Agricultural Pesticides Market Size 2026-2030

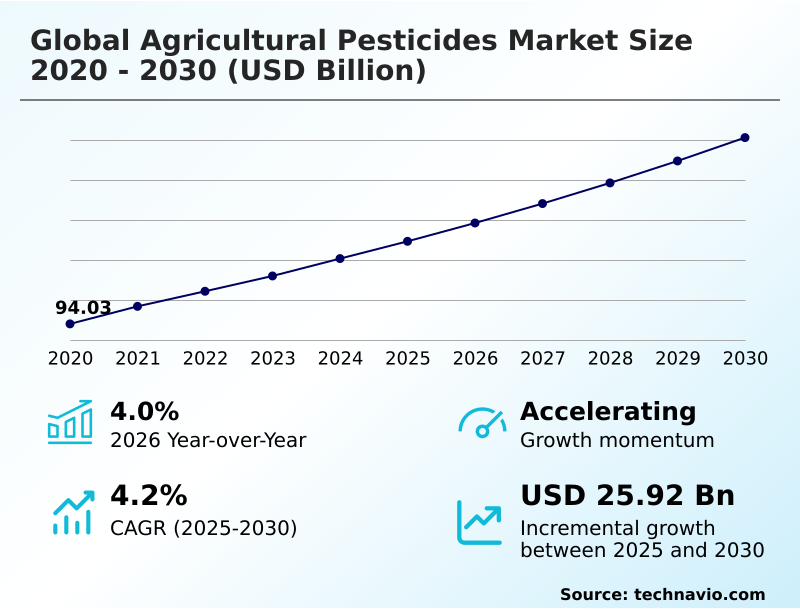

The agricultural pesticides market size is valued to increase by USD 25.92 billion, at a CAGR of 4.2% from 2025 to 2030. Shift toward sustainable, eco‑friendly formulations will drive the agricultural pesticides market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.9% growth during the forecast period.

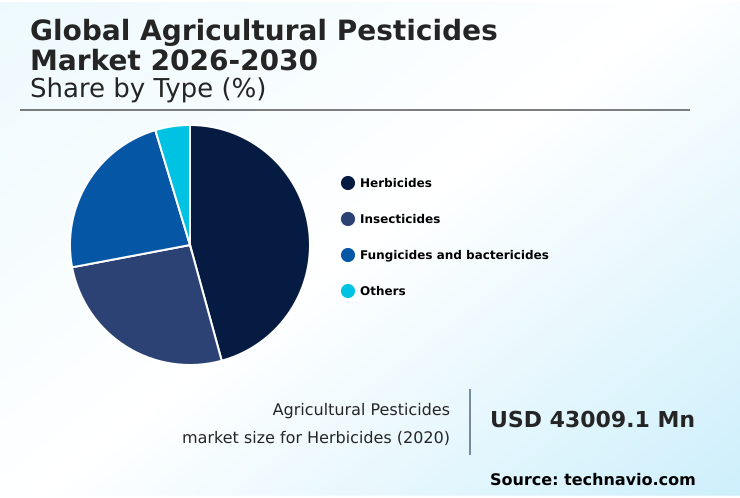

- By Type - Herbicides segment was valued at USD 51.16 billion in 2024

- By Product - Synthetic pesticides segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 46.57 billion

- Market Future Opportunities: USD 25.92 billion

- CAGR from 2025 to 2030 : 4.2%

Market Summary

- The agricultural pesticides market is fundamentally shaped by the critical need to safeguard crop yields against a backdrop of rising global food demand and intensifying climate variability. This sector is undergoing a significant transformation, moving from a reliance on conventional, broad-spectrum chemicals to more sophisticated and sustainable crop protection strategies.

- Key trends include the rapid adoption of biopesticides, derived from natural sources, and the integration of digital agriculture tools that enable precision application, minimizing environmental impact. A central business scenario involves the strategic recalibration of supply chains for active ingredients to navigate geopolitical disruptions and ensure consistent manufacturing of both synthetic and biological formulations.

- However, the industry grapples with persistent challenges, including the development of pest resistance to existing treatments and the high cost of regulatory compliance for new products. This dynamic environment compels continuous innovation in formulations and application technologies to balance agricultural productivity with ecological stewardship, ensuring the long-term viability of food production systems worldwide.

What will be the Size of the Agricultural Pesticides Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Agricultural Pesticides Market Segmented?

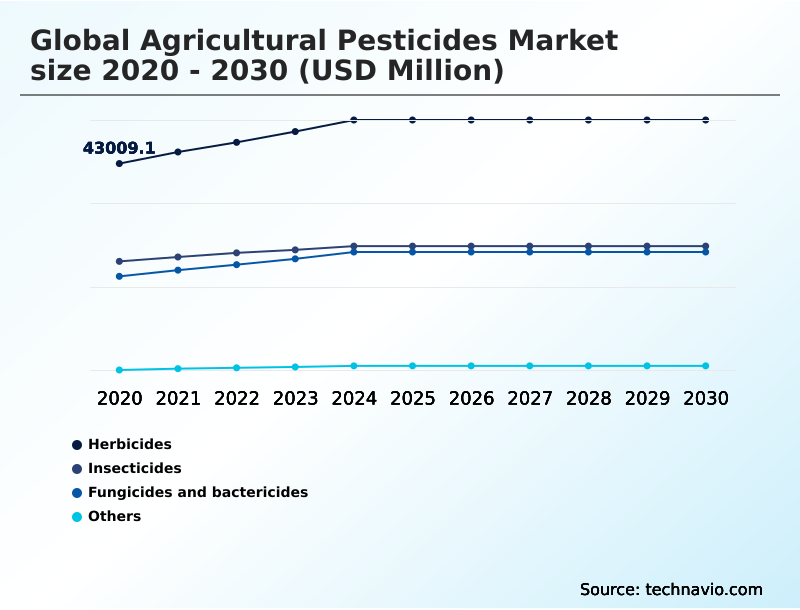

The agricultural pesticides industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Herbicides

- Insecticides

- Fungicides and bactericides

- Others

- Product

- Synthetic pesticides

- Biopesticides

- Formulation

- Liquid

- Emulsifiable concentrate

- Granular

- Wettable powder

- Geography

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- South Africa

- Saudi Arabia

- Turkey

- Rest of World (ROW)

- APAC

By Type Insights

The herbicides segment is estimated to witness significant growth during the forecast period.

The herbicides segment is central to the global agricultural pesticides market 2026-2030, driven by the need for effective weed management solutions. This category, accounting for nearly 40% of the total market, is evolving beyond traditional synthetic pesticides.

The focus is shifting toward developing novel chemical active ingredients and bio-herbicides to combat resistance and meet demand from organic farming methods. This evolution in crop protection products is critical for sustainable farming practices.

Integrated pest management protocols now favor targeted, variable-rate methods over broadcast spraying, leveraging precision agriculture technology.

Manufacturers are prioritizing pre-emergence and specialty formulations, including those for regenerative farming, to offer long-term residual control, thus protecting seedlings and supporting soil health improvement while ensuring consistent agricultural input performance.

The Herbicides segment was valued at USD 51.16 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

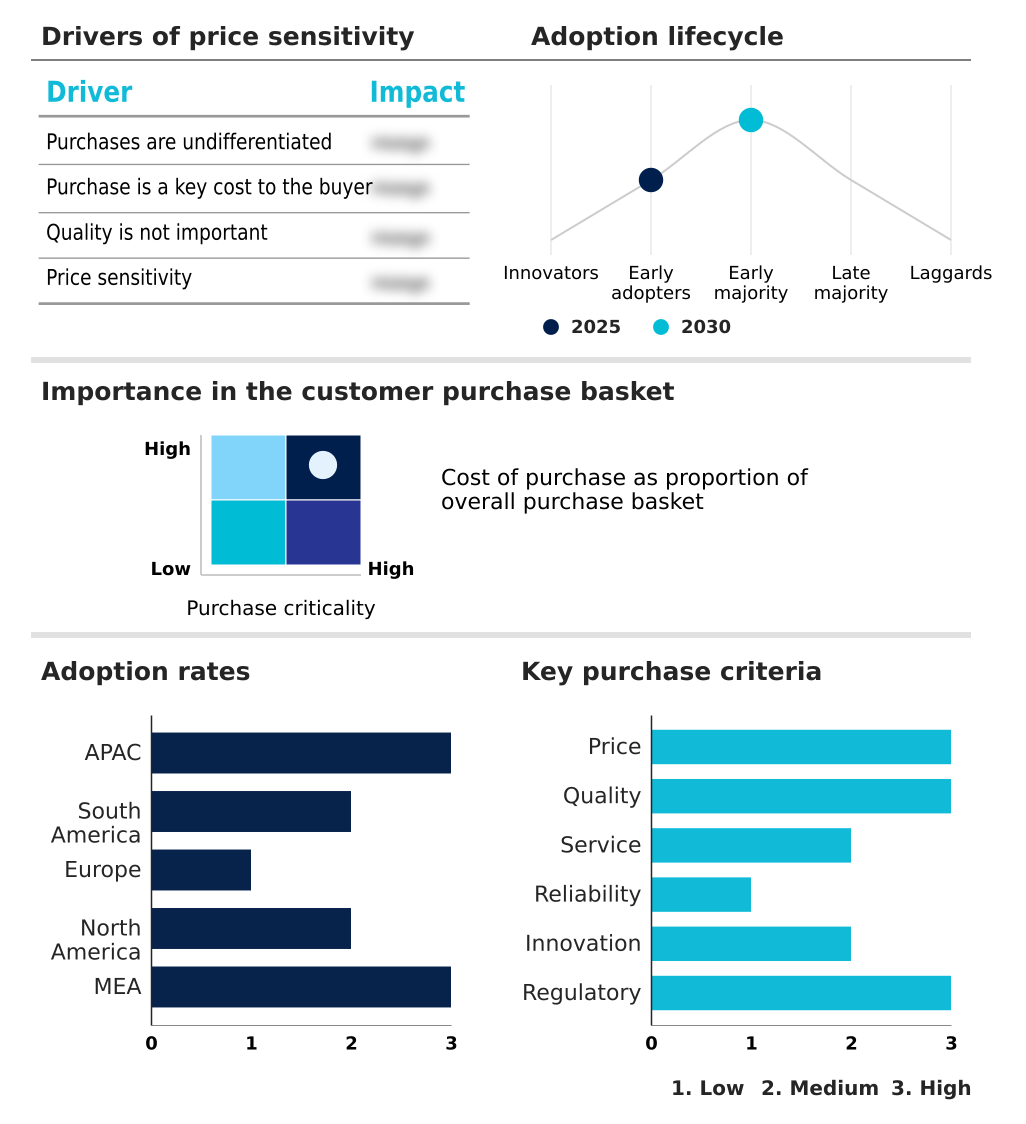

APAC is estimated to contribute 38.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Agricultural Pesticides Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the agricultural pesticides market is led by APAC, which accounts for nearly 39% of incremental growth, driven by agricultural intensification and food security initiatives in countries like China and India.

In this region, regulatory shifts, such as China's digital certificate policy for agricultural chemical registration, enhance supply chain traceability for nematicides and other crop protection chemicals.

This contrasts with mature markets like Europe, where stringent environmental regulations and a focus on low-toxicity formulations are paramount. South America remains a critical hub for commodity crops, where effective pest control performance is essential.

The demand for targeted pesticide application and advanced seed treatments is a common thread, pushing regional players toward more sophisticated and sustainable crop protection strategies to maintain global competitiveness and meet commercial-scale agriculture demands.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global agricultural pesticides market 2026-2030 requires a nuanced understanding of product efficacy and operational resilience. The debate over synthetic versus biological insecticide efficacy continues, with choices depending on crop type, pest pressure, and regulatory context. The impact of biopesticides on the soil microbiome is a growing consideration, influencing integrated pest management in organic farming.

- For high-value crops, the specific use of fungicides is critical for quality and yield, while the cost of pesticide regulatory compliance shapes R&D pipelines for all new chemistries. Formulators are focused on developing broad-spectrum herbicide formulations and selective insecticide chemistry to tackle resistant weeds and pests. Precision spraying technology for herbicides is enhancing the effectiveness of these products.

- Operationally, managing pesticide supply chain risk has become a boardroom priority. Firms that diversified sourcing for key intermediates saw a 40% lower risk of production delays compared to those with concentrated sourcing.

- The impact of climate on pest cycles necessitates adaptable solutions, where the effectiveness of nano-insecticide delivery systems and the impact of adjuvants on pesticide efficacy are key research areas.

- Decisions around post-patent glyphosate alternative options, systemic fungicide application for cereals, nematicide effectiveness in sandy soils, plant growth regulator application timing, and seed treatment for early pest control are all shaped by these intersecting market forces.

What are the key market drivers leading to the rise in the adoption of Agricultural Pesticides Industry?

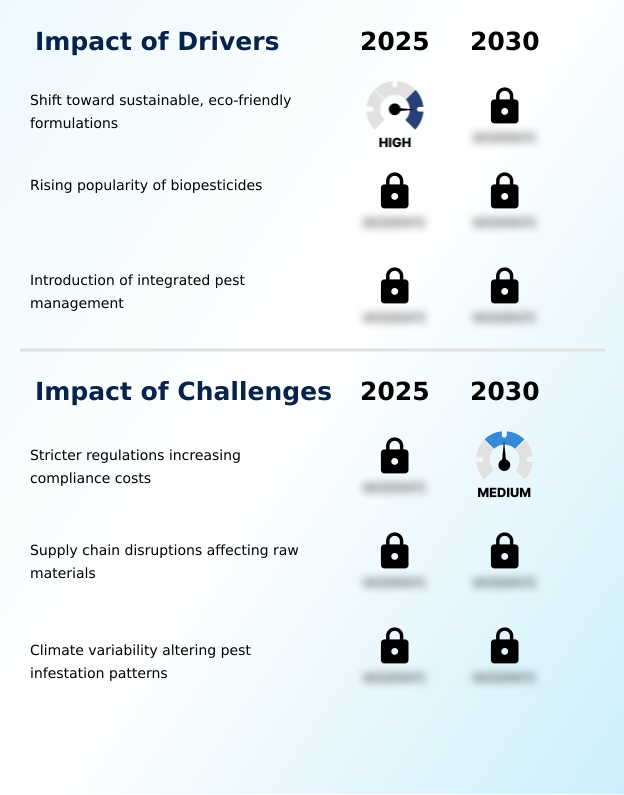

- A key driver for the market is the industry-wide shift toward sustainable and eco-friendly formulations that minimize environmental impact.

- Market growth is significantly influenced by a structural shift toward sustainability and integrated agricultural practices. The rising popularity of biopesticides, a cornerstone of climate-smart agriculture and eco-friendly formulations, is a primary driver.

- The adoption of Integrated Pest Management (IPM) programs can reduce reliance on conventional fungicides by 30-50% in certain high-value crops, contributing to soil health improvement.

- Furthermore, regulatory bodies are increasingly offering fast-track approval pathways for these biological control agents, with review times being up to 24 months shorter than for new synthetic molecules.

- This policy support, combined with consumer demand for residue-free food production, is accelerating investment in microbial pesticides and botanical extracts, fundamentally altering crop protection portfolios and promoting environmental stewardship.

What are the market trends shaping the Agricultural Pesticides Industry?

- A primary trend shaping the market is the increasing demand for pesticides, driven by the continuous rise in global food requirements. This necessity to protect crop yields underpins market momentum.

- Key trends are reshaping the global agricultural pesticides market 2026-2030, driven by the need for greater efficiency and sustainability. The growing adoption of precision spraying technologies, including drone-based systems, can increase application accuracy by over 40% in complex terrains, optimizing the use of insecticides. This aligns with a broader shift toward sustainable farming practices and crop management solutions.

- Concurrently, the emergence of nano-insecticide innovations is significant, with research indicating that these advanced delivery systems can reduce the required volume of active ingredients by up to 50% while maintaining high efficacy.

- This trend addresses both environmental impact reduction and the challenge of pesticide resistance, representing a transformative step in agricultural input technology and supporting both organic farming methods and conventional agriculture.

What challenges does the Agricultural Pesticides Industry face during its growth?

- A significant challenge impacting the industry involves increasingly stringent regulations, which elevate compliance costs for market participants.

- The global agricultural pesticides market 2026-2030 faces significant hurdles from stringent regulations and volatile supply chains. Regulatory compliance costs are a major factor, with the expense of bringing a new chemical active ingredient to market rising substantially; compliance now accounts for over 30% of total R&D expenditure. This financial pressure is compounded by supply chain disruptions for essential intermediates.

- Price volatility for these materials has led to cost spikes exceeding 200% during periods of disruption, impacting the production of broad-spectrum herbicides. These challenges are forcing a strategic pivot toward post-patent crop protection, diversifying sourcing, and investing in less regulated but effective plant growth regulators to ensure stability and manage pest infestation patterns.

Exclusive Technavio Analysis on Customer Landscape

The agricultural pesticides market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the agricultural pesticides market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Agricultural Pesticides Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, agricultural pesticides market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADAMA Ltd. - Offers a comprehensive portfolio of crop protection solutions, including herbicides, insecticides, and fungicides, designed to control pests and enhance agricultural yields.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADAMA Ltd.

- Albaugh LLC

- AMVAC Chemical Corp.

- BASF SE

- Bayer AG

- Coromandel International Ltd.

- Corteva Inc.

- Dhanuka Agritech Ltd.

- FMC Corp.

- Gowan Co.

- HELM AG

- KUMIAI CHEMICAL INDUSTRY CO.

- Mitsui Chemicals Inc.

- Nissan Chemical Corp.

- Nufarm Ltd.

- PI Industries Ltd.

- Rallis India Ltd.

- Syngenta Crop Protection AG

- UPL Ltd.

- Wynca Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Agricultural pesticides market

- In August 2024, Corteva Agriscience launched Ligate in Argentina, a specialized herbicide designed to address complex weed management challenges that have hindered productivity.

- In February 2025, BASF SE initiated the registration process for Prexio Active, a novel insecticide specifically designed to manage rice hopper species in the Asia-Pacific region.

- In March 2025, FMC Corp. and Bayer AG entered into a strategic partnership to introduce the Isoflex active herbicide technology to European markets for cereal crops.

- In May 2025, BioWorks launched PRINCIPLE WP, a bioinsecticide based on the fungus Beauveria bassiana, into the United States market for horticultural applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Agricultural Pesticides Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.2% |

| Market growth 2026-2030 | USD 25923.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, South Africa, Saudi Arabia, Turkey, UAE and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The agricultural pesticides market is evolving from a reliance on high-volume synthetic pesticides toward a sophisticated ecosystem of targeted solutions. This transition is driven by the dual imperatives of enhancing crop yield protection and adhering to stringent environmental standards.

- The core of this shift lies in advanced agricultural biotechnology, which enables the development of selective insecticides, systemic fungicides, and specialized seed treatments. Innovations in chemical active ingredient synthesis and nano-insecticide formulation are improving pest control performance while facilitating chemical residue reduction.

- The rising adoption of biopesticides and biological insect control methods is compelling executive boards to reallocate R&D budgets toward microbial pesticide development and sustainable crop protection. Companies leveraging precision agriculture technology have reported up to a 35% improvement in application efficiency, a key metric for demonstrating ROI.

- This focus on efficiency and sustainability is essential for navigating the complex landscape of pesticide resistance management and achieving long-term growth.

What are the Key Data Covered in this Agricultural Pesticides Market Research and Growth Report?

-

What is the expected growth of the Agricultural Pesticides Market between 2026 and 2030?

-

USD 25.92 billion, at a CAGR of 4.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Herbicides, Insecticides, Fungicides and bactericides, and Others), Product (Synthetic pesticides, and Biopesticides), Formulation (Liquid, Emulsifiable concentrate, Granular, and Wettable powder) and Geography (APAC, South America, Europe, North America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, South America, Europe, North America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Shift toward sustainable, eco‑friendly formulations, Stricter regulations increasing compliance costs

-

-

Who are the major players in the Agricultural Pesticides Market?

-

ADAMA Ltd., Albaugh LLC, AMVAC Chemical Corp., BASF SE, Bayer AG, Coromandel International Ltd., Corteva Inc., Dhanuka Agritech Ltd., FMC Corp., Gowan Co., HELM AG, KUMIAI CHEMICAL INDUSTRY CO., Mitsui Chemicals Inc., Nissan Chemical Corp., Nufarm Ltd., PI Industries Ltd., Rallis India Ltd., Syngenta Crop Protection AG, UPL Ltd. and Wynca Group

-

Market Research Insights

- The agricultural pesticides market is defined by a dynamic interplay between productivity mandates and sustainability goals, driving significant agrochemical innovation. The adoption of precision spraying technologies has demonstrated an ability to reduce chemical runoff by up to 60%, directly supporting environmental stewardship.

- Concurrently, adherence to integrated pest management (IPM) protocols has been linked to a 25% improvement in market acceptance for export crops due to lower chemical residues, a critical factor for producers targeting residue-free food production. This shift compels a focus on a diversified crop protection portfolio, including biological control agents and advanced formulations.

- As a result, sustainable production systems are becoming the standard, aligning with consumer demand for chemical-free produce and stricter phytosanitary regulations across global supply chains.

We can help! Our analysts can customize this agricultural pesticides market research report to meet your requirements.

RIA -

RIA -