Maltodextrin and Maltodextrin Syrup Market Size 2024-2028

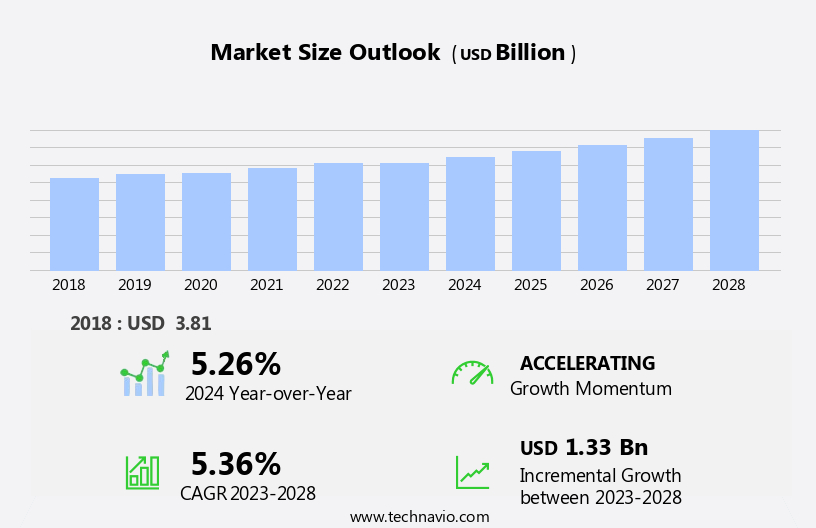

The maltodextrin and maltodextrin syrup market size is forecast to increase by USD 1.33 billion at a CAGR of 5.36% between 2023 and 2028.

- The market is witnessing significant growth due to the numerous industrial applications of maltodextrin. This versatile ingredient is widely used in various industries, including food and beverage, pharmaceuticals, and cosmetics. Additionally, the rising demand for gluten-free food products is driving market growth, as maltodextrin is often used as a replacement for malt and other gluten-containing ingredients. Furthermore, the potential health benefits of maltodextrin, such as its ability to improve nutrient absorption and provide a sustained energy release, are also contributing to its popularity. However, challenges such as the high production cost and the availability of alternative sweeteners may hinder market growth.

- Overall, the market for maltodextrin and maltodextrin syrup is expected to continue expanding, driven by its wide range of applications and the growing consumer preference for gluten-free and functional food products.

What will be the Size of the Maltodextrin and Maltodextrin Syrup Market During the Forecast Period?

- The market In the US is experiencing significant growth due to the increasing demand for maltodextrin as a versatile food additive in various industries. Maltodextrin, a complex carbohydrate, is widely used as a bulking agent, sweetener, thickener, and low-calorie alternative in food and beverages. In the food industry, it is commonly used in baked goods, confectionery, and processed foods. In the personal care sector, maltodextrin syrup is utilized in cosmetics as a thickener and in skincare products for its moisturizing properties. Additionally, maltodextrin has applications in paper processing and drug delivery systems. Health-conscious consumers are driving the demand for low-sugar and low-calorie alternatives, further fueling market growth.

- The trend towards natural and organic products is also influencing the market, as maltodextrin derived from natural sources gains popularity. Overall, the market is expected to continue its growth trajectory In the US due to its wide range of applications and consumer demand for functional and health-conscious products.

How is this Maltodextrin and Maltodextrin Syrup Industry segmented and which is the largest segment?

The maltodextrin and maltodextrin syrup industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Food and beverages

- Pharmaceuticals

- Personal care and cosmetics

- Paper and pulp processing

- Others

- Type

- Dry

- Liquid

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- Middle East and Africa

- South America

- North America

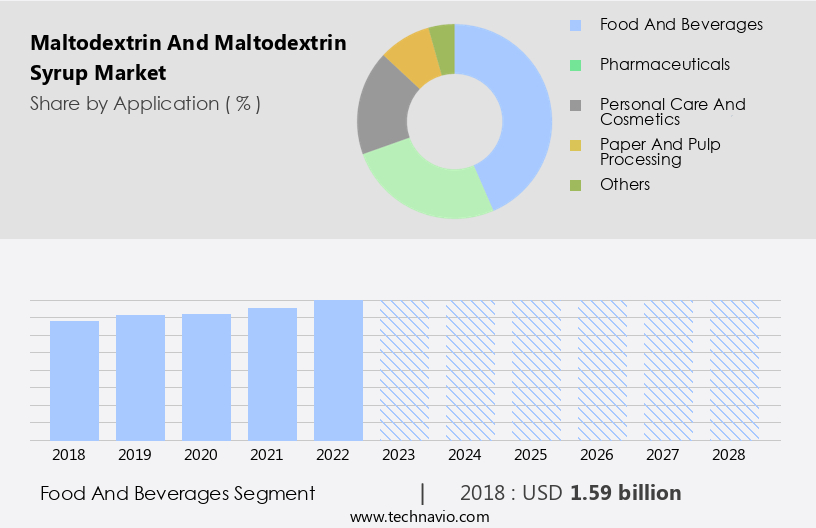

By Application Insights

- The food and beverages segment is estimated to witness significant growth during the forecast period.

Maltodextrin, a versatile carbohydrate with a dextrose equivalent that influences its physical properties, is extensively used In the food industry. Its functional attributes, including good solubility, bulking agent, binding power, non-hygroscopicity, reduced browning, thickening agent, freezing point control, ease of digestion, and neutral or slightly sweet taste, make it an essential ingredient in various food and beverage applications. Maltodextrin's low osmolality further enhances its appeal as an ideal carbohydrate source for sports drinks, infant formulas, and nutritional products. The growing demand for functional foods and beverages is expected to boost the market for maltodextrin and maltodextrin syrups In the forecast period.

This carbohydrate source offers numerous benefits, making it an indispensable ingredient In the food and beverage industry.

Get a glance at the Maltodextrin and Maltodextrin Syrup Industry report of share of various segments Request Free Sample

The Food and beverages segment was valued at USD 1.59 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

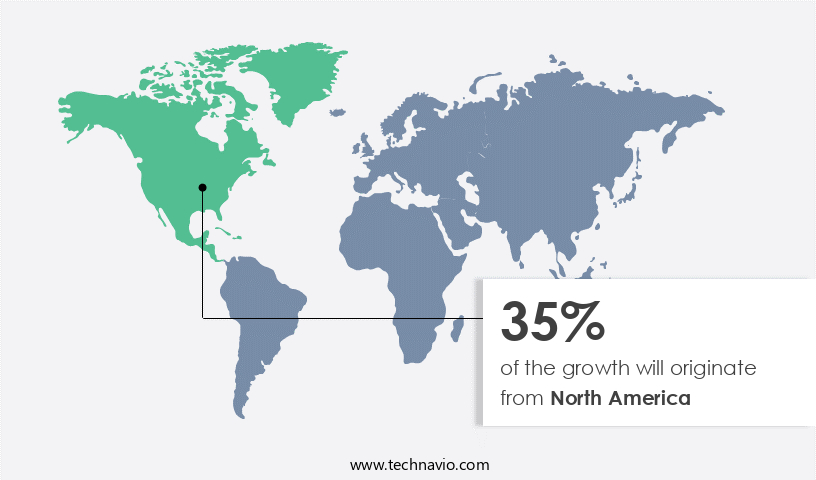

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Maltodextrin is a versatile ingredient widely used in various industries across North America, including food and beverage, pharmaceutical, cosmetic and personal care, and paper. In the US, Canada, and Mexico, maltodextrin is primarily utilized as a sizing and thickening agent, coating bulking agent, binding power, diluent, and viscosity increasing agent. The food and beverage sector is a significant adopter of maltodextrin due to its functional properties and low-calorie and low-sugar alternatives. Maltodextrin is derived from corn, potato, or rice In the US and is regulated under the FDA Code of Federal Regulations (CFR), Section 184. Major contributors to the demand for maltodextrin in North America are the US, Mexico, and Canada.

Market Dynamics

Our maltodextrin and maltodextrin syrup market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Maltodextrin and Maltodextrin Syrup Industry?

Numerous industrial applications of maltodextrin is the key driver of the market.

- Maltodextrin, a carbohydrate derived from starch hydrolysis, is a valuable ingredient in various industries due to its multifunctional properties. In the Food and Beverage sector, maltodextrin functions as a bulking agent, sweetener, and thickener. It is commonly found in sports drinks, soups, sauces, and desserts. Notable suppliers of maltodextrin to this industry include Cargill Inc., Tate and Lyle Plc, and Archer Daniels Midland Co. In the Pharmaceutical industry, maltodextrin is utilized as a filler in tablets and capsules. Additionally, it serves as a carrier for drug delivery systems. Key players in this market are Grain Processing Corp. And Roquette Freres SA.

- Maltodextrin Syrup, a liquid form of maltodextrin, is gaining popularity as a low-calorie and low-sugar alternative In the Food and Beverage industry. It is also used In the Personal Care sector as a thickener in cosmetics and skincare products. Furthermore, maltodextrin is employed in Paper Processing as a binder and coating agent. Health-conscious consumers are increasingly seeking out low-calorie and low-sugar alternatives, driving the demand for maltodextrin and maltodextrin syrup In the Food and Beverage industry. Similarly, the Personal Care sector is witnessing a surge in demand for natural and functional ingredients, leading to an increase In the use of maltodextrin in skincare and cosmetic products.

- In summary, maltodextrin and maltodextrin syrup are versatile ingredients with wide applications across various industries, including Food and Beverages, Pharmaceuticals, and Personal Care. The growing demand for low-calorie and low-sugar alternatives, as well as the increasing preference for natural and functional ingredients, is expected to fuel the growth of the maltodextrin market In the US.

What are the market trends shaping the Maltodextrin and Maltodextrin Syrup Industry?

Rising demand for gluten-free food products is the upcoming market trend.

- Maltodextrin is a versatile carbohydrate derived from starch sources like corn, rice, and potatoes. In the food and beverage industry, it is widely used as a functional ingredient, particularly in gluten-free formulations. As a tasteless and texturally neutral substance, maltodextrin acts as a crucial stabilizer, thickener, and bulking agent. Its application extends to various gluten-free products, including sauces, baked goods, and snacks. With the increasing health consciousness among consumers, there is a growing demand for low-calorie and low-sugar alternatives. Maltodextrin syrup, a liquid form of maltodextrin, offers benefits as a sweetener and soluble dietary fiber. Beyond food and beverages, maltodextrin finds applications in paper processing and personal care industries.

- In cosmetics, it functions as a thickener and improves the texture of various skincare products. In drug delivery systems, it serves as a carrier for active pharmaceutical ingredients. Manufacturers continue to explore the potential of maltodextrin as a functional ingredient to enhance the overall quality and sensory aspects of their products, catering to the evolving consumer preferences.

What challenges does the Maltodextrin and Maltodextrin Syrup Industry face during its growth?

Potential health effects of maltodextrin is a key challenge affecting the industry growth.

- Maltodextrin, a versatile carbohydrate additive, is widely used in various industries, including Food and Beverages, Personal Care, and Paper Processing. The Food and Beverages sector is the largest consumer of maltodextrin, where it functions as a bulking agent, sweetener, and thickener. In the Personal Care industry, maltodextrin syrup is employed in cosmetics due to its ability to improve texture and stability. Maltodextrin, a food additive, is approved by regulatory bodies like the European Food Safety Authority (EFSA) and the US Food and Drug Administration (FDA). However, its impact on health varies based on individual tolerance, dietary context, and consumption levels.

- Maltodextrin has a high glycemic index, leading to a quick rise in blood sugar levels, which may not be suitable for people with diabetes or insulin resistance. On the other hand, athletes and those seeking quick energy may find this feature beneficial. Digestive sensitivity is another factor affecting the use of maltodextrin. Some individuals may experience gas, bloating, or stomach discomfort after ingesting it. Health-conscious consumers are increasingly seeking low-calorie and low-sugar alternatives, which may limit the demand for maltodextrin in certain applications. However, its role in drug delivery systems and skincare products continues to expand, offering growth opportunities In the market.

Exclusive Customer Landscape

The maltodextrin and maltodextrin syrup market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the maltodextrin and maltodextrin syrup market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, maltodextrin and maltodextrin syrup market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

AGRANA BEteilgungs AG - Our company provides top-tier maltodextrin and maltodextrin syrup solutions for the US market. Notable offerings include Agenamalt and Agenanova. Maltodextrin, a glucose polymer, is a popular carbohydrate source due to its rapid energy release and ease of digestion. Maltodextrin syrup, a liquid form of maltodextrin, offers added convenience for various applications. These products cater to diverse industries, including food and beverage, pharmaceuticals, and sports nutrition. Our commitment to quality and innovation ensures that we deliver superior maltodextrin and maltodextrin syrup solutions to meet the unique needs of our clients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGRANA BEteilgungs AG

- Archer Daniels Midland Co.

- Azelis SA

- Bluecraft Agro Pvt. Ltd.

- Cargill Inc.

- Grain Processing Corp.

- Gujarat Ambuja Exports Ltd.

- Gulshan Polyols Ltd.

- Ingredion Inc.

- Kent Corp.

- Lifeasible

- Matsutani Chemical Industry Co. Ltd.

- Merck KGaA

- PPZ NOWAMYL S.A.

- Pruthvis Foods Pvt Ltd.

- Roquette Freres SA

- Sanstar Bio Polymers Ltd.

- Santa Cruz Biotechnology Inc.

- Tate and Lyle PLC

- Tereos Participations

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Maltodextrin Syrup: A Versatile Food Additive and Industrial Ingredient Maltodextrin syrup, a starch hydrolysate derived from corn, rice, potato, or wheat, has gained significant popularity in various industries due to its unique properties. This colorless, odorless, and sweet-tasting liquid is a valuable addition to numerous applications, including food and beverages, personal care, and paper processing. Maltodextrin syrup is a multifunctional ingredient In the food and beverage sector. It serves as a bulking agent, sweetener, and thickener, making it an ideal choice for formulating low-calorie and low-sugar alternatives. Its high solubility and low viscosity enable manufacturers to create beverages with excellent mouthfeel and texture.

Furthermore, maltodextrin syrup's ability to mask bitter tastes makes it an essential component In the production of functional foods and nutritional supplements. In the personal care industry, maltodextrin syrup finds extensive use as a thickener and humectant in various cosmetics and skincare products. Its ability to absorb and retain moisture helps maintaIn the desired consistency and texture of these products. Additionally, its low viscosity and ease of use make it a preferred choice for drug delivery systems, enabling the development of advanced topical treatments. Maltodextrin syrup's applications extend beyond food and personal care industries. In paper processing, it is used as a coating agent to improve the printability and appearance of paper products.

Its ability to form a thin, uniform film on paper surfaces enhances the bonding of inks and coatings, ensuring superior print quality. Health-conscious consumers' increasing demand for natural, low-calorie, and low-sugar alternatives has fueled the growth of the maltodextrin syrup market. Manufacturers are constantly innovating to cater to this trend by developing new products that offer the benefits of maltodextrin syrup while adhering to consumers' preferences. In conclusion, maltodextrin syrup is a versatile and indispensable ingredient in various industries. Its unique properties, including high solubility, low viscosity, and ability to mask bitter tastes, make it an essential component in food and beverage, personal care, and paper processing applications.

The growing demand for natural, low-calorie, and low-sugar alternatives is expected to further boost the market growth for maltodextrin syrup.

|

Maltodextrin and Maltodextrin Syrup Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

177 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.36% |

|

Market growth 2024-2028 |

USD 1.33 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.26 |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Maltodextrin and Maltodextrin Syrup Market Research and Growth Report?

- CAGR of the Maltodextrin and Maltodextrin Syrup industry during the forecast period

- Detailed information on factors that will drive the Maltodextrin and Maltodextrin Syrup growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the maltodextrin and maltodextrin syrup market growth of industry companies

We can help! Our analysts can customize this maltodextrin and maltodextrin syrup market research report to meet your requirements.

RIA -

RIA -