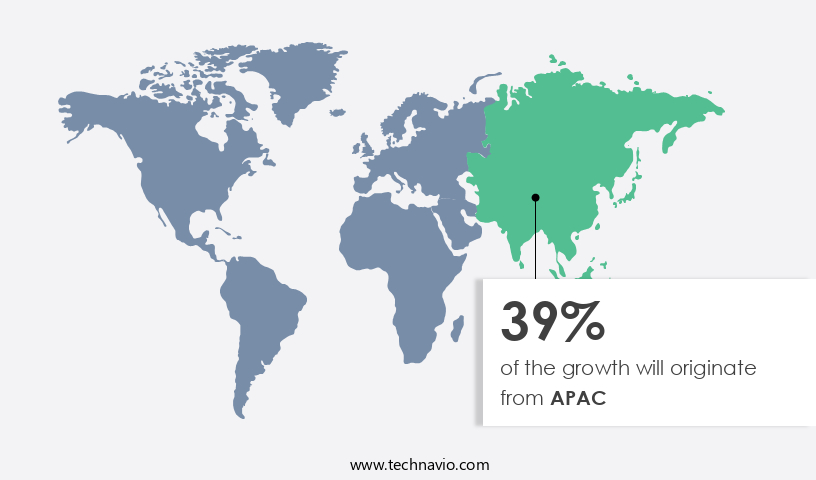

- APAC is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American region is projected to lead the global land-based smart weapons market due to increased defense expenditures and advanced defense industry capabilities. The US, as the primary contributor, has significantly benefited from the adoption of smart weapons, revolutionizing military operations. Precision, operational capabilities, and mission success rates have improved, reducing collateral damage and civilian casualties. Militaries worldwide invest in cutting-edge technologies like artificial intelligence (AI), machine learning, and sensor technologies to enhance their defense systems. These advanced weapon systems include missiles, munitions, and guided projectiles such as smart anti-airfield weapons. Naval warfare and maritime threats also necessitate the use of land-based smart weapons. Despite high costs, development, maintenance, and technology obsolescence, the market's growth is driven by the need to counter adversaries and ensure mission success. Regulations and platform compatibility are essential considerations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Land Based Smart Weapons Industry?

Development and procurement of advanced technologies is the key driver of the market.

- Land-based smart weapons have emerged as a critical component of military arsenals worldwide, with top defense spenders such as Russia, the US, and China leading the way in research and development. These advanced weapon systems offer precision, operational capabilities, and high mission success rates, making them valuable assets in various military applications. However, the high cost of development, maintenance, and technology obsolescence pose challenges to their widespread adoption. Advanced technologies like artificial intelligence (AI), machine learning, and sensor technologies are driving the evolution of land-based smart weapons. For instance, India's Defense Research and Development Organization (DRDO) is developing Energy directed weapons, while its Laser Science and Technology Center is working on a 25-kW laser weapon system for ballistic missile destruction.

- The demand for precision strikes is increasing due to the need to minimize collateral damage and ensure target accuracy. This trend is applicable to various military branches, including air forces, which are investing in smart Anti-Airfield Weapons. Moreover, naval warfare and maritime threats necessitate the development of smart missiles, munitions, and guided projectiles. Defense systems are subject to regulations, and the integration of these advanced technologies requires a careful balance between military effectiveness and ethical considerations. The market for land-based smart weapons is dynamic, with constant advancements in technology and evolving adversaries. Contracts for these systems often involve cutting-edge technologies, including directed energy weapons.

What are the market trends shaping the Land Based Smart Weapons Industry?

Growth in battlefield digitalization is the upcoming market trend.

- The market is witnessing significant growth due to the increasing demand for precision and operational capabilities in militaries worldwide. Militaries are investing in advanced weapon systems to minimize civilian casualties and improve mission success rates through precision strikes. Smart weapons, such as guided projectiles and munitions, offer superior target accuracy, reducing collateral damage. Technological advancements, including artificial intelligence (AI) and machine learning, are driving the development of cutting-edge technologies in smart weapons. Sensor technologies and defense systems are also playing a crucial role in enhancing the capabilities of these weapons. However, the high cost of development, maintenance, and technology obsolescence pose challenges to market growth.

- Modern land-based weapon systems, such as smart anti-airfield weapons, are equipped with advanced technologies like electro-optic systems for tracking armored vehicles and low-observable missiles. These systems enable platoons to strategize their approach effectively. For instance, the latest versions of shoulder-fired weapons, such as Stinger, are integrated with dual-mode seekers and identification, friend, or foe (IFF) systems. These technologies enhance the targeting efficiency of Stinger, making it less susceptible to countermeasures like flares when targeting based on heat signatures. Naval warfare and maritime threats are also driving the adoption of smart weapons in various defense applications. Contracts for directed energy weapons and missiles are on the rise, further boosting the market growth.

What challenges does the Land Based Smart Weapons Industry face during its growth?

Stringent Regulatory norms is a key challenge affecting the industry growth.

- The market is characterized by the integration of advanced technologies such as artificial intelligence (AI), machine learning, and sensor technologies into weapon systems. Precision is a key focus area for militaries to enhance operational capabilities and minimize collateral damage. companies in this market develop and manufacture a range of weapon systems, including guided projectiles, missiles, and munitions, for various defense applications. Strict regulations governing the use and storage of these high-cost weapons systems pose a challenge to market growth. Adherence to regulations related to development, maintenance, technology obsolescence, and safety is mandatory. Incidences of civilian casualties have further intensified regulatory scrutiny.

- Countries such as India, New Zealand, Australia, and the UK have stringent rules regarding the use of land based smart weapons, which may hinder market expansion. Military organizations and defense departments worldwide are investing in cutting-edge technologies such as directed energy weapons to enhance their operational capabilities and counter maritime threats. Air forces and naval warfare applications are major end-users of land based smart weapons. The market also includes smart anti-airfield weapons and various types of guided rockets and missiles. companies in this market must navigate the complex regulatory landscape while ensuring mission success rates and minimizing target inaccuracy.

Exclusive Customer Landscape

The land based smart weapons market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the land based smart weapons market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, land based smart weapons market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- BAE Systems Plc

- Diehl Stiftung and Co. KG

- Hanwha Corp.

- Israel Aerospace Industries Ltd.

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Lockheed Martin Corp.

- MBDA

- Northrop Grumman Corp.

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- RTX Corp.

- Safran SA

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of advanced weapon systems designed to enhance operational capabilities and improve mission success rates. These systems, which include guided projectiles, missiles, and munitions, are characterized by their precision and ability to minimize collateral damage. The integration of artificial intelligence (AI) and machine learning technologies into land-based smart weapons has been a significant driver of market growth. These technologies enable advanced target recognition and identification, increasing the accuracy of strikes and reducing the risk of civilian casualties. However, the high cost of development and maintenance remains a challenge for market participants.

Additionally, the rapid advancement of technology and the threat of obsolescence necessitate continuous innovation and investment. Regulations play a crucial role in shaping the market dynamics. Stringent regulations governing the use of conventional weapons and the need for ethical and responsible deployment are key considerations for manufacturers and military forces. The adoption of smart weapons is not limited to military applications. Civilian industries, such as mining and construction, are also exploring the use of precision-guided munitions for site preparation and demolition. The integration of sensor technologies and AI in defense systems has expanded the capabilities of land-based smart weapons.

Further, these systems can now detect and respond to threats in real-time, enhancing operational readiness and effectiveness. Naval warfare and maritime threats have also spurred the development of smart anti-ship missiles and guided rockets. These systems offer increased range, accuracy, and survivability, making them valuable assets for defense forces. Contracts and collaborations between governments and private companies are driving innovation In the land-based smart weapons market. These partnerships facilitate the transfer of cutting-edge technologies and expertise, enabling the development of next-generation weapon systems. The market for land-based smart weapons is expected to continue growing as military forces seek to enhance their operational capabilities and minimize collateral damage.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.51% |

|

Market Growth 2024-2028 |

USD 2.71 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

7.67 |

|

Key countries |

US, China, Germany, France, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Land Based Smart Weapons Market Research and Growth Report?

- CAGR of the Land Based Smart Weapons industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the land based smart weapons market growth of industry companies

We can help! Our analysts can customize this land based smart weapons market research report to meet your requirements.

RIA -

RIA -