Model Serving Platforms Market Size and Growth Forecast 2026-2030

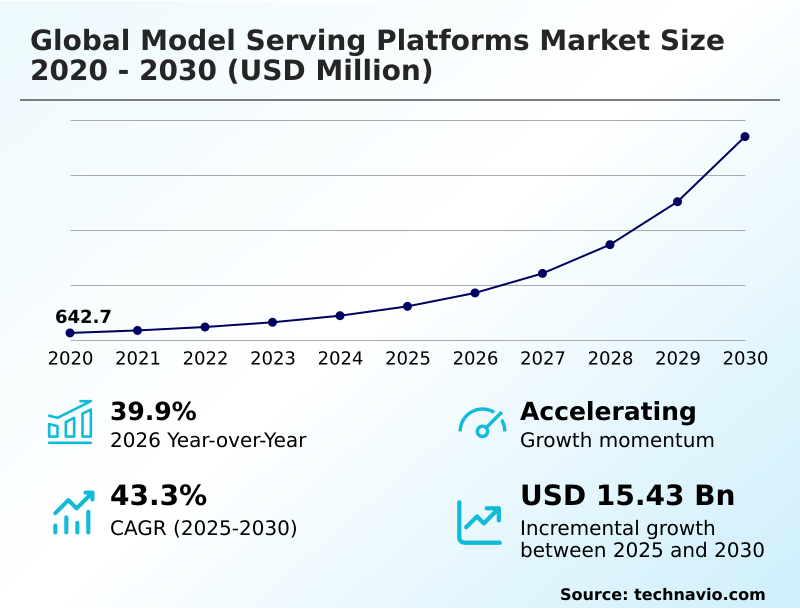

The Model Serving Platforms Market size was valued at USD 3.06 billion in 2025 growing at a CAGR of 43.3% during the forecast period 2026-2030.

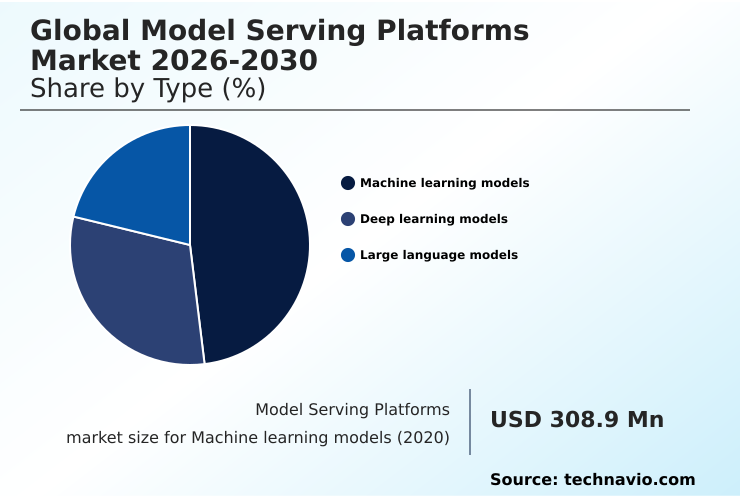

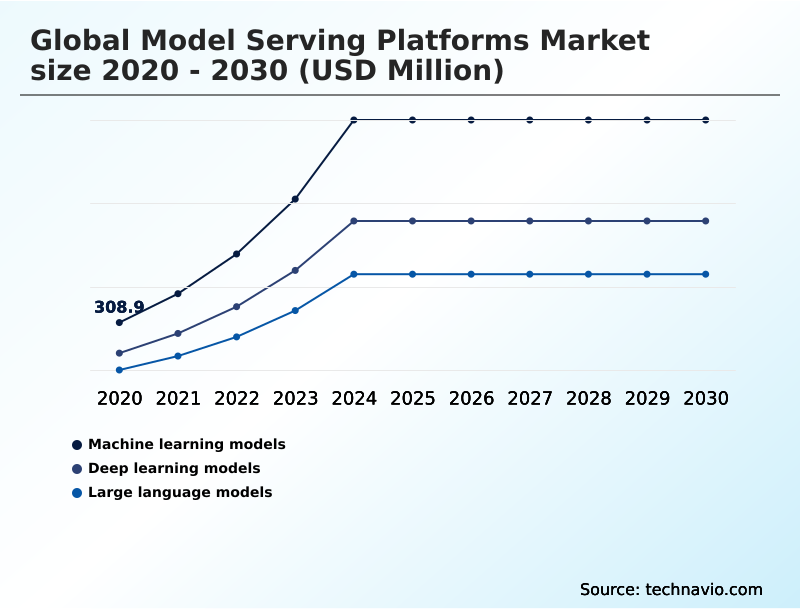

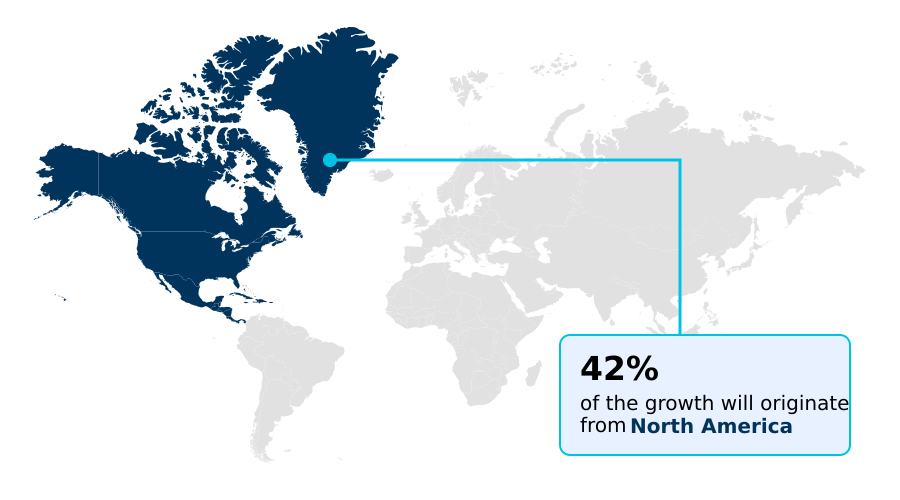

North America accounts for 41.6% of incremental growth during the forecast period. The Machine learning models segment by Type was valued at USD 1.05 billion in 2024, while the Cloud segment holds the largest revenue share by Deployment.

The market is projected to grow by USD 17.85 billion from 2020 to 2030, with USD 15.43 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Model Serving Platforms Market Overview

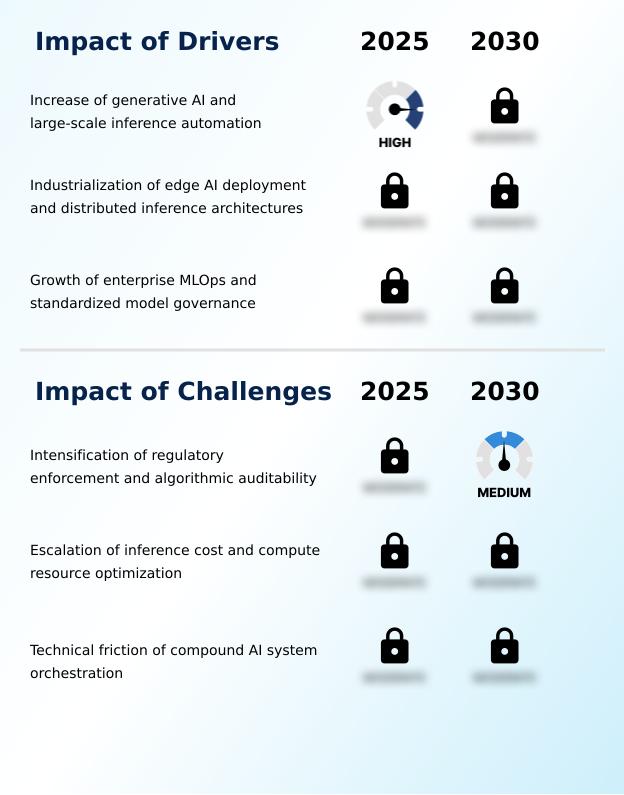

The model serving platforms market is defined by the industrialization of AI, as organizations move from experimental pilots to production systems requiring large-scale inference. This transition demands specialized cloud-native frameworks and a model-as-a-service paradigm to manage operational complexity. With year-over-year growth approaching 40%, driven largely by North America's 41.6% contribution to incremental growth, the focus is on achieving low-latency serving. For instance, a financial institution deploying real-time inference for fraud detection leverages multi-model endpoints to process millions of transactions, reducing false positives by over 30%. The increasing scrutiny on algorithmic auditability, guided by frameworks from bodies like the Federal Trade Commission, necessitates platforms with immutable audit logs and support for explainable AI modules. As the industry advances, the ability to support emerging agentic AI platforms and orchestrate compound AI systems will become a critical differentiator for vendors.

Drivers, Trends, and Challenges in the Model Serving Platforms Market

Procurement decision-makers are now focused on deploying large language models at scale, a task complicated by the need for managing inference costs for generative AI. This forces a critical comparison of cloud vs on-premises model serving, where the latter is gaining favor for building secure and sovereign AI infrastructure to protect intellectual property.

For specialized verticals, such as real-time model serving for financial services, ensuring AI model governance and compliance with mandates like the EU AI Act is non-negotiable. The operational solution often involves automating model deployment with enterprise MLOps, which integrates versioning and monitoring into CI/CD workflows.

For industrial use cases, optimizing model serving on edge devices is essential for applications like predictive maintenance and quality control. However, the rise of agentic frameworks creates challenges in orchestrating compound AI systems, where multiple models and data sources must interact seamlessly. To lower the technical barrier, low-code platforms for enterprise AI deployment are emerging.

The strategic importance of these decisions is amplified by the fact that inference can consume up to 80% of AI budgets, a figure that dwarfs typical IT infrastructure costs and elevates the role of FinOps in operational planning.

Primary Growth Driver: The rapid adoption of generative AI and the industrialization of large-scale inference automation are key drivers for the market.

Growth is primarily driven by generative AI automation and the strategic expansion of edge AI deployment.

The industrialization of large-scale inference for applications ranging from deep learning model serving to large language model deployment necessitates platforms offering high throughput and low latency.

This market is in an accelerating phase, with a projected CAGR of 43.3%, as enterprises require scalable distributed inference architectures.

The adoption of standardized technologies like API-first inference containers and Kubernetes for orchestration underpins this expansion, enabling organizations to manage complex AI workloads efficiently across hybrid and multi-cloud environments, thereby maximizing the utility of their AI investments.

Emerging Market Trend: The institutionalization of low-code frameworks is a primary market trend. This shift enables the deployment of no-code model architectures, democratizing access to AI.

Key market trends include the institutionalization of low-code model deployment and the expansion of sovereign model serving. The simplification of deployment through no-code MLOps and serverless inference functions allows business units to operationalize AI without deep engineering expertise, a trend particularly prominent in APAC, which is forecast to grow at a CAGR of 44.3%.

Concurrently, data residency compliance mandates, such as the framework established by the Indian AI Safety Institute, are driving demand for localized AI governance. This requires platforms that can guarantee data remains within national borders, a critical factor for government and regulated industries in Europe and Asia.

Key Industry Challenge: The intensification of regulatory enforcement and the growing requirement for algorithmic auditability present a primary challenge to industry growth.

Primary market challenges stem from escalating inference cost optimization pressures and the intensification of algorithmic auditability requirements. With inference now accounting for up to 80% of total AI budgets in many enterprises, the demand for sophisticated inference FinOps tools to manage expenses is acute.

Simultaneously, regulatory frameworks like the EU AI Act are compelling organizations to adopt standardized model governance, with nearly 70% of large firms now using formal checklists. This creates technical debt, as legacy systems must be retrofitted with explainable AI modules and immutable audit logs.

The increasing complexity of orchestrating compound AI systems further strains engineering resources, making robust model performance telemetry essential for operational stability.

Explore Full Market Dynamics Analysis Request Free Sample

Model Serving Platforms Market Segmentation

The model serving platforms industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Type Segment Analysis

The machine learning models segment is estimated to witness significant growth during the forecast period.

The machine learning models segment remains foundational for enterprise operations, handling high-frequency tasks like fraud detection and churn prediction using established predictive models.

Procurement decisions prioritize platforms offering robust automated a-b testing and comprehensive automated model monitoring to manage performance and mitigate drift.

While not as compute-intensive as deep learning model serving, this segment demands platforms that provide low-latency real-time inference and integrate seamlessly into enterprise mlops pipelines for continuous deployment.

The segment's scale, growing from a base of over 1,420 to nearly 2,000 between consecutive years, highlights its sustained importance. These platforms excel at model lifecycle management, ensuring the reliability required for business-critical functions and supporting complex predictive maintenance models.

The Machine learning models segment was valued at USD 1.05 billion in 2024 and showed a gradual increase during the forecast period.

Model Serving Platforms Market by Region: North America Leads with 41.6% Growth Share

North America is estimated to contribute 41.6% to the growth of the global market during the forecast period.

The geographic landscape is led by North America, which accounts for 41.6% of incremental growth, driven by hyperscale providers optimizing for low-latency serving and high-performance computing.

In contrast, APAC is the fastest-growing region, with a 44.3% CAGR, prioritizing edge AI deployment to support its mobile-first economies and smart city initiatives.

The European market is heavily influenced by regulations like GDPR and the EU AI Act, which fuels demand for sovereign model serving and platforms that ensure data residency compliance.

This regulatory pressure is fostering innovation in confidential serving nodes and localized AI governance frameworks across all developed regions.

This divergence creates a market where US-based firms focus on raw performance, while European and some APAC players prioritize auditable, secure, and compliant deployment architectures.

Customer Landscape Analysis for the Model Serving Platforms Market

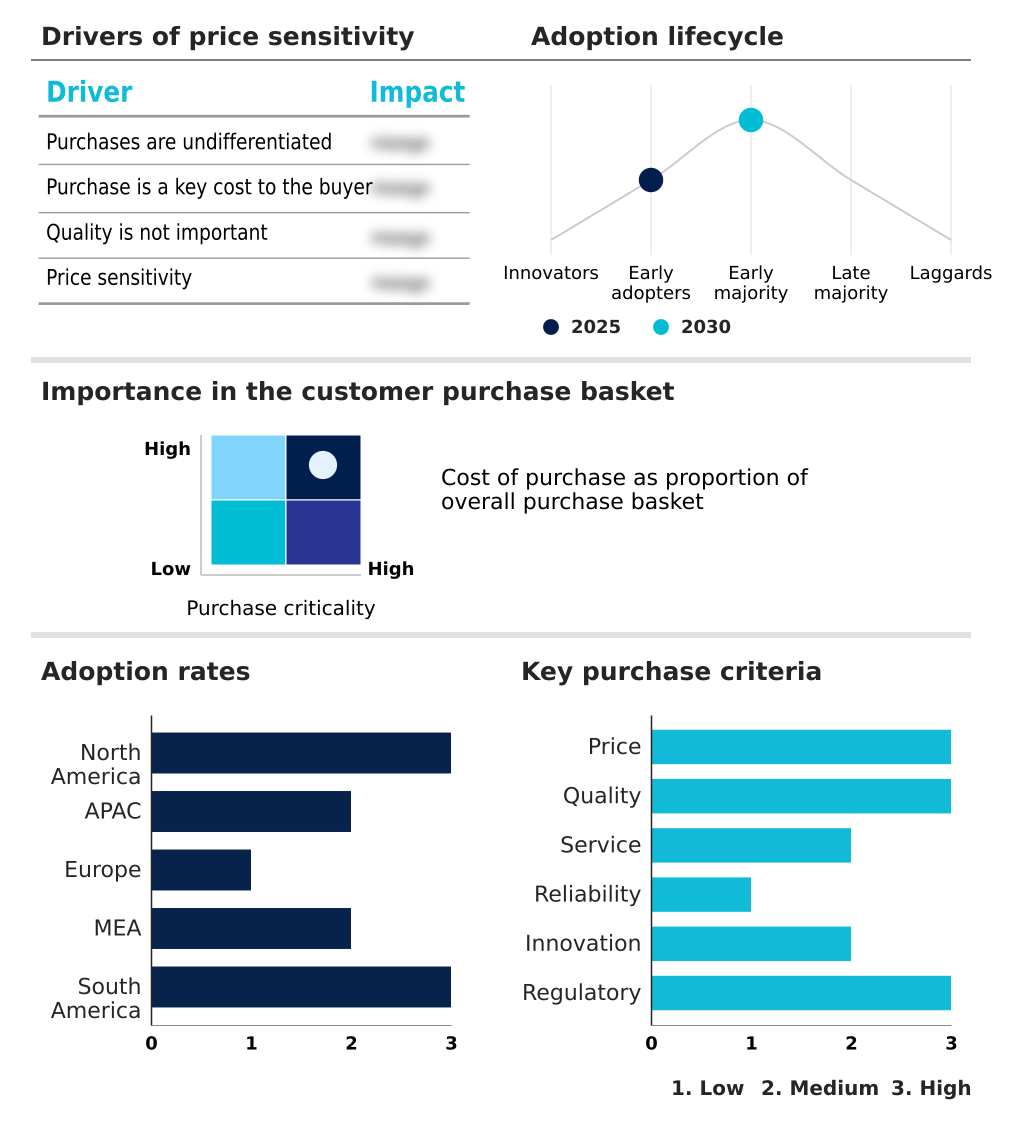

The model serving platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the model serving platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Model Serving Platforms Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the model serving platforms market industry.

Alibaba Cloud - Platforms enable scalable ML model deployment, featuring real-time inference, elastic compute resources, and seamless integration with cloud-native AI and big data services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon.com Inc.

- Anyscale Inc.

- Baidu Inc.

- Cloudera Inc.

- Databricks Inc.

- Dataiku Inc.

- DataRobot Inc.

- Domino Data Lab Inc.

- Google LLC

- H2O.ai Inc.

- Hugging Face Inc.

- IBM Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- SAS Institute Inc.

- Seldon Technologies

- Snowflake Inc.

- TIBCO Software Inc.

- Valohai Oy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Model Serving Platforms Market

- In May 2025, Latent Agent launched the industry's first agentic edge AI platform, designed to simplify and automate the deployment of intelligent agents across diverse hardware ecosystems without requiring manual model-to-hardware optimization.

- In April 2025, the Indian Ministry of Electronics and Information Technology inaugurated the AI Safety Institute with an initial funding of over USD 20 million to oversee the research and validation of models served within its national digital ecosystem.

- In March 2025, Databricks Inc. expanded its serverless model serving ecosystem by hosting the Google Gemini 3.1 Flash Lite model, enabling enterprise users to deploy high-efficiency, low-latency reasoning agents directly within their existing security perimeters.

- In January 2025, the Electronics and Telecommunications Research Institute released the TANGO framework, a no-code MLOps solution designed to automate neural network generation and deployment across cloud, Kubernetes, and on-premises environments.

Research Analyst Overview: Model Serving Platforms Market

The market is shifting toward autonomous, production-grade AI pipelines, where robust enterprise MLOps and standardized model governance are baseline requirements, not premium features. Deployment is consolidating around Kubernetes-native serving for container orchestration, essential for managing both deep learning model serving and large language model deployment.

A primary boardroom consideration is the total cost of ownership, as inference cost optimization becomes critical when compute can consume up to 80% of an AI project's budget.

Compliance with regulations like the EU AI Act is driving investment in explainable AI modules and platforms capable of automated model monitoring and automated drift detection to manage the full model lifecycle management. This scrutiny means generative AI automation cannot scale without verifiable and transparent operational guardrails.

Therefore, vendors that integrate seamless, auditable workflows for retrieval-augmented generation and other compound AI systems are best positioned for growth.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Model Serving Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 43.3% |

| Market growth 2026-2030 | USD 15433.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 39.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Model Serving Platforms Market: Key Questions Answered in This Report

-

What is the expected growth of the Model Serving Platforms Market between 2026 and 2030?

-

The Model Serving Platforms Market is expected to grow by USD 15.43 billion during 2026-2030, registering a CAGR of 43.3%. Year-over-year growth in 2026 is estimated at 39.9%%. This acceleration is shaped by increase of generative ai and large-scale inference automation, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Machine learning models, Deep learning models, and Large language models), Deployment (Cloud, and On premises), End-user (BFSI, IT and telecom, Healthcare, Manufacturing, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Machine learning models segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. North America is estimated to contribute 41.6% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increase of generative ai and large-scale inference automation, which is accelerating investment and industry demand. The main challenge is intensification of regulatory enforcement and algorithmic auditability, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Model Serving Platforms Market?

-

Key vendors include Alibaba Cloud, Amazon.com Inc., Anyscale Inc., Baidu Inc., Cloudera Inc., Databricks Inc., Dataiku Inc., DataRobot Inc., Domino Data Lab Inc., Google LLC, H2O.ai Inc., Hugging Face Inc., IBM Corp., Microsoft Corp., NVIDIA Corp., Oracle Corp., SAS Institute Inc., Seldon Technologies, Snowflake Inc., TIBCO Software Inc. and Valohai Oy. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Model Serving Platforms Market Research Insights

Market dynamics are shaped by the tension between performance demands and financial realities. The need for high-speed interconnects and terabit serving architectures to support high-frequency applications is balanced against the strategic imperative for GPU resource optimization. A key vendor qualification criterion is now multi-cloud compatibility, allowing enterprises to avoid lock-in and leverage hybrid cloud orchestration for cost and latency benefits.

In manufacturing, the deployment of predictive maintenance models on edge devices illustrates this balance, where localized processing must comply with data residency standards like GDPR. Furthermore, the push for sovereign model serving is reshaping procurement, demanding platforms that can guarantee data locality.

North America's market contribution, which is over 1.4 times that of APAC, highlights the advanced adoption in regions with mature cloud infrastructure, though APAC's rapid growth indicates a closing gap.

We can help! Our analysts can customize this model serving platforms market research report to meet your requirements.

RIA -

RIA -