Electronic Health Records Market Size 2026-2030

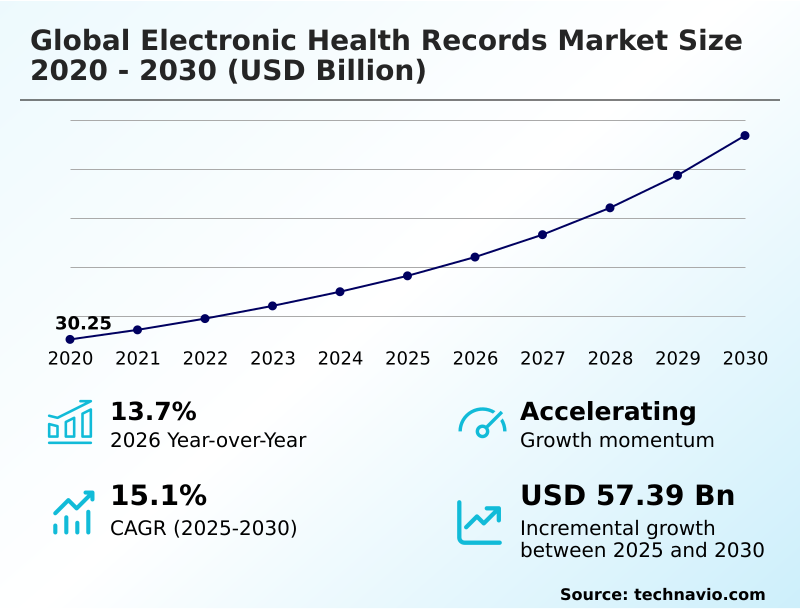

The electronic health records market size is valued to increase by USD 57.39 billion, at a CAGR of 15.1% from 2025 to 2030. Institutionalization of European health data space regulatory frameworks will drive the electronic health records market.

Major Market Trends & Insights

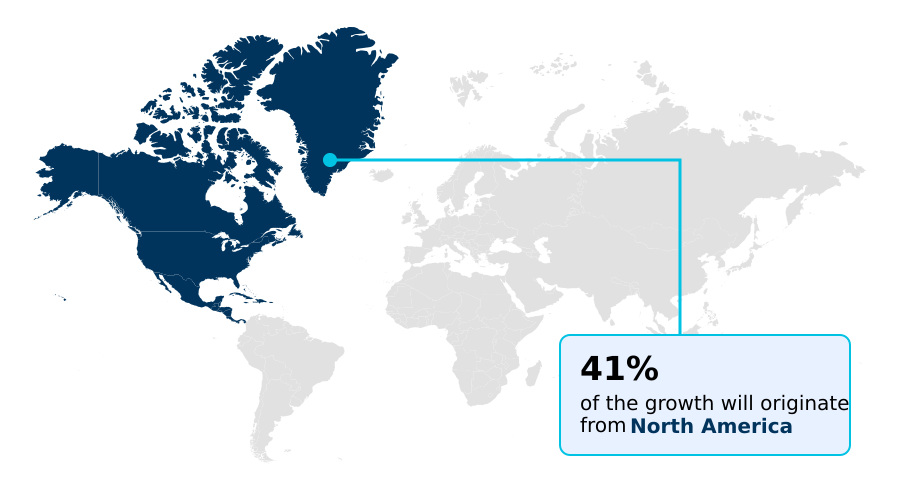

- North America dominated the market and accounted for a 41.3% growth during the forecast period.

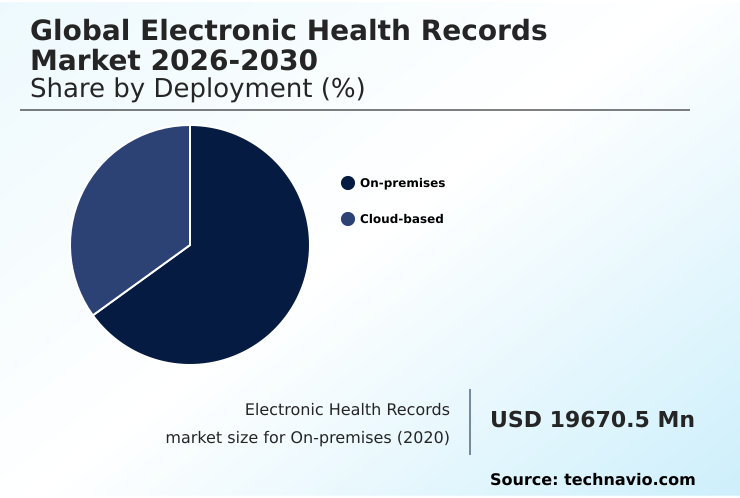

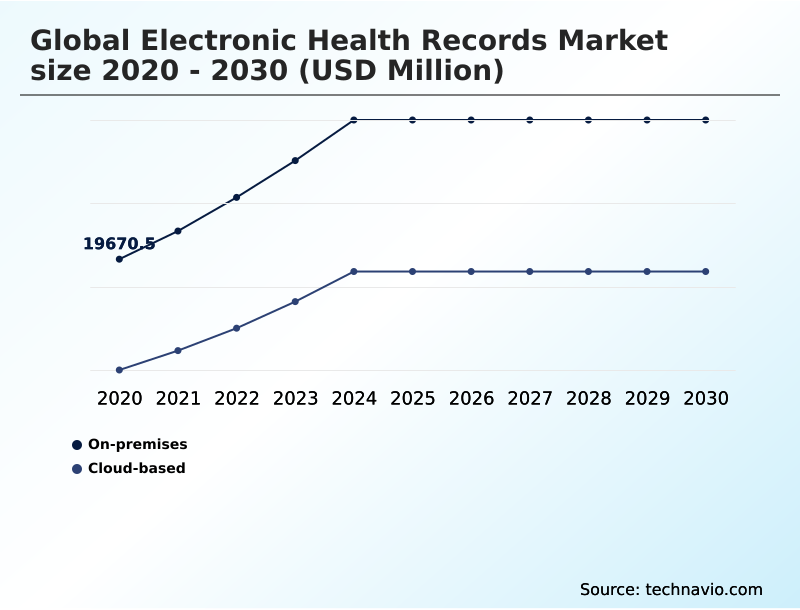

- By Deployment - On-premises segment was valued at USD 31.09 billion in 2024

- By Component - Services segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 83.39 billion

- Market Future Opportunities: USD 57.39 billion

- CAGR from 2025 to 2030 : 15.1%

Market Summary

- The electronic health records market is undergoing a fundamental transformation, evolving from digital filing cabinets into intelligent clinical ecosystems. This shift is driven by the dual pressures of regulatory mandates demanding greater health data interoperability and the operational need to improve care quality under value-based care models.

- Modern systems prioritize clinical workflow automation and the integration of predictive analytics engines to provide real-time clinical decision support at the point of care. For instance, in chronic disease management, a digital health platform can aggregate a longitudinal patient record with patient-generated health data from wearables, using an ai-driven diagnostics module to flag at-risk individuals for proactive intervention.

- This automated clinical documentation and analysis, powered by natural language processing, not only enhances care coordination but also helps mitigate physician burnout. The adoption of cloud-native ehr and robust cybersecurity frameworks is essential to ensure this sensitive data remains secure, accessible, and capable of driving meaningful health outcomes.

What will be the Size of the Electronic Health Records Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Electronic Health Records Market Segmented?

The electronic health records industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud-based

- Component

- Services

- Software

- Hardware

- Type

- Integrated

- Standalone

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The on-premises deployment model remains critical for healthcare organizations prioritizing data sovereignty and direct control over their digital infrastructure.

By maintaining an on-premises data center, institutions can implement a bespoke cybersecurity framework, leveraging zero-trust architecture and biometric authentication to protect sensitive patient information.

This approach facilitates a controlled legacy system migration and allows for a highly customized user interface design tailored to specific ambulatory care workflows.

While requiring significant capital, this model offers unmatched control over data governance policy and disaster recovery planning, with some facilities achieving over 99.9% uptime for critical data access.

This ensures that even with the growth of cloud solutions, on-premises systems continue to be the preferred choice for large hospital networks requiring granular system oversight.

The On-premises segment was valued at USD 31.09 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electronic Health Records Market Demand is Rising in North America Get Free Sample

The geographic landscape reveals a market of varied maturity. In North America and Europe, the focus is on optimizing existing infrastructure through advanced health analytics and telehealth integration.

Adoption of patient portals in these regions has increased patient engagement by 25%. These mature markets leverage the cloud hosting environment to deploy AI-driven diagnostics and build longitudinal patient records for clinical trial management.

In contrast, many parts of Asia are focused on establishing foundational digital health platforms and expanding real-world evidence collection. The integration of remote patient monitoring is a global priority, with some systems showing a 15% reduction in chronic care costs.

This regional divergence creates distinct opportunities, from advanced predictive analytics engine development in established markets to scalable infrastructure deployment in high-growth regions.

Market Dynamics

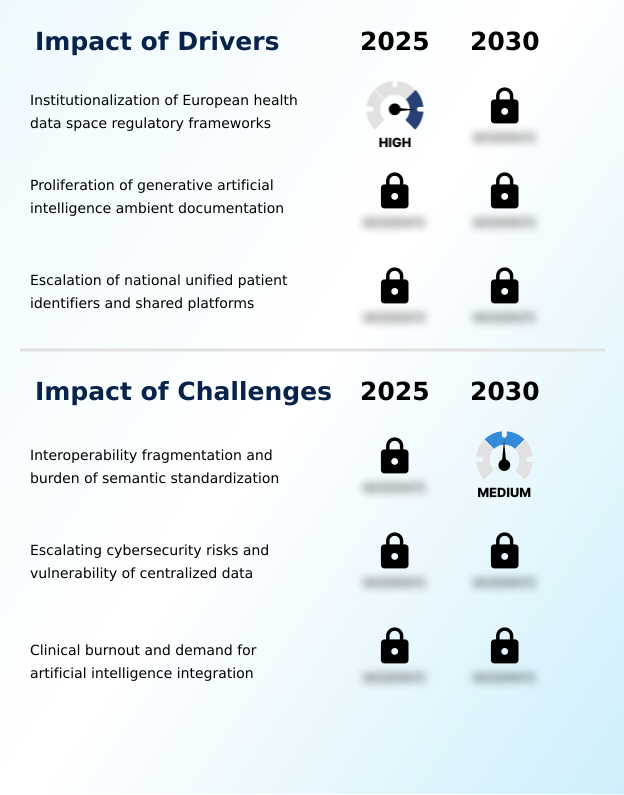

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the electronic health records market is toward creating a deeply interconnected and intelligent healthcare ecosystem. Key initiatives focus on ehr integration with telemedicine platforms to extend care beyond traditional settings, a trend accelerated by the need for remote consultations.

- Concurrently, the rise of ai-driven diagnostic support in ehr is transforming clinical practice by providing tools for early disease detection, such as using predictive analytics in ehr for sepsis detection. The benefits of a unified care record are becoming increasingly clear, particularly for managing chronic conditions with ehr data.

- To achieve this, resolving the challenges of ehr interoperability through standards like the fhir standard is paramount. For smaller providers, cloud based ehr for small practices offers a cost-effective entry point, while larger systems undertake complex ehr data migration best practices.

- The entire ecosystem is underpinned by robust cybersecurity measures for ehr systems and mobile ehr app security protocols to ensure compliance with ehr data privacy laws. Improving patient engagement via ehr portals and integrating wearables with ehr are key to involving patients in their own care.

- Furthermore, optimizing ehr workflow for nurses and addressing the impact of ehr on physician burnout through tools like natural language processing for unstructured ehr data are critical for sustainability.

- The ultimate goal is to measure the roi of ehr implementation not just in financial terms but in improved patient outcomes and provider satisfaction, a metric where systems that integrate patient-generated data have shown effectiveness improvements of over 50% compared to those without.

What are the key market drivers leading to the rise in the adoption of Electronic Health Records Industry?

- A key market driver is the institutionalization of regulatory frameworks, such as the European Health Data Space, which mandates standardized data exchange.

- The market is propelled by the formalization of interoperability standards, such as the FHIR standard and SNOMED CT terminology, which are essential for achieving true data liquidity.

- These standards enable the secure data exchange required for effective population health management and are critical for the success of value-based care models.

- The focus is on creating a seamless health information exchange where data can move freely across a care coordination platform, facilitating cross-continuum communication.

- This level of healthcare data interoperability is vital for chronic disease management, allowing providers to track patient progress over time.

- Adherence to the FHIR standard can reduce system integration costs by up to 40%, while integrated population health management platforms have helped lower hospital readmission rates by 20%.

What are the market trends shaping the Electronic Health Records Industry?

- The industrialization of ambient AI scribing solutions represents a significant market trend. These technologies are being deployed to automate clinical documentation and enhance provider efficiency.

- A primary market trend is the rapid adoption of ambient clinical intelligence, which leverages natural language processing to enable hands-free documentation. This shift toward automated clinical documentation, often using an AI scribe, is a direct response to the need for physician burnout reduction.

- Modern cloud-native EHR platforms are integrating these tools to provide real-time data access and streamline clinical workflow automation. These systems are increasingly designed to incorporate patient-generated health data from mobile EHR applications and wearables, enhancing patient engagement tools. This evolution supports the transition to value-based care reimbursement models by providing richer data for outcomes analysis.

- AI scribe tools can now capture clinical encounters with over 95% accuracy, while mobile EHR applications have increased direct patient data entry by 30%.

What challenges does the Electronic Health Records Industry face during its growth?

- A primary challenge affecting industry growth is the ongoing issue of interoperability fragmentation and the technical burden of semantic standardization.

- A significant market challenge is ensuring regulatory compliance while managing increasingly complex systems. Integrating features like e-prescribing and computerized physician order entry requires robust data encryption and a well-defined application programming interface to prevent unauthorized access. The push for structured data capture and clinical documentation improvement adds another layer of complexity.

- Furthermore, streamlining revenue cycle management through medical billing automation and prior authorization automation demands constant vigilance to meet evolving payer rules and maintain a clean master patient index.

- Systems that automate prior authorization can reduce denial rates by up to 25%, and fully integrated e-prescribing has been shown to reduce medication errors by as much as 50%, highlighting the dual challenge of implementation and the rewards of success.

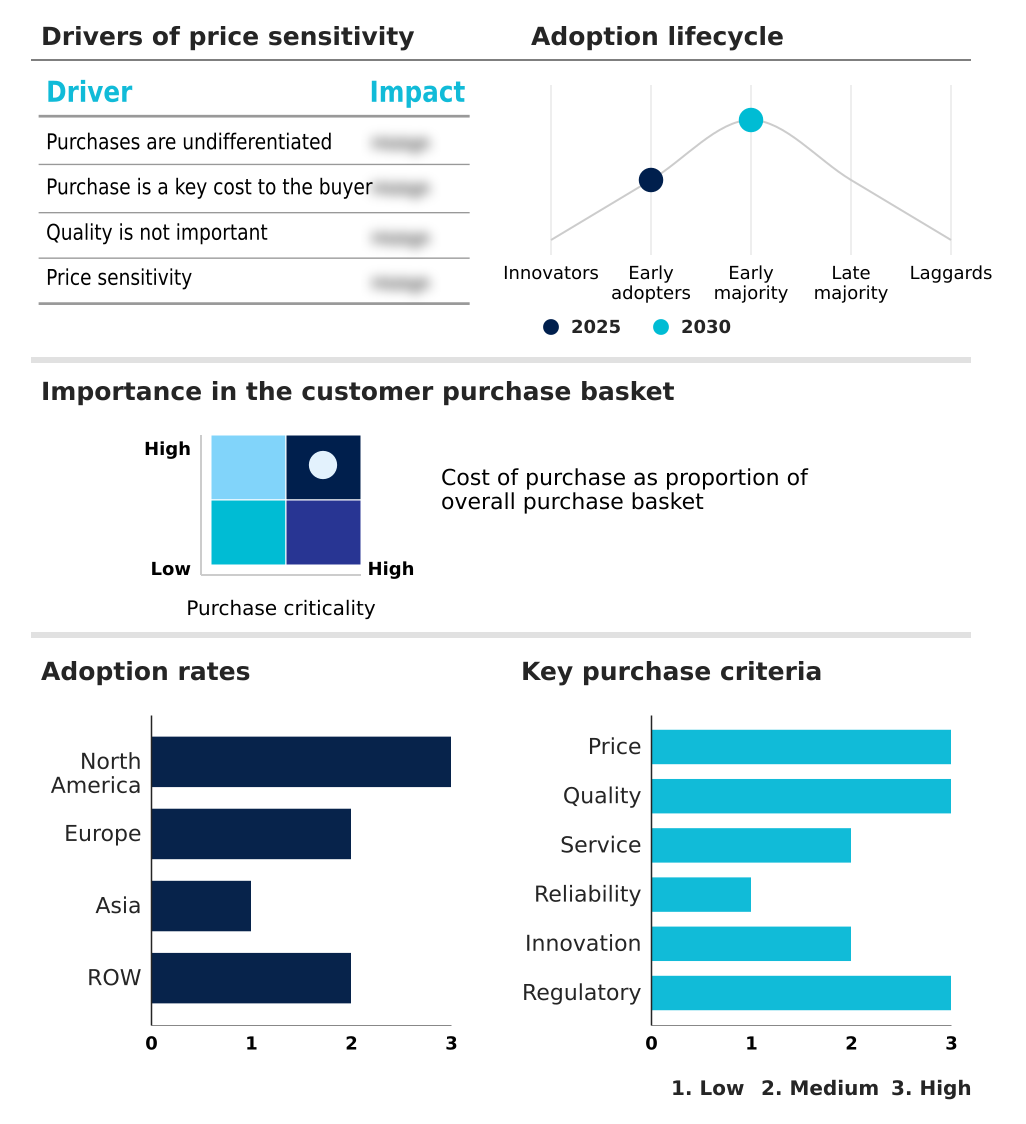

Exclusive Technavio Analysis on Customer Landscape

The electronic health records market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electronic health records market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electronic Health Records Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electronic health records market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AdvancedMD Inc. - Delivering unified cloud software for electronic health records, billing, and practice management to optimize workflows for independent medical practices.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AdvancedMD Inc.

- Altera Digital Health Inc

- Athenahealth Inc.

- Azalea Health Innovations Inc.

- CompuGroup Medical SE and Co.

- CureMD

- Dedalus Group

- DrChrono Inc.

- DXC Technology Co.

- eClinicalWorks LLC

- Epic Systems Corp.

- Flatiron Health

- Greenway Health LLC

- InterSystems Corp.

- Koninklijke Philips NV

- Medical Information Tech Inc.

- NextGen Healthcare

- Oracle Corp.

- Tietoevry Corp.

- TruBridge Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electronic health records market

- In August 2024, Avo partnered with MEDITECH to integrate its AI Scribe directly into the Expanse electronic health records platform, providing native ambient listening capabilities.

- In March 2025, Google officially launched its Medical Records APIs within the Health Connect platform, enabling secure, on-device access to standardized medical data for a new generation of health applications.

- In March 2025, the health authority Te Whatu Ora Health New Zealand launched the Shared Digital Health Records project, a national initiative to consolidate patient data into a unified platform.

- In March 2025, the formal publication of Regulation (EU) 2025/327 established the European Health Data Space, creating a harmonized legal and technical architecture for cross-border health data exchange.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electronic Health Records Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 287 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.1% |

| Market growth 2026-2030 | USD 57388.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, Turkey, UAE, Argentina, South Africa, Colombia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electronic health records market is defined by a strategic shift from static data repositories to dynamic, intelligent systems that enhance data liquidity. The adoption of cloud-native ehr architectures is central to this evolution, enabling greater semantic interoperability and the deployment of advanced health analytics.

- Leading platforms are embedding ambient clinical intelligence and natural language processing to automate clinical documentation improvement, directly addressing physician burnout. This technological pivot has boardroom implications, as investment decisions are increasingly tied to platforms that can demonstrate a direct impact on operational efficiency; for example, solutions offering clinical workflow automation can reduce documentation time by up to 40%.

- The integration of a predictive analytics engine and ai-driven diagnostics is becoming standard, supported by a robust cybersecurity framework and zero-trust architecture. As the industry moves toward value-based care reimbursement, the ability of a system to support population health management and provide a complete longitudinal patient record, compliant with the fhir standard, determines its long-term viability.

What are the Key Data Covered in this Electronic Health Records Market Research and Growth Report?

-

What is the expected growth of the Electronic Health Records Market between 2026 and 2030?

-

USD 57.39 billion, at a CAGR of 15.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud-based), Component (Services, Software, and Hardware), Type (Integrated, and Standalone) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of European health data space regulatory frameworks, Interoperability fragmentation and burden of semantic standardization

-

-

Who are the major players in the Electronic Health Records Market?

-

AdvancedMD Inc., Altera Digital Health Inc, Athenahealth Inc., Azalea Health Innovations Inc., CompuGroup Medical SE and Co., CureMD, Dedalus Group, DrChrono Inc., DXC Technology Co., eClinicalWorks LLC, Epic Systems Corp., Flatiron Health, Greenway Health LLC, InterSystems Corp., Koninklijke Philips NV, Medical Information Tech Inc., NextGen Healthcare, Oracle Corp., Tietoevry Corp. and TruBridge Inc.

-

Market Research Insights

- The market's dynamics are increasingly shaped by the pursuit of measurable efficiency and improved clinical outcomes. A clear trend is the adoption of integrated practice management tools, which have demonstrated a 15% reduction in administrative overhead for ambulatory care workflows. Concurrently, the focus on value-based care models is driving demand for platforms that support secure data exchange and cross-continuum communication.

- Systems that facilitate better care coordination have been linked to a 20% decrease in hospital readmission rates for patients with chronic conditions. The ability of a platform to provide real-time data access is now a key differentiator, with advanced systems improving information retrieval times by up to 30%, thereby enhancing diagnostic decision support and overall patient safety.

We can help! Our analysts can customize this electronic health records market research report to meet your requirements.

RIA -

RIA -