Organic Pesticides Market Size 2025-2029

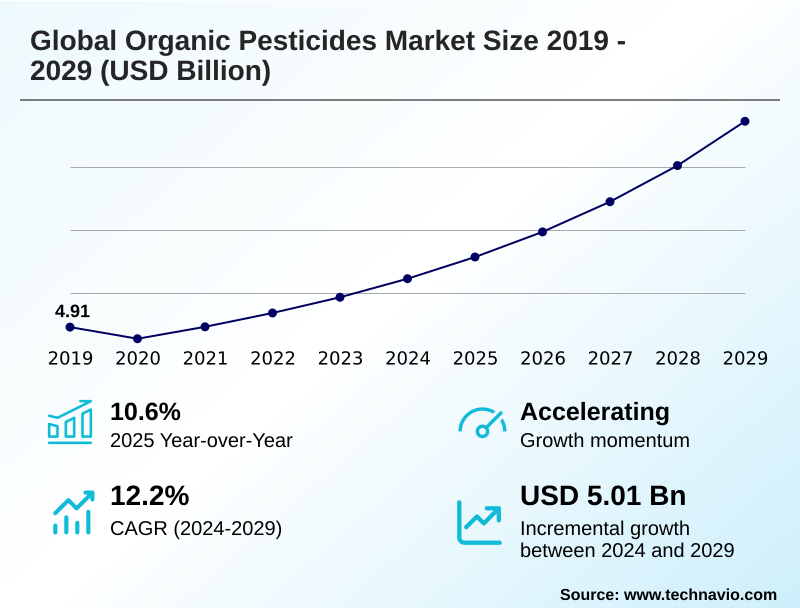

The organic pesticides market size is valued to increase by USD 5.01 billion, at a CAGR of 12.2% from 2024 to 2029. Growing interest in organic products will drive the organic pesticides market.

Major Market Trends & Insights

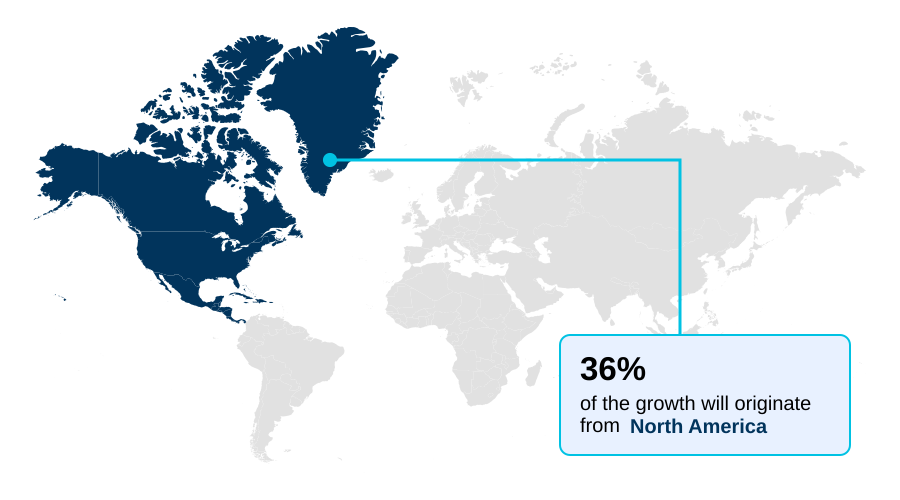

- North America dominated the market and accounted for a 35.7% growth during the forecast period.

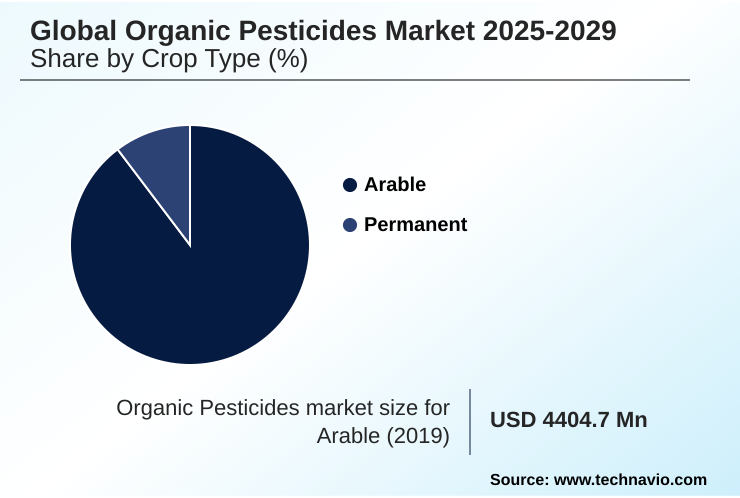

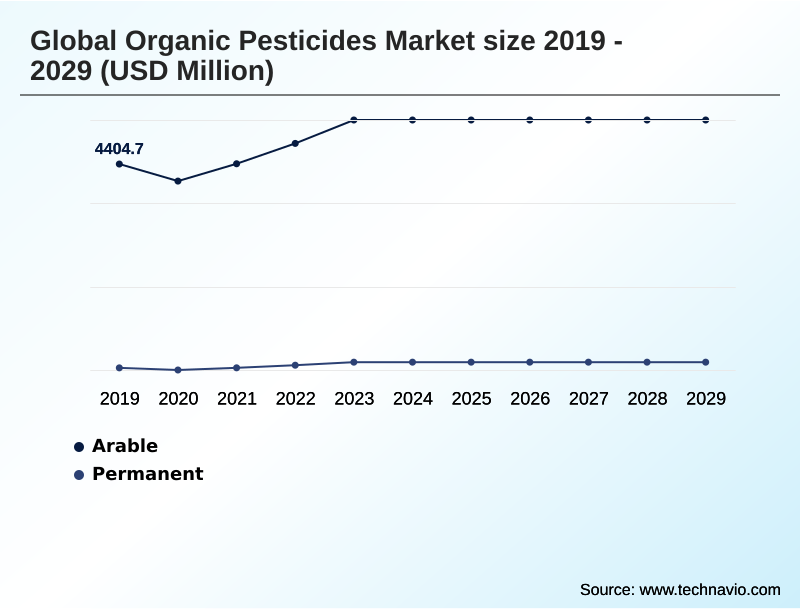

- By Crop Type - Arable segment was valued at USD 5.25 billion in 2023

- By Source - Microbial pesticides segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 6.55 billion

- Market Future Opportunities: USD 5.01 billion

- CAGR from 2024 to 2029 : 12.2%

Market Summary

- The organic pesticides market is undergoing a significant transformation, driven by escalating consumer demand for residue-free food and increasingly stringent environmental regulations. This shift is compelling the agricultural industry to move beyond conventional chemical inputs toward more sustainable alternatives.

- Key drivers include the expansion of organic farming and the growing adoption of integrated pest management (IPM) programs, where biologicals play a crucial role. A central trend is the rapid innovation in biopesticide formulations, including microbial, botanical, and biochemical agents that offer enhanced efficacy and specificity.

- For instance, a farming cooperative seeking to export produce to markets with strict residue limits can leverage advanced biorational solutions to manage pests effectively while maintaining its organic certification. This approach not only ensures compliance but also improves market access.

- However, the industry faces challenges related to the shorter shelf-life of some biological products, their slower mode of action compared to synthetics, and higher initial costs. Overcoming these hurdles through continued research and development is essential for broadening the adoption of organic pesticides and securing a more sustainable future for agriculture.

- The market's trajectory is defined by this balance between strong demand-side pull and supply-side innovation aimed at addressing practical limitations.

What will be the Size of the Organic Pesticides Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Organic Pesticides Market Segmented?

The organic pesticides industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Crop type

- Arable

- Permanent

- Source

- Microbial pesticides

- Botanical pesticides

- Mineral pesticides

- Application

- Foliar spray

- Soil treatment

- Seed treatment

- Post-harvest

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Crop Type Insights

The arable segment is estimated to witness significant growth during the forecast period.

The arable crop segment is foundational to the organic pesticides market, driven by large-scale farming of cereals, oilseeds, and vegetables. Demand is fueled by stringent regulations on synthetic chemical residues and a growing focus on sustainable soil management.

To meet the needs of extensive acreages, research is centered on developing broad-spectrum bioinsecticides and biofungicides that offer competitive efficacy. Innovations in agricultural biologicals and microbial-based insecticide formulations are critical for this segment.

Integrating these solutions into existing farm programs is key, with microbial biopesticides now accounting for over 65% of the biopesticides sector, showcasing their importance in residue-free crop protection and enhancing plant health.

This shift toward advanced biorational solutions and biological pest control agents supports large-scale sustainable farming practices.

The Arable segment was valued at USD 5.25 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Organic Pesticides Market Demand is Rising in North America Get Free Sample

The geographic landscape of the organic pesticides market is shaped by regional regulatory environments and consumer demand for organic food production.

North America is a major contributor to market growth, accounting for over 35% of the global incremental expansion, driven by strong consumer awareness and supportive government policies promoting sustainable pest solutions.

Meanwhile, APAC is projected to experience the fastest regional growth, with a CAGR of 13.6%, fueled by increasing adoption of modern agricultural techniques and a rising preference for eco-friendly farming.

Europe remains a mature market with stringent organic farming standards, fostering innovation in crop-specific formulations and pest resistance management.

The market dynamics in these regions underscore a global shift towards agricultural innovation and sustainable crop production methodologies to meet evolving consumer and regulatory expectations.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global organic pesticides market 2025-2029 is deeply rooted in scientific advancement and shifting agricultural paradigms. Central to this is the development of new biological insecticides and continuous innovations in organic pest management, which are redefining crop protection strategies.

- Advancements in biopesticide formulation technology are addressing historical limitations, such as the shelf life of microbial biopesticides, thereby improving their commercial viability. A thorough cost-benefit analysis of organic pesticides is becoming crucial for growers, who must weigh initial investment against long-term soil health and market access benefits.

- The regulatory landscape for biological pesticides continues to evolve, influencing market entry and product claims. One of the primary challenges in organic pesticide adoption remains perceived efficacy gaps, especially when compared to synthetic alternatives.

- However, the role of biopesticides in integrated pest management is expanding, particularly for organic pest control for fruit crops and in organic pesticide application in greenhouse farming. The broader impact of organic pesticides on biodiversity is a key consideration, aligning with the environmental benefits of using organic pesticides.

- Ultimately, the consumer demand for organic produce impact is the primary force driving the adoption of biodegradable pest control methods and natural alternatives to synthetic chemical pesticides, solidifying the market growth of organic pest solutions and pushing integrated pest management for sustainable agriculture to the forefront of the industry.

What are the key market drivers leading to the rise in the adoption of Organic Pesticides Industry?

- The growing consumer interest in organic products is a key driver for the organic pesticides market.

- The primary driver for the organic pesticides market is the growing global demand for organic agricultural products and certified organic crops.

- This is fueled by consumer awareness of the health benefits, as organic foods can contain up to 68% more antioxidants and have pesticide residue levels that are 48% lower than conventional products.

- This demand incentivizes farmers to adopt organic input materials and natural pesticide ingredients. Consequently, there's a greater emphasis on soil health improvement and the use of beneficial microorganisms.

- The adoption of mineral pesticides, foliar spray application techniques, and other organic methods reflects a broader industry commitment to meeting consumer expectations for healthier and more environmentally friendly food options.

What are the market trends shaping the Organic Pesticides Industry?

- Biodegradation and bioremediation of organic pesticides are emerging as significant market trends. These processes support sustainable agriculture by breaking down residues and detoxifying contaminated environments.

- Key trends in the organic pesticides market are centered on technological advancements that improve efficacy and sustainability. Innovations in biodegradation processes and bioremediation techniques are enabling the development of products with minimal environmental impact. The focus is on creating sophisticated organic pesticides like spinosad-based insecticides and pyrethrin-based insecticides that offer targeted action.

- For example, new bacillus amyloliquefaciens strain formulations have shown up to a 40% increase in disease control efficacy in field trials. This drive for better performance is leading to the adoption of advanced seed treatment solutions and post-harvest application methods, which can reduce application frequency by 25%.

- These trends underscore a market shift toward highly effective, scientifically-backed sustainable crop protection and pest management strategies.

What challenges does the Organic Pesticides Industry face during its growth?

- The potential harm of some organic pesticides to non-target animals presents a key challenge to market growth.

- A significant challenge in the organic pesticides market is overcoming performance and logistical limitations compared to synthetic alternatives. The limited shelf life of organic pesticides, particularly microbial pesticides, can lead to efficacy reductions of over 30% if not stored correctly.

- Furthermore, the production costs for botanical pesticides and other natural plant protection (npp) solutions can be up to 50% higher, impacting their adoption by cost-sensitive growers. Formulations like those based on beauveria bassiana require precise application conditions, and improper soil treatment methods can reduce their effectiveness.

- Addressing these issues through innovation in formulation and manufacturing is crucial for making organic pest control more competitive and accessible.

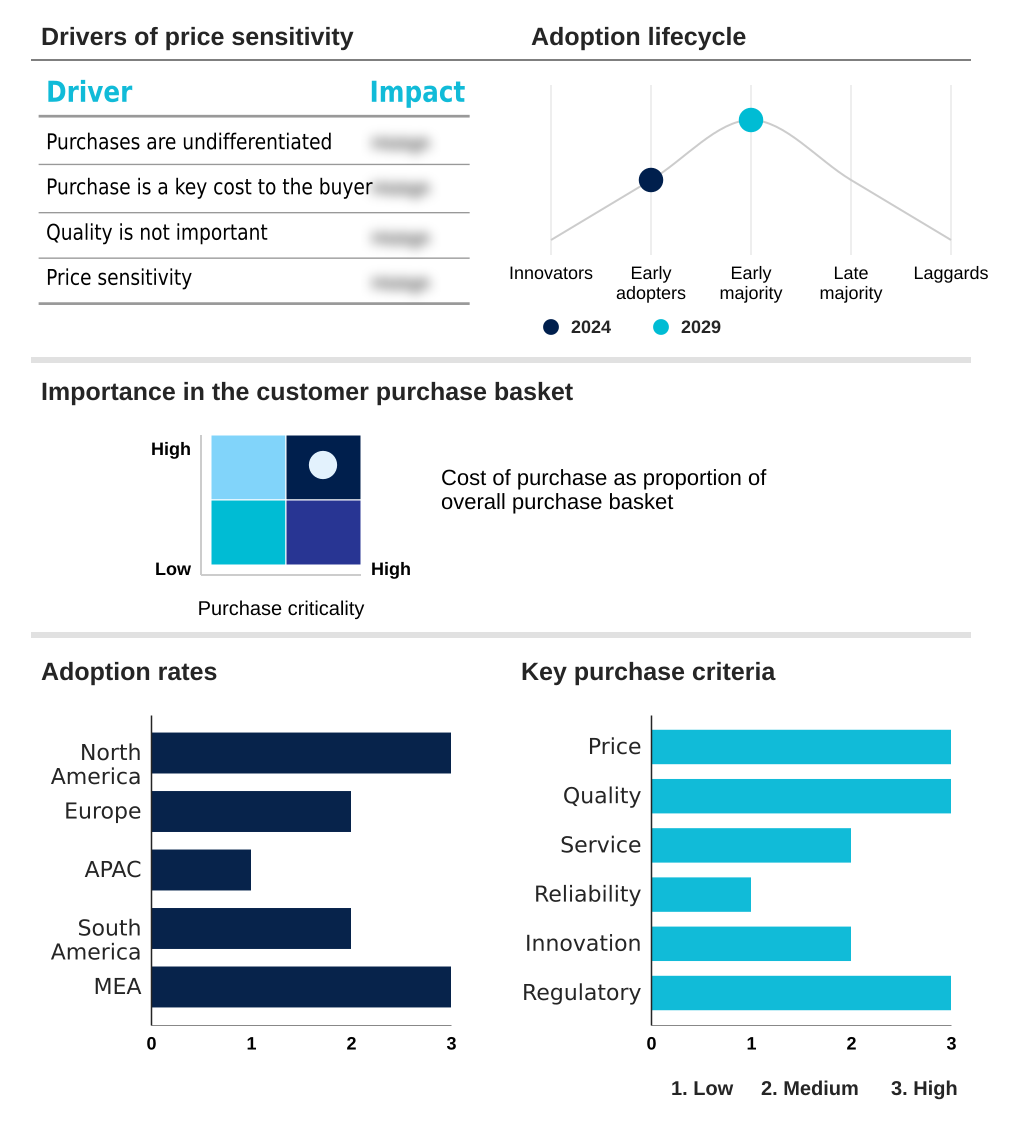

Exclusive Technavio Analysis on Customer Landscape

The organic pesticides market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the organic pesticides market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Organic Pesticides Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, organic pesticides market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Andermatt Group AG - Offerings include microbial and botanical-based organic pesticides, such as biofungicides and bioinsecticides, developed for sustainable crop protection and integrated pest management programs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Andermatt Group AG

- BASF SE

- Bayer AG

- Certis USA LLC

- Corteva Inc.

- Futureco Bioscience SA

- Gitaji Pesticides Industries

- Greenstar Fertilizers Ltd.

- Jaipur Bio Fertilizers

- Nufarm Ltd.

- Redox Industries Ltd.

- Sahkar Pharmaceuticals Pvt. Ltd.

- Sarasota Green Group LLC

- Satpura Bio Fertiliser India Pvt Ltd.

- Sikko Industries Ltd.

- Sumitomo Chemical Co. Ltd.

- UPL Ltd.

- Valent BioSciences LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic pesticides market

- In September 2024, Andermatt Group AG announced the acquisition of a leading Brazilian biopesticide firm, strengthening its footprint in the South American market and adding new microbial fermentation technology to its portfolio.

- In November 2024, BASF SE revealed plans to construct a new state-of-the-art fermentation plant in North America dedicated to biological and biotechnology-based crop protection products, aiming to double its production capacity by 2027.

- In February 2025, the US Environmental Protection Agency (EPA) granted regulatory approval for a novel double-stranded RNA (dsRNA) based insecticide, marking a significant milestone for next-generation biological pest control in row crops.

- In May 2025, Futureco Bioscience SA and Sumitomo Corporation announced a strategic partnership to co-develop and globally distribute a new biological fungicide technology targeting resilient crop diseases in viticulture and horticulture.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Pesticides Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 281 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.2% |

| Market growth 2025-2029 | USD 5007.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 10.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The organic pesticides market is defined by a strategic shift towards advanced agricultural biologicals and residue-free crop protection. The development of biorational solutions, including biofungicides, bioinsecticides, and biostimulants, is accelerating, driven by the need for sustainable agriculture inputs that comply with omri certified inputs standards.

- Innovations in microbial-based insecticide and plant-derived nematicide technologies, such as those using bacillus thuringiensis and double-stranded rna pesticide platforms, are becoming central to product portfolios.

- A key boardroom consideration is the allocation of R&D capital toward proprietary technologies like the burkholderia platform and bacillus subtilis formulation, as firms possessing advanced microbial fermentation technology have demonstrated a 25% improvement in product stability.

- This focus on sustainable soil management and plant health enhancement through solutions like neem-based pesticides is critical for maintaining a competitive edge in a market focused on integrated pest management (ipm) and biological pest control agents.

What are the Key Data Covered in this Organic Pesticides Market Research and Growth Report?

-

What is the expected growth of the Organic Pesticides Market between 2025 and 2029?

-

USD 5.01 billion, at a CAGR of 12.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Crop Type (Arable, and Permanent), Source (Microbial pesticides, Botanical pesticides, and Mineral pesticides), Application (Foliar spray, Soil treatment, Seed treatment, and Post-harvest) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing interest in organic products, Organic pesticides harmful to other animals

-

-

Who are the major players in the Organic Pesticides Market?

-

Andermatt Group AG, BASF SE, Bayer AG, Certis USA LLC, Corteva Inc., Futureco Bioscience SA, Gitaji Pesticides Industries, Greenstar Fertilizers Ltd., Jaipur Bio Fertilizers, Nufarm Ltd., Redox Industries Ltd., Sahkar Pharmaceuticals Pvt. Ltd., Sarasota Green Group LLC, Satpura Bio Fertiliser India Pvt Ltd., Sikko Industries Ltd., Sumitomo Chemical Co. Ltd., UPL Ltd. and Valent BioSciences LLC

-

Market Research Insights

- The organic pesticides market is expanding due to a strong push for sustainable farming practices and the rising popularity of eco-friendly pest management. Consumer demand for agricultural sustainability is a major factor, as organic crops are perceived as healthier, containing up to 68% more antioxidants than conventionally grown produce.

- Furthermore, the use of certified organic inputs ensures that harmful contaminants are approximately 48% lower. This emphasis on crop quality improvement and eco-conscious agriculture is driving innovation in natural pest management and agricultural microbiology.

- As a result, the market is seeing increased adoption of biological control systems that align with organic farming standards, promoting both environmental stewardship and enhanced crop yields.

We can help! Our analysts can customize this organic pesticides market research report to meet your requirements.

RIA -

RIA -