Oil Gas Pipeline Fabrication And Construction Market Size 2024-2028

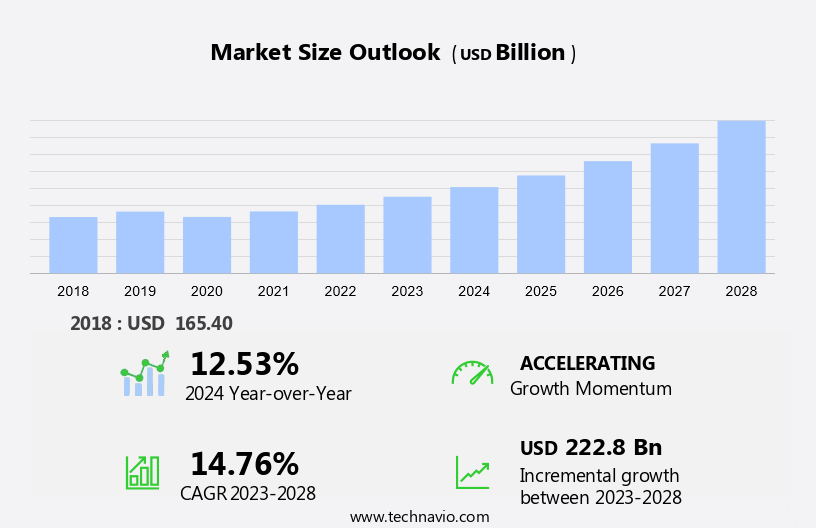

The oil gas pipeline fabrication and construction market size is estimated to grow by USD 222.8 billion at a CAGR of 14.76% between 2023 and 2028. The energy sector is experiencing a significant shift with growing natural gas consumption and a notable increase in oil production. This trend is driven by various factors, including the shift towards cleaner energy sources and advancements in extraction technologies. In response, pipeline expansion projects and new gas pipeline initiatives are underway to meet the increasing demand for natural gas. These projects aim to enhance energy security, reduce carbon emissions, and support economic growth. For instance, the Trans-Atlantic Pipeline is a proposed project that intends to transport natural gas from North America to Europe, while the Mountain Valley Pipeline in the United States is designed to transport natural gas from West Virginia to Virginia and North Carolina. These initiatives underscore the industry's commitment to meeting the growing energy needs while reducing the carbon footprint.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Request Free Sample

Market Dynamic and Customer Landscape

The market is a significant sector in the energy industry, focusing on the design, manufacturing, and installation of pipelines for transporting natural gas and crude oil. The market caters to various segments, including the National Gas Grid and city gas distribution networks. In regions like North America, the Tennessee Gas Pipeline and Plaquemines LNG Project are notable projects. In Latin America, Federal Electricidad's Tuxpan-Veracruz-Coatzacoalcos pipeline and Mexico's Dos Bocas and Tabasco pipelines are underway. The market's growth is driven by the increasing demand for natural gas as a cleaner energy source and the expansion of midstream infrastructure. Carbon steel is the primary material used in pipeline fabrication due to its strength and durability. In the US, the Federal Energy Regulatory Commission (FERC) regulates the construction and operation of interstate oil and gas pipelines. The market also includes projects in Iran, where the Chah Dangah-Veys Rupar pipeline is under development. Overall, the oil and gas pipeline fabrication and construction market is a vital contributor to the global energy sector.

Further, the market is a significant sector in the energy industry, focusing on the design, manufacturing, and installation of pipelines for transporting natural gas and crude oil. The market caters to various segments, including the National Gas Grid, gas distribution, and midstream infrastructure. In regions like North America, key projects include the Tennessee Gas Pipeline and Plaquemines LNG Project. In Latin America, Federal Electricidad's Tuxpan-Veracruz-Coatzacoalcos pipeline and Dos Bocas project in Tabasco are underway. Iran is another major player in the oil pipeline sector. Carbon steel is the primary material used in pipeline fabrication due to its strength and durability. In the US, the Federal Energy Regulatory Commission (FERC) regulates the construction and operation of interstate natural gas pipelines.

The market is driven by the increasing demand for natural gas as a cleaner alternative to traditional energy sources and the expansion of oil and gas pipeline networks. The oil sector also contributes significantly to the market, with projects like the Iran-Pakistan-India pipeline and the proposed City gas network in various countries.The global oil and gas pipeline fabrication and construction market is a significant sector in the energy industry, focusing on the design, manufacturing, and installation of pipelines for transporting natural gas and crude oil. The market caters to various segments, including the National Gas Grid and city gas distribution networks. In regions like North America, the Tennessee Gas Pipeline and Plaquemines LNG Project are notable projects. In Latin America, Federal Electricidad's Tuxpan-Veracruz-Coatzacoalcos pipeline and Mexico's Dos Bocas and Tabasco pipelines are underway. The market's growth is driven by the increasing demand for natural gas as a cleaner energy source and the expansion of midstream infrastructure. Carbon steel is the primary material used in pipeline fabrication due to its strength and durability. In the US, the Federal Energy Regulatory Commission (FERC) regulates the construction and operation of interstate oil and gas pipelines. The market also includes projects in Iran, where the Chah Dangah-Veys Rupar pipeline is under development. Overall, the oil and gas pipeline fabrication and construction market is a vital contributor to the global energy sector. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The growing natural gas consumption is notably driving market growth. The global oil and gas pipeline fabrication and construction market are witnessing significant growth due to the increasing demand for natural gas as a cleaner alternative fuel. According to International Energy Agency (IEA), natural gas consumption is projected to expand at the fastest rate among all fuel types by 2030, driven by factors such as environmental benefits and energy security needs, particularly in Asia-Pacific (APAC) region. The demand for natural gas is increasing due to its lower cost compared to other fossil fuels, making it an attractive choice for many countries. Pipeline projects are a crucial part of midstream infrastructure for transporting natural gas from production sites to city gas distribution networks and LNG terminals. In Mexico, for instance, pipeline projects such as the National Gas Grid's extension from Veracruz to Coatzacoalcos and the Dos Bocas pipeline in Tabasco are underway to expand the pipeline network. Similarly, in the US, pipeline projects like the Tennessee Gas Pipeline and the Plaquemines LNG Project are under construction. Carbon steel is the most commonly used material for pipeline fabrication due to its strength, durability, and cost-effectiveness. In Iran, for instance, the South Pars Gas Field's Phase 11 development project involves the construction of a 1,100-kilometer long pipeline using carbon steel. Regulatory bodies like the Federal Energy Regulatory Commission (FERC) in the US oversee the construction and operation of oil and gas pipelines to ensure safety and compliance with environmental regulations. Thus, such factors are driving the growth of the market during the forecast period.

Significant Market Trends

The safer and continuous transportation is the key trend in the market. The global market play a crucial role in the international energy sector by facilitating the transportation of large volumes of oil and natural gas. The pipeline network is a vital component of midstream infrastructure, connecting production sites to consumption centers, and reducing the need for less efficient methods such as rail, truck, or ship transport. In specific regions like Mexico, pipeline projects such as the National Gas Grid, Dos Bocas, and Tabasco, are underway to expand the existing network. These pipelines are primarily constructed using carbon steel to ensure durability and resistance to extreme weather conditions and temperature fluctuations. The United States, with its extensive pipeline transportation system, including the Tennessee Gas Pipeline and Plaquemines LNG Project, is a significant player in this market. Other countries like Iran and those in the Middle East also invest heavily in pipeline infrastructure for natural gas distribution, both domestically and internationally. Safety is a top priority in pipeline construction, as oil and natural gas are highly combustible and volatile. Underground pipelines minimize exposure to natural factors and potential sabotage. Above-ground pipelines are engineered to withstand extreme conditions, ensuring safe and reliable transportation of these energy resources. City gas distribution networks also rely on pipeline transportation to deliver natural gas to consumers for cooking, heating, and industrial applications. Overall, the pipeline fabrication and construction market continue to grow, driven by the increasing demand for oil and natural gas and the need for efficient, safe, and reliable transportation solutions. Thus, such trends will shape the growth of the market during the forecast period.

Major Market Challenge

The issues related to pipeline transportation is the major challenge that affects the growth of the market. The global market are experiencing significant growth due to the increasing demand for natural gas as a primary source of energy in the International Energy sector. The National Gas Grid in various countries, including Veracruz and Tabasco in Mexico, Coatzacoalcos and Dos Bocas in Mexico, and Tennessee in the United States, are investing heavily in pipeline projects to expand their gas distribution networks. These pipelines transport oil and gas products over long distances, often passing through challenging terrains and water bodies, making their construction and maintenance a complex process. Carbon steel is the primary material used in pipeline fabrication due to its strength and durability. In the United States, the Federal Energy Regulatory Commission (FERC) regulates the construction and operation of interstate natural gas pipelines. Similarly, the Plaquemines LNG Project in Louisiana and the Iranian gas pipeline network are undergoing expansion to meet the rising demand for natural gas. City gas distribution and midstream infrastructure facilities are also investing in pipeline transportation to ensure a stable and smooth supply of natural gas. Despite the advantages, pipelines face challenges such as vandalism and sabotage, which can lead to leakages of combustible gases and fuels. Larger leaks can be detected and located with precision using advanced technologies, but smaller leaks may go unnoticed, leading to potential hazards and environmental degradation. Regular surveillance and monitoring are essential to maintain the safe and efficient operation of oil and gas pipelines. Hence, the above factors will impede the growth of the market during the forecast period.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Barnard Construction Co. - The company offers the construction services and as well as oil and gas pipeline construction facility and services.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A.Hakpark B.V.

- AECOM

- Barnard Construction Co. Inc.

- Bechtel Corp.

- Bonatti Joint Stock Co.

- Fluor Corp.

- Gateway Companies LLC

- KAD Construction LLC

- Larsen and Toubro Ltd.

- Ledcor IP Holdings Ltd.

- MasTec Inc.

- McDermott International Ltd.

- Michels Corp

- Primoris Services Corp

- Shengli Oil and Gas Pipe Holdings Ltd.

- Snelson Companies Inc.

- Strike Inc.

- Sunland Construction Inc.

- Tenaris SA

- The AES Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

By Application

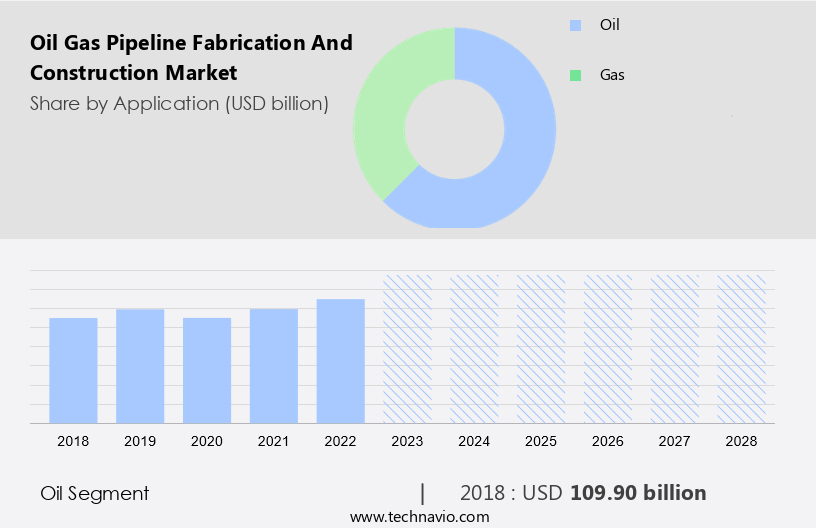

The oil segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth due to the expanding international energy sector and the development of new pipeline projects. The National Gas Grid in countries like Mexico, for instance, is undergoing expansion with initiatives such as the Dos Bocas and Tabasco projects in Veracruz and Coatzacoalcos. These projects aim to enhance natural gas distribution and midstream infrastructure, contributing to the pipeline network in the region.

Get a glance at the market share of various regions Download the PDF Sample

The oil segment accounted for USD 109.9 billion in 2018. The market encompasses various pipeline projects, including those for pipeline transportation of carbon steel pipelines. In the United States, Tennessee Gas Pipeline and Plaquemines LNG Project are notable examples. Internationally, the Iranian gas pipeline network is undergoing modernization to boost energy production and distribution. City gas distribution is another area of focus, with an increasing emphasis on the use of natural gas as a cleaner alternative to traditional fuels. Overall, the oil and gas pipeline fabrication and construction market is a critical facet of the energy industry, facilitating the transportation of oil and gas products to various end-users.

Regional Analysis

For more insights on the market share of various regions Download PDF Sample now!

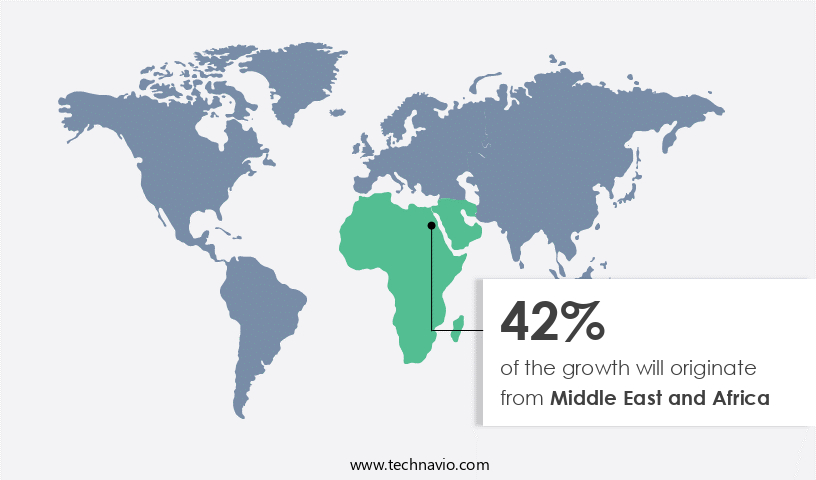

Middle East and Africa is estimated to contribute 42% to the growth of the global market during the market forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The global oil and gas pipeline fabrication and construction market is experiencing significant growth due to the expanding energy requirements of international markets. The National Gas Grid in countries like the UK and the pipeline network in Mexico, particularly in regions such as Veracruz, Coatzacoalcos, Dos Bocas, and Tabasco, are witnessing substantial pipeline projects. Natural gas is increasingly becoming a preferred choice for energy due to its cleaner burning properties, leading to an increase in demand for pipeline transportation. Carbon steel is the primary material used in pipeline fabrication due to its strength and durability. In the US, the Tennessee Gas Pipeline and the Plaquemines LNG Project are notable pipeline infrastructure facilities underway. Globally, pipeline projects in Iran and the City gas distribution networks in various countries are also contributing to the market growth. Midstream infrastructure development, including oil and gas pipelines, plays a crucial role in the energy sector by ensuring the efficient transportation of resources. The Federal Energy Regulatory Commission (FERC) in the US oversees the regulation of interstate pipeline transportation and sales of natural gas.

Segment Overview

The market report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion " for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application Outlook

- Oil

- Gas

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- South America

- Argentina

- Brazil

- Chile

- North America

You may also be interested in:

- Sheet Metal Market Analysis APAC, Europe, North America, Middle East and Africa, South America - China, US, Germany, Japan, UK - Size and Forecast

- HDPE Pipes Market Analysis APAC, North America, Europe, Middle East and Africa, South America - China, US, India, Germany, France - Size and Forecast

- Galvanized Steel Market by Product, Type and Geography - Forecast and Analysis

Market Analyst Overview

The market is a significant segment of the international energy industry, focusing on the design, manufacturing, and installation of pipelines for transportation of natural gas and oil. The market caters to various pipeline projects, including those for the National Gas Grid in countries like the UK, and international projects such as the Dos Bocas in Mexico, and the Plaquemines LNG Project in the US. Carbon steel is the primary material used in pipeline fabrication due to its strength and durability. In North America, Tennessee Gas Pipeline and Gas Pipeline are key players in this market. In Latin America, countries like Mexico have ongoing pipeline projects in Veracruz, Coatzacoalcos, and Tabasco, expanding their natural gas distribution network. Pipeline transportation plays a crucial role in midstream infrastructure, connecting oil and gas production sites to refineries and cities for distribution as city gas. Regulatory bodies like the Federal Energy Regulatory Commission (FERC) oversee pipeline construction and operations in the US. Iran is another significant player in the oil and gas pipeline market, with extensive pipeline networks for both oil and gas transportation. The oil and gas pipeline fabrication and construction market is a dynamic industry, with ongoing projects in various regions worldwide. The market's growth is driven by the increasing demand for natural gas and oil, and the need for reliable and efficient transportation infrastructure to meet this demand.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

135 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.76% |

|

Market growth 2024-2028 |

USD 222.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.53 |

|

Regional analysis |

Middle East and Africa, North America, Europe, APAC, and South America |

|

Performing market contribution |

Middle East and Africa at 42% |

|

Key countries |

US, Saudi Arabia, Russia, China, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

A.Hakpark B.V., AECOM, Barnard Construction Co. Inc., Bechtel Corp., Bonatti Joint Stock Co., Fluor Corp., Gateway Companies LLC, KAD Construction LLC, Larsen and Toubro Ltd., Ledcor IP Holdings Ltd., MasTec Inc., McDermott International Ltd., Michels Corp, Primoris Services Corp, Shengli Oil and Gas Pipe Holdings Ltd., Snelson Companies Inc., Strike Inc., Sunland Construction Inc., Tenaris SA, and The AES Corp. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Middle East and Africa, North America, Europe, APAC, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

RIA -

RIA -