Machine Learning (ML) Platforms Market Size 2025-2029

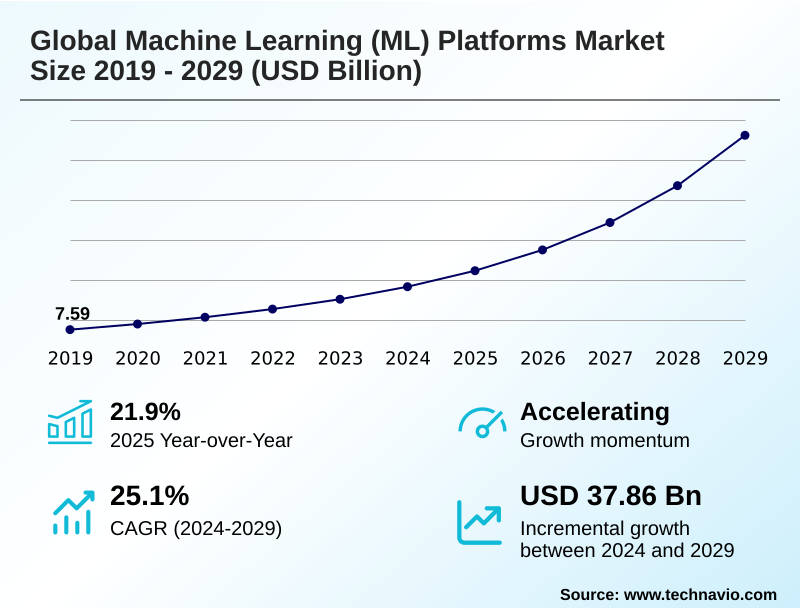

The machine learning (ml) platforms market size is valued to increase by USD 37.86 billion, at a CAGR of 25.1% from 2024 to 2029. Escalating volume and complexity of data will drive the machine learning (ml) platforms market.

Major Market Trends & Insights

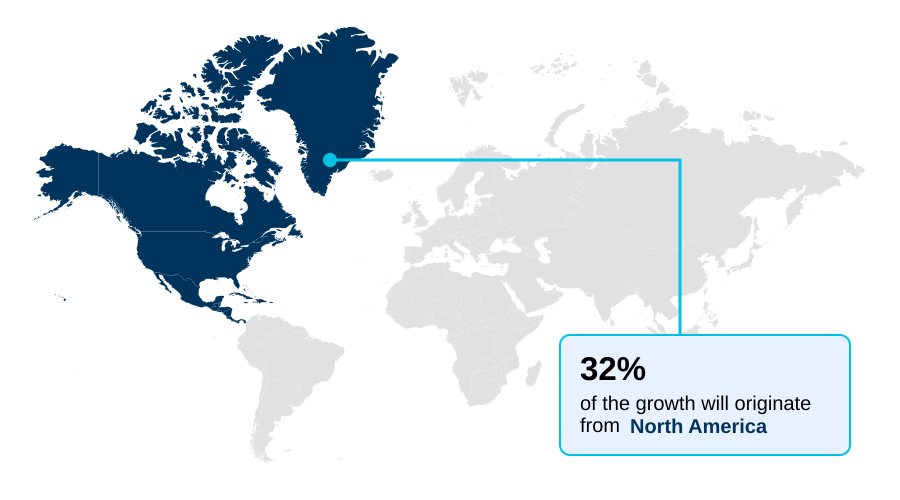

- North America dominated the market and accounted for a 32.5% growth during the forecast period.

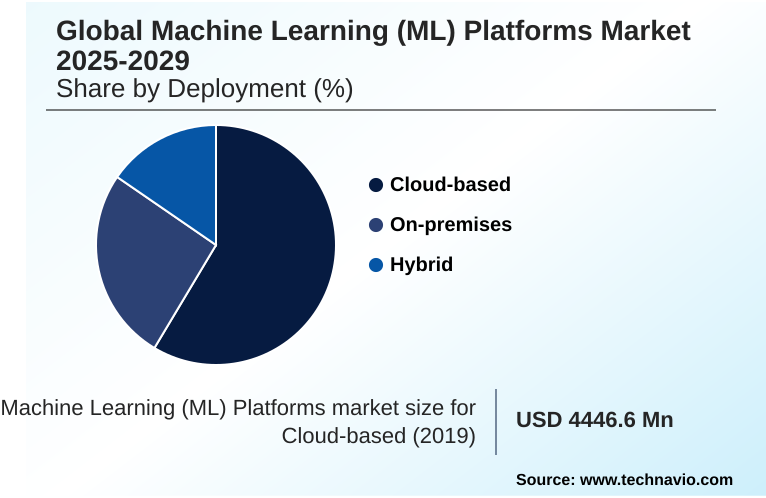

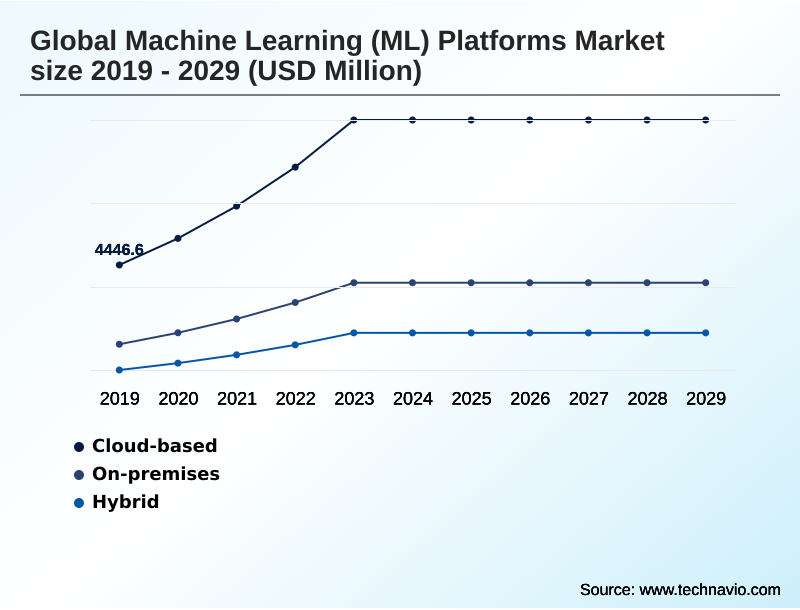

- By Deployment - Cloud-based segment was valued at USD 8.97 billion in 2023

- By Application - Predictive analytics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 48.59 billion

- Market Future Opportunities: USD 37.86 billion

- CAGR from 2024 to 2029 : 25.1%

Market Summary

- The machine learning (ML) platforms market is expanding as organizations prioritize data-driven decision-making. A primary driver is the explosion of big data, which necessitates sophisticated tools to extract actionable insights. These platforms provide the infrastructure for the end-to-end ml lifecycle, from data preprocessing and feature engineering to model deployment and monitoring.

- A key trend is the integration of generative and predictive ai, enabling applications capable of creating novel content and forecasting future outcomes. In manufacturing, for instance, a company can implement machine learning for predictive maintenance by analyzing sensor data to anticipate equipment failures, reducing downtime and operational costs.

- However, the market's progress is moderated by challenges such as the persistent scarcity of skilled data scientists and engineers. Furthermore, concerns regarding data governance and the need for responsible ai frameworks that ensure fairness and model explainability are becoming central to enterprise adoption strategies, shaping platform development to include robust tools for compliance and ethical oversight.

- The shift towards MLOps is also critical, as it operationalizes AI at scale, ensuring models remain accurate and reliable in production environments.

What will be the Size of the Machine Learning (ML) Platforms Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Machine Learning (ML) Platforms Market Segmented?

The machine learning (ml) platforms industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Application

- Predictive analytics

- Computer vision

- Natural language processing

- Recommendation systems

- Others

- End-user

- BFSI

- Healthcare and life science

- Retail and e-commerce

- Manufacturing

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based deployment model is the cornerstone of the machine learning platforms market, offering organizations unmatched scalability and flexibility. This model provides pay-as-you-go access to vast computational resources, including GPU acceleration and tensor processing units, essential for complex model training.

It democratizes AI, enabling businesses to leverage automated machine learning and no-code model building tools without prohibitive upfront investment in physical hardware.

Cloud platforms deliver a fully managed, end-to-end ml lifecycle, integrating seamlessly with other data and analytics services to create a cohesive workflow.

By abstracting infrastructure complexities, these cloud-native solutions allow teams to focus on innovation, with some platforms improving model deployment efficiency by over 40%.

The approach provides a scalable ml infrastructure that supports everything from initial data exploration to production-level serverless computing.

The Cloud-based segment was valued at USD 8.97 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Machine Learning (ML) Platforms Market Demand is Rising in North America Get Free Sample

The geographic landscape of the machine learning platforms market is led by North America, which accounts for over 32% of the incremental growth, driven by its mature technology ecosystem and high adoption rates.

The region's leadership is anchored in its widespread use of computer vision for industrial automation and recommendation systems in e-commerce.

Following this, APAC is the fastest-growing region, with countries like China and India leveraging large language models and other foundational models for digital services at an unprecedented scale.

Europe's market is distinguished by a strong focus on industrial applications and regulatory leadership in responsible AI. Key applications gaining traction globally include natural language processing for customer service and reinforcement learning for autonomous systems.

Platforms are also enhancing capabilities like data annotation and streamlined model deployment to support these diverse use cases.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategically navigating the machine learning platforms market requires a deep understanding of both opportunities and operational costs. A primary consideration is the total cost of training large models, which can be substantial. Effective management involves not only building and deploying ml models but also managing the entire model lifecycle to ensure long-term value.

- For industrial firms, implementing machine learning for predictive maintenance can yield significant ROI, often reducing unplanned downtime by more than half compared to traditional methods. Similarly, in finance, leveraging AI for algorithmic trading and automating fraud detection processes are now standard practices for maintaining a competitive edge.

- The ability to fine-tune models on proprietary data is a key differentiator, allowing businesses to create unique solutions. For consumer-facing applications, building intelligent chatbot applications and providing real-time model serving capabilities are essential for user engagement. In specialized sectors, AI for medical image analysis and optimizing semiconductor fabrication processes demonstrate the technology's deep impact.

- Broader applications like ML for supply chain optimization and AI for public utility management showcase its versatility. Success hinges on ensuring data quality and consistency, integrating models into existing workflows, and monitoring model performance in production while detecting and mitigating model bias.

- Adherence to compliance with data privacy regulations is non-negotiable, and platforms that focus on reducing model deployment time while automating complex creative analytical tasks provide a distinct advantage.

What are the key market drivers leading to the rise in the adoption of Machine Learning (ML) Platforms Industry?

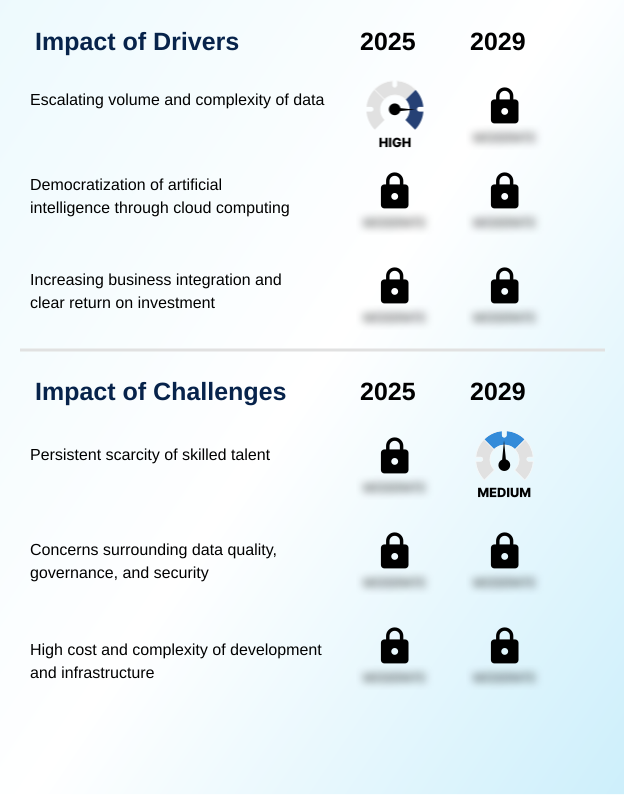

- The escalating volume and complexity of data across industries is a primary driver for the adoption of machine learning platforms.

- The primary driver for the machine learning platforms market is the imperative to transform vast data reservoirs into strategic assets.

- Organizations are leveraging these platforms for advanced predictive analytics, which can improve forecasting accuracy by over 25% compared to traditional methods. The process begins with rigorous data preprocessing and feature engineering, which are streamlined by modern data science workflows.

- The integration of deep learning models enables solutions that were previously unattainable. Furthermore, the availability of open-source data science tools and enterprise AI suites lowers the barrier to entry, while AI-driven iPaaS solutions simplify complex integrations.

- By utilizing techniques such as hyperparameter tuning within generative and predictive AI frameworks, businesses can optimize model performance, turning raw data into a decisive competitive advantage across various industries.

What are the market trends shaping the Machine Learning (ML) Platforms Industry?

- The mainstream adoption of MLOps is emerging as a critical market trend, focusing on standardizing and automating the machine learning lifecycle for production environments.

- The machine learning platforms market is increasingly shaped by the mainstream adoption of MLOps. This trend focuses on bringing discipline to the full lifecycle ml, from development to the production environment. By implementing MLOps, organizations can achieve a 30% reduction in the time it takes to move models from research to live applications.

- A core component is continuous monitoring, which is crucial for detecting model drift and ensuring sustained performance. This systematic approach, supported by robust model monitoring and model versioning tools, helps maintain model accuracy over time.

- Consequently, businesses are prioritizing platforms that offer integrated automated pipelines and facilitate custom model development, ensuring that AI initiatives are not only innovative but also reliable and scalable within their operational frameworks.

What challenges does the Machine Learning (ML) Platforms Industry face during its growth?

- A persistent scarcity of skilled talent presents a key challenge, potentially constraining the industry's growth trajectory.

- A significant challenge facing the machine learning platforms market is the complexity surrounding data governance and the growing demand for responsible AI. Navigating the landscape of compliance with data privacy regulations requires platforms with strong AI governance and observability features. For high-stakes applications, model auditability is non-negotiable, and platforms must offer clear model explainability to build trust.

- Organizations are investing in secure, scalable generative AI that can be fine-tuned while protecting sensitive information, with some firms seeing a 20% improvement in risk mitigation through better governance. The use of a model gateway for controlled access to various foundational models is becoming a standard security practice.

- Furthermore, the technical difficulty of detecting and mitigating model bias and applying advanced techniques like collaborative filtering without introducing fairness issues remains a critical hurdle for widespread, ethical AI adoption.

Exclusive Technavio Analysis on Customer Landscape

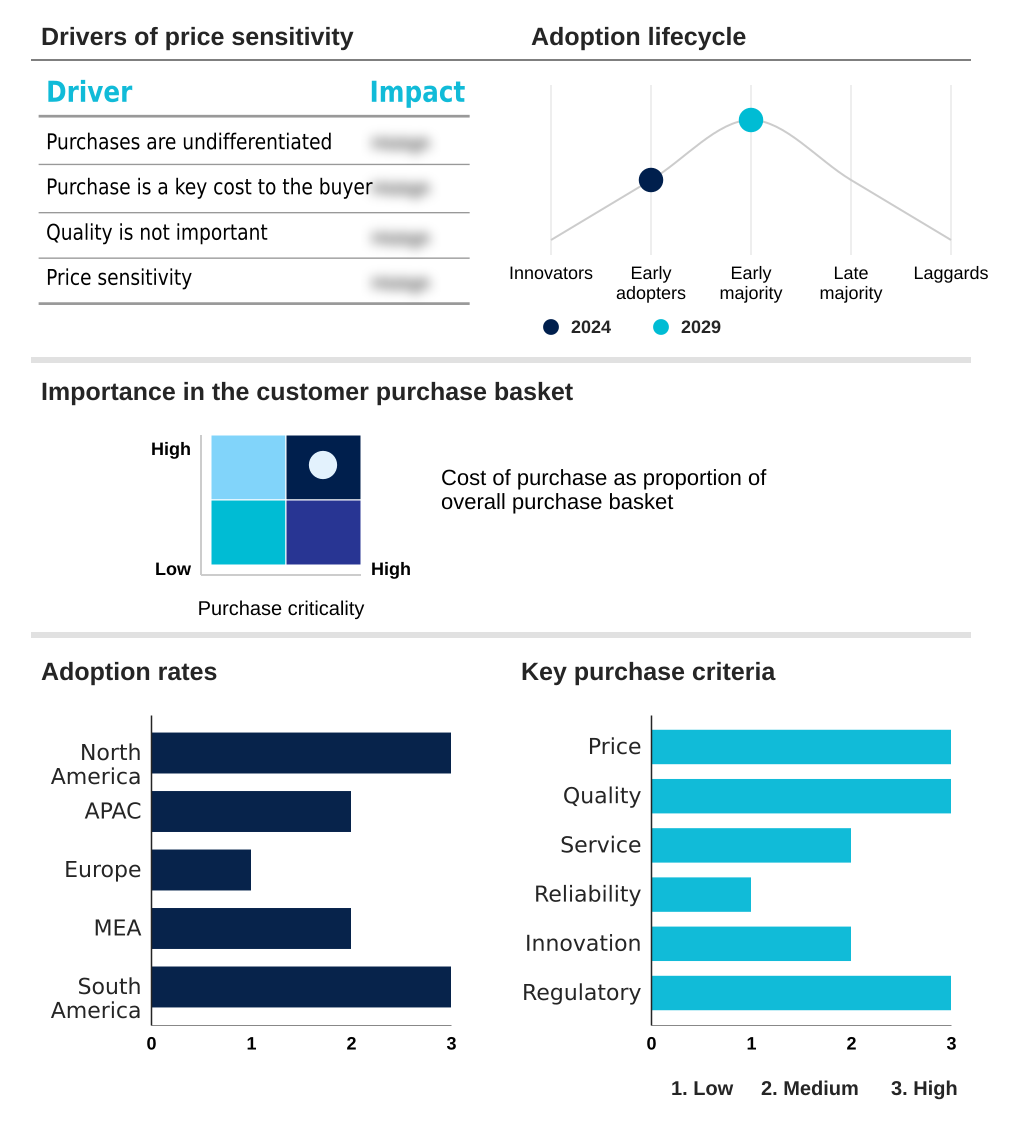

The machine learning (ml) platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the machine learning (ml) platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Machine Learning (ML) Platforms Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, machine learning (ml) platforms market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altair Engineering Inc. - Offerings include integrated platforms that streamline the complete machine learning lifecycle, from data preparation and model development to deployment, monitoring, and governance in enterprise environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altair Engineering Inc.

- Alteryx Inc.

- Amazon Web Services Inc.

- Anaconda Inc.

- Baidu Inc.

- Databricks Inc.

- DataRobot Inc.

- Google LLC

- H2O.ai Inc.

- Hugging Face

- Intel Corp.

- IBM Corp.

- KNIME AG

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- SAP SE

- SAS Institute Inc.

- The MathWorks Inc.

- TIBCO Software Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Machine learning (ml) platforms market

- In August, 2024, Google LLC announced the general availability of its advanced multimodal model, Gemini Pro, directly within its Vertex AI platform, allowing developers to leverage state-of-the-art generative AI capabilities within a managed, scalable environment.

- In November, 2024, Amazon Web Services Inc. announced the general availability of Amazon Bedrock, a fully managed service that provides businesses with access to a range of high-performing foundation models from leading AI companies through a single API.

- In January, 2025, Snowflake Inc. announced the general availability of Snowflake Cortex, a fully managed service providing businesses with access to large language models and advanced AI capabilities directly within the Snowflake Data Cloud.

- In May, 2025, The Council of the European Union granted its final approval to the landmark Artificial Intelligence Act, imposing stringent requirements on AI systems based on their risk level, mandating rigorous data governance, transparency, and human oversight.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Machine Learning (ML) Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.1% |

| Market growth 2025-2029 | USD 37859.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 21.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The machine learning platforms market is defined by the enterprise-wide push to operationalize AI, moving beyond experimentation to scalable production. This shift necessitates comprehensive tools that manage everything from initial data preprocessing and feature engineering to final model deployment and versioning.

- Key technologies like AutoML, deep learning models, and reinforcement learning are becoming standard, while the rise of large language models and other foundational models is creating new application frontiers. For boardroom consideration, the adoption of responsible AI principles is paramount, as robust data governance and model explainability are now critical for regulatory compliance and maintaining customer trust.

- For example, platforms offering clear model auditability can reduce compliance-related risks by over 50%. The discipline of MLOps is central to this evolution, with its focus on automated pipelines and continuous monitoring to combat model drift.

- Success depends on leveraging cloud-native solutions that provide access to GPU acceleration and tensor processing units, enabling efficient development of predictive analytics, natural language processing, computer vision, and recommendation systems using techniques like collaborative filtering.

What are the Key Data Covered in this Machine Learning (ML) Platforms Market Research and Growth Report?

-

What is the expected growth of the Machine Learning (ML) Platforms Market between 2025 and 2029?

-

USD 37.86 billion, at a CAGR of 25.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises, and Hybrid), Application (Predictive analytics, Computer vision, Natural language processing, Recommendation systems, and Others), End-user (BFSI, Healthcare and life science, Retail and e-commerce, Manufacturing, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating volume and complexity of data, Persistent scarcity of skilled talent

-

-

Who are the major players in the Machine Learning (ML) Platforms Market?

-

Altair Engineering Inc., Alteryx Inc., Amazon Web Services Inc., Anaconda Inc., Baidu Inc., Databricks Inc., DataRobot Inc., Google LLC, H2O.ai Inc., Hugging Face, Intel Corp., IBM Corp., KNIME AG, Microsoft Corp., NVIDIA Corp., Oracle Corp., SAP SE, SAS Institute Inc., The MathWorks Inc. and TIBCO Software Inc.

-

Market Research Insights

- The market is shaped by the strategic integration of AI into core business functions, where a focus on the end-to-end ml lifecycle is paramount. Platforms offering no-code model building capabilities have seen adoption rates increase by over 25% among non-technical users.

- The push for scalable ml infrastructure is evident, with organizations achieving up to a 40% reduction in deployment times by leveraging automated machine learning. Furthermore, as enterprises adopt enterprise integration and analytics, the ability to connect disparate data sources becomes critical, with successful projects showing a 20% improvement in decision-making accuracy.

- The demand for cloud-native solutions continues to grow, driven by the need for flexible, pay-as-you-go access to powerful computational resources like GPU acceleration and specialized tensor processing units, which are essential for advanced AI development.

We can help! Our analysts can customize this machine learning (ml) platforms market research report to meet your requirements.

RIA -

RIA -