North America Seismic Survey Market Size 2024-2028

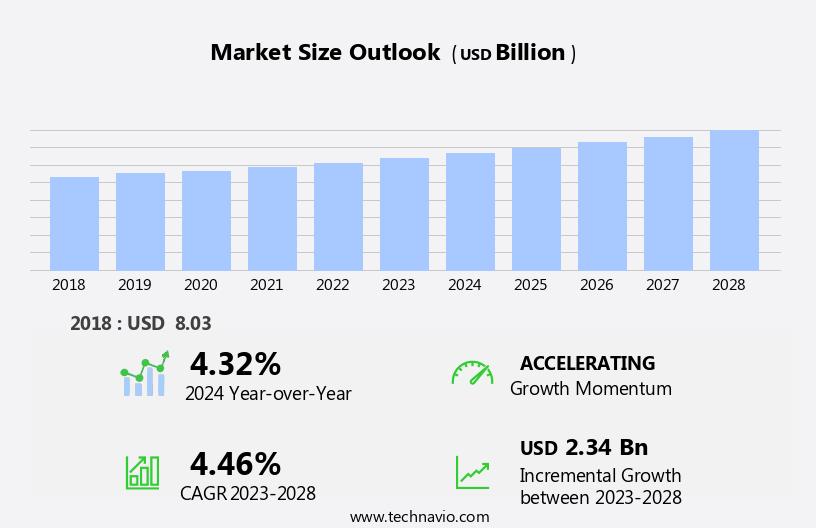

The north america seismic survey market size is forecast to increase by USD 2.34 billion at a CAGR of 4.46% between 2023 and 2028.

What will be the size of the North America Seismic Survey Market during the forecast period?

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Data acquisition

- Data processing

- Data interpretation

- End-user

- Oil

- gas

- Others

- Geography

- North America

- Canada

- Mexico

- US

- North America

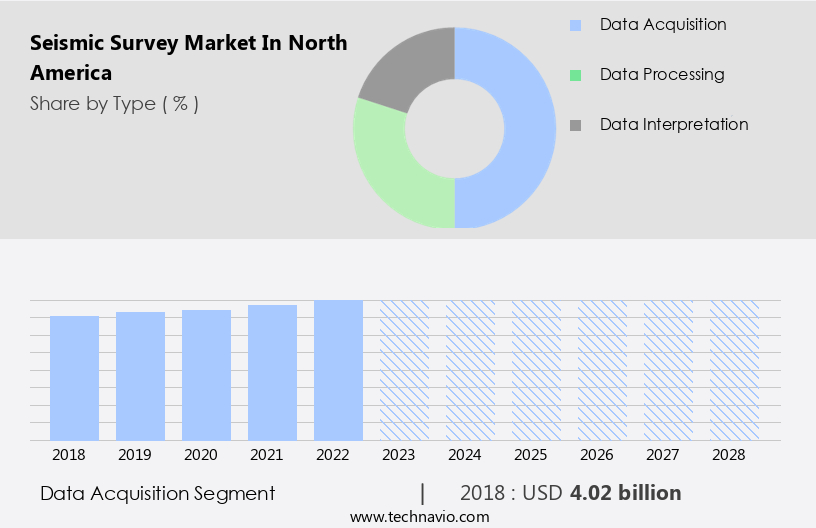

By Type Insights

- The data acquisition segment is estimated to witness significant growth during the forecast period.

The market is driven by the data acquisition segment, which focuses on gathering subsurface data for geological analysis and interpretation. Technological innovations, including high-resolution 3D and 4D seismic imaging, have revolutionized seismic survey technology. Advanced imaging algorithms, broadband seismic sensors, and high-performance computing facilitate more accurate and detailed subsurface data. This data is essential for the oil and gas industry, which uses it extensively for exploration and production activities. As energy demand continues to rise, the need for precise data to locate and assess potential hydrocarbon reservoirs drives market growth. Additionally, the expansion of renewable energy projects, such as offshore wind farms and geothermal energy, requires subsurface site characterization and geotechnical assessments, further fueling market demand.

Seismic survey services, including processing, interpretation, permitting requirements, and seismic protection devices, are integral components of the data acquisition process. Ensuring the protection of human life, property, and the environment during seismic events is a critical priority. Seismic survey equipment, including sensors, streamers, and data processing software, are continually evolving to meet the industry's demands for subsurface insights.

Get a glance at the market share of various segments Request Free Sample

The Data acquisition segment was valued at USD 4.02 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of North America Seismic Survey Market?

Rise in deepwater and ultra-deepwater E and P projects is the key driver of the market.

What are the market trends shaping the North America Seismic Survey Market?

Growing shift toward AI-powered analytics and machine learning for interpreting seismic data is the upcoming trend In the market.

What challenges does North America Seismic Survey Market face during the growth?

Environmental scrutiny and regulatory hurdles associated with seismic survey is a key challenge affecting the market growth.

Exclusive North America Seismic Survey Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agile Seismic LLC

- Amerapex Corp.

- CGG SA

- China National Petroleum Corp.

- Earth Signal Processing Ltd.

- Echo Seismic Ltd.

- Fairfield Geotechnologies

- Fugro NV

- Halliburton Co.

- PGS ASA

- PT Pertamina Persero

- Pulse Seismic Inc.

- SAExploration Holdings Inc.

- Schlumberger Ltd.

- Seitel Inc.

- Terrex Seismic

- TGS NOPEC Geophysical Co ASA

- Shearwater GeoServices

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is characterized by the ongoing quest for enhanced subsurface imaging and interpretation to optimize hydrocarbon recovery from both conventional and unconventional resources. This market is driven by the need for accurate and detailed subsurface insights to inform exploration, development, and production activities. Imaging resolution plays a crucial role In the effectiveness of seismic surveys. Advanced imaging algorithms and high-performance computing enable the processing of vast amounts of data, leading to improved subsurface characterization. Broadband seismic sensors, which capture a wider range of frequencies than traditional sensors, provide more detailed images of the subsurface. Seismic services companies offer a range of processing and interpretation services to help clients make informed decisions about their hydrocarbon reservoirs.

These services include data processing, optimization, and reservoir monitoring. Seismic protection devices are also essential to ensure the safety of human life, property, and the environment during seismic surveys. The use of seismic technology extends beyond the oil and gas industry. In the renewable energy sector, seismic surveys are employed for site characterization and geotechnical assessments for offshore wind farms and geothermal energy projects. Technological innovation continues to drive advancements in seismic imaging technology, with cutting-edge equipment and techniques being developed to improve efficiency and accuracy. Seismic surveys involve the deployment of sensors, such as streamers and sensors, to collect data.

Data processing software is then used to analyze the data and extract valuable subsurface insights. Seismic protection measures, including earthquake-resistant structures, are essential to ensure the safety and reliability of seismic survey equipment during seismic events. The market is subject to various market dynamics, including exploration budgets, project delays, permitting requirements, and indigenous land rights. Navigating these complexities requires a deep understanding of the regulatory landscape and stakeholder engagement. In conclusion, the market is a dynamic and evolving industry that plays a critical role In the exploration, development, and production of hydrocarbon resources. The use of advanced imaging algorithms, high-performance computing, and cutting-edge equipment enables more accurate subsurface characterization, leading to improved decision-making and optimized hydrocarbon recovery.

The market also extends to the renewable energy sector, where seismic surveys are employed for site characterization and geotechnical assessments. The ongoing quest for technological innovation and regulatory compliance will continue to shape the market In the coming years.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

137 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.46% |

|

Market growth 2024-2028 |

USD 2.34 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.32 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -