Leadless Pacemakers Market Size and Growth Forecast 2026-2030

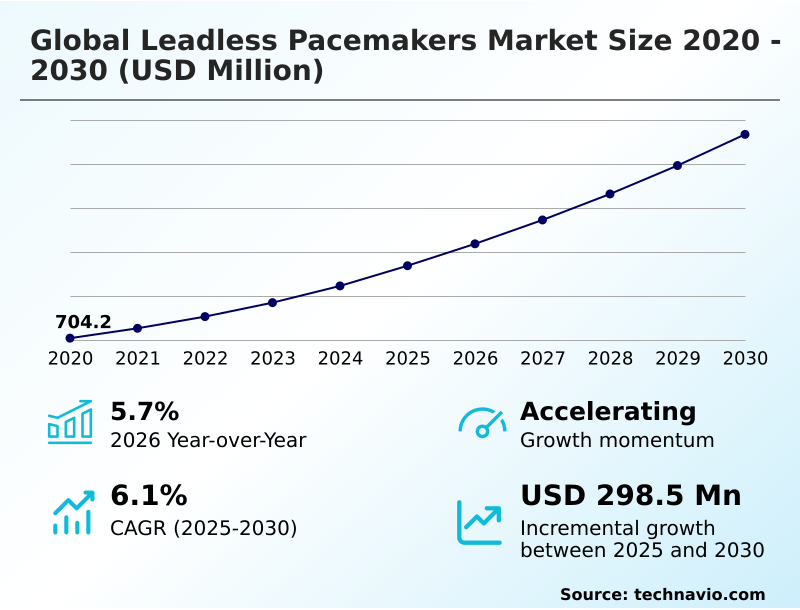

The Leadless Pacemakers Market size was valued at USD 868.8 million in 2025 growing at a CAGR of 6.1% during the forecast period 2026-2030.

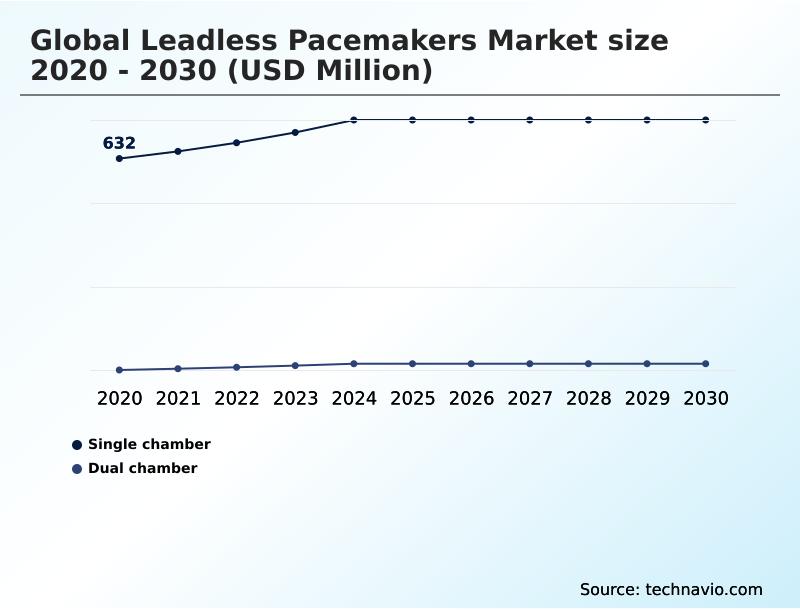

North America accounts for 39.3% of incremental growth during the forecast period. The Single chamber segment by Type was valued at USD 734.1 million in 2024, while the Hospitals segment holds the largest revenue share by End-user.

The market is projected to grow by USD 463.1 million from 2020 to 2030, with USD 298.5 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Leadless Pacemakers Market Overview

The leadless pacemakers market is defined by a rapid technological shift away from traditional transvenous systems toward fully intracardiac pacemakers. This evolution is driven by the need to mitigate transvenous lead complications and improve patient quality of life, with market expansion reflecting a year-over-year growth of 5.7%. At the operational level, a specialized cardiac catheterization laboratory transitioning to dual-chamber leadless pacemaker technology can significantly enhance its electrophysiology procedures. By adopting these systems, which utilize sophisticated implant-to-implant communication for atrioventricular synchrony, facilities can offer minimally invasive implantation to a broader patient population, including those requiring more complex cardiac rhythm management. This shift not only reduces post-operative recovery time but also aligns with value-based healthcare models by minimizing long-term device-related adverse events. North America currently contributes 39.3% of the incremental growth, propelled by favorable pacemaker reimbursement codes and a high concentration of advanced healthcare infrastructure compliant with FDA regulations, which mandate rigorous standards for device safety and efficacy. The continuous push for cardiac device miniaturization and improved pacemaker battery longevity further solidifies the market's trajectory.

Drivers, Trends, and Challenges in the Leadless Pacemakers Market

The leadless pacemakers market is shaped by a complex interplay between clinical innovation and economic realities, forcing procurement decision-makers to conduct a thorough cost-benefit analysis of leadless versus traditional pacemakers.

While the upfront investment for transcatheter pacing systems is several times higher, the long-term safety profile of intracardiac pacemakers, characterized by the near elimination of lead-related failures and pocket infections, presents a compelling total cost of ownership argument. This is especially true in high-volume cardiac centers managing patients with conditions like symptomatic bradycardia.

In practice, a hospital's cardiology department must weigh the capital expenditure against the avoidance of costly revision surgeries, a calculation influenced by the evolving reimbursement landscape for transcatheter pacing systems. The long-term performance is supported by dual-chamber leadless pacemaker clinical trial outcomes, which demonstrate effective atrioventricular synchrony.

However, challenges remain, particularly concerning end-of-life device management and the technical nuances of retrieval. Regulatory frameworks, such as the FDA's Unique Device Identification (UDI) system, add another layer of complexity by mandating comprehensive device tracking to ensure patient safety, directly impacting hospital inventory and compliance protocols.

Furthermore, technological advancements in pacemaker battery technology are critical for expanding the application to younger patients who require a decades-long solution.

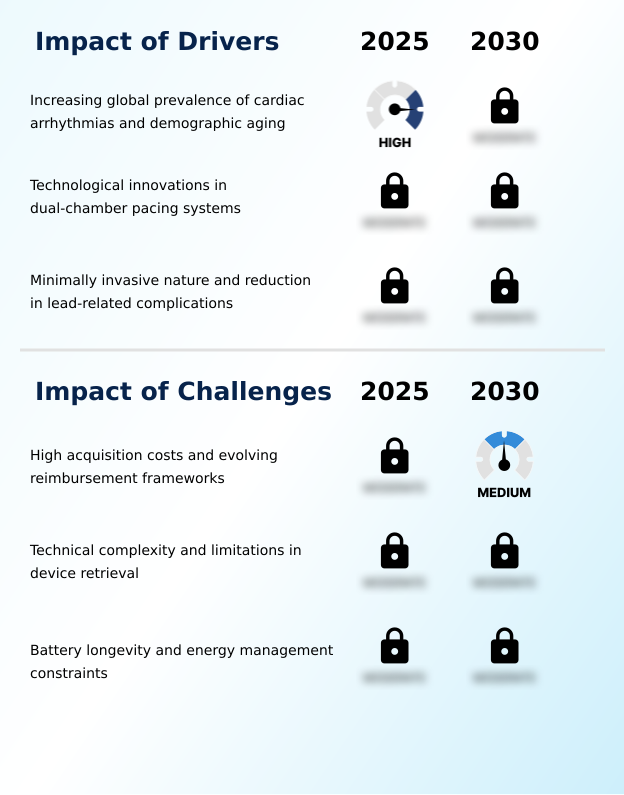

Primary Growth Driver: The increasing global prevalence of cardiac arrhythmias, coupled with an aging demographic, is a primary driver for the leadless pacemakers market.

A primary driver propelling the market, which is experiencing a 5.7% year-over-year growth, is the rising global prevalence of cardiac arrhythmias in an aging population. This demographic shift increases demand for symptomatic bradycardia treatment.

The strong clinical preference for minimally invasive implantation procedures is another significant catalyst, as catheter-delivered pacemakers reduce post-operative recovery time and eliminate pacemaker pocket infection risks.

This aligns with the objectives of value-based healthcare models, which prioritize long-term patient quality of life and reduced hospital readmissions.

Technological innovations, particularly in cardiac device miniaturization and the development of specialized delivery catheters, are making these electrophysiology procedures safer and more accessible, further accelerating adoption according to established clinical practice guidelines.

Emerging Market Trend: A significant paradigm shift is underway, moving from traditional pacemakers toward leadless solutions. This evolution is driven by technological advancements that eliminate lead-related complications and improve patient quality of life.

The market is advancing beyond single-chamber leadless pacemaker technology toward sophisticated dual-chamber systems. This trend is fueled by breakthroughs in implant-to-implant communication, enabling atrioventricular synchrony for a broader patient base with conditions like atrioventricular block. Another defining trend is the integration of digital health, with bluetooth low energy connectivity allowing for real-time remote monitoring and predictive analytics in cardiology.

This connectivity improves patient outcomes by enabling early detection of device-related adverse events and reducing hospital visits. Furthermore, research into energy harvesting pacemakers and advanced biocompatible materials is addressing the critical challenge of pacemaker battery longevity, aiming to create lifelong devices that minimize the need for risky replacement procedures and support better hemodynamic performance.

Key Industry Challenge: High acquisition costs for the devices and the complexities of evolving reimbursement frameworks present a key challenge to the widespread adoption and growth of the industry.

A critical challenge constraining market expansion is the high initial acquisition cost, which makes the technology less accessible in price-sensitive healthcare systems without established pacemaker reimbursement codes. This financial barrier is compounded by the technical complexities of end-of-life device management, as the permanent cardiac device encapsulation makes device retrieval technology both risky and difficult.

This is a major concern for younger patients who may require multiple devices over their lifetime. Additionally, limitations in current pacemaker battery longevity, especially in energy-intensive dual-chamber systems, pose an ongoing obstacle.

The physical space within the right ventricle is also a factor, as the presence of multiple abandoned devices could lead to concerns about long-term cardiac perforation risk and hemodynamic impact.

Explore Full Market Dynamics Analysis Request Free Sample

Leadless Pacemakers Market Segmentation

The leadless pacemakers industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Type Segment Analysis

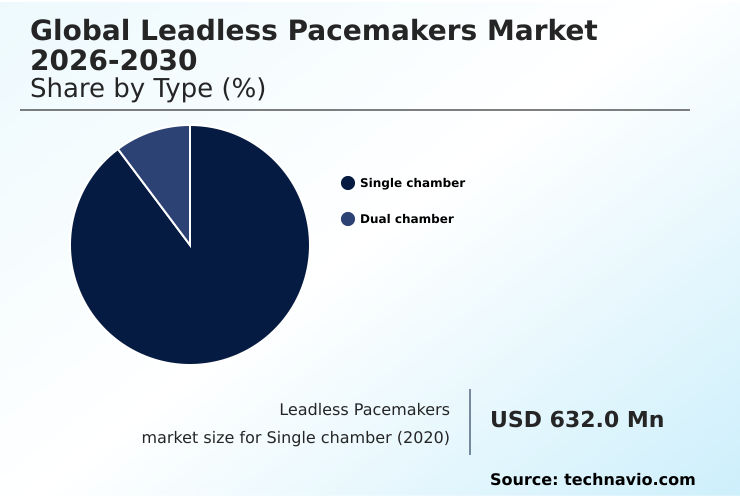

The single chamber segment is estimated to witness significant growth during the forecast period.

The single-chamber segment remains a foundational component of the leadless pacemakers market, primarily serving patients requiring right ventricle pacing without atrioventricular synchrony.

These transcatheter pacing systems, delivered via femoral vein access, eliminate transvenous lead complications and the need for a subcutaneous generator pocket, which significantly reduces risks like pacemaker pocket infection.

The technology's maturity is supported by extensive long-term clinical evidence, reinforcing its role in electrophysiology procedures. This segment, which still accounts for a majority of the market's unit volume, is crucial for elderly patients or those with compromised vascular access.

As device retrieval technology improves and clinical practice guidelines evolve under frameworks like the Medical Device Regulation (MDR), the single-chamber leadless pacemaker continues to be a vital option in cardiac rhythm management.

The Single chamber segment was valued at USD 734.1 million in 2024 and showed a gradual increase during the forecast period.

Leadless Pacemakers Market by Region: North America Leads with 39.3% Growth Share

North America is estimated to contribute 39.3% to the growth of the global market during the forecast period.

The geographic landscape of the leadless pacemakers market is led by North America, which accounts for approximately 39.3% of the market's incremental growth, driven by high healthcare spending and early technology adoption under FDA oversight.

Europe follows, contributing nearly 27%, with countries like Germany and the UK adopting these devices based on clinical evidence and recommendations from bodies like the European Society of Cardiology, all while adhering to the stringent Medical Device Regulation (MDR).

Asia is the fastest-growing region, representing over 24% of the growth, fueled by modernizing healthcare in China and Japan's large elderly population.

This region's expansion is supported by the integration of real-time remote monitoring and bluetooth low energy connectivity, which are critical for managing geographically dispersed patients.

The focus on healthcare cost-effectiveness is pushing for wider adoption of these advanced transcatheter pacing systems globally.

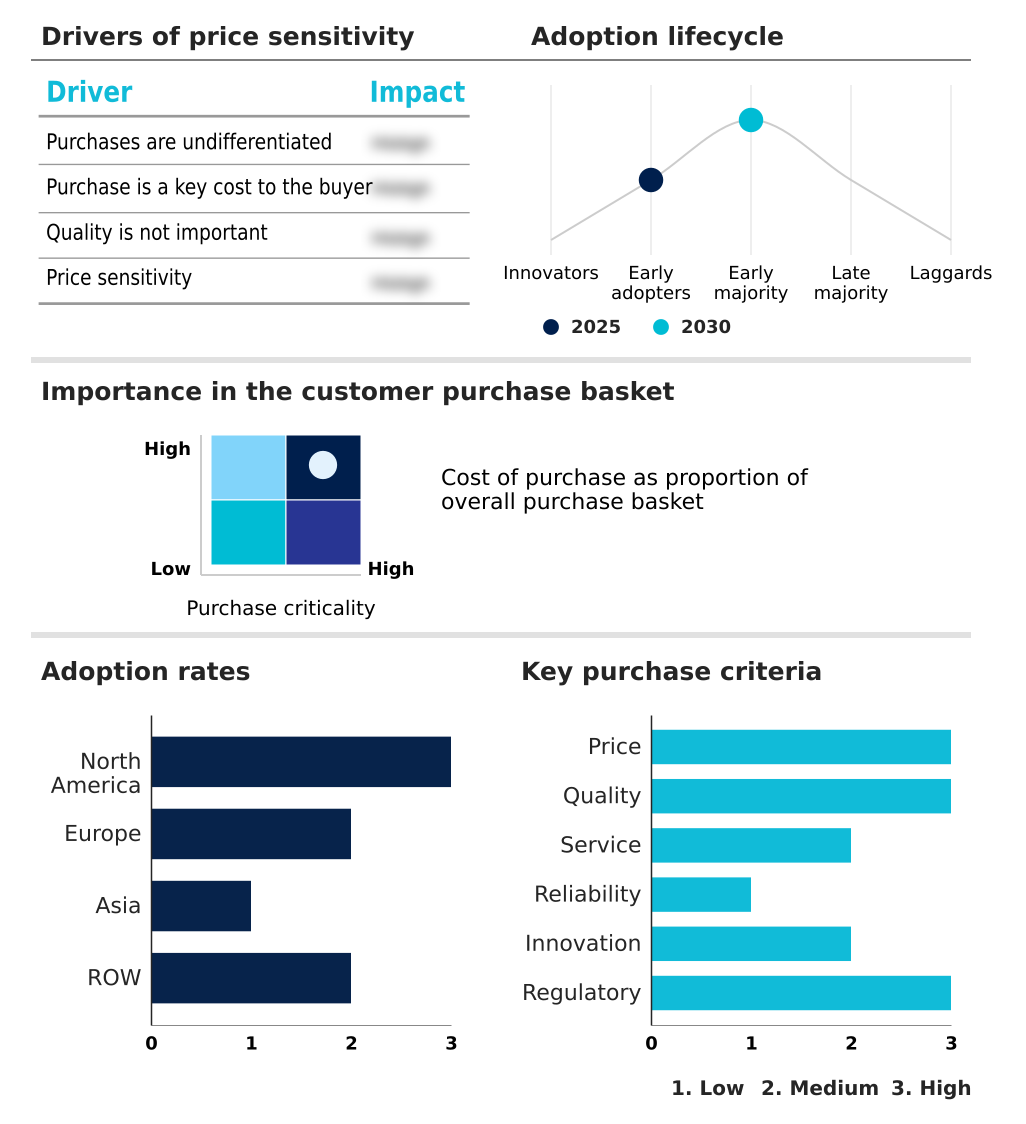

Customer Landscape Analysis for the Leadless Pacemakers Market

The leadless pacemakers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the leadless pacemakers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Leadless Pacemakers Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the leadless pacemakers market industry.

Abbott Laboratories - Key offerings include miniaturized single-chamber and dual-chamber leadless cardiac pacing systems designed to provide atrioventricular synchrony and advanced cardiac rhythm management without transvenous leads.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- BIOTRONIK SE and Co. KG

- Boston Scientific Corp.

- CAIRDAC

- Cirtec Medical

- Integer Holdings Corp.

- Medtronic Plc

- MicroPort Scientific Corp.

- OSYPKA AG

- Shree Pacetronix Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Leadless Pacemakers Market

- In October 2024, Abbott announced the introduction of its AVEIR dual-chamber (DR) leadless pacemaker system, a first-of-its-kind device designed for minimally invasive implantation to restore atrioventricular synchrony.

- In April 2025, Medtronic launched its Micra AV2 and Micra VR2, the world's smallest leadless pacemakers, in India, offering extended battery longevity and improved performance for patients with bradycardia.

- In May 2025, Institut Jantung Negara in Malaysia became the first medical center in Southeast Asia to successfully implant Abbott's AVEIR DR dual-chamber leadless pacemaker system, marking a significant clinical milestone for the region.

- In March 2025, the UK's National Institute for Health and Care Excellence (NICE) issued a provisional recommendation for the use of leadless cardiac pacemaker implantation for patients with bradyarrhythmias who need single-chamber ventricular pacing.

Research Analyst Overview: Leadless Pacemakers Market

Boardroom-level budgeting decisions for hospital networks are increasingly shaped by the capital-intensive nature of adopting advanced leadless cardiac pacing technology. While the clinical benefits of transcatheter pacing systems are clear—eliminating the subcutaneous generator pocket and mitigating long-term transvenous lead complications—the high acquisition cost necessitates a strategic evaluation of the total cost of ownership.

The introduction of the dual-chamber leadless pacemaker, which relies on proprietary implant-to-implant communication to maintain atrioventricular synchrony, has expanded the addressable market to a larger patient demographic, intensifying these capital allocation discussions. This technological leap in cardiac rhythm management allows for minimally invasive implantation via femoral vein access in a cardiac catheterization laboratory.

However, the market's trajectory is moderated by challenges in device retrieval technology and the need for improved pacemaker battery longevity to make it a viable lifelong solution. Compliance with standards like the European Medical Device Regulation (MDR) requires robust post-market surveillance, influencing procurement strategies and vendor partnerships.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Leadless Pacemakers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 275 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2026-2030 | USD 298.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, Saudi Arabia, UAE and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Leadless Pacemakers Market: Key Questions Answered in This Report

-

What is the expected growth of the Leadless Pacemakers Market between 2026 and 2030?

-

The Leadless Pacemakers Market is expected to grow by USD 298.5 million during 2026-2030, registering a CAGR of 6.1%. Year-over-year growth in 2026 is estimated at 5.7%%. This acceleration is shaped by increasing global prevalence of cardiac arrhythmias and demographic aging, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Single chamber, and Dual chamber), End-user (Hospitals, and ASC), Indication (Bradyarrhythmia, Atrioventricular block, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Single chamber segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). North America is estimated to contribute 39.3% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, Saudi Arabia, UAE and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increasing global prevalence of cardiac arrhythmias and demographic aging, which is accelerating investment and industry demand. The main challenge is high acquisition costs and evolving reimbursement frameworks, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Leadless Pacemakers Market?

-

Key vendors include Abbott Laboratories, BIOTRONIK SE and Co. KG, Boston Scientific Corp., CAIRDAC, Cirtec Medical, Integer Holdings Corp., Medtronic Plc, MicroPort Scientific Corp., OSYPKA AG and Shree Pacetronix Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Leadless Pacemakers Market Research Insights

Market dynamics are heavily influenced by the clinical and economic advantages of avoiding transvenous lead complications. This is driving a significant shift toward catheter-delivered pacemakers, particularly in outpatient settings like ambulatory surgical centers, which now account for an increasing share of procedures.

These facilities can leverage the shorter post-operative recovery time and lower infection risk profile of leadless devices to improve patient throughput and satisfaction. The adoption is further supported by specific pacemaker reimbursement codes established by bodies like the Centers for Medicare and Medicaid Services (CMS), which validate the healthcare cost-effectiveness of the technology.

The integration of proprietary communication protocols in dual-chamber systems addresses more complex conditions like atrioventricular block therapy, expanding the addressable patient population and reinforcing the move toward these advanced cardiac device telemetry solutions.

We can help! Our analysts can customize this leadless pacemakers market research report to meet your requirements.

RIA -

RIA -