Medical Device Security Solutions Market Size 2024-2028

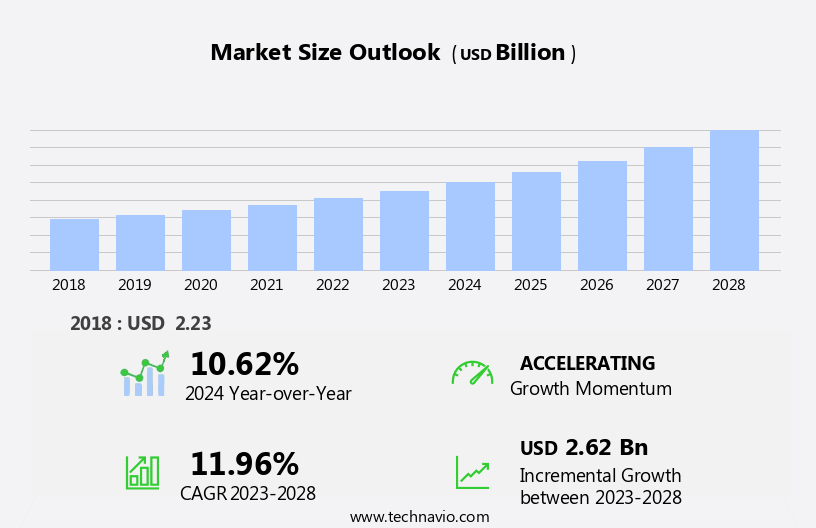

The medical device security solutions market size is forecast to increase by USD 2.62 billion, at a CAGR of 11.96% between 2023 and 2028.

- The market is experiencing significant growth, driven by increasing concerns about healthcare data security and the widespread adoption of Internet of Things (IoT) and connected devices in the healthcare industry. The healthcare sector's reliance on digital technologies and interconnected devices has led to a surge in data generation and exchange, necessitating robust security measures. However, the market faces challenges, including the use of outdated platforms in healthcare organizations. These legacy systems may lack adequate security features, making them vulnerable to cyber threats. As the healthcare industry continues to digitize, addressing these security challenges will be crucial for market participants to capitalize on the opportunities presented by the growing demand for secure medical device solutions.

- Companies must focus on developing innovative, secure solutions that cater to the unique needs of the healthcare sector while ensuring compliance with regulatory frameworks. Effective collaboration between healthcare providers, technology companies, and regulatory bodies will be essential to mitigate risks and protect sensitive patient data.

What will be the Size of the Medical Device Security Solutions Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve as healthcare organizations seek to safeguard their systems and data from cyber threats. Compliance standards, such as FDA regulations, mandate robust security measures for medical devices, driving innovation in this space. Security auditing and biometric authentication are becoming increasingly common for access control, while network security and data encryption are essential components of a comprehensive security architecture. IoT security is a growing concern, with multi-factor authentication (MFA) and secure coding practices essential to mitigate risks. Malware protection, behavioral analytics, and intrusion detection are integral to identifying and responding to threats in real-time.

AI in cybersecurity is revolutionizing threat intelligence, enabling predictive analysis and proactive measures. Risk management is a continuous process, with penetration testing, access control systems, and threat modeling essential to identify vulnerabilities and mitigate risks. Physical security, incident response, and disaster recovery are also crucial components of a holistic security strategy. Data integrity, software security, and blockchain security are essential to protect sensitive information, while patch management and vulnerability scanning help maintain system security. Wireless security, data loss prevention, and cloud security are critical considerations for modern healthcare organizations. The market dynamics of medical device security solutions are ever-changing, with new threats and regulatory requirements emerging constantly.

Staying informed and adhering to best practices is essential to maintaining a secure and compliant environment.

How is this Medical Device Security Solutions Industry segmented?

The medical device security solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Device

- Wearable and external medical devices

- Hospital medical devices

- Internally embedded medical devices

- End-user

- Healthcare providers

- Medical devices manufacturers

- Healthcare payers

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Device Insights

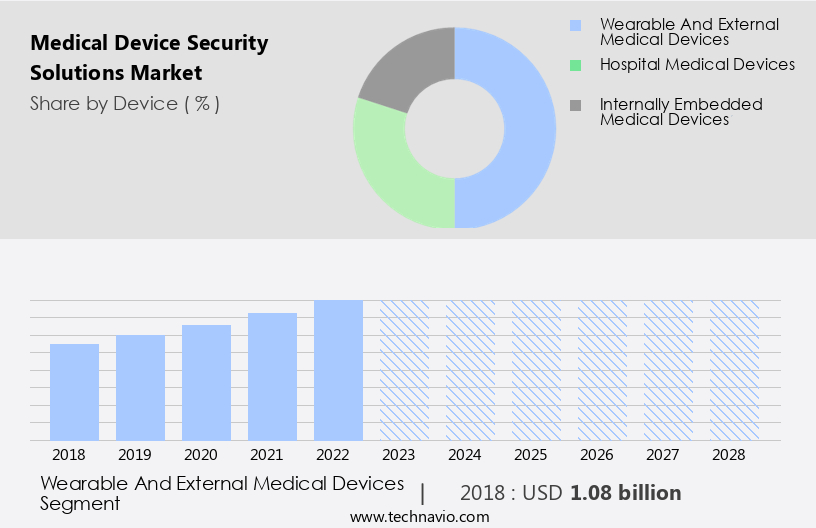

The wearable and external medical devices segment is estimated to witness significant growth during the forecast period.

The healthcare industry's digital transformation has led to the integration of advanced technologies such as IoT, artificial intelligence, and cybersecurity solutions to ensure data privacy and security. Medical devices have become increasingly connected, leading to a heightened need for robust network security, data encryption, and anomaly detection. Compliance with regulatory requirements, such as FDA regulations and HIPAA, is crucial. Biometric authentication and multi-factor authentication (MFA) have become essential for access control and risk management. Cybersecurity threats, including malware and intrusions, pose significant risks to medical devices and patient data. Therefore, healthcare organizations prioritize incident response, vulnerability scanning, and patch management.

Threat intelligence and penetration testing help identify and mitigate potential vulnerabilities. Access control systems, behavioral analytics, and surveillance systems ensure physical security. Data backup and disaster recovery are essential for business continuity. Software security, blockchain security, and security frameworks provide additional layers of protection. Wireless security and data loss prevention are crucial for securing remote patient monitoring and telemedicine services. Training employees on cybersecurity best practices is essential to mitigate human error and insider threats. The adoption of cloud security and vulnerability management helps healthcare organizations manage risks and respond to threats effectively. Threat modeling and risk assessment are crucial components of a comprehensive cybersecurity strategy.

The evolving cybersecurity landscape requires a holistic approach to medical device security, encompassing all aspects of security architecture, from hardware to software.

The Wearable and external medical devices segment was valued at USD 1.08 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

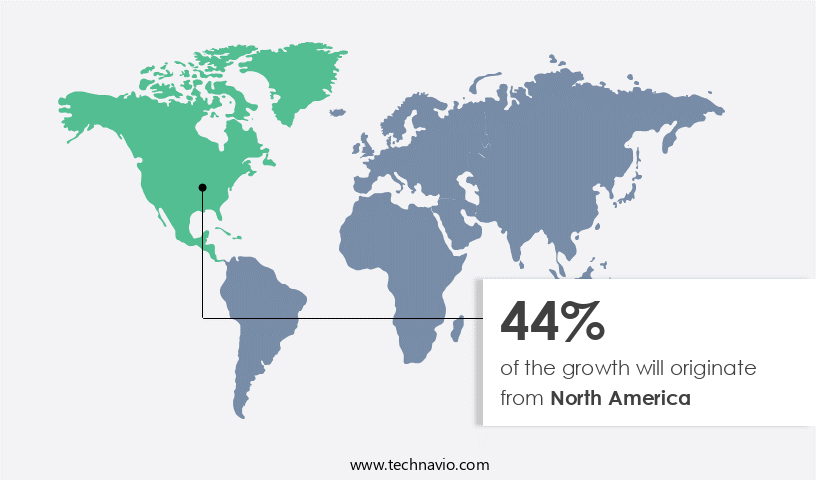

North America is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic healthcare landscape of North America, medical device security solutions have emerged as a critical priority. With the widespread adoption and integration of wired and wireless networked medical devices, the region leads the global market. Strict regulatory requirements, including FDA regulations, mandate robust security measures to protect sensitive patient data. These regulations, coupled with the increasing threat of cyberattacks on healthcare organizations, fuel the market's growth. In the US, the high adoption rate of technology in healthcare, a growing geriatric population, and the need for advanced healthcare facilities further boost market expansion. Security solutions encompass various elements, such as compliance standards, security auditing, biometric authentication, network security, data encryption, anomaly detection, authentication protocols, access control, security architecture, IoT security, and medical device security.

Advanced technologies like AI in cybersecurity, multi-factor authentication (MFA), secure coding practices, data backup, hardware security, embedded systems security, malware protection, employee awareness, intrusion detection, antivirus software, behavioral analytics, risk management, penetration testing, access control systems, threat intelligence, surveillance systems, physical security, incident response, vulnerability scanning, data integrity, security monitoring, patch management, disaster recovery, software security, blockchain security, security frameworks, wireless security, data loss prevention, risk assessment, cloud security, vulnerability management, threat modeling, and cybersecurity training are integral to this market. The evolving patterns reflect the industry's commitment to ensuring the highest level of patient care and data protection.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Medical Device Security Solutions Industry?

- The growing apprehensions regarding the security and privacy of healthcare data serve as the primary catalyst for market expansion in this sector.

- The market is experiencing significant growth due to the increasing number of cyberattacks in the healthcare industry and the resulting need for robust security measures. With the integration of data-generating devices and the centralization of data in the healthcare sector, there is a surge in big data, which is crucial for improving healthcare quality, gaining insights, and reducing costs. However, this data influx also presents challenges in terms of security and privacy. The healthcare industry's transition to digitizing workflows and electronic patient records necessitates advanced security solutions. Compliance with various regulatory requirements, such as HIPAA and GDPR, is essential to ensure data privacy and security.

- Security auditing, biometric authentication, network security, data encryption, anomaly detection, authentication protocols, access control, security architecture, and IoT security are critical components of medical device security solutions. These technologies help protect sensitive patient data, maintain regulatory compliance, and enhance overall healthcare security.

What are the market trends shaping the Medical Device Security Solutions Industry?

- The healthcare industry is witnessing an emerging trend towards the widespread adoption of IoT and connected devices. This includes the use of wearable technology, remote monitoring systems, and automated diagnostic tools. These innovations are enhancing patient care and improving operational efficiency within healthcare organizations.

- The market is experiencing significant growth due to the increasing adoption of IoT and connected medical devices in the healthcare industry. IoT infrastructure facilitates real-time patient monitoring, enhances accessibility to healthcare services, and reduces operational burdens on healthcare facilities. This digital transformation in healthcare is driving the demand for advanced security solutions to protect against potential cyber threats. To ensure medical device security, various measures are being implemented, including the use of AI in cybersecurity for threat detection, multi-factor authentication (MFA) for access control, secure coding practices, data backup, hardware security, embedded systems security, malware protection, employee awareness training, intrusion detection, and antivirus software.

- Behavioral analytics is another crucial aspect of medical device security, as it helps in identifying and responding to anomalous behavior that could indicate a cyber attack. The healthcare industry's shift towards digitalization and connected devices necessitates a robust security framework to protect sensitive patient data and maintain data privacy. The market for medical device security solutions is expected to continue growing as healthcare organizations invest in advanced security technologies to mitigate cyber risks and ensure the secure exchange of digital health information.

What challenges does the Medical Device Security Solutions Industry face during its growth?

- The use of outdated platforms in the healthcare industry poses a significant challenge to industry growth, necessitating the adoption of modern technologies to enhance efficiency and effectiveness in healthcare delivery.

- In the rapidly evolving healthcare landscape, the integration of advanced medical devices brings significant benefits but also introduces new risks. With the increasing use of connected medical devices, ensuring data integrity and security becomes paramount. However, the healthcare sector faces unique challenges, such as the prevalence of legacy systems and outdated devices, which increase vulnerabilities to cyberattacks. These vulnerabilities can have severe consequences, affecting not only the devices themselves but also the networks that connect them. To mitigate these risks, robust security solutions are essential. Threat intelligence, penetration testing, access control systems, vulnerability scanning, and patch management are crucial components of a comprehensive medical device security strategy.

- Surveillance systems and physical security measures are also vital in securing medical facilities and protecting patient data. Incident response plans and disaster recovery solutions are necessary to minimize the impact of potential breaches. Security monitoring and patch management are ongoing processes to ensure that systems remain up-to-date and protected against the latest threats. Data integrity is a top priority, as manipulation of critical infrastructure can directly impact human life. In conclusion, a multi-layered approach to medical device security is necessary to address the unique challenges faced by the healthcare industry. By implementing a combination of risk management, access control, threat intelligence, surveillance, patch management, incident response, and data integrity solutions, healthcare providers can safeguard their systems and protect patient data.

Exclusive Customer Landscape

The medical device security solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical device security solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, medical device security solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Battelle Memorial Institute - This company specializes in medical device security, providing innovative solutions such as Battelle DeviceSecure and employing expert cybersecurity professionals. They identify vulnerabilities and potential cyberattacks, ensuring the integrity and confidentiality of medical devices. Their offerings prioritize patient safety and data protection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Battelle Memorial Institute

- Broadcom Inc.

- Cisco Systems Inc.

- CLEARDATA

- Clearwater Security and Compliance LLC

- Coalfire Systems Inc.

- Device Authority

- Dragerwerk AG and Co. KGaA

- DXC Technology Co.

- Extreme Networks Inc.

- Forescout

- Fortinet Inc.

- General Electric Co.

- Imperva Inc.

- International Business Machines Corp.

- Koninklijke Philips N.V.

- Meditology Services LLC

- Palo Alto Networks Inc.

- Sophos Ltd.

- UL Solutions Inc.

- Check Point Software Technologies Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical Device Security Solutions Market

- In January 2024, MedSec, a leading cybersecurity firm specializing in medical devices, announced the launch of its new Medical Device Security Platform, designed to protect connected medical devices from cyber threats. The platform uses artificial intelligence and machine learning to detect and respond to vulnerabilities in real-time (MedSec press release).

- In March 2024, CyberArk, a global leader in privileged access security, entered into a strategic partnership with Medtronic, a medical technology company, to secure Medtronic's insulin pumps and cardiac devices. This collaboration aimed to improve security for millions of connected medical devices worldwide (CyberArk press release).

- In May 2024, Cisco Systems, a technology company, acquired Privo, a medical device security startup, for USD150 million. The acquisition strengthened Cisco's portfolio in the medical device security market and expanded its offerings to healthcare providers (Cisco Systems SEC filing).

- In April 2025, the U.S. Food and Drug Administration (FDA) issued a final rule requiring medical device manufacturers to implement cybersecurity risk management plans. The rule, which applies to both new and existing devices, aims to reduce vulnerabilities and protect patient safety (FDA press release).

Research Analyst Overview

- The market is experiencing significant growth, driven by the increasing use of connected medical devices and the sensitivity of patient data. To address the unique security challenges in this sector, providers offer various solutions, including secure firmware, security testing, and data encryption standards. Threat hunting, network segmentation, and software security assurance are essential for proactively identifying and mitigating risks. Incident response planning, data anonymization, and privacy protection are crucial for minimizing the impact of potential breaches. Access control lists, role-based access control, and device authentication ensure only authorized users can access sensitive information. Cloud security solutions, data governance, and security certifications help maintain regulatory compliance.

- Security orchestration, ethical hacking, and security architecture design enable effective threat intelligence and vulnerability remediation. Red teaming, security policy development, and secure communication protocols strengthen overall security posture. Security analytics, security automation, wireless network security, and secure remote access improve operational efficiency. Vulnerability management tools, intrusion prevention systems, attribute-based access control, advanced threat protection, and next-generation firewalls provide comprehensive security solutions for medical device manufacturers and healthcare organizations. Data masking and security policy development further enhance data protection. Overall, the market is evolving to meet the complex security needs of the healthcare industry, with a focus on zero trust security, endpoint security, secure boot, and next-generation technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Device Security Solutions Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.96% |

|

Market growth 2024-2028 |

USD 2.62 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.62 |

|

Key countries |

US, Japan, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Medical Device Security Solutions Market Research and Growth Report?

- CAGR of the Medical Device Security Solutions industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the medical device security solutions market growth of industry companies

We can help! Our analysts can customize this medical device security solutions market research report to meet your requirements.

RIA -

RIA -