Liquid Applied Membrane Market for Construction Industry Size 2024-2028

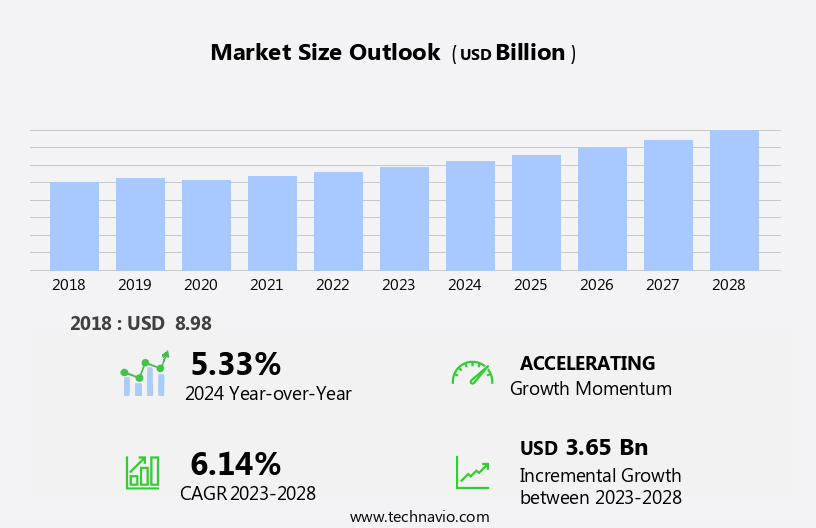

The liquid applied membrane market for construction industry size is forecast to increase by USD 3.65 billion, at a CAGR of 6.14% between 2023 and 2028.

- The Liquid Applied Membrane Market in the Construction Industry is experiencing significant growth due to the increasing demand for energy-efficient buildings. This trend is driven by stringent energy regulations and growing awareness of sustainable construction practices. Additionally, advancements in robotic application systems and automatic spray technologies have streamlined the installation process, making Liquid Applied Membranes an attractive option for construction projects. However, the market faces challenges in the form of higher initial material and installation costs when compared to traditional methods. These costs may hinder the widespread adoption of liquid applied membranes, particularly in price-sensitive markets. To capitalize on market opportunities, construction companies can focus on offering value-added services, such as energy consulting and long-term maintenance contracts, to offset the higher upfront costs.

- Additionally, ongoing research and development efforts aimed at reducing material costs and improving application efficiency will be crucial for market growth. Companies seeking to navigate these challenges effectively should also explore strategic partnerships and collaborations to share resources and expertise, ultimately driving innovation and competitiveness in the market.

What will be the Size of the Liquid Applied Membrane Market for Construction Industry Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

Liquid applied membranes have become a significant solution in the construction industry, offering versatility and effectiveness in various applications. These membranes, which include roofing membranes and foundation waterproofing, have evolved to cater to the ever-changing market dynamics. Acrylic membranes, for instance, have gained popularity due to their high tensile strength and chemical resistance. Moreover, the continuous pursuit of energy efficiency and environmental sustainability has led to the emergence of green building materials and low-volatile organic compound (VOC) coatings. The use of recycled materials and reinforced membranes has also become increasingly common in the industry. In commercial buildings, seamless membranes have gained traction for their improved service life and tear resistance.

Silicone membranes and polymer-modified bitumen have been favored for their adhesion strength and moisture vapor transmission properties, respectively. Application methods have also evolved, with roller application and brush application offering cost-effective solutions, while spray application and trowel application providing more precise and uniform coverage. Industry standards and environmental regulations continue to shape the market, with a focus on reducing waste and improving VOC emissions. The ongoing unfolding of market activities reveals a trend towards high-performance membranes, offering thermal insulation, UV resistance, and crack bridging properties. Self-adhering membranes and primer coatings have also gained popularity for their ease of application and improved joint sealing capabilities.

Infrastructure projects and wall cladding applications have further expanded the market for liquid applied membranes, with the need for chemical resistance, crack bridging, and application equipment becoming increasingly important considerations. Building codes and residential buildings have also adopted these membranes for their durability and cost-effectiveness. Overall, the liquid applied membrane market continues to evolve, with ongoing research and development leading to new innovations and applications across various sectors. The market's continuous dynamism underscores the importance of staying informed and adaptable to meet the evolving needs of the construction industry.

How is this Liquid Applied Membrane for Construction Industry Industry segmented?

The liquid applied membrane for construction industry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Roofing and walls

- Building structures

- Industrial water and wastewater management

- Landfills and tunnels

- End-user

- Commercial

- Public infrastructure

- Residential

- Type

- Polyurethane

- Bituminous

- Cementitious

- Elastomeric

- Acrylic

- Technology

- Solvent-based

- Water-based

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

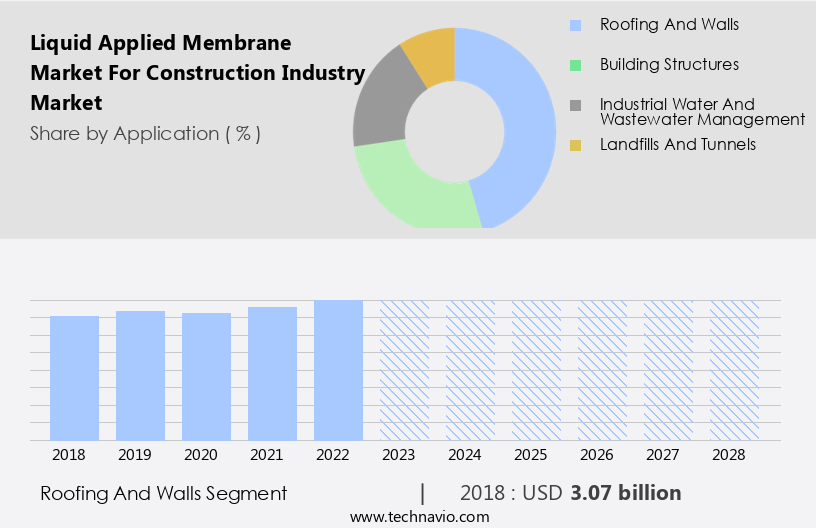

By Application Insights

The roofing and walls segment is estimated to witness significant growth during the forecast period.

The global liquid applied membrane market in the construction industry is gaining momentum due to the numerous benefits these membranes offer over traditional roofing and wall systems. Liquid applied membranes are applied in a liquid form directly to surfaces, creating a seamless and continuous barrier against water, moisture, and other elements. This segment is vital for ensuring the structural integrity and extended service life of roofs and walls in various commercial and residential projects. Compared to conventional methods, liquid applied membranes provide several advantages. They eliminate joints and seams, which are common sources of leakage in other systems.

These membranes offer excellent puncture resistance, thermal insulation, and energy efficiency, making them an attractive option for green building materials. Additionally, they are available in various types, such as high-performance membranes, asphalt membranes, acrylic membranes, silicone membranes, and polyurethane membranes, among others. Moreover, liquid applied membranes can be applied using various techniques, including roller application, trowel application, brush application, and spray application. They are also available in water-based and solvent-based coatings, catering to different environmental regulations and industry standards. Furthermore, these membranes can be reinforced with reinforcement fabrics and self-adhering, providing enhanced tear resistance and adhesion strength. Liquid applied membranes also offer cost-effective solutions through waste reduction and life-cycle cost analysis.

They are available in recycled materials and can be easily repaired and maintained, reducing the need for frequent replacements. Additionally, they offer excellent UV resistance, moisture vapor transmission, and crack bridging properties, making them suitable for various infrastructure projects. In conclusion, the liquid applied membrane market for construction industry is evolving, with a focus on innovation and sustainability. These membranes offer several advantages, including seamless application, durability, energy efficiency, and cost-effectiveness, making them an attractive option for various construction projects.

The Roofing and walls segment was valued at USD 3.07 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

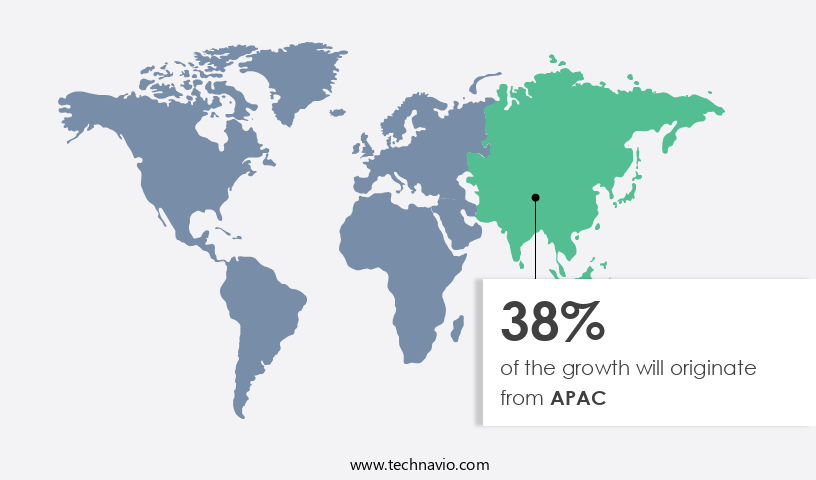

APAC is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The liquid applied membrane market in the construction industry is experiencing notable expansion in the Asia-Pacific (APAC) region. These membranes are increasingly adopted for various applications, such as roofing, waterproofing, and building exteriors, due to their protective qualities and ease of application. The primary driver of market growth in APAC is the region's rapid urbanization and infrastructure development, particularly in countries like China, India, and Japan. As construction of residential, commercial, and industrial buildings surges in these countries, there is a heightened demand for robust waterproofing solutions to shield structures from water damage. Liquid applied membranes offer advantages such as shorter curing times, waste reduction, and improved energy efficiency compared to traditional solvent-based coatings.

Additionally, they exhibit desirable properties like puncture resistance, thermal insulation, moisture vapor transmission control, and chemical resistance. High-performance membranes, including acrylic, silicone, polyurethane, and polymer-modified bitumen, cater to diverse construction needs. Application methods range from roller and trowel to brush, spray, and trowel. Industry standards and environmental regulations ensure the use of low-voc coatings, recycled materials, and reinforced membranes for enhanced sustainability. Seamless membranes, self-adhering membranes, and primer coatings are essential components of the system. Building codes and joint sealing techniques further ensure the durability and longevity of the structures. Overall, the liquid applied membrane market in the construction industry is poised for continued growth in APAC, driven by the region's construction boom and the demand for advanced, efficient, and eco-friendly waterproofing solutions.

Market Dynamics

The global liquid applied membrane market (construction) is experiencing significant growth, driven by increasing demand for effective waterproofing membranes in diverse applications. The expanding liquid applied membrane market size (construction) and positive liquid applied membrane market trends (construction) highlight the market's dynamism, fueled by strong liquid applied membrane market growth drivers. Liquid applied membranes (LAM), including versatile polyurethane membranes, acrylic membranes, bituminous membranes, and robust polyurea membranes, are widely utilized. These solutions are crucial for roof waterproofing, basement waterproofing, foundation waterproofing, and wet room waterproofing in both new construction projects and renovation & refurbishment initiatives. Innovations in polymer technology (LAM) facilitate seamless application technology and the development of rapid curing liquid membranes. The increasing focus on sustainability also boosts the adoption of VOC-compliant membranes, further solidifying LAM's position in the construction industry.Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Liquid Applied Membrane for Construction Industry Industry?

- The surge in demand for energy-efficient buildings is the primary catalyst driving growth in the market.

- The construction industry is undergoing a transformation with a focus on sustainability and energy efficiency. This shift is driven by the increasing demand for energy-efficient buildings, which aim to reduce energy consumption and minimize carbon footprints. Liquid applied membranes are playing a pivotal role in this transition. These membranes offer a seamless, durable, and protective layer for various building surfaces, contributing to enhanced insulation, optimized energy usage, and improved building performance. Liquid applied membranes come in different types, including high-performance membranes and asphalt membranes. High-performance membranes provide excellent puncture resistance, tear resistance, and moisture vapor transmission control.

- They are ideal for applications where durability and long-term performance are crucial. Asphalt membranes, on the other hand, offer excellent thermal insulation and are widely used in low-slope roofing applications. Solvent-based coatings, a traditional alternative to liquid applied membranes, have higher curing times and generate more waste. In contrast, liquid applied membranes have shorter curing times and produce minimal waste, making them a more eco-friendly and cost-effective choice. Moreover, the use of liquid applied membranes can lead to significant energy savings over the building's life cycle due to their insulating properties. In summary, the liquid applied membrane market for the construction industry is experiencing substantial growth due to the increasing demand for energy-efficient buildings.

- These membranes offer numerous benefits, including improved insulation, optimized energy usage, and reduced waste, making them a preferred choice for modern construction projects.

What are the market trends shaping the Liquid Applied Membrane for Construction Industry Industry?

- The convergence of robotic application systems and automatic spray technologies represents a significant market trend. Advancements in these technologies are driving innovation and efficiency in various industries.

- The global market for liquid applied membranes in the construction industry has witnessed notable advancements, driven by technological innovations in application systems. Robotic application systems and automatic spraying technologies have gained prominence, streamlining the process of applying membranes onto various surfaces. These systems, equipped with sophisticated programming software and sensors, ensure precise and consistent application, thereby enhancing project outcomes. Acrylic membranes, polymer-modified bitumen, silicone membranes, and specialty membranes are popular choices for roofing and foundation waterproofing applications. Surface preparation plays a crucial role in ensuring the longevity and effectiveness of these membranes. Low-voc coatings, a sustainable choice for green building materials, are increasingly being adopted due to their minimal volatile organic compound emissions.

- Tensile strength, a critical factor in membrane selection, is a key consideration for commercial buildings. Roller application and trowel application techniques are also used, depending on the specific project requirements. Overall, the liquid applied membrane market is characterized by continuous innovation and a focus on delivering high-performance, reliable, and cost-effective solutions for the construction industry.

What challenges does the Liquid Applied Membrane for Construction Industry Industry face during its growth?

- The higher initial material and installation costs relative to traditional methods pose a significant challenge to industry growth. This issue, which is mandatory for businesses to address in a professional and knowledgeable manner, can hinder the expansion and competitiveness of companies in the sector.

- The Liquid Applied Membrane market in the construction industry experiences growth driven by the membranes' superior waterproofing and protective properties. However, the market encounters challenges due to the higher initial material and installation costs compared to traditional methods. Liquid Applied Membranes necessitate specialized liquid compounds, primers, and coatings, which can be more expensive than conventional waterproofing materials. Furthermore, the application process may require additional equipment and tools, increasing upfront expenses. Industry standards and environmental regulations also impact the market. Adherence to these regulations can add to the cost of production and installation. Liquid Applied Membranes offer benefits such as crack bridging, chemical resistance, and UV resistance, making them an attractive option for wall cladding and other protective applications.

- Environmental consciousness is a significant factor influencing the market. The use of recycled materials in the production of liquid applied membranes is gaining popularity due to their reduced environmental impact. The application methods, such as brush or spray application, offer flexibility and ease of use. Despite the initial high costs, the long-term benefits of Liquid Applied Membranes, including durability and low maintenance, make them a cost-effective solution for construction projects. The market is expected to continue growing as the construction industry seeks innovative and effective waterproofing and protective solutions.

Exclusive Customer Landscape

The liquid applied membrane market for construction industry market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the liquid applied membrane market for construction industry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, liquid applied membrane market for construction industry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alchimica - The construction industry benefits from the company's innovative liquid applied membrane solutions, such as MasterSeal 730 UVS. This high-performance waterproofing membrane utilizes pre-applied, high-density polyethylene (HDPE) sheets with a unique pressure-sensitive adhesive and protective coating. The membrane ensures excellent adhesion to concrete surfaces without the need for additional protective screeds.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alchimica

- BASF SE

- Bauder Ltd.

- Berkshire Hathaway Inc.

- Carlisle Companies Inc.

- Compagnie de Saint Gobain

- Dow Chemical Co.

- Follmann Chemie GmbH

- Fosroc International Ltd.

- H.B. Fuller Co.

- IBG Industrie Beteiligungs Gesellschaft mbH and Co. KG

- IKO Industries Ltd.

- Mapei SpA

- Nippon Paint Holdings Co. Ltd.

- RPM International Inc.

- Sika AG

- SOPREMA SAS

- Standard Industries Inc.

- Western Colloid

- Pidilite Industries Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Liquid Applied Membrane Market For Construction Industry Market

- In January 2024, Sika AG, a leading specialty chemical company, announced the launch of its new liquid applied membrane product, Sikalastik 611, designed for roofing and waterproofing applications in the construction industry (Sika AG Press Release, 2024). This innovative product offers enhanced durability and improved sustainability, making it a significant addition to the company's membrane portfolio.

- In March 2024, BASF SE and Covestro AG, two major chemical companies, entered into a strategic partnership to jointly develop and produce liquid applied membranes using renewable raw materials (BASF SE Press Release, 2024). This collaboration aims to reduce the environmental footprint of membrane production and cater to the growing demand for eco-friendly construction solutions.

- In May 2024, H.B. Fuller Company, a global adhesives provider, acquired Permabond LLC, a leading manufacturer of structural bonding adhesives and sealants, including liquid applied membranes (H.B. Fuller Company Press Release, 2024). This acquisition strengthened H.B. Fuller's position in the construction industry and expanded its product offerings, providing a broader range of solutions for customers.

- In April 2025, the European Union passed the new Construction Products Regulation (CPR) for liquid applied membranes, which sets stricter requirements for health, safety, and environmental performance (European Commission Press Release, 2025). This regulation will drive innovation and improvements in the production and application of liquid applied membranes, ensuring better quality and sustainability in the construction industry.

Research Analyst Overview

- In the construction industry, Liquid Applied Membranes (LAMs) have gained significant traction as an effective solution for preventing moisture ingress and ensuring health and safety. Project management teams increasingly prioritize risk assessment and supply chain management when considering LAMs for their construction projects. Bid specifications require careful attention to application temperature, membrane thickness, and technical assistance during the contract negotiation phase. Industry innovations, such as technology advancements and performance guarantees, are driving the market forward. Quality control measures, including bond strength testing, inspection procedures, and material data sheets, are essential for ensuring successful LAM installations.

- Competitor analysis and environmental impact assessments are also crucial factors in the decision-making process. UV degradation, puncture resistance testing, and substrate compatibility are essential considerations for assessing LAMs' long-term performance. Contractors must also address problem-solving, thermal aging, and safety data sheets during the project scheduling phase. Cost estimation, training programs, and customer support are essential for managing the LAM project's financial and logistical aspects. Installation guidelines, failure analysis, and technical specifications are vital for ensuring a successful project outcome. Regardless of the challenges, the LAM market continues to evolve, driven by ongoing advancements in technology and a commitment to maintaining standards compliance.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Liquid Applied Membrane Market for Construction Industry Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.14% |

|

Market growth 2024-2028 |

USD 3.65 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.33 |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Liquid Applied Membrane Market for Construction Industry Market Research and Growth Report?

- CAGR of the Liquid Applied Membrane for Construction Industry industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the liquid applied membrane market for construction industry market growth of industry companies

We can help! Our analysts can customize this liquid applied membrane market for construction industry market research report to meet your requirements.

RIA -

RIA -