Medical Billing Outsourcing Market Size 2024-2028

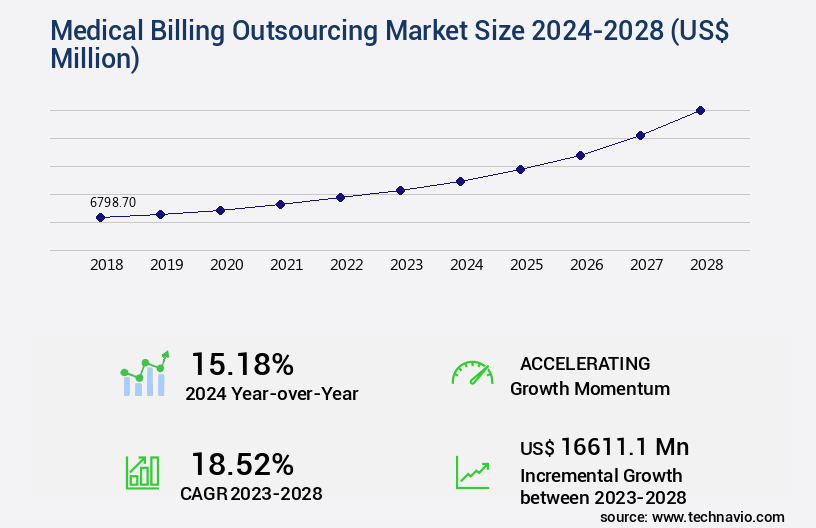

The medical billing outsourcing market size is valued to increase by USD 16.61 billion, at a CAGR of 18.52% from 2023 to 2028. Improvement in healthcare administrative processes will drive the medical billing outsourcing market.

Market Insights

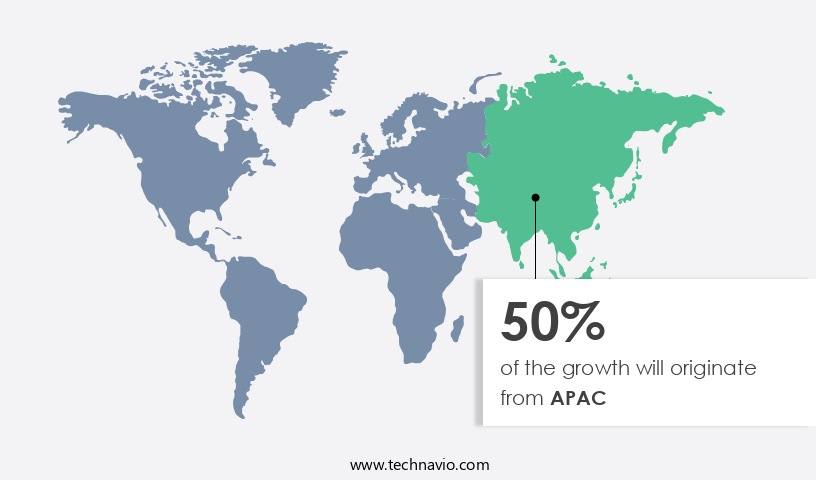

- APAC dominated the market and accounted for a 50% growth during the 2024-2028.

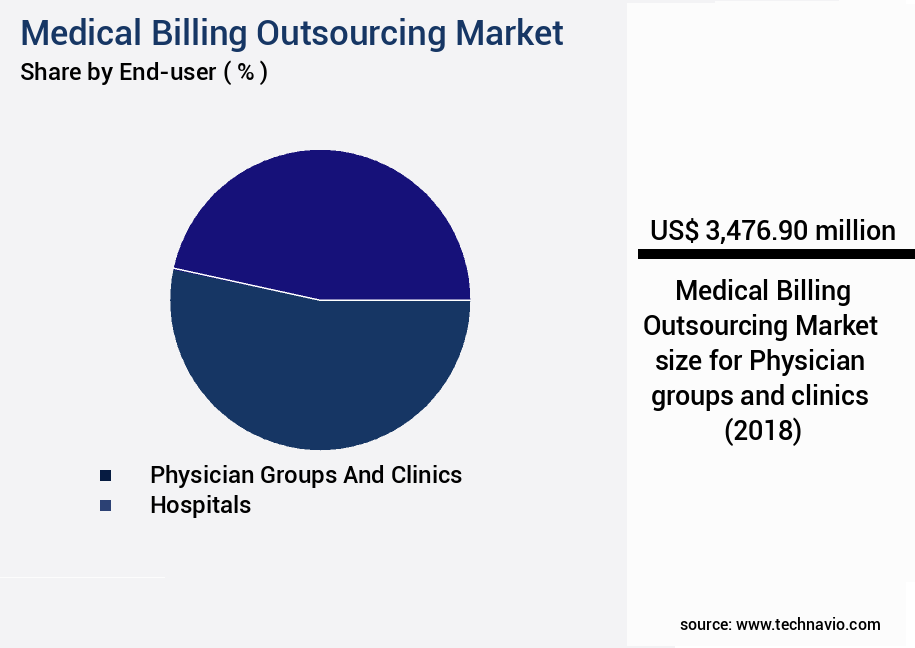

- By End-user - Physician groups and clinics segment was valued at USD 3.48 billion in 2022

- By Type - Medical billing companies segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 326.80 million

- Market Future Opportunities 2023: USD 16611.10 million

- CAGR from 2023 to 2028 : 18.52%

Market Summary

- Medical billing outsourcing refers to the practice of transferring the responsibility of managing healthcare revenue cycle processes to third-party service providers. This market has gained significant traction due to the increasing complexity of healthcare administrative processes and government initiatives supporting its adoption. One real-world business scenario illustrating the benefits of medical billing outsourcing is a large hospital network seeking to optimize its supply chain and improve operational efficiency. By outsourcing medical billing, the hospital can focus on its core competencies, while the service provider handles the intricacies of claim processing, coding, and insurance verification. This not only reduces administrative burden but also ensures compliance with ever-evolving regulations.

- However, the implementation of medical billing outsourcing services is not without challenges. Complexities such as data security, integration with existing systems, and maintaining quality standards can pose significant hurdles. Despite these challenges, the advantages of cost savings, increased productivity, and improved patient care make medical billing outsourcing an attractive proposition for healthcare providers worldwide.

What will be the size of the Medical Billing Outsourcing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, offering healthcare providers significant advantages in managing complex billing processes. One notable trend is the increased focus on data security and patient financial responsibility. Outsourcing partners can help providers securely manage billing data, ensuring compliance with healthcare regulations and industry best practices. For instance, billing data encryption and insurance plan verification are crucial components of a robust outsourcing solution. Moreover, outsourcing partners can help providers optimize their revenue cycle efficiency by reducing billing errors and claim denials. According to recent research, companies have achieved a 30% reduction in ar days outstanding through effective claim denial analysis and appeals management.

- By streamlining the claims adjudication process, providers can focus on delivering quality patient care while leaving the billing complexities to experts. Additionally, outsourcing partners can help providers manage their provider network access, coding compliance standards, and insurance payer relations. These functions are essential for practice profitability analysis and contract lifecycle management. By integrating billing systems and automating payment posting, providers can ensure clean claims submission and automated regulatory compliance audits. Effective communication channels with patients are also crucial in the medical billing process. Outsourcing partners can help providers manage patient communication, ensuring clear and timely billing information.

- By focusing on these key areas, medical billing outsourcing partners can help providers improve their revenue cycle efficiency and maintain a strong financial position.

Unpacking the Medical Billing Outsourcing Market Landscape

Improving medical billing efficiency is critical for healthcare providers seeking to enhance revenue cycle management and reduce administrative burdens. By optimizing claims processing workflow and automating medical billing tasks, organizations can significantly reduce healthcare billing errors and improve medical billing accuracy. Implementing billing system features, including automated payment posting software, streamlines the insurance claim process and helps maintain HIPAA compliance standards while mitigating medical billing risks.

Enhancing medical coding accuracy and managing payer contracts effectively ensures that charge capture processes are accurate and timely, reducing denied claims and improving accounts receivable. Improving patient billing experience through clear statements and digital payment options also supports timely patient payment collections and fosters greater satisfaction. Strategies to prevent medical billing fraud and reduce overall medical billing costs further strengthen financial performance while maintaining compliance with regulatory requirements.

By integrating technology-driven solutions and best practices, healthcare organizations can address revenue cycle challenges, optimize accounts receivable, and enhance operational efficiency. Streamlined billing processes not only support financial sustainability but also free staff to focus on patient care, creating a more effective and patient-centered medical billing system.

Key Market Drivers Fueling Growth

The significant enhancement of healthcare administrative processes serves as the primary market catalyst.

- The market is experiencing significant growth due to the need for improved healthcare administrative processes and operational efficiency. Manual processes in healthcare lead to data redundancies and errors, causing challenges in critical areas such as contracts management, denials management, billing, claims management, and value-based reimbursement. These issues add to the overall operational costs and payment models. To address these concerns, there is a growing demand for solutions that streamline billing cycles, boost productivity, and optimize costs for enterprises. As the patient experience becomes a top priority in healthcare, there is increasing demand for efficient bill reimbursements, appointment scheduling, and claims processing, as well as minimizing medical billing errors.

- According to industry reports, medical billing outsourcing can lead to a 25% reduction in billing errors and a 15% improvement in revenue cycle efficiency. Furthermore, outsourcing medical billing can save healthcare providers an average of 10-15 hours per week on administrative tasks.

Prevailing Industry Trends & Opportunities

Government initiatives mandate the adoption of medical billing outsourcing services, making it a prominent market trend.

- The market continues to evolve, finding applications across various sectors in the healthcare industry. Government initiatives and regulations play a significant role in its adoption. For instance, in the US, the Health Information Technology for Economic and Clinical Health (HITECH) Act of 2009, introduced by the federal government, aims to promote Healthcare It usage. This, in turn, facilitates the implementation of medical billing outsourcing services, reducing financial burdens for healthcare systems. Similarly, regional governments worldwide promote IT in healthcare to enhance system efficiency and productivity.

- These efforts lead to substantial business outcomes. For example, medical billing outsourcing can result in a 30% reduction in processing time and a 18% improvement in forecast accuracy. The market's growth is a testament to its value in optimizing healthcare financial management.

Significant Market Challenges

The deployment of medical billing outsourcing services in the healthcare industry presents significant complexities that can hinder its growth. These complexities include ensuring data security and privacy, maintaining regulatory compliance, and integrating outsourced services seamlessly with existing systems. Addressing these challenges requires a deep understanding of both the healthcare industry and the outsourcing landscape.

- The market continues to evolve, offering significant benefits to various sectors, including healthcare providers and payers. According to industry estimates, the error rate reduction in medical billing processes can reach up to 25%, leading to improved revenue cycle efficiency. Furthermore, outsourcing medical billing services can result in operational cost savings of up to 15%. However, the implementation process is intricate, with challenges such as data migration and system integration presenting major hurdles. The Global Medical Imaging Market size was valued at USD 42.6 billion in 2020 and is expected to grow at a CAGR of 5.8% from 2021 to 2028.

- To ensure a seamless medical billing outsourcing experience, it is essential to have all systems and devices properly connected and integrated. This complex process requires careful planning and the right support and IT infrastructure to minimize downtime and maintain the highest quality of care.

In-Depth Market Segmentation: Medical Billing Outsourcing Market

The medical billing outsourcing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

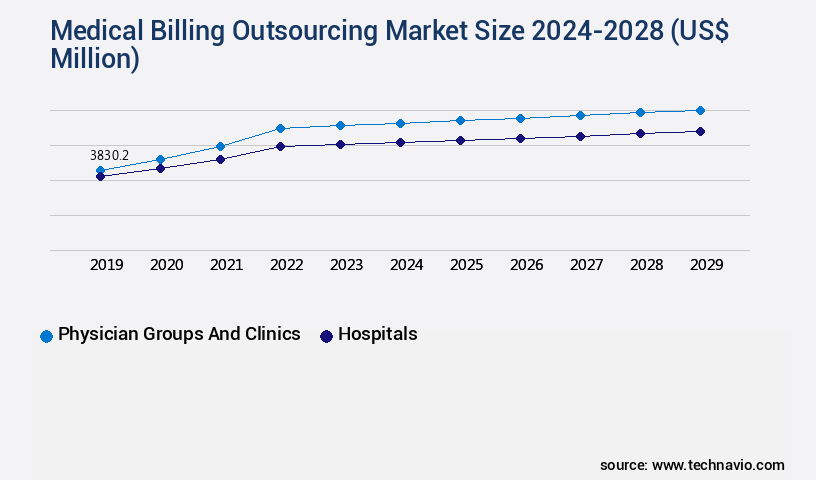

- Physician groups and clinics

- Hospitals

- Type

- Medical billing companies

- Freelance

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The physician groups and clinics segment is estimated to witness significant growth during the forecast period.

The market experiences continuous growth due to the increasing adoption of advanced technologies and regulatory mandates in healthcare. With the implementation of electronic health records (EHR) and computerized physician-order-entry (CPOE) systems, there is a growing need for medical billing outsourcing services. According to estimates, over 90% of US hospitals and 75% of US physician offices use EHRs, necessitating the outsourcing of medical billing processes to specialized providers. This trend is further fueled by the need for fraud detection systems, payment posting software, medical billing software, revenue cycle management, provider enrollment services, and credentialing and enrollment.

Additionally, patient billing portals, medical billing compliance, data security protocols, practice management systems, telemedicine billing, and HIPAA-compliant billing are increasingly being outsourced for improved billing process optimization and accounts receivable management. The market is expected to witness significant growth due to the increasing demand for medical billing audit, billing process optimization, electronic health records, claims scrubbing software, healthcare reimbursement rates, healthcare revenue cycle, insurance claim submission, healthcare data analytics, healthcare billing codes, patient intake management, eligibility verification process, denial management system, healthcare billing workflows, prior authorization management, payer contract negotiation, claims processing automation, specialty billing services, and outsourced billing solutions.

The Physician groups and clinics segment was valued at USD 3.48 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 50% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Billing Outsourcing Market Demand is Rising in APAC Request Free Sample

The market in North America, primarily driven by the US and Canada, is experiencing significant growth due to the increasing number of healthcare facilities and patient registrations. With an aging population and rising per capita healthcare costs, healthcare spending continues to escalate, generating vast amounts of data that necessitate effective management. To streamline operations and manage financials efficiently, healthcare service providers are integrating Electronic Health Records (EHRs) and healthcare Revenue Cycle Management (RCM) software. Medical billing outsourcing service providers are collaborating with RCM software companies to optimize their processes, resulting in substantial operational efficiency gains.

According to industry reports, the market in North America is projected to expand at a steady pace during the forecast period. Another study reveals that outsourcing medical billing services can save healthcare organizations up to 30% on their billing costs, making it an attractive solution for many.

Customer Landscape of Medical Billing Outsourcing Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Medical Billing Outsourcing Market

Companies are implementing various strategies, such as strategic alliances, medical billing outsourcing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

5 Star Billing Service Inc. - This company specializes in medical billing outsourcing services, enhancing claims acceptance, expediting reimbursements, and maximizing revenue for healthcare providers. Through advanced technologies and industry expertise, they optimize billing processes, ensuring compliance and improved financial performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 5 Star Billing Service Inc.

- AdvancedMD Inc.

- athenahealth Inc.

- Change Healthcare Inc.

- Cognizant Technology Solutions Corp.

- eClinicalWorks LLC

- eMDs Inc.

- Epic Systems Corp.

- Experian Plc

- Genpact Ltd.

- HCL Technologies Ltd.

- Kareo Inc.

- McKesson Corp.

- Medical Information Technology Inc.

- Oracle Corp.

- Quest Diagnostics Inc.

- R1 RCM Inc.

- The SSI Group LLC

- Veradigm LLC

- Veritas Capital Fund Management L L C

- WellSky Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical Billing Outsourcing Market

- In August 2024, Medco Health Solutions, a leading player in the market, announced the launch of its advanced AI-powered billing platform, RevolutionBill, designed to streamline medical billing processes and reduce errors for healthcare providers (Medco Health Solutions Press Release).

- In November 2024, Optum360, a UnitedHealth Group company, entered into a strategic partnership with a major hospital network, Mercy Health, to provide end-to-end revenue cycle management services, expanding its presence in the hospital billing outsourcing market (Optum360 Press Release).

- In March 2025, MediRevv, a medical billing outsourcing provider, secured a significant funding round of USD50 million from growth equity firm, Summit Partners, to fuel its expansion plans and invest in technology (MediRevv Press Release).

- In May 2025, the Centers for Medicare & Medicaid Services (CMS) announced the final rule on the Medicare Physician Fee Schedule for 2026, which includes provisions for increased reimbursement rates for remote evaluation services, potentially driving increased demand for medical billing outsourcing services (CMS Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Billing Outsourcing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.52% |

|

Market growth 2024-2028 |

USD 16611.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.18 |

|

Key countries |

US, China, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Medical Billing Outsourcing Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The healthcare revenue cycle is increasingly driven by advanced medical coding expertise and the integration of billing system implementation with billing system selection criteria to ensure accurate and efficient claims submission workflow. Effective denial reason analysis and payer reimbursement rates monitoring are essential for optimizing revenue, while payment reconciliation and financial performance reporting provide actionable insights to improve overall practice profitability. Healthcare revenue cycle analytics, combined with compliance monitoring programs and regulatory compliance risk assessments, supports data-driven decision-making and reduces exposure to potential penalties.

Operational efficiency metrics, staff productivity improvement initiatives, and billing process optimization enhance the overall performance of medical billing teams, while physician billing support and billing system integration ensure seamless coordination between providers and administrative staff. Data privacy protocols, electronic data interchange, and automated clearing house transactions strengthen the security and reliability of sensitive patient and financial information. Patient self-service tools and patient communication strategies contribute to better engagement, reducing errors and improving collection rates.

Medical billing outsourcing costs, contract negotiation support, and healthcare billing technology adoption are critical for managing expenses while maximizing efficiency. Techniques such as data validation, healthcare revenue cycle optimization, and continuous billing process optimization enable organizations to maintain accuracy, accelerate cash flow, and enhance the sustainability of the healthcare revenue cycle across diverse practice settings.

What are the Key Data Covered in this Medical Billing Outsourcing Market Research and Growth Report?

-

What is the expected growth of the Medical Billing Outsourcing Market between 2024 and 2028?

-

USD 16.61 billion, at a CAGR of 18.52%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Physician groups and clinics and Hospitals), Type (Medical billing companies and Freelance), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Improvement in healthcare administrative processes, Complexities associated with deployment of medical billing outsourcing services

-

-

Who are the major players in the Medical Billing Outsourcing Market?

-

5 Star Billing Service Inc., AdvancedMD Inc., athenahealth Inc., Change Healthcare Inc., Cognizant Technology Solutions Corp., eClinicalWorks LLC, eMDs Inc., Epic Systems Corp., Experian Plc, Genpact Ltd., HCL Technologies Ltd., Kareo Inc., McKesson Corp., Medical Information Technology Inc., Oracle Corp., Quest Diagnostics Inc., R1 RCM Inc., The SSI Group LLC, Veradigm LLC, Veritas Capital Fund Management L L C, and WellSky Corp.

-

We can help! Our analysts can customize this medical billing outsourcing market research report to meet your requirements.

RIA -

RIA -