Lignocellulosic Feedstock-Based Biofuel Market Size 2024-2028

The lignocellulosic feedstock-based biofuel market size is forecast to increase by USD 33.65 billion, at a CAGR of 50.35% between 2023 and 2028.

- The market is driven by the increasing ethanol blending rate targets, which necessitate the exploration of alternative feedstocks beyond traditional corn and sugarcane. However, the market faces significant challenges. The non-cropland affecting nature of lignocellulosic feedstock, which includes agricultural residues and energy crops, poses a challenge in terms of availability and sustainability. Additionally, the complex and costly conversion process for lignocellulosic biomass into biofuels remains a significant hurdle.

- Companies seeking to capitalize on this market must navigate these challenges by focusing on innovation in feedstock sourcing and conversion technologies. Success in this market requires a strategic approach to supply chain management and cost optimization, ensuring a sustainable and cost-effective production process.

What will be the Size of the Lignocellulosic Feedstock-Based Biofuel Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in enzymatic hydrolysis and separation technologies. Agricultural residues, such as sugarcane bagasse and corn stover, are increasingly utilized as feedstocks due to their availability and fuel efficiency. However, scale-up challenges persist, necessitating supply chain optimization and improved feedstock logistics. Energy crops and anaerobic digestion offer alternative sources of lignocellulosic biomass, while waste management initiatives provide a sustainable solution for reducing carbon footprint. Investment incentives and sustainability metrics play a crucial role in ensuring economic viability, as process optimization and the reduction of water usage become key priorities. Food waste and government subsidies also contribute to the market's dynamism, with the potential to significantly increase biomass yield.

Policy regulations and market penetration strategies continue to shape the industry, with a focus on commercialization of cellulosic ethanol and the exploration of new conversion technologies, such as acid hydrolysis and thermal pretreatment. The ongoing quest for higher conversion efficiency and lower carbon footprint drives innovation in the sector, with a growing emphasis on life cycle assessment and greenhouse gas emissions reduction. Storage and transportation solutions are also essential for ensuring the competitiveness of lignocellulosic biofuels in the marketplace. Market players continue to explore commercialization strategies, with wood chips and municipal solid waste emerging as promising feedstocks. The integration of advanced technologies, such as mechanical pretreatment and process optimization, is essential for addressing the complexities of lignocellulosic biomass conversion and ensuring long-term market growth.

How is this Lignocellulosic Feedstock-Based Biofuel Industry segmented?

The lignocellulosic feedstock-based biofuel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Conversion Process

- Biochemical

- Thermochemical

- Application

- Automotive

- Aviation

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- APAC

- China

- South America

- Brazil

- Rest of World (ROW)

- North America

By Conversion Process Insights

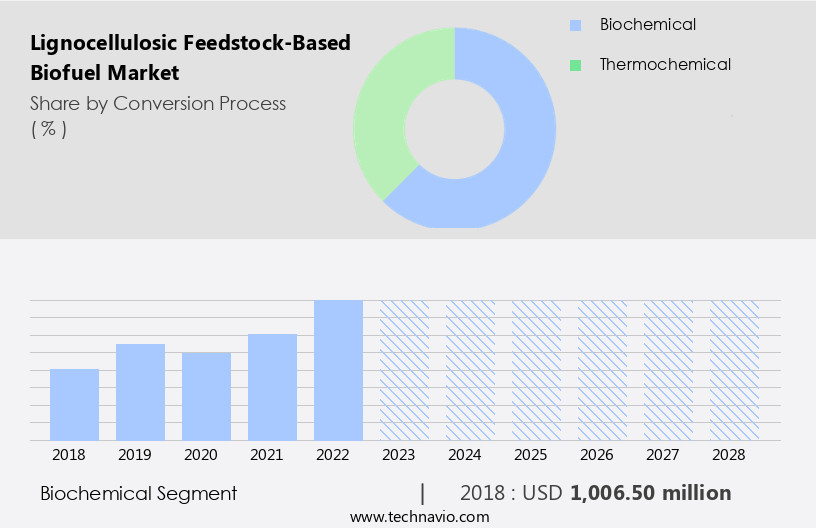

The biochemical segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing focus on sustainable energy sources and the availability of abundant agricultural residues and energy crops. The biochemical segment dominates this market, driven by the emphasis on research and development in the conversion process. This process involves three primary steps: pretreatment of feedstocks, enzymatic hydrolysis, and fermentation, followed by the recovery of end-products. Feedstocks undergo physical or chemical pretreatment to disrupt their fibrous structure, allowing for the separation of hemicelluloses from lignin and cellulose chains. Enzymatic hydrolysis then breaks down the cellulose into simple sugars, which are fermented into biofuels. Scale-up challenges persist due to the complex nature of the conversion process and the need for efficient separation technologies.

Supply chain optimization is crucial for economic viability, with feedstock logistics and water usage being key considerations. Sugarcane bagasse and corn stover are common feedstocks, but wood chips and municipal solid waste are also gaining attention. Energy crops, such as switchgrass and miscanthus, offer potential for increased biomass yield. Anaerobic digestion is an alternative biofuel production method, converting organic waste into biogas through microbial processes. Investment incentives, sustainability metrics, and process optimization are essential for commercialization strategies. Government subsidies and policy regulations play a significant role in market penetration, while carbon footprint and life cycle assessment are crucial for assessing the environmental impact.

Market penetration is influenced by factors such as conversion efficiency, land use, and energy yield. Acid hydrolysis and thermal pretreatment are common pretreatment methods, with conversion efficiency and process optimization being key challenges. Cellulosic ethanol is a promising biofuel, but commercialization strategies must address storage and transportation logistics. Overall, the market is evolving, driven by technological advancements and the need for sustainable energy solutions.

The Biochemical segment was valued at USD 1.01 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 29% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing moderate growth, with significant contributions from the US and Canada. Favorable government policies promoting biofuel adoption and development are a major growth driver in the US. Agricultural residues, such as corn stover and sugarcane bagasse, are commonly used feedstocks for this market. Enzymatic hydrolysis and separation technologies are employed for converting lignocellulosic biomass into biofuels, with challenges in scale-up and supply chain optimization being key considerations. Energy crops, municipal solid waste, and wood chips are other potential feedstocks. Water usage is a critical factor in the production process, and economic viability is a significant concern.

Downstream processing, anaerobic digestion, and waste management are integral parts of the value chain. Investment incentives and sustainability metrics are essential for process optimization, while food waste and government subsidies offer opportunities for market expansion. Carbon footprint, life cycle assessment, and greenhouse gas emissions are crucial sustainability metrics. Energy yield and conversion efficiency are important factors influencing market penetration. Policy regulations and land use also impact market dynamics. Lignocellulosic feedstocks, including corn stover, are subjected to mechanical or thermal pretreatment before hydrolysis, with acid hydrolysis and thermal pretreatment being common methods. The market's growth is influenced by factors such as fuel efficiency, scale-up challenges, supply chain optimization, and government regulations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Lignocellulosic Feedstock-Based Biofuel Industry?

- The non-cropland source and eco-friendly nature of lignocellulosic feedstocks serve as the primary market drivers, making them an essential alternative to traditional crops in the bioenergy sector.

- Lignocellulosic feedstocks, derived from agricultural residues and other non-food sources, are gaining popularity as sustainable alternatives to traditional fossil fuels in the bioenergy sector. The production of biofuels from lignocellulosic biomass involves enzymatic hydrolysis to convert complex plant structures into simpler sugars, followed by fermentation and separation technologies to produce fuel. However, scaling up this process presents challenges due to the complexities of lignocellulosic feedstock and the need for water usage in the hydrolysis process. Supply chain optimization is crucial for the cost-effective production of lignocellulosic biofuels. Feedstock logistics, including the transportation and storage of agricultural residues, can significantly impact production costs.

- Sugarcane bagasse, a common feedstock for bioethanol production, is often co-located with sugar mills to minimize transportation costs. Despite these challenges, the market for lignocellulosic feedstock-based biofuels is expected to grow due to their potential for increased fuel efficiency and reduced greenhouse gas emissions compared to traditional fossil fuels. However, addressing scale-up challenges and improving the overall efficiency of the production process will be essential for the commercial viability of this sector.

What are the market trends shaping the Lignocellulosic Feedstock-Based Biofuel Industry?

- The ethanol blending rate is increasingly becoming a significant trend in the market, with mandatory targets on the rise. This development reflects the growing emphasis on renewable energy sources and sustainable fuel options.

- The market is experiencing significant growth due to increasing government initiatives and economic viability. Biofuels derived from lignocellulosic feedstocks, such as energy crops and waste, offer a sustainable alternative to traditional fossil fuels, contributing to the reduction of greenhouse gas (GHG) emissions. Governments worldwide are implementing policies and incentives to promote the use of biofuels, including subsidies, tax incentives, and mandates. For instance, the US government provides incentives through the Renewable Fuel Standard (RFS) and the Production Tax Credit (PTC). These incentives have encouraged the investment in downstream processing technologies, such as anaerobic digestion and process optimization, to convert lignocellulosic feedstocks into biofuels.

- Furthermore, the increasing focus on sustainability metrics and waste management has led to an increase in the utilization of food waste as a feedstock for biofuel production. The anaerobic digestion process converts food waste into biogas, which can be further processed into biofuels. This not only reduces the amount of waste sent to landfills but also provides a renewable energy source. Investment in research and development is also driving the market growth, with a focus on improving the efficiency and economics of the production process. The use of advanced technologies, such as enzyme engineering and microbial optimization, is expected to reduce the production costs and increase the competitiveness of biofuels with fossil fuels.

- Overall, the market is expected to continue its growth trajectory, driven by government initiatives, economic viability, and the need for sustainable and renewable energy sources.

What challenges does the Lignocellulosic Feedstock-Based Biofuel Industry face during its growth?

- The complex and costly conversion process poses a significant challenge to the industry's growth trajectory, necessitating the need for innovative solutions and strategic investments to streamline the transition and maintain competitiveness.

- Lignocellulosic feedstocks, comprised primarily of lignin, hemicellulose, and cellulose, serve as a significant source for biofuel production, particularly bioethanol. However, converting these feedstocks into biofuels poses challenges due to factors like the inefficient breakdown of hemicellulose and cellulose, and lignin's recalcitrant nature to degradation. Additional hurdles include the diverse sugars produced from carbohydrate polymers and the high expenses associated with feedstock storage, transportation, and collection. The bioethanol production process from lignocellulosic feedstocks consists of four stages: pretreatment, enzymatic hydrolysis, fermentation, and separation. Pretreatment breaks down the feedstock structure, making it easier for enzymes to access the polysaccharides. Enzymatic hydrolysis converts the polysaccharides into simple sugars, which are then fermented into ethanol.

- Lastly, separation isolates the ethanol from the fermentation broth. Despite these challenges, the environmental benefits of lignocellulosic feedstocks are substantial. Through life cycle assessments and carbon footprint studies, it has been shown that these feedstocks can significantly reduce greenhouse gas emissions compared to traditional fossil fuels. Commercialization strategies for lignocellulosic biofuels are continually evolving, with various feedstocks under consideration, including corn stover, wood chips, and municipal solid waste.

Exclusive Customer Landscape

The lignocellulosic feedstock-based biofuel market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the lignocellulosic feedstock-based biofuel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, lignocellulosic feedstock-based biofuel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aemetis Inc. - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and research to enhance athlete performance and consumer experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aemetis Inc.

- ALTRET GREENFUELS Ltd

- BDI BioEnergy International GmbH

- Blue Biofuels Inc.

- Borregaard ASA

- China Petrochemical Corp.

- Clariant International Ltd.

- COSAN S.A.

- DuPont de Nemours Inc.

- ENERKEM Inc.

- Genera Inc.

- Gevo Inc.

- GranBio Investimentos SA

- New Energy Blue LLC

- Novozymes AS

- VERBIO Vereinigte BioEnergie AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Lignocellulosic Feedstock-Based Biofuel Market

- In January 2024, DuPont Nutrition & Biosciences, a leading biotech company, announced the commercial launch of its new enzyme product, Danisco CELLIC CTEC2, designed to improve the efficiency of lignocellulosic biofuel production from non-food feedstocks (DuPont Press Release, 2024).

- In March 2024, Shell New Energies and LanzaTech, a carbon recycling technology company, signed a strategic partnership to build a commercial-scale carbon capture and utilization facility in the Netherlands, which will convert emissions from steel production into ethanol for biofuel production (Shell Press Release, 2024).

- In May 2024, POET, the largest bioethanol producer in the US, raised USD 300 million in a funding round led by Temasek, a global investment company, to expand its production capacity for advanced biofuels from lignocellulosic feedstocks (POET Press Release, 2024).

- In April 2025, the European Union approved the Renewable Energy Directive II, which sets a binding target of at least 14% renewable content in transport fuels by 2030, creating significant market opportunities for lignocellulosic biofuels (European Commission Press Release, 2025).

Research Analyst Overview

- The market is witnessing significant advancements, driven by the need for sustainable fuels and renewable resources. Second-generation biofuels derived from lignocellulosic biomass, such as agricultural residues and energy crops, offer engine compatibility with existing infrastructure and contribute to rural development. Enzyme technology plays a crucial role in the production process, enabling the conversion of complex lignocellulosic feedstocks into simple sugars. Carbon capture and process intensification are essential for reducing the environmental impact of biofuel production. Genetic engineering and metabolic engineering are employed to optimize feedstock yield and improve the efficiency of biofuel production. Third-generation biofuels, including advanced biofuels and bio-based chemicals, are gaining traction due to their potential to further reduce emissions and contribute to a circular economy.

- Sustainable agriculture practices are integral to the biofuel value chain, ensuring the social impact and economic development of rural communities. Biofuel blends and fuel additives are essential components of the market, contributing to process control and meeting emission standards. Precision agriculture and quality control are essential for optimizing feedstock production and ensuring consistent product quality. The market for biomass energy and renewable resources is evolving, with a focus on next-generation biofuels and sustainable fuels. Process control and advanced technologies, such as emission standards and circular economy principles, are shaping the industry's future. The integration of biofuels into the renewable energy landscape offers a promising pathway to reduce green energy's environmental impact and promote economic growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Lignocellulosic Feedstock-Based Biofuel Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 50.35% |

|

Market growth 2024-2028 |

USD 33648.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

38.86 |

|

Key countries |

US, China, Brazil, Germany, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Lignocellulosic Feedstock-Based Biofuel Market Research and Growth Report?

- CAGR of the Lignocellulosic Feedstock-Based Biofuel industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, South America, Europe, APAC, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the lignocellulosic feedstock-based biofuel market growth of industry companies

We can help! Our analysts can customize this lignocellulosic feedstock-based biofuel market research report to meet your requirements.

RIA -

RIA -