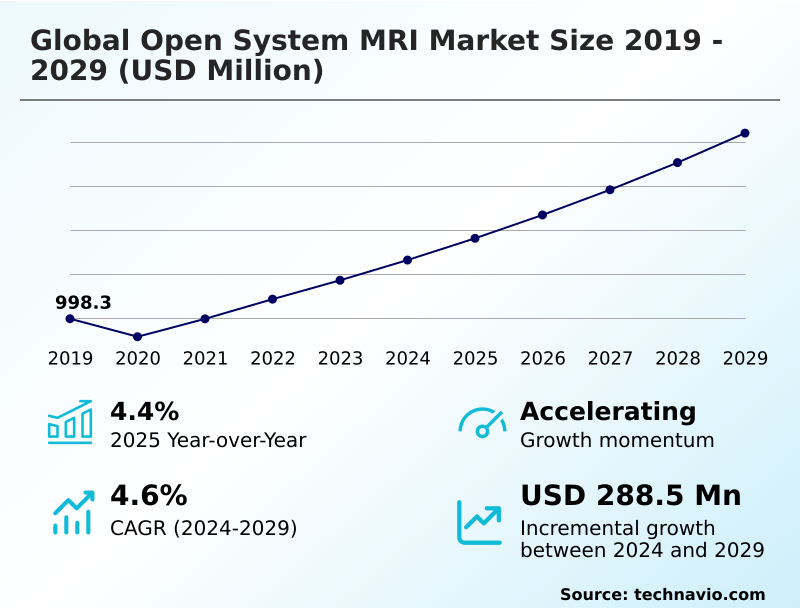

Open System MRI Market Size 2025-2029

The open system mri market size is valued to increase by USD 288.5 million, at a CAGR of 4.6% from 2024 to 2029. Increasing prevalence of diseases coupled with growing geriatric population will drive the open system mri market.

Major Market Trends & Insights

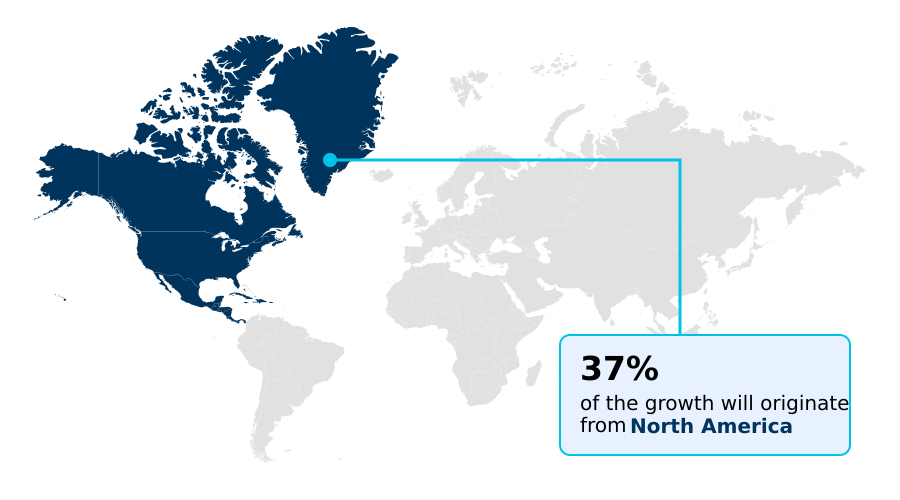

- North America dominated the market and accounted for a 36.8% growth during the forecast period.

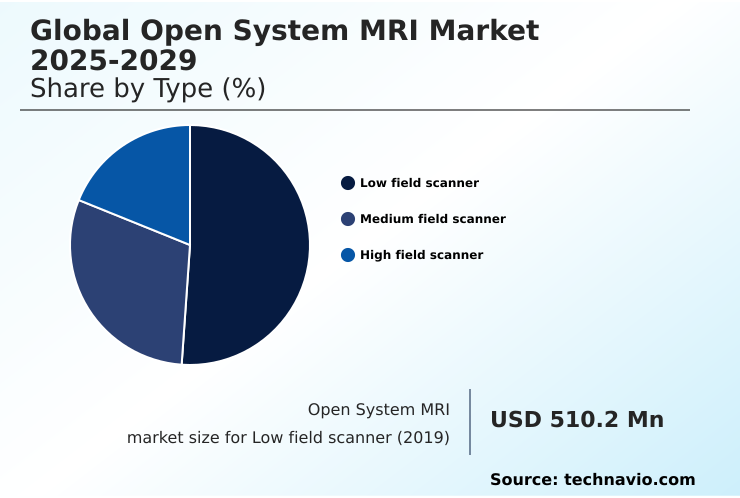

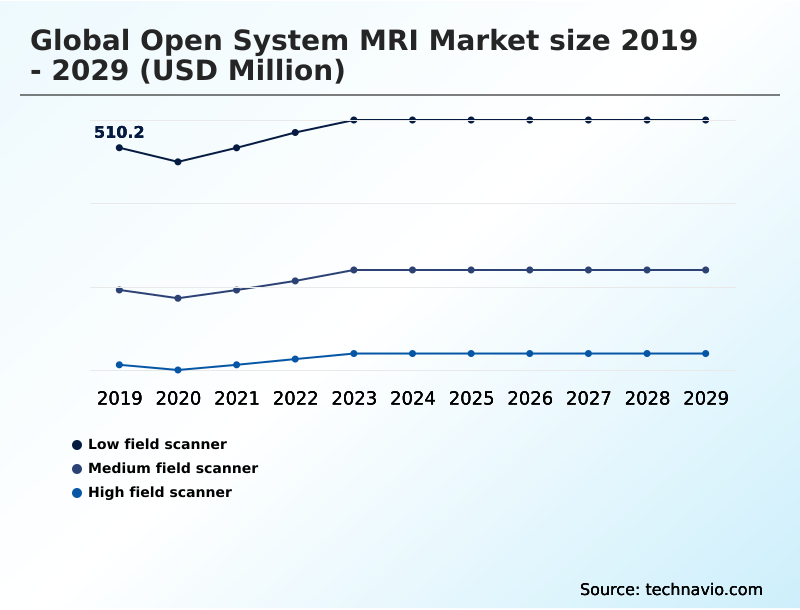

- By Type - Low field scanner segment was valued at USD 551.3 million in 2023

- By Technology - Superconducting magnet segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 421.9 million

- Market Future Opportunities: USD 288.5 million

- CAGR from 2024 to 2029 : 4.6%

Market Summary

- The open system MRI market is defined by its patient-centric approach to diagnostic imaging, fundamentally designed to alleviate the claustrophobia and anxiety often associated with traditional closed-bore scanners.

- This focus on patient comfort is a primary driver, particularly with the rising global prevalence of chronic conditions requiring imaging and an expanding geriatric and bariatric population that benefits from more accessible system designs.

- Technological innovation is a key theme, with advancements in software and AI-powered reconstruction engines enhancing image quality and reducing scan times, directly challenging the historical performance gap with closed systems. For instance, an outpatient imaging center can leverage these innovations to improve patient throughput and satisfaction, strengthening its competitive position.

- However, the market grapples with the inherent physics-based challenge of balancing field strength and homogeneity with an open architecture, which can impact the signal-to-noise ratio in some systems. The high capital cost of advanced scanners also remains a significant barrier to widespread adoption, leading to a dynamic interplay between clinical need, patient experience, and economic realities for healthcare providers.

What will be the Size of the Open System MRI Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Open System MRI Market Segmented?

The open system mri industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Low field scanner

- Medium field scanner

- High field scanner

- Technology

- Superconducting magnet

- Permanent magnet

- Hybrid systems

- End-user

- Neurology

- Oncology

- Cardiology

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The low field scanner segment is estimated to witness significant growth during the forecast period.

The low-field scanner segment is experiencing a resurgence, driven by technological advancements that enhance its clinical utility.

Initially perceived as having lower performance, modern low-field MRI scanner models now incorporate sophisticated hardware and software, making them viable for a range of applications previously reserved for high-field systems.

Innovations in advanced imaging sequences and image reconstruction engine technology are improving diagnostic confidence. These systems, often featuring a wide-bore MRI design, address critical needs in outpatient imaging centers by improving patient compliance rates and expanding healthcare accessibility.

Their adoption is also driven by the significant operational cost reduction they offer, with some systems demonstrating a 15% lower total cost of ownership, making advanced imaging more feasible for a wider range of healthcare providers.

The Low field scanner segment was valued at USD 551.3 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Open System MRI Market Demand is Rising in North America Get Free Sample

The geographic landscape of the open system MRI market is characterized by mature, high-adoption regions and rapidly emerging growth areas.

North America currently dominates, accounting for over 36% of the market opportunity, driven by advanced healthcare infrastructure and a strong emphasis on patient-centric design in a competitive provider environment.

Europe follows, with established markets focused on upgrading to systems with better magnetic field homogeneity and diagnostic confidence.

However, the highest growth is concentrated in Asia, where expanding healthcare access and rising investments are increasing the adoption of systems utilizing both superconducting magnet and cost-effective permanent magnet MRI technology.

This regional expansion is broadening the availability of specialized services like interventional MRI procedures and weight-bearing MRI scans.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Healthcare providers evaluating imaging technologies must weigh numerous factors, beginning with the clear benefits of open mri for claustrophobic patients. The decision extends to specific populations, with open system mri for bariatric patients becoming a critical service offering.

- A thorough cost-benefit analysis of low-field mri is often the next step, leading to a technical evaluation of superconducting vs permanent magnet open mri designs. The promise of ai-enabled open mri for faster scans is a compelling driver, directly impacting patient scheduling and throughput.

- Many are now exploring cryogen-free open mri system advantages to lower long-term operational costs, which is a key element in the future of helium-free mri technology. The clinical utility is further demonstrated by the upright mri scanner for spinal instability diagnosis and the growing use of interventional procedures using open architecture mri.

- For specialized demographics, pediatric imaging with reduced sedation mri represents a significant advancement in patient safety. Facilities also conduct high-field open mri image quality assessment to ensure diagnostic efficacy, constantly seeking ways of improving signal-to-noise ratio in open mri.

- This technology has found new niches, with growing open mri applications in sports medicine and demand for weight-bearing mri for orthopedic assessment. The operational model, particularly the open mri workflow in outpatient centers, is optimized when comparing open mri vendors and technology.

- This leads to a deeper look at integrating ai into existing mri systems and calculating the roi on advanced open mri scanners, especially as regulatory requirements for mri installation become more complex. Ultimately, the focus remains on managing patient anxiety during mri scans and minimizing motion artifacts in open mri to ensure high-quality outcomes.

- New applications such as open mri for cardiac stress testing are enabled by advanced software suites for open mri, which also help in optimizing patient scheduling for mri. Facilities that adopt these comprehensive strategies often see a greater return, with some reporting that AI-assisted workflows nearly double the diagnostic yield for complex cases compared to older, manual processes.

What are the key market drivers leading to the rise in the adoption of Open System MRI Industry?

- The increasing prevalence of chronic diseases, combined with a growing global geriatric population, serves as a key driver for market growth.

- The rising prevalence of chronic conditions and an aging population are significant market drivers.

- There is growing demand for systems that accommodate specific patient groups, such as those requiring bariatric patient imaging and pediatric neuroimaging, where comfort and accessibility are paramount.

- Open MRI is crucial for expanding cardiac MRI applications and oncology imaging solutions, as it allows for better patient monitoring and positioning. An upright MRI scanner, for instance, is invaluable for diagnosing spinal conditions under natural weight-bearing load.

- The need for advanced diagnostic techniques like diffusion tensor imaging and blood oxygenation level dependent imaging for neurological assessment further propels demand.

- These systems improve diagnostic access, with some facilities reporting a 20% increase in scan success rates for anxious or larger patients.

What are the market trends shaping the Open System MRI Industry?

- Significant software advancements are a key trend shaping the MRI technology landscape, enhancing imaging capabilities and driving market evolution.

- Software advancements are fundamentally reshaping the market, with AI-enabled reconstruction and motion correction algorithms at the forefront. These innovations directly address historical limitations by enhancing diagnostic procedure accuracy and enabling faster, more detailed scans. For example, simultaneous multi-slice imaging can accelerate 2D acquisition by a factor of three, significantly boosting patient throughput improvement.

- This focus on software enhances clinical workflow efficiency, with some platforms reducing scan setup time by over 25%. Furthermore, capabilities like real-time image processing support the move toward value-based healthcare by providing actionable data more quickly and supporting easier tele-radiology integration, which expands diagnostic reach.

What challenges does the Open System MRI Industry face during its growth?

- The high acquisition and maintenance costs associated with MRI systems present a significant challenge to market growth and wider adoption.

- The substantial capital equipment investment required for high-field open MRI systems remains a primary market challenge. High costs for acquisition, installation, and maintenance limit adoption, especially in smaller healthcare facilities. While innovations like the cryogen-free magnet aim to reduce long-term expenses, the initial outlay is significant.

- This has led to a robust market for refurbished MRI systems, which can offer savings of up to 50% compared to new equipment. Another challenge is managing patient motion artifacts, although designs focused on claustrophobia reduction help mitigate this.

- Vendors must balance advanced gradient coil design and radiofrequency coil technology with cost-effectiveness to broaden market penetration and align with evolving radiological society guidelines.

Exclusive Technavio Analysis on Customer Landscape

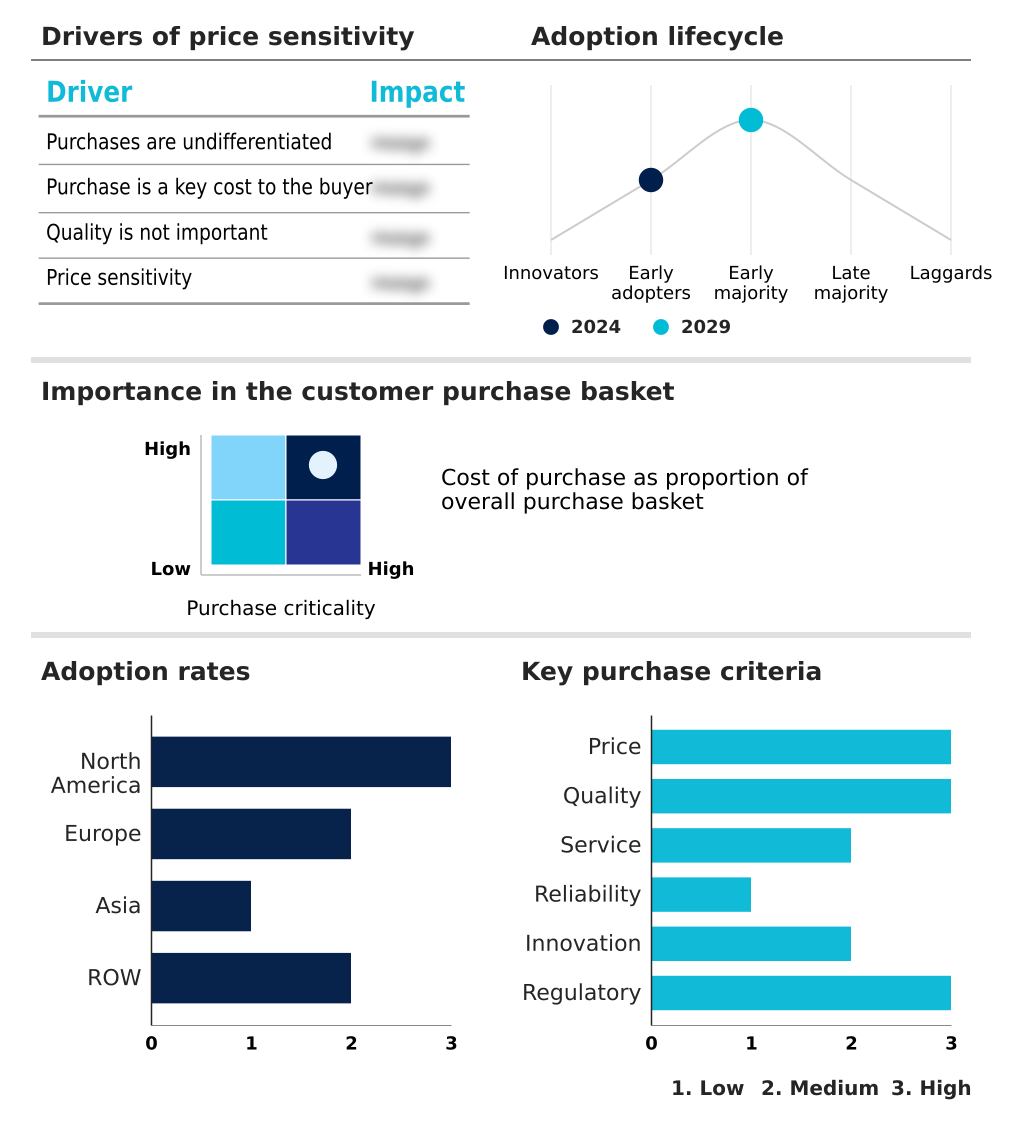

The open system mri market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the open system mri market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Open System MRI Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, open system mri market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alltech Inc. - Key offerings are centered on advanced open MRI systems that enhance diagnostic accuracy and patient comfort, expanding clinical applications in neurology and oncology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alltech Inc.

- ASG Superconductors Spa

- Aspect Imaging Ltd.

- AURORA HEALTHCARE US Corp.

- Beijing Wandong Medical Technology Co. Ltd.

- Canon Inc.

- Esaote Spa

- FONAR Corp.

- FUJIFILM Holdings Corp.

- General Electric Co.

- Hitachi Ltd.

- Koninklijke Philips NV

- Medonica Co. Ltd.

- Neusoft Corp.

- Siemens AG

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Open system mri market

- In November 2024, Siemens AG announced the launch of the MAGNETOM Aura, a next-generation 1.5T open MRI system featuring a cryogen-free superconducting magnet and an AI-powered reconstruction engine that reduces scan times by up to 40%.

- In January 2025, Koninklijke Philips NV entered into a strategic partnership with NVIDIA to integrate the NVIDIA Clara Holoscan platform into its next-generation open MRI systems, aiming to accelerate real-time image processing and enable AI-assisted diagnostics at the edge.

- In March 2025, FONAR Corp. received FDA 510(k) clearance for its new motion-compensated imaging software suite for its Upright Multi-Position MRI, allowing for high-resolution scans of patients in weight-bearing positions to better diagnose spinal instabilities.

- In May 2025, Hitachi Ltd. announced the opening of a new manufacturing and R&D facility in Singapore, dedicated to producing its latest line of mid-field open MRI systems tailored for the specific clinical and economic needs of the Southeast Asian market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Open System MRI Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2025-2029 | USD 288.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The open system MRI market is advancing beyond its traditional role of accommodating claustrophobic patients. The integration of advanced imaging sequences and sophisticated image reconstruction engine technology in both low-field MRI scanner and high-field open MRI systems is enhancing diagnostic capabilities.

- At a technical level, innovations in gradient coil design, radiofrequency coil technology, and cryogen-free magnet engineering are central to this evolution. A high-field open MRI utilizing a superconducting magnet now rivals closed-bore systems in certain applications, while permanent magnet MRI and hybrid MRI systems offer cost-effective alternatives.

- For boardroom consideration, the adoption of AI-enabled reconstruction is a strategic imperative, directly impacting operational budgets. The use of simultaneous multi-slice imaging and motion correction algorithms has demonstrated a 25% reduction in non-diagnostic scans, reducing repeat appointments and increasing asset utilization.

- Advanced applications like diffusion tensor imaging, blood oxygenation level dependent imaging, and dynamic contrast-enhanced MRI are becoming standard, while the upright MRI scanner with its vertical field magnet opens new diagnostic pathways. This push towards higher performance, evident in improved signal-to-noise ratio and magnetic field homogeneity, is making wide-bore MRI a cornerstone of modern radiology.

What are the Key Data Covered in this Open System MRI Market Research and Growth Report?

-

What is the expected growth of the Open System MRI Market between 2025 and 2029?

-

USD 288.5 million, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Low field scanner, Medium field scanner, and High field scanner), Technology (Superconducting magnet, Permanent magnet, and Hybrid systems), End-user (Neurology, Oncology, Cardiology, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of diseases coupled with growing geriatric population, High cost of MRI

-

-

Who are the major players in the Open System MRI Market?

-

Alltech Inc., ASG Superconductors Spa, Aspect Imaging Ltd., AURORA HEALTHCARE US Corp., Beijing Wandong Medical Technology Co. Ltd., Canon Inc., Esaote Spa, FONAR Corp., FUJIFILM Holdings Corp., General Electric Co., Hitachi Ltd., Koninklijke Philips NV, Medonica Co. Ltd., Neusoft Corp., Siemens AG and Toshiba Corp.

-

Market Research Insights

- The market's momentum is increasingly tied to demonstrating value beyond patient comfort. A strong focus on patient-centric design has led to measurable improvements in care, with some facilities reporting a 25% reduction in aborted scans due to claustrophobia reduction.

- Innovations are also targeting clinical workflow efficiency, as AI-driven protocols have been shown to accelerate patient throughput improvement by over 30% for routine examinations. This aligns with the principles of value-based healthcare by linking technological investment to operational cost reduction.

- Furthermore, systems tailored for bariatric patient imaging are expanding service access, contributing to greater diagnostic confidence across a wider patient demographic and reinforcing the strategic importance of open architecture in modern radiology.

We can help! Our analysts can customize this open system mri market research report to meet your requirements.

RIA -

RIA -