US Lithium-ion Battery Recycling Market Size 2026-2030

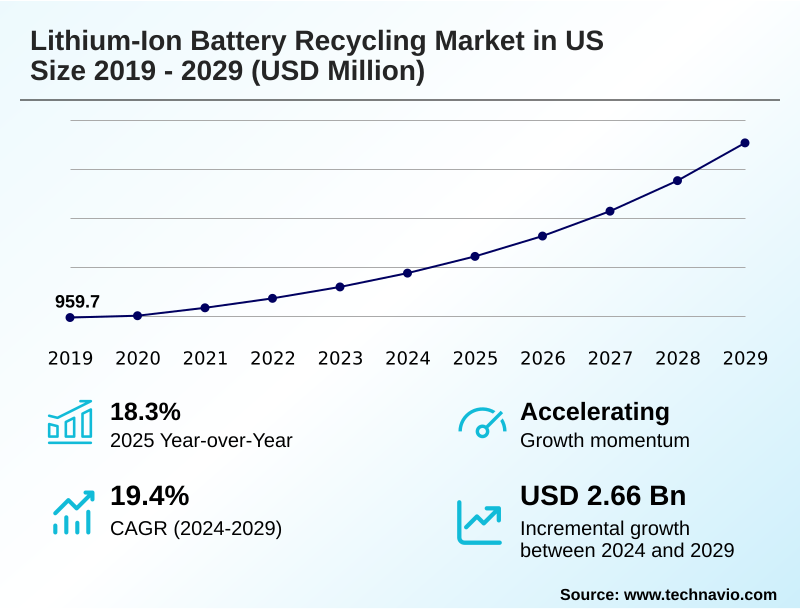

The us lithium-ion battery recycling market size is valued to increase by USD 3.42 billion, at a CAGR of 20.5% from 2025 to 2030. Imperative for supply chain sovereignty and critical mineral independence will drive the us lithium-ion battery recycling market.

Major Market Trends & Insights

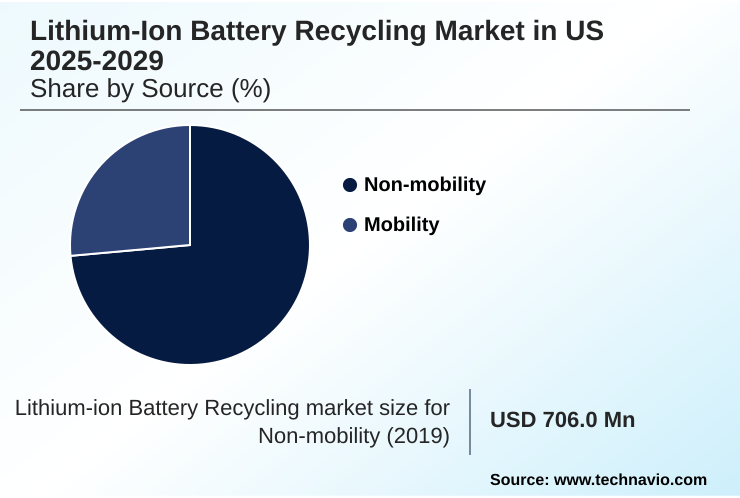

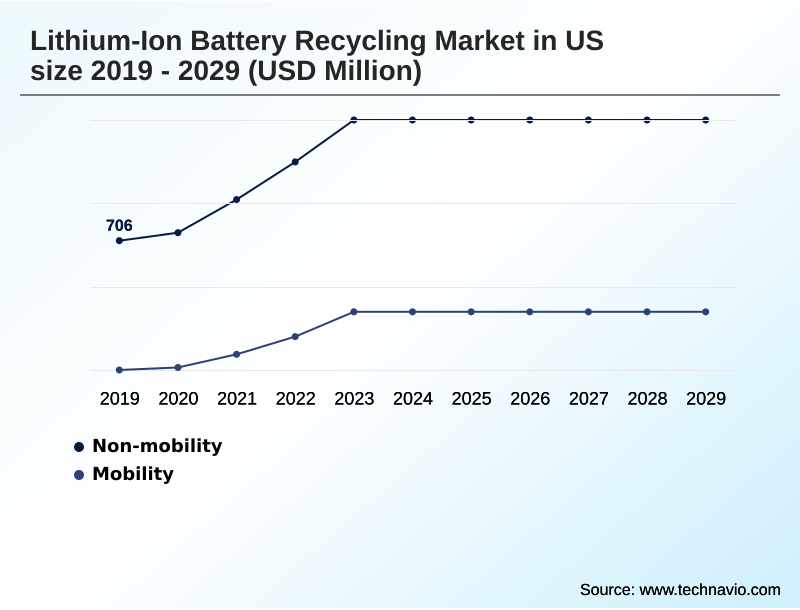

- By Source - Non-mobility segment was valued at USD 1.28 billion in 2024

- By Type - Hydrometallurgical segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.63 billion

- Market Future Opportunities: USD 3.42 billion

- CAGR from 2025 to 2030 : 20.5%

Market Summary

- The lithium-ion battery recycling market in US is undergoing a significant transformation, driven by the dual imperatives of environmental stewardship and the strategic need for domestic supply chain resilience. As the adoption of electric vehicles and stationary energy storage systems (ESS) accelerates, a substantial volume of end-of-life (EOL) battery management challenges and opportunities emerges.

- The industry is moving beyond nascent technologies toward scalable hydrometallurgical processing and pyrometallurgical methods designed for high-yield critical mineral recovery. This evolution is critical for establishing a circular economy where materials like lithium, cobalt, and nickel are perpetually reintroduced into the supply chain.

- For instance, an EV manufacturer can establish a closed-loop supply chain by partnering with a recycler to process its manufacturing scrap and EOL batteries.

- This strategy not only ensures compliance with emerging recycled content mandates but also provides a hedge against the mineral price volatility impact, securing a stable supply of secondary raw materials like precursor cathode active materials (pCAM) and battery-grade metal salts for new battery production.

- This integrated approach transforms a waste stream into a strategic asset, reinforcing supply chain sovereignty and reducing dependence on foreign material processing.

What will be the Size of the US Lithium-ion Battery Recycling Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Lithium-ion Battery Recycling Market Segmented?

The us lithium-ion battery recycling industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Source

- Non-mobility

- Mobility

- Type

- Hydrometallurgical

- Pyrometallurgical

- Mechanical separation

- Others

- Product type

- LiCoO2 battery

- NMC battery

- LiFePO4 battery

- Others

- Geography

- North America

- US

- North America

By Source Insights

The non-mobility segment is estimated to witness significant growth during the forecast period.

The non-mobility segment, comprising consumer electronics and stationary energy storage systems (ESS), serves as a foundational source of urban mining feedstock.

Historically, the high concentration of cobalt in lithium cobalt oxide (LCO) batteries from electronics provided significant value, though this is shifting with the rise of low-cobalt battery chemistries.

Effective consumer electronics collection remains a logistical challenge, necessitating efficient hazardous waste logistics to manage dispersed end-of-life products.

In contrast, the decommissioning of large-scale ESS installations presents different complexities, often requiring advanced battery dismantling automation before materials undergo processes like pyrometallurgical smelting or mechanical separation.

To manage costs, some recyclers have implemented gate fee pricing models, ensuring operational viability. Advanced sorting systems now achieve over 95% accuracy in identifying battery chemistries, improving downstream processing efficiency.

The Non-mobility segment was valued at USD 1.28 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the industry increasingly hinge on the technical and economic trade-offs between different recycling pathways. The debate over hydrometallurgical vs pyrometallurgical efficiency is central, as companies weigh recovery rates against energy consumption and capital costs.

- A key consideration is the challenge of recycling LFP versus NMC batteries, as the lower intrinsic value of LFP chemistries alters the entire black mass value proposition analysis. This directly influences the cost of recycling lithium-ion batteries and forces operators to innovate to remain profitable, especially given the impact of cobalt price on recycling revenues from higher-value streams.

- Furthermore, navigating regulatory compliance for battery transport and improving battery collection logistics are persistent operational hurdles. Investment in automation in battery dismantling process is seen as a solution to enhance safety and throughput. Automakers are pursuing closed-loop recycling for EV manufacturers to secure supply chains and achieve sustainability targets, driving demand for pCAM production from recycled materials.

- This mitigates supply chain risk in battery recycling and fosters innovation in areas like new technologies for lithium recovery from slag. As the industry scales, the environmental impact of battery recycling is under scrutiny, compelling firms to adopt best practices and publish clear safety protocols for handling EOL batteries.

- The economics of recycling consumer electronics batteries are being reassessed, contributing to the broader effort of scaling up battery recycling infrastructure. The role of AI in sorting battery chemistries is emerging as a critical enabler, alongside improved methods for separating anode and cathode materials and developing new end-of-life solutions for energy storage.

- Ultimately, these efforts are building viable circular economy models for EV batteries, transforming a complex waste stream into a sustainable resource. In this context, integrated firms show a logistical cost advantage of nearly two-to-one compared to those using fragmented, multi-stage processing networks.

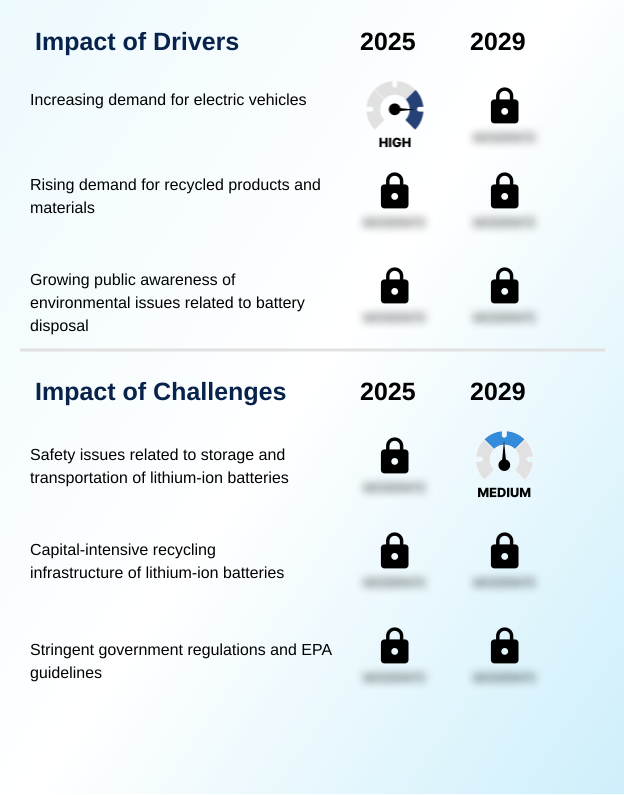

What are the key market drivers leading to the rise in the adoption of US Lithium-ion Battery Recycling Industry?

- The primary market driver is the national strategic imperative to establish supply chain sovereignty and achieve critical mineral independence.

- The drive for supply chain sovereignty is accelerating investment in domestic critical mineral recovery capabilities. A primary focus is on manufacturing scrap recycling, which currently constitutes over 70% of the feedstock for many new facilities.

- The execution of long-term offtake agreements ensures a stable market for products like battery-grade metal salts and supports sustainable precursor production. Advanced hydrometallurgical refining plants, utilizing improved solvent extraction technology, are central to building domestic supply chain resilience.

- These facilities can produce high-purity precursor cathode active materials (pCAM) with recovery rates exceeding 95% for key metals, directly competing with and often surpassing the efficiency of established international processors.

What are the market trends shaping the US Lithium-ion Battery Recycling Industry?

- A dominant market trend is the strategic transition toward vertically integrated operations and co-located industrial ecosystems. This shift aims to consolidate the recycling value chain and reduce logistical complexities.

- A pivotal trend is the move away from the traditional spoke and hub collection model toward integrated gigafactory co-location. This approach facilitates closed-loop manufacturing and supports ambitious recycled content mandates. Advanced direct recycling technology is gaining traction, enabling cathode-to-cathode recycling, which can improve material recovery efficiency by up to 15% compared to conventional methods.

- This integration minimizes transportation risks and enhances thermal runaway prevention protocols. Some facilities report a 20% reduction in logistical costs by processing manufacturing scrap on-site. The focus on direct reuse is also expanding opportunities for second-life battery applications before end-of-life processing, creating a more holistic circular model.

What challenges does the US Lithium-ion Battery Recycling Industry face during its growth?

- A key market challenge stems from economic volatility and significant fluctuations in raw material prices, which directly impact the viability of recycling operations.

- The significant mineral price volatility impact remains a primary market challenge, complicating the economics of end-of-life (EOL) battery management. The increasing prevalence of lithium iron phosphate (LFP) chemistry in the feedstock mix, which offers lower intrinsic value, has compressed recycler margins by as much as 30% in some cases. This necessitates precise feedstock composition analysis to optimize processing batches.

- Furthermore, stringent regulations for the transportation of dangerous goods (TDG) increase operational costs by 15-20% and can delay recycling plant commissioning. While extended producer responsibility (EPR) policies aim to improve collection, the economic viability of processing low-value materials using capital-intensive pyrometallurgical methods continues to be a significant hurdle.

Exclusive Technavio Analysis on Customer Landscape

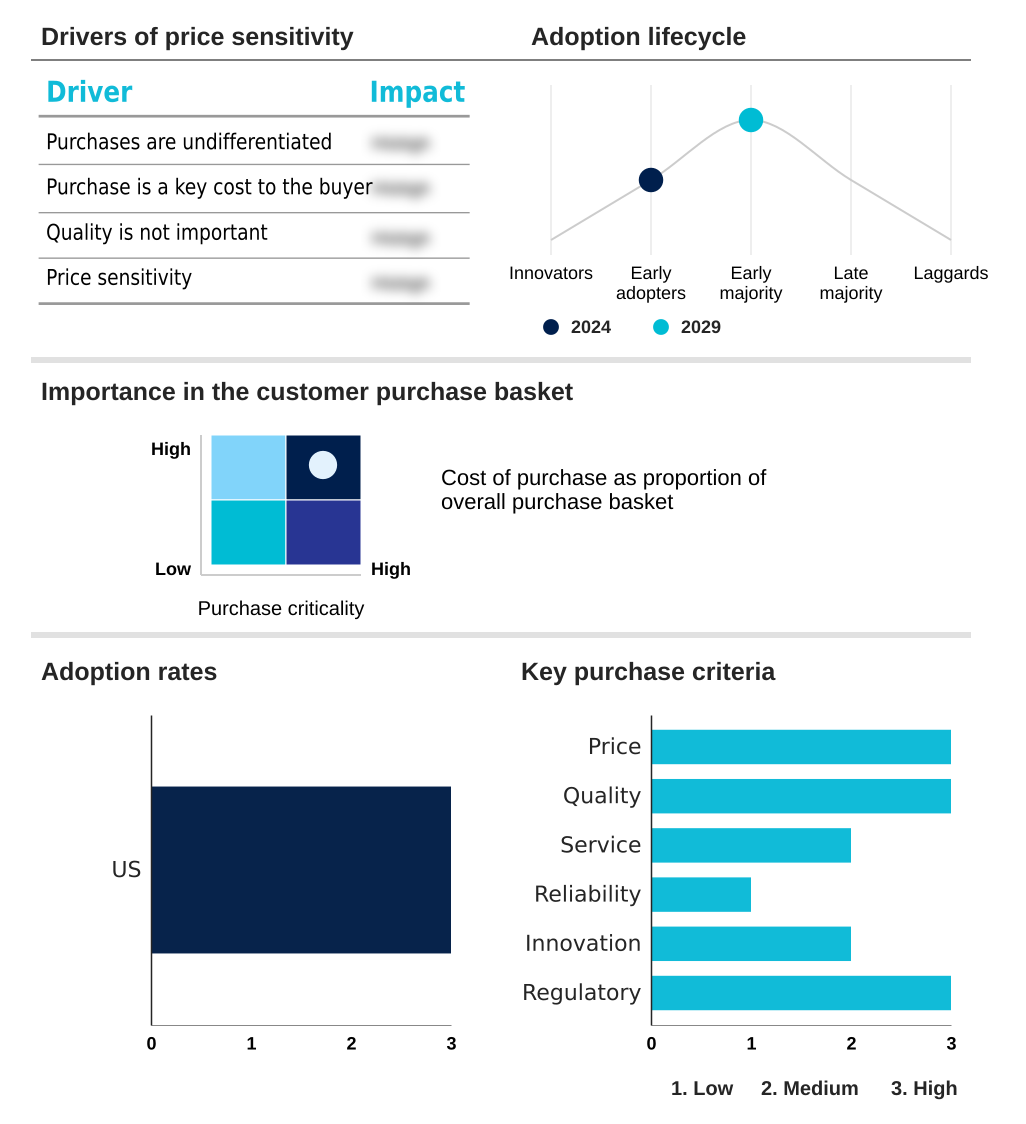

The us lithium-ion battery recycling market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us lithium-ion battery recycling market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Lithium-ion Battery Recycling Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us lithium-ion battery recycling market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Battery Technology Co. - Analysis indicates a focus on platform-based solutions designed to scale the production of primary metals essential for advanced battery applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Battery Technology Co.

- American Zinc Recycling

- Aqua Metals Inc.

- Ascend Elements Inc.

- Battery Recyclers of America

- Call2Recycle Inc.

- Exxon Mobil Corp.

- Green Li-ion Pte Ltd.

- Lohum Cleantech Pvt. Ltd.

- Onto Technology LLC

- Raw Materials Co. Inc.

- Redwood Materials Inc.

- RENEWANCE

- Retriev Technologies

- SMS group GmbH

- Total Reclaim

- Umicore SA

- Vesco Clean Energy LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us lithium-ion battery recycling market

- In August 2025, Ascend Elements formally commissioned the final phase of its Apex 1 facility in Hopkinsville, Kentucky, integrating battery recycling directly with the production of sustainable precursor cathode active materials.

- In October 2025, Redwood Materials secured USD 350 million in Series E funding to expand its operations in Nevada and South Carolina, enhancing critical mineral recovery and domestic battery material production.

- In November 2025, American Battery Technology Company received formal approval from the United States Environmental Protection Agency to receive and recycle hazardous lithium-ion batteries from large-scale energy storage systems.

- In July 2025, Cirba Solutions announced the execution of a long-term offtake agreement with a major domestic manufacturer for battery-grade metal salts, demonstrating the maturation of domestic supply chains.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Lithium-ion Battery Recycling Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 179 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.5% |

| Market growth 2026-2030 | USD 3415.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.0% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly maturing from pilot projects to industrial-scale operations centered on sophisticated hydrometallurgical processing and, to a lesser extent, pyrometallurgical methods. The primary goal is efficient critical mineral recovery from a diverse urban mining feedstock, including both manufacturing scrap recycling and complex end-of-life (EOL) battery management streams.

- A key focus is the refinement of black mass to produce high-value secondary raw materials, such as precursor cathode active materials (pCAM) and battery-grade metal salts. Decision-making at the executive level is heavily influenced by recycled content mandates, which necessitate investments in advanced solvent extraction technology and mechanical separation processes to maximize material recovery efficiency.

- As feedstock composition analysis becomes more critical with the rise of lithium iron phosphate (LFP) chemistry alongside traditional lithium cobalt oxide (LCO) and nickel manganese cobalt (NMC) types, facilities are investing in battery dismantling automation. This pivot addresses both hazardous waste logistics and thermal runaway prevention, with some automated systems increasing dismantling throughput by 30% over manual methods.

- The entire ecosystem is moving toward a closed-loop supply chain, shifting away from the fragmented spoke and hub collection model.

What are the Key Data Covered in this US Lithium-ion Battery Recycling Market Research and Growth Report?

-

What is the expected growth of the US Lithium-ion Battery Recycling Market between 2026 and 2030?

-

USD 3.42 billion, at a CAGR of 20.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Source (Non-mobility, and Mobility), Type (Hydrometallurgical, Pyrometallurgical, Mechanical separation, and Others), Product Type (LiCoO2 battery, NMC battery, LiFePO4 battery, and Others) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Imperative for supply chain sovereignty and critical mineral independence, Economic volatility and raw material price fluctuations

-

-

Who are the major players in the US Lithium-ion Battery Recycling Market?

-

American Battery Technology Co., American Zinc Recycling, Aqua Metals Inc., Ascend Elements Inc., Battery Recyclers of America, Call2Recycle Inc., Exxon Mobil Corp., Green Li-ion Pte Ltd., Lohum Cleantech Pvt. Ltd., Onto Technology LLC, Raw Materials Co. Inc., Redwood Materials Inc., RENEWANCE, Retriev Technologies, SMS group GmbH, Total Reclaim, Umicore SA and Vesco Clean Energy LLC

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for domestic supply chain resilience and adherence to circular economy principles. Gigafactory co-location with recycling facilities is a key strategy, reducing scrap logistics costs by over 20% and improving the efficiency of closed-loop manufacturing. The implementation of chain-of-custody verification systems is becoming standard practice, ensuring compliance with extended producer responsibility (EPR) regulations.

- As the market adapts to low-cobalt battery chemistries, new hydrometallurgical refining processes are achieving over 95% recovery rates for critical metals. The execution of long-term offtake agreements has also become crucial, securing revenue streams and de-risking the significant capital investment required for recycling plant commissioning, thereby stabilizing the urban resource harvesting ecosystem against mineral price volatility.

We can help! Our analysts can customize this us lithium-ion battery recycling market research report to meet your requirements.

RIA -

RIA -