Liquid Waste Management Market Size 2026-2030

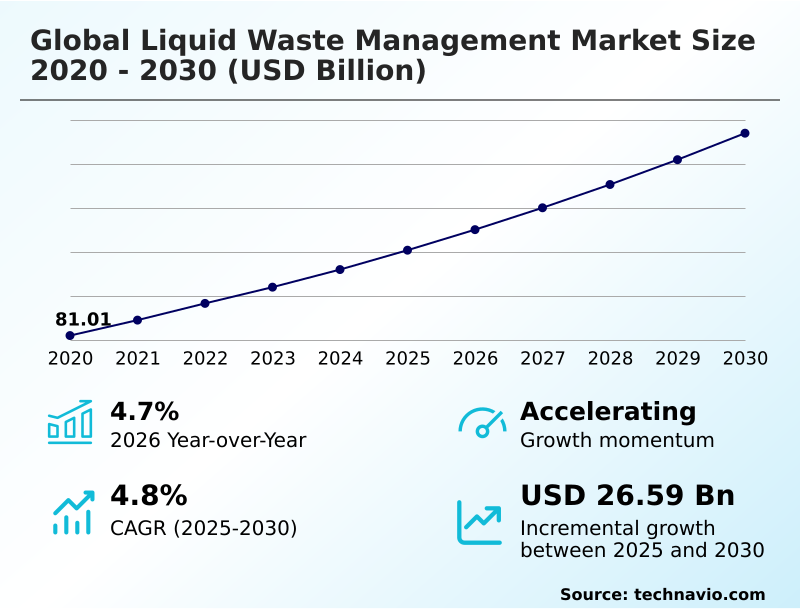

The Liquid Waste Management Market size was valued at USD 100.41 billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.5% growth during the forecast period.

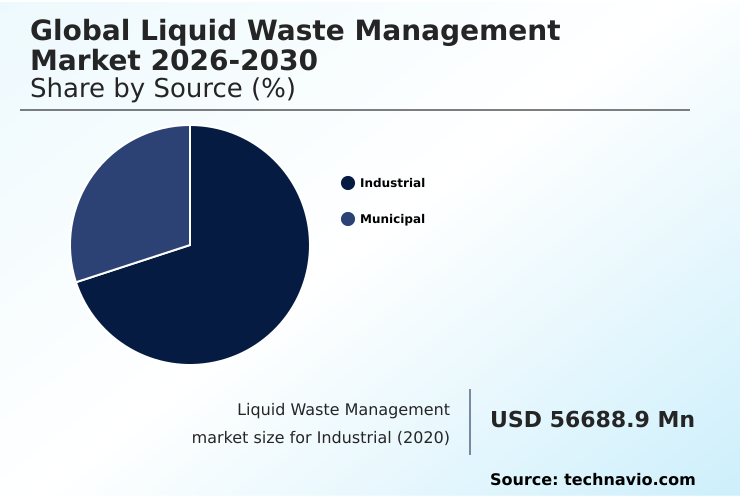

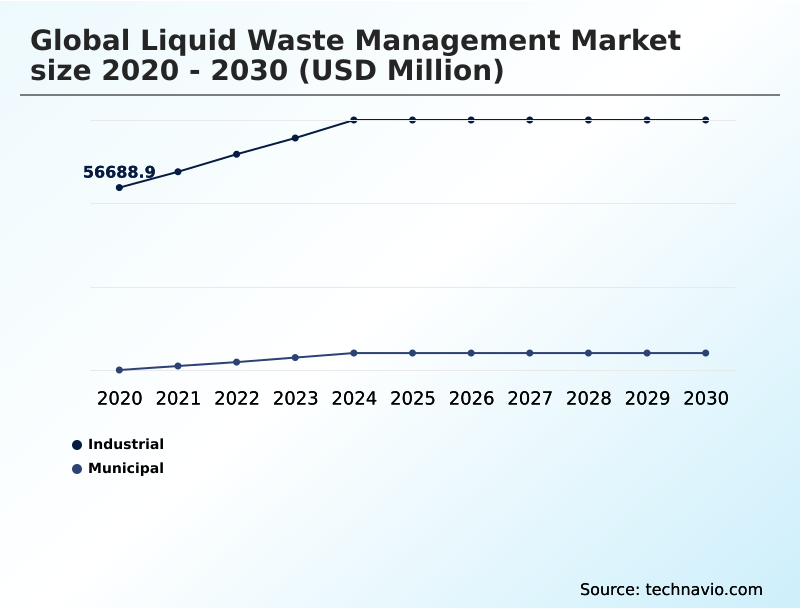

- By Source - Industrial segment was valued at USD 68.68 billion in 2024

- By Service - Treatment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 45.99 billion

- Market Future Opportunities 2025-2030: USD 26.59 billion

- CAGR from 2025 to 2030 : 4.8%

Market Summary

- The liquid waste management market is pivoting from a disposal-centric model to a resource-oriented framework, with modern facilities recovering over 95% of water for reuse. This transition is exemplified in manufacturing, where a facility manager implements a closed-loop system not just for compliance but to reduce operational dependency on freshwater sources, cutting water acquisition costs by over 40%.

- A primary driver is the global push for circularity, compelling industries to view wastewater as a source of valuable materials. However, this evolution is constrained by a significant challenge: the high energy consumption of advanced treatment methods.

- Technologies like reverse osmosis, while effective, can consume double the energy of conventional processes, creating a direct conflict with corporate carbon reduction goals and pressuring operators to balance environmental stewardship with financial viability.

What will be the Size of the Liquid Waste Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Liquid Waste Management Market Segmented?

The liquid waste management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Source

- Industrial

- Municipal

- Service

- Treatment

- Collection

- Transportation

- Disposal

- Material

- Non-hazardous

- Hazardous

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

How is the Liquid Waste Management Market Segmented by Source?

The industrial segment is estimated to witness significant growth during the forecast period.

The industrial segment, representing over 70% of liquid waste management services, is driven by stringent regulations for industrial wastewater.

This sector has shifted from disposal-centric models to resource recovery, with zero liquid discharge (ZLD) systems capable of reclaiming up to 95% of process water.

This transition is critical in sectors like pharmaceutical wastewater and textile industry effluent treatment, where complex pollutants necessitate advanced oxidation process technologies for effective breakdown.

Unlike municipal streams, industrial flows often require specialized on-site decentralized treatment systems for heavy metal removal and management of outputs from oil and gas produced water, making it a technology-intensive and high-value segment.

The use of granular activated carbon is also becoming standard for polishing final effluent before discharge or reuse.

The Industrial segment was valued at USD 68.68 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Liquid Waste Management market is rising in the leading region?

APAC is estimated to contribute 54.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Liquid Waste Management Market demand is rising in APAC Request Free Sample

APAC will contribute 54.5% of the global liquid waste management market's growth, a rate nearly 2.3 times that of North America.

This expansion is driven by rapid industrialization in China and India, where demand for new effluent treatment infrastructure is surging.

In contrast, the North American market, dominated by the US, focuses on upgrading aging activated sludge process plants and integrating advanced membrane bioreactor (MBR) technology to manage complex pollutants from established industries.

Adoption of MBR can increase nutrient removal efficiency by over 30% compared to conventional systems.

This regional divergence impacts the supply chain, with APAC requiring scalable, cost-effective solutions for high volumes of municipal sewage and industrial wastewater, while North America prioritizes specialized technologies for effluent polishing and biosolids management to meet stricter environmental standards.

What are the key Drivers, Trends, and Challenges in the Liquid Waste Management Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in liquid waste management requires a thorough evaluation of total lifecycle expenses, where the initial cost of zero liquid discharge implementation is weighed against long-term operational savings and regulatory compliance. For industrial facilities, deploying advanced oxidation for industrial wastewater can reduce chemical consumption by up to 25% compared to traditional methods, but it necessitates significant upfront capital.

- As urban areas expand, decentralized wastewater treatment for communities is emerging as a scalable alternative to expanding overburdened centralized plants, offering phased investment and faster deployment. A critical and growing concern is the development of effective PFAS removal technologies in liquid waste, as future regulations are expected to mandate near-complete elimination, making this a key area for R&D investment.

- Furthermore, the focus on circularity is elevating the importance of nutrient recovery from municipal sludge, transforming a waste byproduct into a marketable fertilizer, with some processes recovering over 90% of phosphorus. This shift reframes waste management from a cost center to a potential revenue-generating operation.

What are the key market drivers leading to the rise in the adoption of Liquid Waste Management Industry?

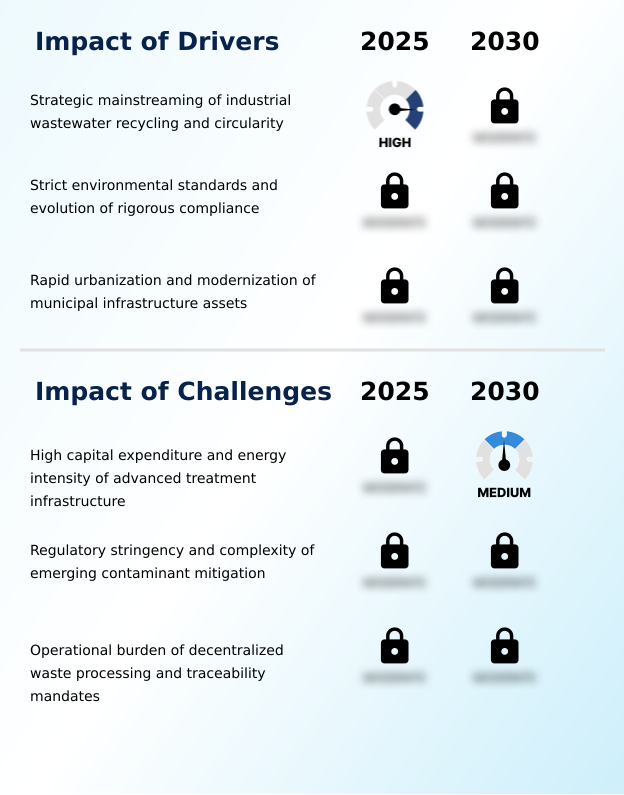

- The strategic mainstreaming of industrial wastewater recycling and the application of circular economy principles serve as a primary driver for the market.

- The adoption of circular economy principles is a primary driver, fundamentally changing how municipal sewage and hazardous liquid waste are managed.

- This shift is propelled by the need for water reclamation, with advanced systems recovering over 95% of wastewater for reuse in applications like industrial process water.

- Instead of being a disposal cost, effluent is now viewed as a source of valuable resources. Technologies such as coagulation-flocculation and electrocoagulation are being optimized for resource recovery, not just contaminant removal.

- The integration of process control automation further enhances efficiency, reducing chemical usage by 15-20% while ensuring consistent water quality. This driver reframes liquid waste management as a critical component of sustainable industrial operations and resilient urban water strategies.

What are the market trends shaping the Liquid Waste Management Industry?

- A key trend is the institutionalization of decentralized and modular treatment infrastructure. This shift addresses the need for flexible, scalable solutions at the point of waste generation.

- A significant trend shaping liquid waste management is the shift toward modular wastewater plants, which can be deployed in a fraction of the time compared to large-scale civil projects, reducing project timelines by up to 75%.

- These containerized, plug-and-play systems, often utilizing high-efficiency reverse osmosis (RO) and anaerobic digestion, address the need for agile and scalable solutions in rapidly growing industrial zones. This approach minimizes the physical footprint and allows for localized treatment and reuse, easing the burden on aging municipal infrastructure.

- The integration of a smart water grid with real-time monitoring further optimizes these decentralized networks, enhancing the efficiency of processes like sludge dewatering and management of landfill leachate treatment, ultimately supporting a more resilient and cost-effective sanitation model.

What challenges does the Liquid Waste Management Industry face during its growth?

- The high capital expenditure and significant energy intensity required for advanced treatment infrastructure present a key challenge to industry growth.

- A primary challenge confronting the liquid waste management market is the high energy intensity of advanced treatment systems, which can consume up to double the electricity of conventional methods. This escalates operational costs, particularly in regions with high energy prices, and creates a conflict with corporate sustainability goals aimed at reducing carbon footprints.

- For instance, processes essential for salinity management and nutrient removal, such as reverse osmosis and biological nutrient removal, are energy-intensive. Achieving stringent limits for biological oxygen demand (BOD) in complex waste from food processing wastewater often requires these advanced, high-cost technologies.

- The financial burden is particularly acute for small and medium-sized enterprises that lack the capital for such investments, limiting widespread adoption and posing a barrier to achieving higher environmental standards.

Exclusive Technavio Analysis on Customer Landscape

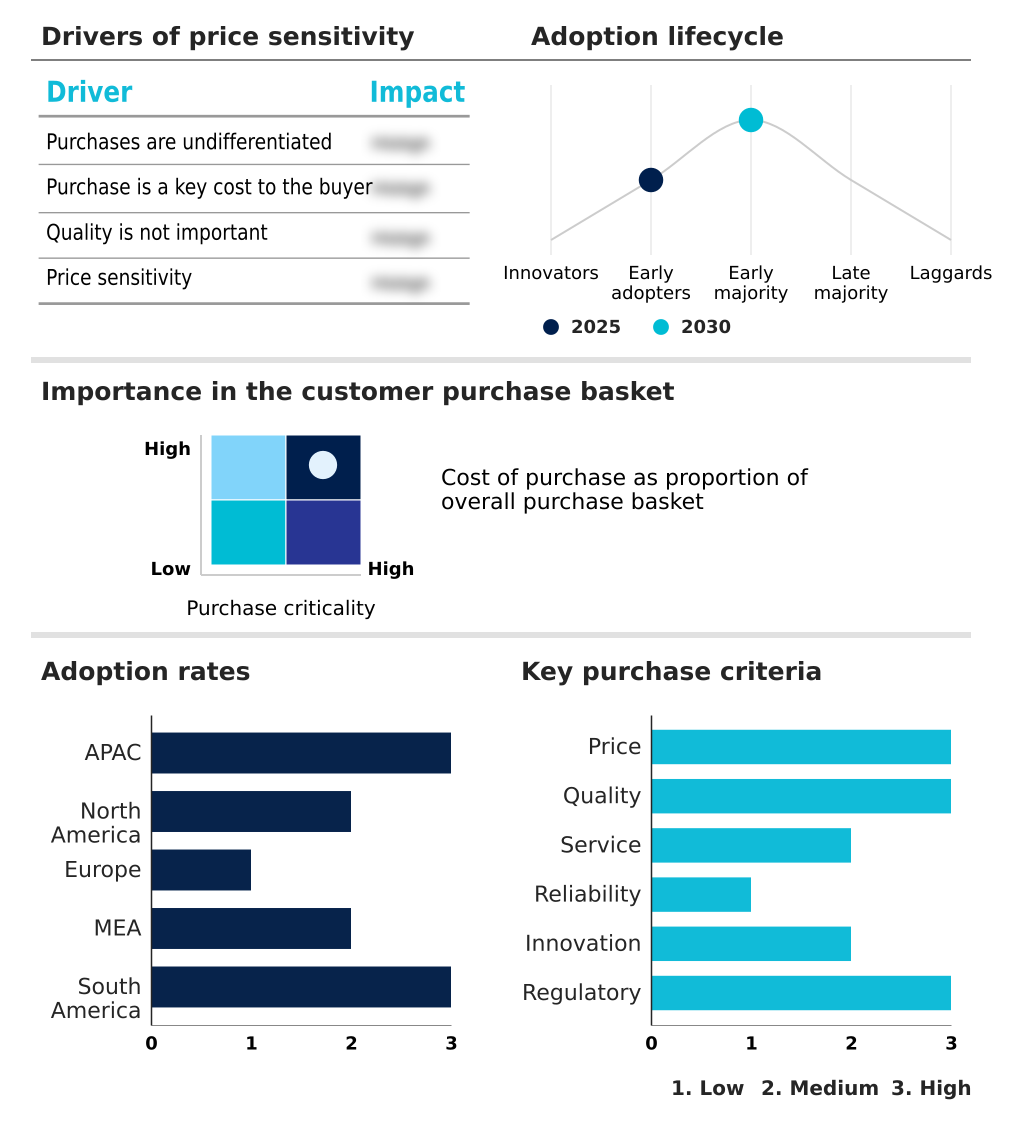

The liquid waste management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the liquid waste management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Liquid Waste Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, liquid waste management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Augean plc - Providers deliver comprehensive management solutions, including the collection, treatment, and disposal of hazardous and non-hazardous liquid waste for industrial and municipal clients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Augean plc

- Casella Waste Systems Inc.

- Clean Harbors Inc.

- Cleanaway Waste Management Ltd.

- Enva

- Enviri Corp.

- GFL Environmental Inc.

- Grupo Tradebe Medioambiente SL

- Heritage Crystal Clean Inc.

- Remondis SE and Co. KG

- Republic Services Inc.

- ReWorld Waste

- Seche Environnement SA

- SUEZ SA

- Veolia Environment SA

- Waste Management Inc.

- Whites Recycling Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Environmental and Facilities Services industry, the mainstreaming of circular economy principles is compelling a move beyond simple waste disposal. This directly impacts the liquid waste management market by driving demand for technologies that facilitate resource recovery and water reuse applications, turning treated effluent into a valuable commodity.

- The enforcement of stricter environmental regulations and pollutant discharge limits is fundamentally reshaping operational requirements. For the liquid waste management market, this translates to increased investment in advanced treatment technologies capable of heavy metal removal and organic pollutant degradation to ensure compliance.

- A growing trend toward outsourcing non-core operations has expanded the addressable market for third-party service providers. This directly benefits the liquid waste management sector as industrial and municipal entities seek specialized expertise for complex wastewater challenges, including biosolids management and effluent polishing.

- Digital transformation, including the adoption of IoT for real-time monitoring and process control automation, is enhancing operational efficiency. In liquid waste management, this allows for optimized chemical dosing, predictive maintenance of equipment, and improved management of decentralized treatment systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Liquid Waste Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2026-2030 | USD 26592.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The liquid waste management market ecosystem involves a complex interplay of stakeholders, where technology suppliers provide critical components like membranes and chemical coagulants that enable service providers to manage industrial and municipal waste streams. Industrial end-users, comprising over 70% of the market, are the primary revenue source, driven by regulatory bodies that enforce stringent effluent discharge standards.

- These regulations, in turn, spur innovation in R&D entities focused on developing more efficient treatment processes. For instance, advanced systems can reduce specific contaminants by over 99%, a benchmark often required for discharge permits.

- Logistics and distribution channels, including specialized tanker fleets, are essential for the collection and transport of waste to centralized treatment facilities, completing a value chain centered on compliance and environmental protection.

What are the Key Data Covered in this Liquid Waste Management Market Research and Growth Report?

-

What is the expected growth of the Liquid Waste Management Market between 2026 and 2030?

-

The Liquid Waste Management Market is expected to grow by USD 26.59 billion during 2026-2030, registering a CAGR of 4.8%. Year-over-year growth in 2026 is estimated at 4.7%%. This acceleration is shaped by strategic mainstreaming of industrial wastewater recycling and circularity, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Source (Industrial, and Municipal), Service (Treatment, Collection, Transportation, and Disposal), Material (Non-hazardous, and Hazardous) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Industrial segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 54.5% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is strategic mainstreaming of industrial wastewater recycling and circularity, which is accelerating investment and industry demand. The main challenge is high capital expenditure and energy intensity of advanced treatment infrastructure, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Liquid Waste Management Market?

-

Key vendors include Augean plc, Casella Waste Systems Inc., Clean Harbors Inc., Cleanaway Waste Management Ltd., Enva, Enviri Corp., GFL Environmental Inc., Grupo Tradebe Medioambiente SL, Heritage Crystal Clean Inc., Remondis SE and Co. KG, Republic Services Inc., ReWorld Waste, Seche Environnement SA, SUEZ SA, Veolia Environment SA, Waste Management Inc. and Whites Recycling Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The liquid waste management market's competitive landscape is consolidated, with the top five players accounting for over 45% of industry revenue. This environment is shaped by strategic actions aimed at technological leadership and geographic expansion. For instance, key vendors are heavily investing in proprietary PFAS destruction technologies that achieve over 99% elimination rates, directly responding to tightening regulatory controls.

- These innovations address urgent enterprise needs for compliance and risk mitigation in handling hazardous liquid waste. Other companies are expanding their footprint in emerging markets through acquisitions, gaining access to high-growth industrial sectors.

- However, the operational complexity and high capital cost of scaling these advanced treatment solutions remain a persistent challenge, forcing firms to balance innovation with cost-effective service delivery to maintain market share.

We can help! Our analysts can customize this liquid waste management market research report to meet your requirements.

RIA -

RIA -