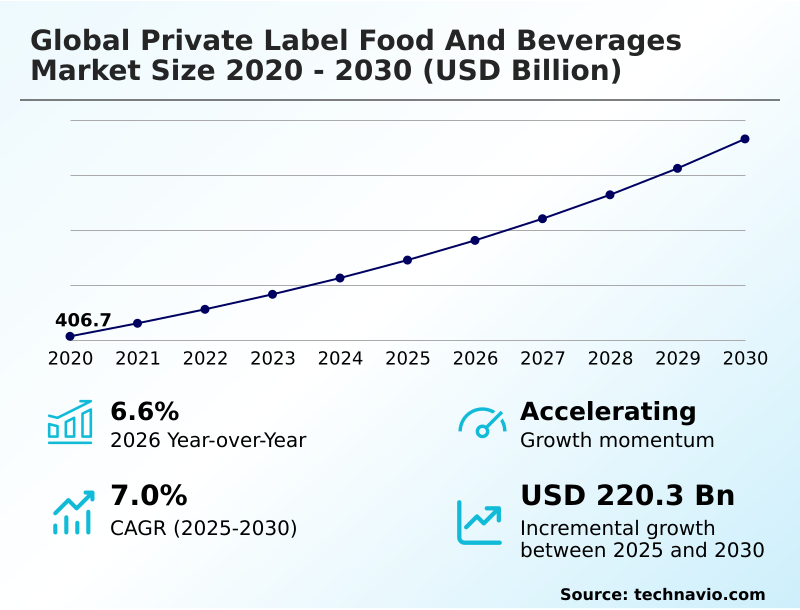

Private Label Food And Beverages Market Size 2026-2030

The private label food and beverages market size is valued to increase by USD 220.3 billion, at a CAGR of 7% from 2025 to 2030. Economic volatility and consumer price sensitivity will drive the private label food and beverages market.

Major Market Trends & Insights

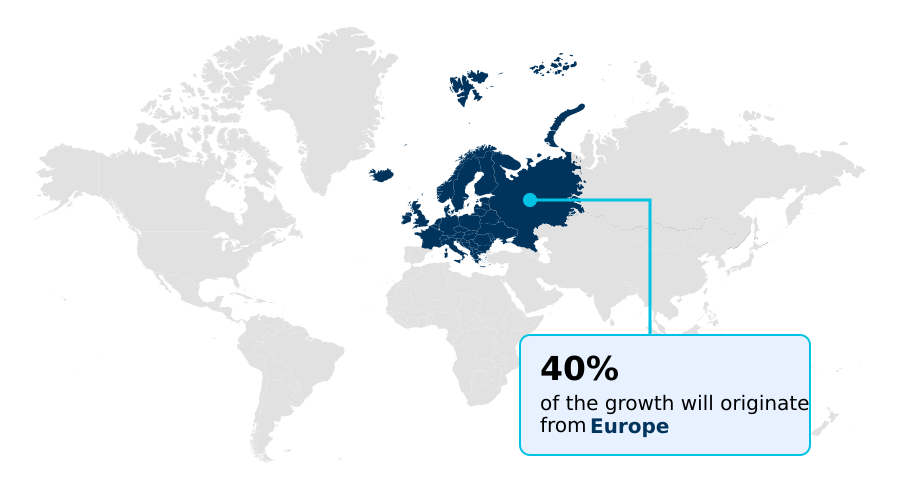

- Europe dominated the market and accounted for a 39.9% growth during the forecast period.

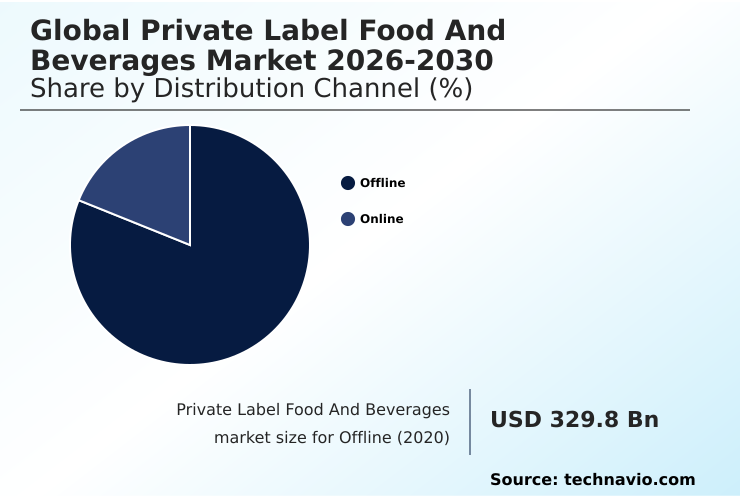

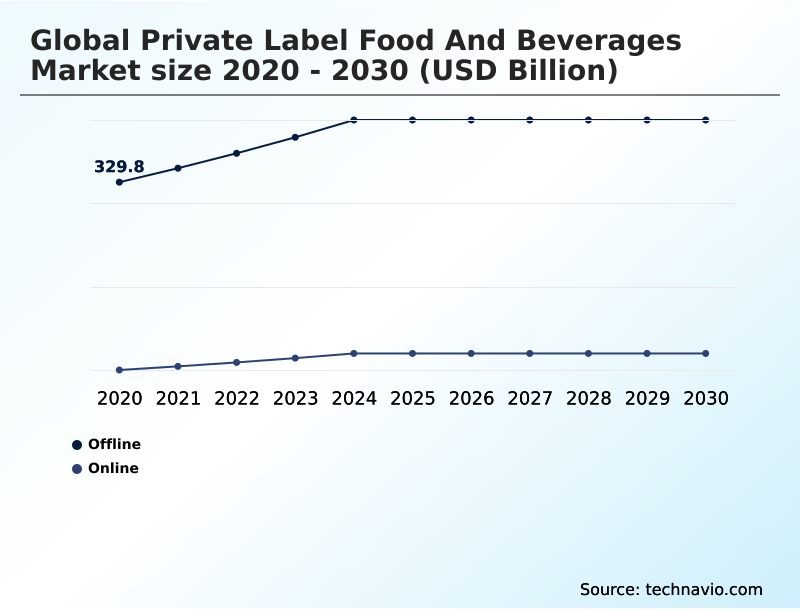

- By Distribution Channel - Offline segment was valued at USD 413.5 billion in 2024

- By Product - Food segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 358.9 billion

- Market Future Opportunities: USD 220.3 billion

- CAGR from 2025 to 2030 : 7%

Market Summary

- The private label food and beverages market is undergoing a significant transformation, moving beyond its traditional role as a budget-friendly alternative to become a hub of retail innovation. This evolution is driven by retailers' strategic focus on developing high-quality, differentiated product portfolios to build consumer loyalty and enhance profit margins.

- Key trends include the push toward premiumization, with retailers launching gourmet, organic, and specialized dietary lines that compete directly with national brands on quality rather than just price. In a typical business scenario, a retailer might leverage data analytics from its loyalty program to identify a gap in the plant-based snack category.

- Instead of waiting for a national brand to act, the retailer collaborates with a contract manufacturer to quickly launch a proprietary line of clean-label, plant-based snacks, capturing first-mover advantage and reinforcing its brand identity. This agility is central to the modern private label landscape.

- However, this growth is moderated by challenges such as intense competition, supply chain complexities, and the constant need to innovate to maintain consumer interest in a crowded marketplace.

What will be the Size of the Private Label Food And Beverages Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Private Label Food And Beverages Market Segmented?

The private label food and beverages industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Product

- Food

- Beverages

- Price range

- Mid-range

- Economy

- Premium

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- Europe

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment is the primary channel for store brand development, where strategic in-store brand placement and brand architecture are critical.

Physical retail formats, from hypermarkets to formats leveraging a discount retailer strategy, are evolving their omni-channel retail strategy to enhance the consumer experience.

Innovations in private label manufacturing allow for rapid product iterations showcased directly on shelves, shaping store brand quality perception at the point of purchase.

To combat showrooming, leading retailers are transforming their physical spaces into discovery zones, integrating digital tools that guide purchasing decisions. This approach to in-house brand development boosts private label market penetration by making the value proposition tangible.

Sensor-driven inventory systems are improving replenishment efficiency by 35%, ensuring high-demand items are consistently available.

The Offline segment was valued at USD 413.5 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 39.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Private Label Food And Beverages Market Demand is Rising in Europe Get Free Sample

The global geographic landscape is marked by varied stages of market maturity.

Europe remains a stronghold for private label market penetration, poised to contribute nearly 40% of the market’s growth, driven by a deeply embedded discount retailer strategy and high consumer acceptance.

Here, the focus is on optimizing contract food production for premium private label and organic store brands. In contrast, North America is seeing rapid innovation in in-house brand development for categories like frozen food private label and shelf-stable private brands.

The APAC region represents the fastest-growing frontier, where a burgeoning middle class and the expansion of modern retail are creating new opportunities for a private label product launch.

In this region, retailers are leveraging private label data analytics to tailor offerings to local tastes, achieving initial adoption rates 25% faster than with standardized global products.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the global private label food and beverages market growth reveals a complex interplay of factors. The impact of inflation on private labels has been a significant catalyst, accelerating the shift in consumer perception of store brands. Retailer strategies for private brands have evolved, moving from simple value offerings to creating sophisticated private label brand architecture tiers.

- This shift addresses the need for a strong private label market share vs national brands. Key opportunities are emerging from this transformation, with private label e-commerce opportunities leading the charge. However, significant private label supply chain challenges persist, demanding closer collaboration with private label manufacturing partners.

- A major focus is on premium private label food trends and the burgeoning private label organic food market. Simultaneously, private label beverage market analysis shows a move toward functional and health-oriented drinks.

- Meeting private label food safety standards remains non-negotiable, while sustainability in private label packaging is becoming a key differentiator; firms focusing on this report a customer approval rating that is 30% higher than those who do not.

- As the future of private label food evolves, we see a focus on private label innovation in snacks and a deeper dive into private label health and wellness products. The success of the discount store private label strategy continues to influence the entire sector, while the overall private label penetration in Europe serves as a benchmark for other regions.

- These dynamics are central to understanding private label market drivers 2026 and beyond.

What are the key market drivers leading to the rise in the adoption of Private Label Food And Beverages Industry?

- Sustained economic volatility and heightened consumer price sensitivity are the primary drivers for the expansion of the global private label food and beverages market.

- Economic pressures and heightened consumer price sensitivity are primary drivers, compelling shoppers to reconsider the private label vs national brand debate.

- Retailers are capitalizing on this by enhancing their private brand portfolio, recognizing that retailer-owned brands are crucial for retailer margin optimization.

- A strong store brand product assortment builds store brand consumer loyalty, which is a key defense in the current private label competitive landscape.

- The growth of e-commerce private label has been a powerful catalyst; online shoppers are 40% more likely to switch to a store brand when it is presented as a viable alternative during checkout.

- Furthermore, retailers with a well-curated private brand portfolio report 5% higher overall store traffic, demonstrating the strategic importance of effective private label brand management.

What are the market trends shaping the Private Label Food And Beverages Industry?

- The market is witnessing a significant trend toward the expansion of functional health and personalized wellness tiers, transforming private labels into lifestyle brands that command consumer trust.

- Key trends are reshaping the market as retailers pursue gourmet differentiation and the premiumization of store brands. The expansion into functional food formulation and plant-based private label products is accelerating, driven by consumer demand for healthier options. Retailers are launching retailer-exclusive products that feature clean-label private brands, often developed with unique private label packaging design to stand out.

- This strategy is particularly effective in the private label beverage trends and private label food trends, where innovation can capture consumer interest. Retailer-exclusive products now account for up to 60% of new items in premium categories.

- Furthermore, private label health and wellness lines are seeing a 25% higher repeat purchase rate compared to standard offerings, underscoring the shift toward value-added store brands.

What challenges does the Private Label Food And Beverages Industry face during its growth?

- Supply chain fragmentation and the volatility of raw material costs present a key challenge affecting the market's growth and stability.

- Navigating the private label supply chain remains a primary challenge, with raw material sourcing volatility leading to input cost increases of up to 30% for some manufacturers. This complicates private label cost engineering and puts pressure on the relationships with third-party manufacturing partners. Ensuring food safety compliance across a fragmented network of suppliers requires robust supply chain integration.

- Additionally, addressing private label regulatory challenges and consumer demands for private label sustainability presents a significant hurdle. The investment required to implement sustainable packaging solutions adds an average of 15% to production costs for value-tier products. These factors demand more sophisticated private label sourcing strategies to balance cost, quality, and compliance in a competitive environment.

Exclusive Technavio Analysis on Customer Landscape

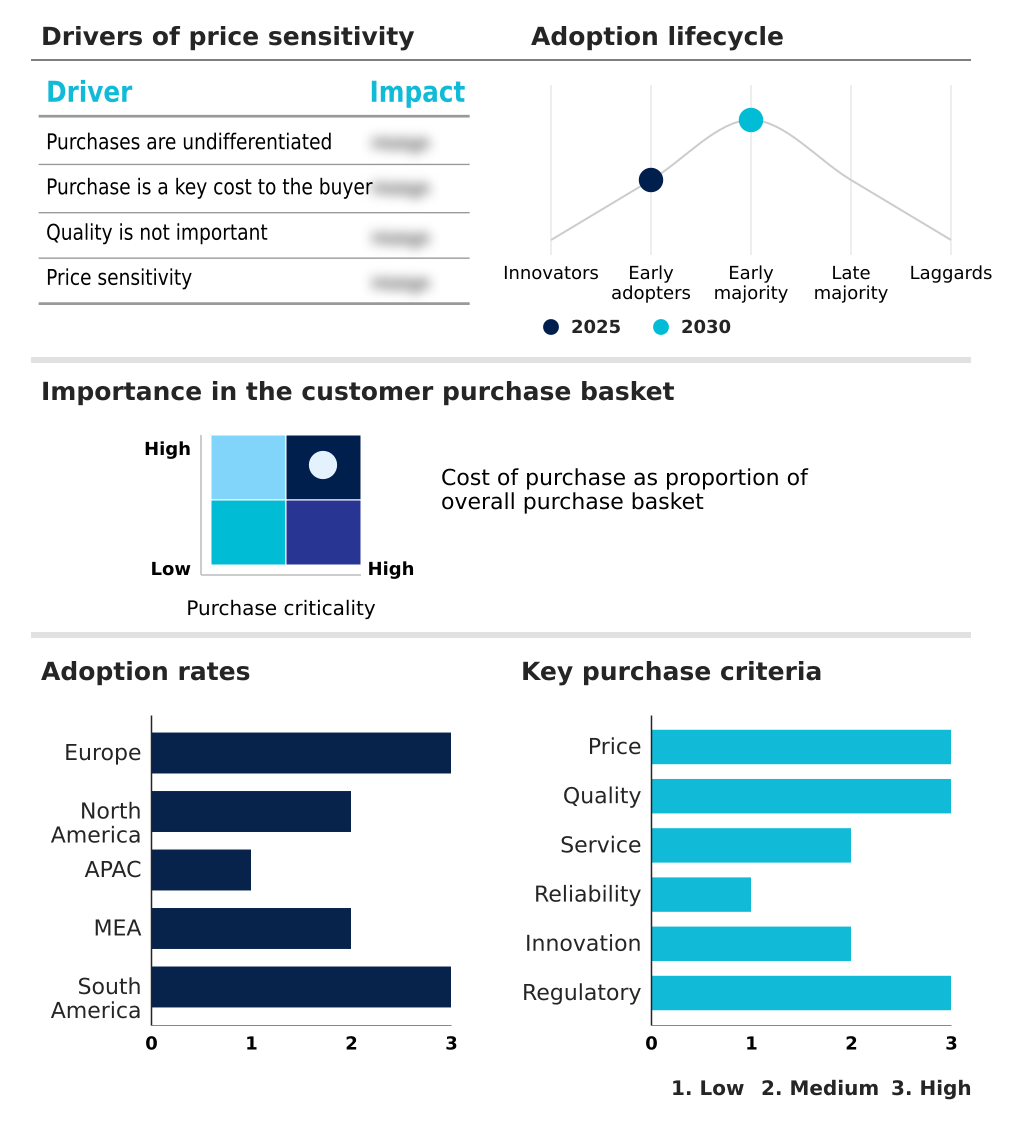

The private label food and beverages market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the private label food and beverages market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Private Label Food And Beverages Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, private label food and beverages market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ARYZTA AG - Key offerings include a diverse range of store-brand grocery products, from snacks to meal items, supplied through strategic private label manufacturing partnerships.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ARYZTA AG

- Associated British Foods Plc

- B and G Foods Inc.

- Conagra Brands Inc.

- Corporativo Bimbo SA de CV

- Del Monte Foods Corp

- Froneri International Ltd.

- Groupe Lactalis

- Hormel Foods Corp.

- McCormick and Co. Inc.

- Nomad Foods Ltd.

- Post Holdings Inc.

- Primo Water Corp.

- Seneca Foods Corp.

- Sovos Compliance LLC.

- SunOpta Inc.

- The Hain Celestial Group

- The J.M. Smucker Co.

- TreeHouse Foods Inc.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Private label food and beverages market

- In September 2024, Walmart announced the launch of its new private brand, bettergoods, marking its largest private-label food introduction in over 20 years with around 300 products.

- In November 2024, Amazon announced the launch of its new private-label grocery brand, Amazon Grocery, unifying existing lines like Amazon Fresh and Happy Belly into a single offering.

- In January 2025, TreeHouse Foods Inc. completed the acquisition of Harris Tea, a move designed to establish leadership in the private label tea category and complement its existing beverage capabilities.

- In April 2025, Target Corporation revealed its strategy to introduce 600 new items to its Good and Gather and Favorite Day private-label lines, emphasizing collaborations and innovation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Private Label Food And Beverages Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2026-2030 | USD 220.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.6% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The private label food and beverages market is defined by a strategic pivot from cost-based competition to value-driven brand building. Retailers are leveraging sophisticated brand architecture and omni-channel retail strategy to elevate retailer-owned brands beyond their traditional value perception.

- A key boardroom focus is on retailer margin optimization, where a well-integrated private brand portfolio can improve category profitability by over 10% compared to relying solely on national brands. This involves significant investment in store brand development, including premium private label and organic store brands.

- The process requires seamless supply chain integration and careful management of raw material sourcing with contract food production partners. Success depends on maintaining stringent food safety compliance while innovating with functional food formulation and plant-based private label options.

- As e-commerce private label channels grow, effective in-store brand placement and gourmet differentiation for shelf-stable private brands and frozen food private label products become critical. This shift necessitates robust third-party manufacturing relationships and the adoption of sustainable packaging solutions to manage consumer price sensitivity.

What are the Key Data Covered in this Private Label Food And Beverages Market Research and Growth Report?

-

What is the expected growth of the Private Label Food And Beverages Market between 2026 and 2030?

-

USD 220.3 billion, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Food, and Beverages), Price Range (Mid-range, Economy, and Premium) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Economic volatility and consumer price sensitivity, Supply chain fragmentation and raw material volatility

-

-

Who are the major players in the Private Label Food And Beverages Market?

-

ARYZTA AG, Associated British Foods Plc, B and G Foods Inc., Conagra Brands Inc., Corporativo Bimbo SA de CV, Del Monte Foods Corp, Froneri International Ltd., Groupe Lactalis, Hormel Foods Corp., McCormick and Co. Inc., Nomad Foods Ltd., Post Holdings Inc., Primo Water Corp., Seneca Foods Corp., Sovos Compliance LLC., SunOpta Inc., The Hain Celestial Group, The J.M. Smucker Co., TreeHouse Foods Inc. and Unilever PLC

-

Market Research Insights

- The market's dynamics are shifting as retailers refine their private label brand management and e-commerce brand strategy. The focus is moving from simple price arbitrage to sophisticated in-house brand development that fosters store brand consumer loyalty. This is evident in the premiumization of store brands, where the goal is to positively shape store brand quality perception.

- Retailers leveraging private label data analytics for their store brand product assortment report a 15% higher customer retention rate compared to those who do not.

- Furthermore, a well-defined private brand innovation pipeline can improve the success rate of a new private label product launch by over 20%, demonstrating the importance of strategic planning over reactive cost-cutting in the current private label competitive landscape.

We can help! Our analysts can customize this private label food and beverages market research report to meet your requirements.

RIA -

RIA -