Pet Sitting Market Size 2024-2028

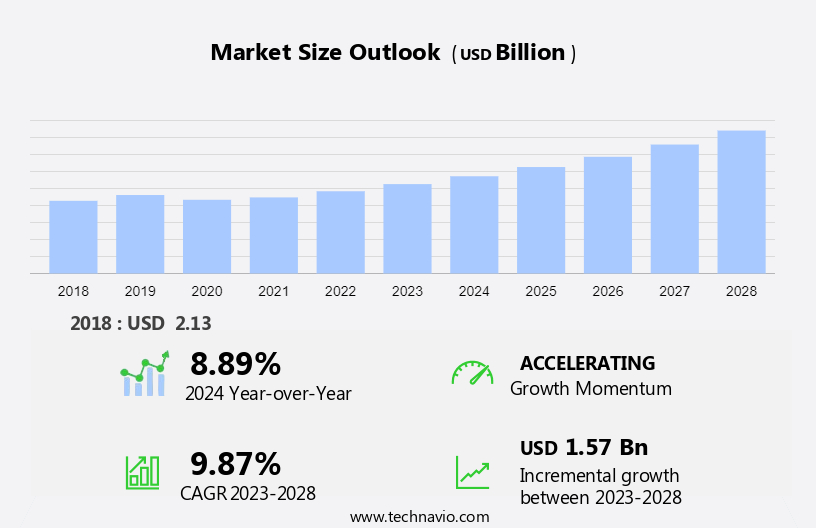

The pet sitting market size is forecast to increase by USD 1.57 billion at a CAGR of 9.87% between 2023 and 2028. The market is experiencing significant growth due to several key factors. First, the rising trend of pet humanization has led to increased pet ownership and spending on pets. Pet types encompass a wide range, from small mammals and birds to freshwater fish, smart pet livestock, and exotic pets. As pet owners prioritize their pets' wellbeing, they seek professional pet sitting services for care visits during their absence. Service types include regular check-ins, feeding, administering medication, and playtime. Compliance with stringent regulations and certifications is essential for pet sitting businesses to ensure the highest level of care and safety for pets. These factors collectively contribute to the market's growth and ongoing demand for professional services.

The pet sitting market is thriving as more pet owners seek reliable care for their furry companions. With the return-to-work trend, many retired people and students are turning to pet sitting services to accommodate their busy lifestyles. This growing demand has led to increased spending of consumers on quality pet care. In particular, the pet care cost associated with hiring a service provider can vary, but it ensures pets are well cared for while owners travel or work. Furthermore, societal shifts in pet acceptance have made pets a central part of many households, leading to a rise in the need for professional care. Ultimately, the pet sitting market reflects the evolving relationship between humans and their animal companions, providing peace of mind for pet owners.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for 2024-2028, as well as historical data from 2018-2022 for the following segments.

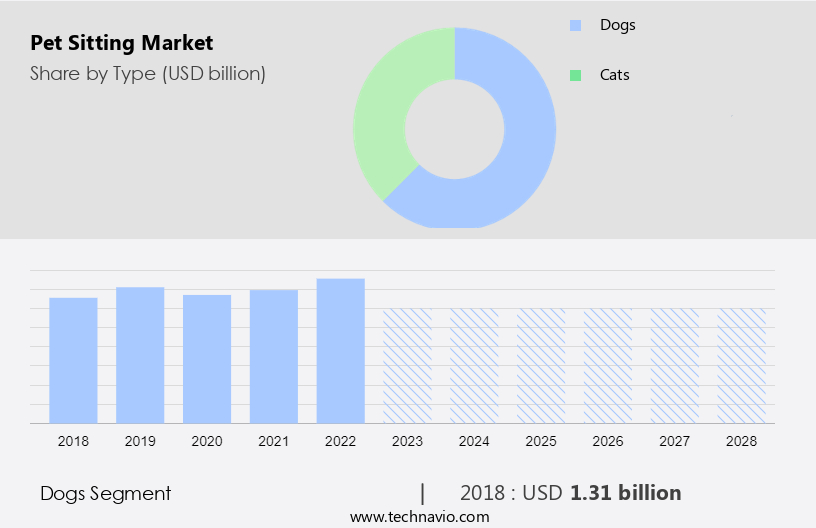

- Type

- Dogs

- Cats

- Service

- Care visits

- Drop-in visits

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- Middle East and Africa

- South America

- North America

By Type Insights

The dogs segment is estimated to witness significant growth during the forecast period. The market experiences significant growth due to the increasing popularity of dogs as pets and the resulting demand for pet care services. Dogs, the most commonly owned pets worldwide, are sought after for their ability to alleviate feelings of loneliness, reduce anxiety, stress, and depression, and promote physical activity and cardiovascular health. Additionally, dogs serve as valuable companions for children and the elderly, instilling responsibility, kindness, and empathy.

Additionally, pet owners require pet sitting services, including daycare visits and dog walking, when they are unable to be at home. Animal-borne disorders, such as abdominal pain and diarrhea, can necessitate the need for pet sitting services, further driving market growth. The rise of e-commerce platforms has also made it easier for pet owners to access a wide range of pet grooming products and services online, contributing to market expansion. Furthermore, legislation and regulations governing pet care and pet sitting services may vary by region, segmenting the market by pet type and location.

Get a glance at the market share of various segments Request Free Sample

The dogs segment was valued at USD 1.31 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

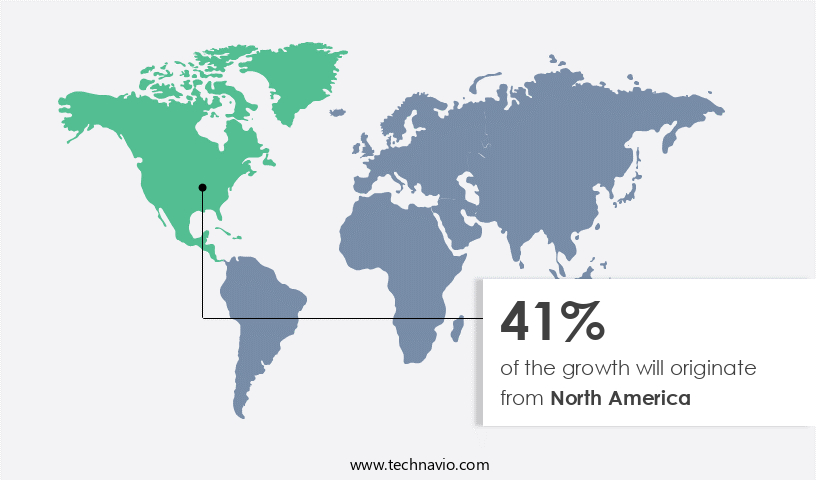

North America is estimated to contribute 41% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market, a significant sector within the pet care industry, experiences substantial growth, particularly in North America. With the US, Canada, and Mexico leading the way, this region hosts the largest number of pets and pet-sitting services worldwide. Factors such as the affordability of these services and the availability of experienced, full-time providers contribute significantly to the market's expansion in North America.

Additionally, increasing awareness among pet owners regarding various pet sitting options, including daycare visits and dog walking, further fuels market growth. Animal-borne disorders like abdominal pain and diarrhea necessitate the need for professional pet care services, leading to increased demand for pet sitting. Legislation mandating proper care for pets during their owners' absences also supports the market's growth.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The rising pet ownership and increased spending on pets is the key driver of the market. Pet sitting, as a service that allows pet owners to entrust the care of their animal companions to service providers, has experienced significant growth in response to the increasing adoption of pets among consumers. This trend can be attributed to the health benefits associated with pet ownership, particularly for millennials who are increasingly prioritizing their pets as valued members of their families.

Furthermore, the Centers for Disease Control and Prevention (CDC) highlights that owning companion pets offers numerous health advantages, such as reducing blood pressure, anxiety, cholesterol, and triglyceride levels, and delaying mental decline. Moreover, pets provide opportunities for regular exercise and socialization, fostering a pleasant bond between humans and animals. Pet sitting services play a crucial role in ensuring the well-being of pets when their owners are unable to be present, making them an essential component of the pet care industry.

Market Trends

Increasing pet humanization is the upcoming trend in the market. The market has experienced significant growth in recent years, driven in large part by the increasing humanization of pets. As more consumers view their pets as cherished animal companions rather than simple possessions, the demand for high-quality pet care services has risen.

Furthermore, pet owners, particularly millennials, are increasingly treating their pets as family members, leading them to seek out professional pet sitting services that provide human-like care and attention. These firms highlight the importance of pet sitting services in catering to the unique needs and preferences of pet owners, offering peace of mind and ensuring the well-being of pets while their owners are away.

Market Challenge

The need for compliance with stringent regulations and certifications is a key challenge affecting the market growth. Pet sitting, as a service that allows pet owners to entrust the care of their animal companions to service providers while they are away, has gained significant traction among consumers in recent years. To ensure the highest quality of care for pets, several organizations have established regulations to monitor pet-sitting service providers. One such organization is the Professional Animal Care Certification Council (PACCC), which offers certifications for pet sitting professionals based on their industry experience and responsibility levels.

Furthermore, these certifications, which include Certified Professional Animal Care Provider (CPACP), Certified Professional Animal Care Manager (CPACM), and Certified Professional Animal Care Operator (CPACO), confirm the providers' expertise in animal care and their commitment to providing balanced care for pets. The PACCC certifications are mandatory for pet sitting service providers who aim to be recognized as professionals in the industry.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Dogtopia Enterprises LLC: The company offers pet sitting services such as boarding for an overnight stay, weekend, holiday, or extended care.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bark

- Bark Park

- Careguide Inc.

- Dogtopia Enterprises LLC

- Fetch Pet Care

- Holidog

- Katie and Co. Pet Sitting

- Mad Paws

- Pawland

- Pawshake Inc.

- Pawspace

- PetBacker

- Petsfolio

- PetSmart Inc.

- Rover Group Inc.

- Swifto Inc.

- The Pet Sitting Co.

- TrustedHousesitters.com

- Wag Labs Inc.

- Wanderlust Pet Services Pvt Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Pet sitting, a form of animal care service, has gained significant traction among pet owners, particularly millennials, as the adoption of pets continues to rise. This market caters to the needs of pet parents who require assistance in caring for their animal companions while they are away from home. Service providers offer various types of services, including daycare visits, dog walking, pet transportation, and house-sitting services. The market serves a diverse range of consumers and their pets, including dogs, cats, fish, cage pets, birds, small mammals, exotic pets, and pet livestock. Animal wellbeing is a top priority, with service offerings extending to grooming, boarding, training, and veterinary care for pets suffering from animal-borne disorders such as abdominal pain and diarrhea.

The pet sitting market is experiencing significant growth, driven by increasing animal care expenditure, urbanization, and pet population. According to recent reports, pet owners in urban areas are spending more on specialized services such as subscription-based pet care solutions, including in-home pet sitting, daycare services, and boarding services. Technology advancements have played a crucial role in the growth of this market. Booking platforms have made it easier than ever for pet owners to find and book reliable pet care services online. From veterinary nurses to care visits services, pet health awareness has become a top priority for pet parents. The disposable income of pet owners continues to rise, leading to an increase in demand for high-quality pet care services. Boarding services and daycare services have become increasingly popular, offering pet owners peace of mind while they are away from home.

The pet sitting market is experiencing significant growth, fueled by increasing pet expenditure and the rising number of pet adoption. Pet Sitters International, a leading organization for professional pet sitters, reports a steady increase in demand for pet care service providers. With pet welfare regulations becoming stricter, the need for trusted caregivers who can offer personalized care is on the rise. Digital platforms have revolutionized the pet sitting industry, enabling individual pet sitters to expand their customer base and reach more potential clients. However, the market faces the risk of substitutes, such as automated pet feeders and monitoring systems. Premium pet services, offering community engagement and round-the-clock care, are gaining popularity among pet owners with shifting lifestyles. As the pet sitting market continues to evolve, it is essential for providers to stay informed about the latest trends, regulations, and customer preferences.

In conclusion, the pet sitting market presents a wealth of opportunities for entrepreneurs and professionals looking to make a difference in the lives of pets and their owners. By focusing on personalized care, adhering to welfare regulations, and leveraging digital platforms, pet care service providers can build a loyal customer base and thrive in this growing industry. Furthermore, legislation plays a crucial role in the market, ensuring the welfare and safety of animals. Segmental analysis reveals that the market is segmented based on pet types and service types. The forecast period sees an increasing trend of pet owners returning to work, driving the demand for overnight pet care and house-sitting services. Pet parents' spending on pet care costs, including pet insurance, is a significant factor influencing the growth of the market. A Brazilian start-up, for instance, offers a range of pet services, including care visits, drop-in visits, and rover services, catering to the varying needs of pet owners and their animal companions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.87% |

|

Market growth 2024-2028 |

USD 1.57 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.89 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 41% |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Bark, Bark Park, Careguide Inc., Dogtopia Enterprises LLC, Fetch Pet Care, Holidog, Katie and Co. Pet Sitting, Mad Paws, Pawland, Pawshake Inc., Pawspace, PetBacker, Petsfolio, PetSmart Inc., Rover Group Inc., Swifto Inc., The Pet Sitting Co., TrustedHousesitters.com, Wag Labs Inc., and Wanderlust Pet Services Pvt Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -