North America Ambulatory Surgical Centers Software Market Size 2024-2028

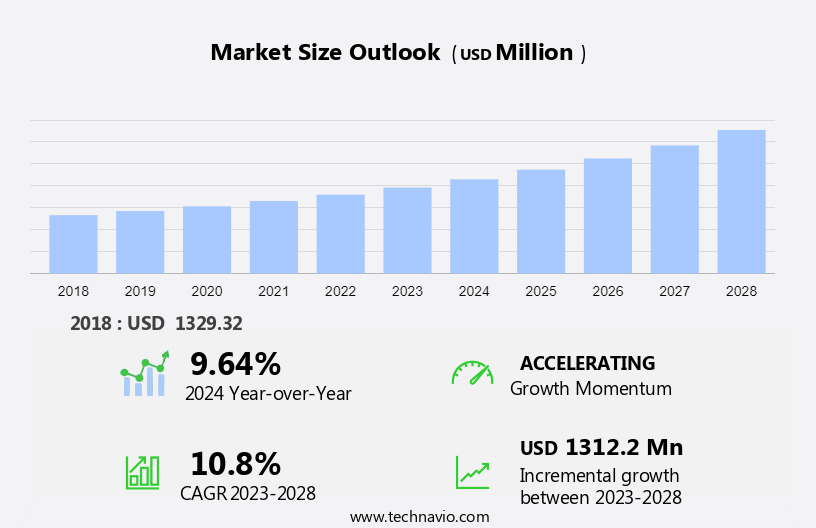

The North America ambulatory surgical centers software market size is forecast to increase by USD 1.31 billion, at a CAGR of 10.8% between 2023 and 2028.

- The Ambulatory Surgical Centers (ASC) Software Market in North America is driven by the increasing prevalence of chronic diseases, which necessitates efficient and effective healthcare management solutions. ASC software plays a crucial role in streamlining operations, improving patient outcomes, and reducing costs. Another significant factor fueling market growth is the emphasis on patient satisfaction and engagement, as ASCs strive to provide personalized care and enhance the overall patient experience. Furthermore, substantial investments in ASC software are being made to improve operational efficiency, ensure regulatory compliance, and leverage advanced technologies such as telemedicine and artificial intelligence. However, the market faces challenges including data security concerns, interoperability issues, and the high cost of implementation and maintenance.

- To capitalize on market opportunities and navigate challenges effectively, companies must focus on addressing these obstacles through robust security measures, seamless integration with existing systems, and cost-effective solutions. By prioritizing these areas, market participants can differentiate themselves and gain a competitive edge in the dynamic and evolving ASC Software Market in North America.

What will be the size of the North America Ambulatory Surgical Centers Software Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

- The North American ambulatory surgical centers (ASC) software market is experiencing significant growth, driven by the need for advanced solutions to streamline clinical documentation, enhance staff communication, and improve patient feedback systems. Surgical scheduling software and surgical reporting tools are essential components, enabling operational efficiency and regulatory compliance. Performance improvement is facilitated through integrated electronic health records (EHR) systems, secure data storage, and revenue cycle automation. Anesthesia management, medical billing, and medical coding systems ensure financial reporting accuracy. Health information exchange and appointment management systems foster seamless patient data access and engagement.

- Remote access capabilities and inventory control systems further enhance operational efficiency. Surgical workflow optimization is achieved through surgical data analysis and electronic claims submission. Patient check-in kiosks, physician communication tools, and discharge planning software contribute to a positive patient experience. Robust security measures prioritize patient data security, while compliance with regulatory standards is maintained.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Software

- Services

- Deployment

- Cloud

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- North America

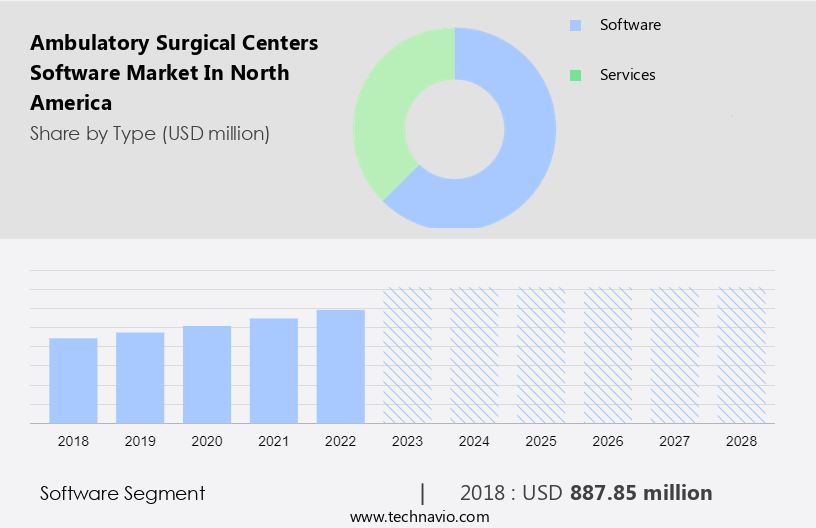

By Type Insights

The software segment is estimated to witness significant growth during the forecast period.

In the North American Ambulatory Surgical Centers (ASC) software market, various solutions cater to the unique requirements of ASCs, encompassing administrative and operational management, clinical documentation, and patient engagement. These software solutions optimize diverse aspects of ASC operations, boosting efficiency, enhancing patient care, and ensuring regulatory compliance. One prominent software category in the ASC market is Electronic Health Records (EHR) systems. EHR software facilitates the digitization and centralization of patient medical records, enabling secure access to essential patient information, including treatment histories and diagnostic results. By implementing EHR software, ASCs can streamline documentation processes, coordinate care more effectively, and bolster patient safety.

Additionally, ASC software solutions encompass electronic prescribing, staff scheduling, claims processing, appointment reminder systems, telehealth integration, data encryption protocols, HIPAA compliance software, surgical workflow optimization, medical billing codes, surgical inventory management, operating room scheduling, medical device tracking, performance tracking metrics, patient satisfaction surveys, patient scheduling systems, anesthesia record keeping, physician credentialing, post-operative care software, data analytics dashboards, patient communication tools, procedure documentation, revenue cycle management, insurance verification, appointment confirmations, patient portal integration, surgical case management, compliance reporting tools, secure messaging platforms, remote patient monitoring, cloud-based ambulatory software, surgical billing software, and pre-operative assessments. These software solutions contribute significantly to the evolving ASC landscape by addressing the complex needs of ASCs, ultimately improving operational performance and patient outcomes.

The Software segment was valued at USD 887.85 million in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the North America Ambulatory Surgical Centers Software Market drivers leading to the rise in adoption of the Industry?

- The increasing prevalence of chronic diseases serves as the primary driver for market growth in this sector.

- The North American Ambulatory Surgical Centers (ASC) software market is experiencing significant growth due to the increasing prevalence of chronic diseases in the region. Chronic conditions like diabetes, cardiovascular diseases, and obesity are becoming more common, leading to a higher demand for efficient and accessible healthcare services. ASCs offer an ideal solution by providing outpatient surgical procedures for managing these conditions, allowing patients to receive timely and specialized care while minimizing disruption to their daily lives. To cater to this growing demand, ASCs are investing in advanced software solutions designed specifically for their needs. These software solutions include electronic prescribing, staff scheduling, claims processing, appointment reminder systems, telehealth integration, data encryption protocols, and HIPAA compliance software.

- Additionally, surgical workflow optimization and medical billing codes are essential features that ASC software must offer to streamline operations and ensure accurate billing. ASC software plays a crucial role in optimizing the delivery of outpatient surgical care, enhancing patient experience, and improving operational efficiency. By implementing these advanced software solutions, ASCs can reduce wait times, minimize errors, and improve overall patient outcomes.

What are the North America Ambulatory Surgical Centers Software Market trends shaping the Industry?

- Focusing on patient satisfaction and engagement is a key trend in the current market. It is essential for healthcare providers to prioritize these aspects to deliver high-quality care and improve patient outcomes.

- The North American Ambulatory Surgical Centers (ASC) software market is experiencing significant growth due to the increasing prioritization of patient satisfaction and engagement. Healthcare providers recognize the importance of delivering superior patient experiences, leading them to adopt software solutions that streamline processes, enhance communication, and personalize care delivery. These solutions optimize the patient journey by offering features such as online appointment scheduling, surgical inventory management, operating room scheduling, medical device tracking, performance tracking metrics, patient scheduling systems, electronic health records, anesthesia record keeping, and more.

- By minimizing wait times and improving access to care, ASC software enables a positive patient experience from scheduling to discharge, thereby increasing patient satisfaction.

How does North America Ambulatory Surgical Centers Software Market faces challenges face during its growth?

- A significant investment in Advanced Surgical Center (ASC) software poses a crucial challenge to the industry's growth trajectory. This financial commitment necessitates careful consideration and strategic planning to ensure optimal returns and sustainable expansion.

- The Ambulatory Surgical Centers (ASC) software market in North America faces significant growth challenges due to the high cost of investment. Implementing robust software solutions for areas such as physician credentialing, post-operative care, data analytics dashboard, patient communication tools, procedure documentation, revenue cycle management, insurance verification, appointment confirmations, and patient portal integration requires substantial financial resources. These expenses include software licensing, customization, implementation, training, and ongoing maintenance. For smaller ASCs or those operating on tight budgets, the upfront investment can be a significant barrier. Perceived risks associated with technology investments and uncertainty surrounding return on investment further exacerbate reluctance to commit to costly software solutions.

- Despite these challenges, the benefits of advanced software platforms, such as improved operational efficiency, enhanced patient care, and streamlined revenue cycle management, make them an attractive proposition for many ASCs.

Exclusive North America Ambulatory Surgical Centers Software Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Data Systems Corp.

- AdvancedMD Inc.

- ALLSCRIPTS HEALTHCARE SOLUTIONS INC.

- AMSURG

- athenahealth Inc.

- CureMD

- eClinicalWorks LLC

- EverCommerce Inc.

- GE Healthcare Technologies Inc.

- HCA Healthcare Inc.

- Healthcare Systems and Technologies LLC

- McKesson Corp.

- Meditab Software Inc.

- NextGen Healthcare Inc.

- Optum Inc.

- Oracle Corp.

- SCA health

- Surgical Information Systems

- Tebra Technologies Inc.

- Weave Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ambulatory Surgical Centers Software Market In North America

- In January 2024, Meditech, a leading healthcare IT company, announced the launch of its new Ambulatory Care Solution, which includes advanced software for managing operations at ambulatory surgical centers (ASCs). This solution aims to streamline workflows, enhance patient care, and improve financial performance for ASCs (Meditech Press Release, 2024).

- In March 2024, KLAS Research reported that GE Healthcare's Centricity Perioperative solution had gained significant market share in the North American ASC software market due to its user-friendly interface and strong customer support (KLAS Research Report, 2024).

- In April 2025, Cerner Corporation, a prominent health IT provider, entered into a strategic partnership with Surgical Information Systems (SIS), a leading ASC software company. The partnership aimed to integrate Cerner's Millennium electronic health record (EHR) system with SIS's ASC software, enhancing interoperability and data exchange between the two platforms (Cerner Press Release, 2025).

- In May 2025, McKesson Corporation, a Fortune 500 company, completed its acquisition of RelayHealth, a healthcare IT solutions provider specializing in revenue cycle management and connectivity solutions. This acquisition was expected to bolster McKesson's ambulatory offerings, including its ASC software solutions, and expand its reach in the North American market (McKesson Press Release, 2025).

Research Analyst Overview

The ambulatory surgical centers (ASC) software market in North America is characterized by continuous evolution and dynamic market activities. Seamlessly integrated solutions are increasingly adopted to optimize surgical workflows, enhance patient care, and improve operational efficiency. Surgical inventory management systems enable real-time tracking of supplies, ensuring their availability for procedures. Operating room scheduling software facilitates efficient allocation of resources, reducing wait times and enhancing patient satisfaction. Medical device tracking solutions ensure accurate and timely maintenance, while performance tracking metrics provide valuable insights into center performance. Patient satisfaction surveys offer valuable feedback, helping centers improve their services. Patient scheduling systems streamline appointment scheduling, reducing administrative burden.

Electronic health records (EHRs) facilitate seamless sharing of patient information among healthcare providers. Anesthesia record keeping solutions ensure accurate and comprehensive documentation, contributing to improved patient safety. Surgical center management software offers comprehensive functionality, from admission to discharge. Compliance reporting tools ensure adherence to regulatory requirements, such as HIPAA. Advancements in technology continue to shape the market, with cloud-based ambulatory software gaining popularity for its flexibility and scalability. Telehealth integration, remote patient monitoring, and data analytics dashboards are increasingly adopted to enhance patient care and improve operational efficiency. The market is further characterized by the integration of various tools, such as patient communication, revenue cycle management, and secure messaging platforms.

The integration of physician credentialing, post-operative care software, procedure documentation, insurance verification, appointment confirmations, patient portal integration, surgical case management, and compliance reporting tools further enhances the functionality of ASC software. The ongoing evolution of technology and market dynamics continue to shape the market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ambulatory Surgical Centers Software Market in North America insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

143 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.8% |

|

Market growth 2024-2028 |

USD 1312.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.64 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -