Non-Ferrous Castings Market Size 2025-2029

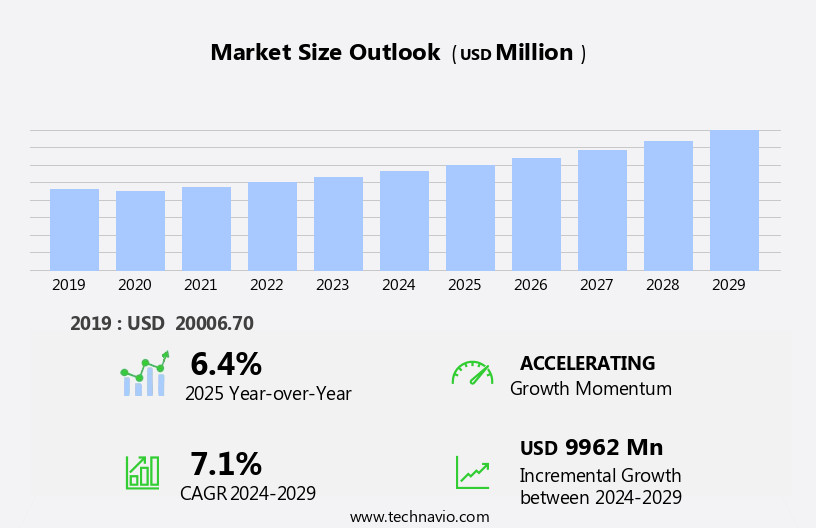

The non-ferrous castings market size is forecast to increase by USD 9.96 billion, at a CAGR of 7.1% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing adoption of simulation-based castings for improved efficiency and productivity. This trend is accompanied by a shift from ferrous to non-ferrous casting materials, as non-ferrous alloys offer superior properties for various applications. Furthermore, innovation leadership is a key driver, with ongoing advancements in high-strength alloys, casting simulation, and advanced materials such as titanium and magnesium. However, this market is not without challenges. Maintaining quality control and addressing defects in non-ferrous castings remains a significant obstacle. Producers must invest in advanced technologies and processes to ensure consistency and reliability in their products. Effective management of these challenges will be crucial for companies seeking to capitalize on the opportunities presented by the growing demand for non-ferrous castings.

- By focusing on innovation and quality, market participants can differentiate themselves and gain a competitive edge in this dynamic market. The market trends also reflect an increasing focus on casting finishing techniques, automation, and defect reduction, ensuring the production of high-quality castings.

What will be the Size of the Non-Ferrous Castings Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market encompasses a diverse range of materials and processes, including casting material selection, semi-permanent mold casting, ceramic shell casting, lost wax casting, permanent mold casting, green sand casting, and various other techniques. Market competition intensifies as industry certifications, such as ISO and AFS, become increasingly important for ensuring casting quality control. Casting process optimization, driven by advancements in casting technology, plays a crucial role in enhancing production capacity and reducing casting costs. Simultaneously, casting industry standards continue to evolve, necessitating the adoption of casting design software and foundry automation systems.

- Vacuum casting and precision casting are gaining popularity due to their ability to produce high-quality, defect-free castings. Casting process selection, influenced by industry regulations, is a critical factor in the competitive landscape. Casting simulation software facilitates process optimization, enabling foundries to stay ahead in the market.

How is this Non-Ferrous Castings Industry segmented?

The non-ferrous castings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Aluminum

- Copper

- Zinc

- Magnesium

- Others

- Application

- Automobiles

- Electrical and construction

- Industrial machinery

- Others

- Manufacturing Type

- Sand casting

- Die casting

- Investment casting

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Middle East and Africa

- Turkey

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

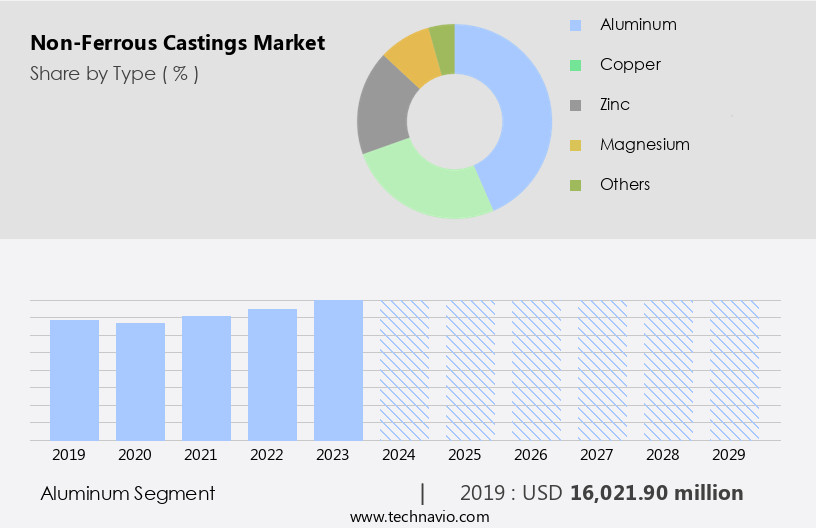

By Type Insights

The aluminum segment is estimated to witness significant growth during the forecast period. In the dynamic market, aluminum castings hold a dominant position, accounting for over 82% of the share. This dominance can be attributed to the surging demand from the automotive industry and manufacturing sectors for lightweight components. Aluminum castings are increasingly replacing traditional materials like gray iron in the production of automotive parts, particularly in cylinder blocks. The automotive sector's significant growth is driven by the industry's ongoing weight reduction strategy, with aluminum's use becoming increasingly prevalent. Other non-ferrous metals like magnesium, copper, nickel, and zinc also find extensive applications in various industries, including construction equipment, aerospace, and consumer products.

Innovations in casting design, molds, and simulation, as well as advancements in casting equipment and process optimization, are driving market growth. Additionally, the demand for high-performance casting alloys with enhanced properties, such as corrosion resistance, yield strength, and tensile strength, is fueling market expansion.

The Aluminum segment was valued at USD 16.02 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

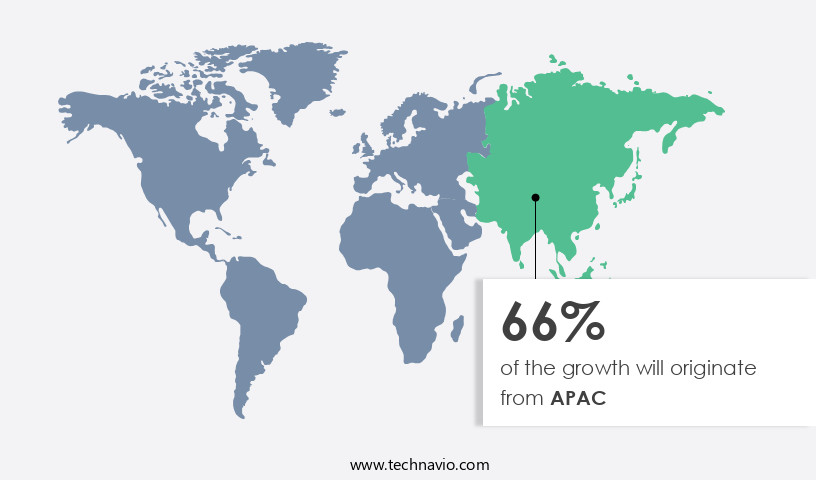

APAC is estimated to contribute 66% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth in major end-user industries, particularly in Asia Pacific (APAC), where economic expansion is driving demand. In the financial year 2023-24, India exported approximately USD 4.11 billion worth of castings, with non-ferrous castings comprising a substantial portion. The automotive sector in APAC is thriving, with India, Indonesia, Thailand, and Vietnam leading the way. However, China's demand is decreasing due to recent economic instability. The automotive industry's growing demand for casting components is fueled by the increasing production of motor vehicles in APAC. Non-ferrous castings' properties, such as thermal conductivity, yield strength, and corrosion resistance, make them essential in various industries.

Aluminum and magnesium castings are widely used in automotive components due to their lightweight and high strength. Gravity casting, sand casting, and investment casting are popular methods for producing these castings. Heat treatment and casting alloys enhance casting properties, while surface finishing ensures the desired appearance and performance. Casting simulation and innovation have streamlined the casting process, optimizing casting process parameters and reducing defects. Foundry operations have embraced automation and casting patterns to improve efficiency and consistency. Casting standards ensure product quality and safety. Wear resistance is a critical factor in the casting industry, particularly in industries such as construction equipment and aerospace components.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Non-Ferrous Castings market drivers leading to the rise in the adoption of Industry?

- Simulation-based castings have emerged as a significant driving force in the market, with increased adoption contributing to its growth. Non-ferrous metal casting is a critical process in manufacturing industries, particularly for producing components from aluminum and magnesium alloys. Advanced simulation-based casting technology plays a significant role in this process, enabling a virtual representation of the casting process, including mold filling, cooling, and solidification. This technology aids in predicting and identifying internal defects, optimizing casting design and process methods, and ensuring the production of economical, reliable, and high-accuracy cast components. The adoption of simulation-based casting is driven by the increasing demand for precise casting with specific dimensions, size, and weight requirements.

- Casting equipment manufacturers continue to invest in research and development to improve casting properties through heat treatment and casting alloys. Surface finishing techniques are also essential for enhancing the aesthetic and functional properties of non-ferrous castings. Overall, the integration of advanced technologies in non-ferrous casting processes is crucial for maintaining competitiveness and meeting the evolving needs of end-users.

What are the Non-Ferrous Castings market trends shaping the Industry?

- The transition from ferrous to non-ferrous casting is gaining momentum in the market. This shift reflects a growing demand for lighter, more corrosion-resistant materials in various industries. The market has experienced significant growth due to the increasing demand for lightweight and corrosion-resistant materials in various industries. Aluminum castings, in particular, have gained popularity due to their superior properties, including high yield strength and conductivity. The automotive sector, for instance, is transitioning from cast iron engine blocks to aluminum engine blocks to enhance product quality and efficiency. This shift is driven by the need to reduce overall weight and improve fuel efficiency. Additionally, industries such as telecommunications and industrial machinery are also adopting non-ferrous castings, like zinc and magnesium, to manufacture components with enhanced performance and durability.

- Casting techniques, such as sand casting, pressure casting, and lost foam casting, are being employed to produce these high-performance castings. Furthermore, advanced technologies like casting simulation and casting finishing are being utilized to ensure precise casting specifications and improve overall product quality.

How does Non-Ferrous Castings market face challenges during its growth?

- Maintaining quality control and addressing defects are significant challenges that can hinder industry growth. These concerns necessitate continuous focus and effective solutions to ensure product excellence and customer satisfaction. Non-ferrous casting involves intricate processes, from mold preparation to metal pouring and cooling, each stage introducing potential defects. The use of non-ferrous alloys, which can exhibit material property variability, further complicates matters. Inconsistent material properties necessitate rigorous material testing and quality assurance measures to prevent casting defects. Complex casting designs increase the likelihood of defects, making it essential to ensure design manufacturability and compatibility with the chosen casting process. The quality of the mold is paramount, as it significantly impacts the casting process outcome. Casting process optimization is crucial to mitigate defects and maintain consistent quality.

- Non-ferrous castings find extensive applications in various industries, including automotive components, medical devices, and investment casting. Bronze and copper castings are popular choices due to their excellent tensile strength and resistance to corrosion. Casting automation and inspection technologies have significantly improved casting quality and efficiency. Despite these advancements, addressing casting defects remains a key challenge in the non-ferrous casting market.

Exclusive Customer Landscape

The non-ferrous castings market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the non-ferrous castings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, non-ferrous castings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alcast Co. - The company specializes in the production of non-ferrous castings. Our expertise encompasses commercial non-ferrous castings, utilizing advanced techniques to ensure superior quality and consistency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcast Co.

- Alcast Technologies Ltd.

- CAB Worldwide

- Elecon Engineering Co. Ltd.

- FSE Foundry Ltd.

- Georg Fischer Ltd.

- Inova Cast Pvt. Ltd.

- Kovolit

- Leitelt Brothers Inc.

- Meena Cast Pvt. Ltd.

- MRT Castings Ltd.

- Nap Engineering Works

- Patriot Foundry

- Rukmani Non- Ferrous Industries

- spectra cast pvt. ltd.

- Toyota Motor Corp.

- Vellan Global

- Vesuvius Plc

- voestalpine AG

- Warner Brothers Foundry Company

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Non-Ferrous Castings Market

- In March 2024, Alcoa Corporation, a leading non-ferrous castings producer, announced the launch of its new line of aluminum engine blocks for the automotive industry, marking a significant stride in lightweighting and sustainability (Alcoa Corporation Press Release, 2024).

- In November 2024, Tenaris S.A., a major steel tubes and related services company, completed the acquisition of Allegheny Technologies Incorporated's (ATI) non-ferrous foundry business, significantly expanding its non-ferrous castings capabilities and market presence (Tenaris S.A. Press Release, 2024).

- In January 2025, the European Union passed new regulations on the recycling of non-ferrous metals, which will boost the demand for non-ferrous castings in the region due to the increased focus on circular economy and sustainable manufacturing (European Parliament and Council of the European Union, 2025).

Research Analyst Overview

The market continues to evolve, driven by the diverse applications across various sectors. Casting patterns and their resulting properties, such as tensile strength and corrosion resistance, are paramount in determining the suitability of non-ferrous castings for specific industries. Bronze castings, known for their excellent tensile strength and thermal conductivity, find extensive use in automotive components and construction equipment. Casting defects, however, can impact the quality and performance of these castings, necessitating rigorous casting process optimization. Copper castings, with their superior electrical conductivity, are integral to the electrical industry, while investment casting is a preferred method for producing intricate shapes in aerospace components and medical devices.

The Non-Ferrous Castings Market is evolving with advancements in casting technology, such as shell molding and gravity die casting, improving efficiency and precision. Thorough casting defect analysis ensures quality, while increased casting production capacity meets growing industrial demand. Casting market segmentation highlights diverse applications, driving casting industry competition. Compliance with casting industry regulations and obtaining casting industry certifications are crucial for maintaining standards. The market thrives on casting innovation, integrating 3D printing to enhance designs. Materials like brass castings and iron castings play key roles, supported by reliable casting molds and casting cores. Emerging casting industry trends shape future developments, ensuring sustainable growth and technological progress in non-ferrous metal casting solutions worldwide.

Casting automation and innovation are key trends shaping the industry, with advancements in casting simulation and finishing techniques enhancing efficiency and productivity. Casting applications span beyond automotive and construction, encompassing consumer products, foundry operations, and even the production of specialized components in the aerospace and healthcare sectors. Magnesium and nickel castings, with their unique properties, cater to specific industries, such as the automotive and heavy machinery sectors, respectively. Casting inspection plays a crucial role in ensuring the quality and consistency of non-ferrous castings, with continuous casting and die casting processes requiring stringent monitoring to maintain casting tolerances. The evolving nature of the market necessitates ongoing research and development efforts to address the ever-changing demands of various industries.

Casting alloys, such as aluminum, brass, zinc, and iron, offer unique properties that cater to specific applications. Heat treatment and surface finishing techniques further enhance the performance and durability of these castings. Lost foam casting and centrifugal casting are alternative casting processes that offer advantages in terms of cost and complexity. The market is a dynamic and intricate ecosystem, with ongoing research and innovation shaping its future. The continuous unfolding of market activities and evolving patterns underscore the importance of adaptability and flexibility in the industry.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Non-Ferrous Castings Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

233 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.1% |

|

Market growth 2025-2029 |

USD 9.96 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.4 |

|

Key countries |

China, US, India, Japan, Germany, Canada, Mexico, Italy, France, and Turkey |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Non-Ferrous Castings Market Research and Growth Report?

- CAGR of the Non-Ferrous Castings industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the non-ferrous castings market growth of industry companies

We can help! Our analysts can customize this non-ferrous castings market research report to meet your requirements.

RIA -

RIA -