Plasma Protease C1 Inhibitor Market Size 2024-2028

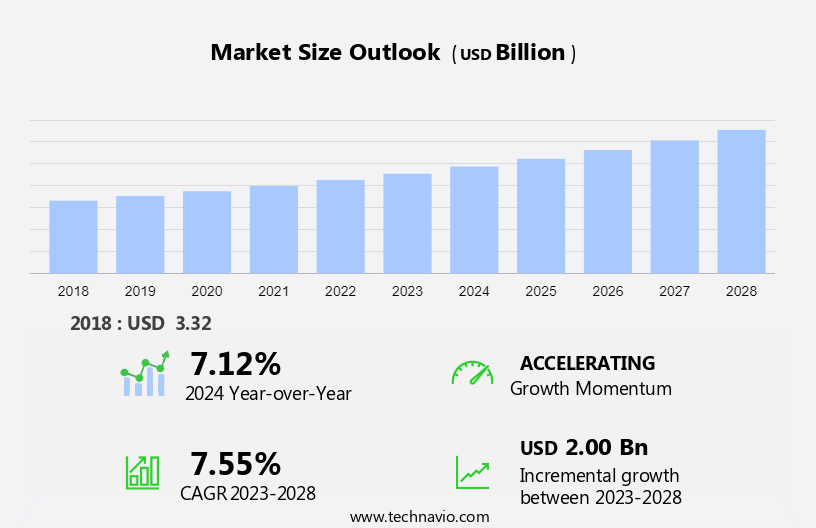

The plasma protease C1 inhibitor market size is forecast to increase by USD 2.00 billion at a CAGR of 7.55% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing research and development in this field. The growing adoption of bradykinin B2 receptor antagonists as effective treatments for various conditions, such as hereditary angioedema and paroxysmal nocturnal hemoglobinuria, is driving market expansion. However, the high cost and complex treatment procedures associated with plasma protease C1 inhibitors remain challenges for market growth. Despite these obstacles, the potential benefits of these therapies in improving patient outcomes and quality of life are expected to fuel market demand. The market analysis also covers emerging trends, such as the development of biosimilars and the exploration of alternative delivery methods, which are poised to disrupt the market landscape. Overall, the market is anticipated to experience steady growth In the coming years, driven by advancements in technology and the increasing prevalence of diseases that can be treated with these therapies.

What will be the Plasma Protease C1 Inhibitor Market Size During the Forecast Period?

- The market caters to the growing demand for treatments targeting inflammatory diseases, particularly those involving the complement and contact systems. Key conditions include sepsis and septic shock, where endotoxins trigger a cascade of inflammatory responses, leading to the activation of C1, C5a, bradykinin, and other mediators. Plasma Protease C1 Inhibitor plays a crucial role in inhibiting these proteases, thereby controlling the inflammatory response. The Serpin family, specifically C1-inh, is a vital component of the classical pathway, coagulation system, kinin system, and fibrinolytic system. Deficiencies in C1-inh lead to hereditary and acquired angioedema, characterized by symptoms such as swelling In the subcutaneous tissue, gastrointestinal mucosa, and upper respiratory tract.

- Moreover, replacement therapy using anti-plasmin agents is a common treatment approach. The market dynamics for Plasma Protease C1 Inhibitor are influenced by ongoing research and development efforts, regulatory approvals, and increasing awareness of inflammatory diseases. The trend towards personalized medicine and e-commerce platforms may also impact market growth. Despite this, challenges such as high production costs and the emergence of alternative therapies persist.

How is this Plasma Protease C1 Inhibitor Industry segmented and which is the largest segment?

The plasma protease C1 inhibitor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

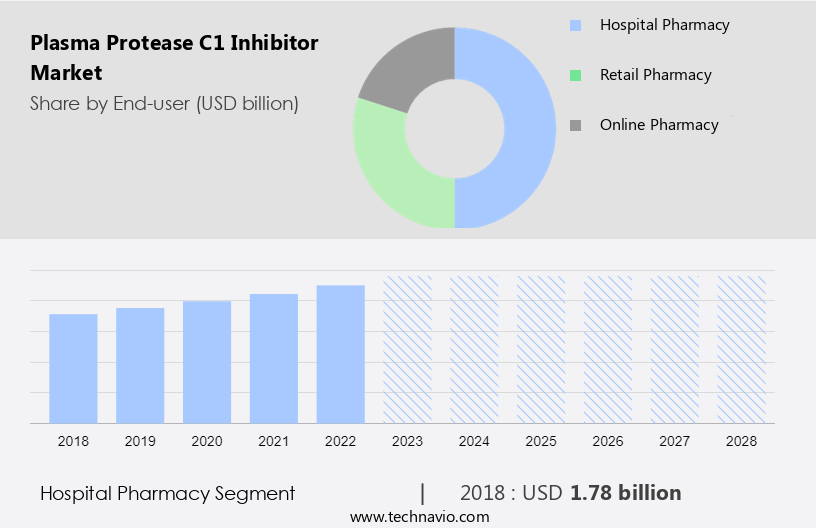

- Hospital pharmacy

- Retail pharmacy

- Online pharmacy

- Product

- Lyophilized

- Injectable

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

- The hospital pharmacy segment is estimated to witness significant growth during the forecast period.

The hospital pharmacy segment holds a significant position In the market due to the increasing prevalence of C1-INH deficiency, particularly hereditary angioedema. This condition necessitates the regular use of plasma protease C1 inhibitors for symptom management. Hospital pharmacies play a vital role in procuring, storing, and dispensing these medications to patients. The growing number of HAE diagnoses worldwide fuels the demand for plasma protease C1 inhibitors, providing an opportunity for hospital pharmacies to cater to the medication needs of these patients. Moreover, hospital pharmacies ensure the accessibility and availability of these essential medications for HAE patients.

Get a glance at the Plasma Protease C1 Inhibitor Industry report of share of various segments Request Free Sample

The hospital pharmacy segment was valued at USD 1.78 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

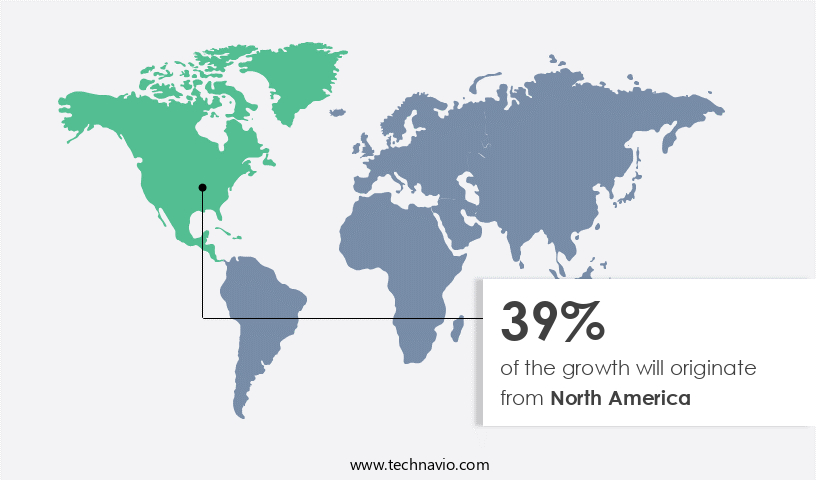

- North America is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market is significantly driven by the rising prevalence of inflammatory diseases, such as hereditary angioedema (HAE), and increasing research and development investments. North America dominates this market due to a well-established healthcare infrastructure and the presence of major market participants offering effective treatment options for HAE patients. Organizations like the US Hereditary Angioedema Association are dedicated to providing access to the latest treatments and support for patients. Recent studies, such as one published In the National Library of Medicine, evaluate HAE management and new treatment options' impact on physician practice patterns. The complement system and contact system play crucial roles in protease inhibition, and endotoxin naturally triggers the inflammatory response, further increasing market demand. Overall, the market is poised for growth due to these factors.

Market Dynamics

Our plasma protease C1 inhibitor market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Plasma Protease C1 Inhibitor Industry?

Increasing research and development in plasma protease C1 inhibitor is the key driver of the market.

- The market is projected to expand due to the growing focus of biopharmaceutical companies on developing effective treatments for inflammatory diseases, such as hereditary angioedema (HAE) and diabetic macular edema (DME), using plasma protease C1 inhibitor drugs. The complement system and contact system play crucial roles In the pathogenesis of these conditions, and plasma protease C1 inhibitor functions as a key regulator of these systems through protease inhibition. Kallikrein inhibitor medicines are currently In the preclinical and clinical stages of development.

- Furthermore, plasma protease C1 inhibitor deficiency results In the activation of the complement system, coagulation system, and kinin system, leading to angioedema symptoms such as swelling of the subcutaneous tissue, gastrointestinal mucosa, and upper respiratory tract. Plasma protease C1 inhibitor is a serine protease inhibitor that plays a significant role in regulating various plasma enzyme systems, including the classical pathway, coagulation system, and fibrinolytic system. The activation of these systems results In the formation of C1-INH complexes and activation complexes, which can be detected through ELISA. The molecular background of plasma protease C1 inhibitor deficiency involves the dysregulation of these systems, leading to the release of endotoxins, selectins, and autoantibodies.

What are the market trends shaping the Plasma Protease C1 Inhibitor Industry?

Growing adoption of bradykinin B2 receptor antagonist is the upcoming market trend.

- Plasma protease C1 inhibitors serve a vital function in regulating the complement and contact systems, which are crucial In the production of the inflammatory mediator, bradykinin. However, insufficient levels of these inhibitors can lead to uncontrolled bradykinin release, resulting in inflammatory conditions such as angioedema. In particular, hereditary angioedema (HAE) is characterized by C1-INH deficiency, leading to the activation of the complement and contact systems and subsequent bradykinin production. This results in symptoms such as swelling of the subcutaneous tissue, gastrointestinal mucosa, and upper respiratory tract. To manage HAE attacks and prevent future episodes, Bradykinin B2 receptor antagonists have gained significant attention In the market.

- In addition, these antagonists inhibit the activation of B2 receptors by bradykinin, thereby mitigating angioedema symptoms. The complement system, coagulation system, and fibrinolytic system are all involved In the pathogenesis of angioedema, and plasma protease C1 inhibitors play a crucial role In their regulation. Plasma concentrations of C1-INH and the presence of C1-INH complexes and activation complexes are essential markers in diagnosing HAE. The molecular background of HAE involves the dysregulation of the complement and contact systems, leading to the production of pro-inflammatory cytokines, endotoxins, and autoantibodies. The plasma enzyme systems, including plasmin, antiplasmin agents, and serine protease inhibitors, are also implicated In the pathogenesis of angioedema.

What challenges does the Plasma Protease C1 Inhibitor Industry face during its growth?

High cost and complex treatment of plasma protease C1 inhibitor is a key challenge affecting the industry growth.

- Plasma protease C1 inhibitor (C1-INH) is an essential anti-inflammatory protein involved In the regulation of various systems, including the complement system, contact system, coagulation system, and kinin system. Its primary function is protease inhibition, which plays a crucial role in preventing the activation of key enzymes such as plasma kallikrein, thrombin, and plasmin. C1-INH deficiency can lead to inflammatory diseases, including sepsis and septic shock, as well as hereditary and acquired angioedema. Angioedema symptoms, such as swelling of the subcutaneous tissue In the upper respiratory tract and gastrointestinal mucosa, can be debilitating and potentially life-threatening. Replacement therapy is often necessary during symptom-free periods to prevent HAE attacks.

- Furthermore, C1-INH functions as a serine protease inhibitor, regulating the pathogenesis of these conditions by modulating the activation of the complement and coagulation systems. Despite the benefits of C1-INH replacement therapy, it comes with challenges. The risk of blood-borne diseases, such as HIV, hepatitis B, and hepatitis C, is a concern due to the use of plasma-derived products. Although primary blood screening is performed, the risk of infection transmission during transfusion remains significant due to various pathogen strains, blood purification-resistant pathogens, and the threat of new viruses. In the US market, the demand for C1-INH replacement therapies continues to grow, driven by the increasing prevalence of inflammatory diseases and the need for effective treatments.

Exclusive Customer Landscape

The plasma protease c1 inhibitor market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the plasma protease c1 inhibitor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, plasma protease c1 inhibitor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- AstraZeneca Plc

- Bausch Health Companies Inc.

- Bio Techne Corp.

- BioCryst Pharmaceuticals Inc.

- Biosynth Ltd.

- Bristol Myers Squibb Co.

- Cayman Chemical

- CSL Ltd.

- FibroGen Inc.

- Fresenius SE and Co. KGaA

- Gilead Sciences Inc.

- Ionis Pharmaceuticals Inc.

- KalVista Pharmaceuticals Inc.

- Merck KGaA

- Novartis AG

- Pharming Group NV

- Sino Biological Inc.

- Takeda Pharmaceutical Co. Ltd.

- Thermo Fisher Scientific Inc.

- Vertex Pharmaceuticals Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The plasma protease C1 inhibitor (C1-INH) is a crucial component of the human body's defense system against inflammation and coagulation. This protein plays a pivotal role in regulating various physiological processes, including the complement system, contact system, and coagulation system. C1-INH functions as a serine protease inhibitor, preventing the activation of complement components C1r and C1s, and regulating the contact system by inhibiting plasma kallikrein and factor XIIa. In the coagulation system, C1-INH acts as a cofactor for activated protein C (APC) and inhibits the activation of factor Va and VIIIa.

Moreover, inflammatory diseases, such as sepsis and septic shock, are characterized by an excessive activation of the complement system and coagulation cascade. C1-INH deficiency can lead to uncontrolled activation of these systems, resulting in various complications, including angioedema, thrombosis, and hemorrhage. The complement system is a critical part of the innate immune response, and its dysregulation can lead to the development of inflammatory diseases. Endotoxins, such as lipopolysaccharides (LPS), can activate the complement system, leading to the production of anaphylatoxins and the recruitment of inflammatory cells to the site of infection. C1-INH plays a crucial role in regulating this response by inhibiting the activation of the complement system's classical pathway.

In addition, the contact system, another pathway of the coagulation cascade, is also regulated by C1-INH. The contact system is activated upon interaction between blood and surfaces, leading to the generation of bradykinin and the initiation of the coagulation cascade. C1-INh inhibits the activation of plasma kallikrein, a key enzyme In the contact system, preventing the excessive production of bradykinin and the subsequent coagulation response. The pathogenesis of inflammatory diseases, such as hereditary angioedema (HAE) and acquired angioedema (AAE), is characterized by a deficiency or dysfunction of C1-INH. In HAE, the deficiency is caused by mutations In the C1-INH gene, leading to a reduced production of functional C1-INH.

Furthermore, in AAE, the dysfunction is caused by the formation of C1-INH autoantibodies, which neutralize the functional activity of C1-INH. The symptoms of angioedema, a common complication of C1-INH deficiency, can affect various parts of the body, including the subcutaneous tissue, gastrointestinal mucosa, and upper respiratory tract. Symptoms can range from mild swelling to life-threatening airway obstruction. Replacement therapy with C1-INH is an effective treatment for these conditions, preventing the symptoms and reducing the risk of complications. Plasma enzyme systems, such as plasmin and antiplasmin agents, also play a role In the regulation of the coagulation system. Plasmin is a proteolytic enzyme that degrades fibrin clots, while antiplasmin agents inhibit its activity.

|

Plasma Protease C1 Inhibitor Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.55% |

|

Market growth 2024-2028 |

USD 2.00 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.12 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, market growth and forecasting , Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Plasma Protease C1 Inhibitor Market Research and Growth Report?

- CAGR of the Plasma Protease C1 Inhibitor industry during the forecast period

- Detailed information on factors that will drive the Plasma Protease C1 Inhibitor growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the plasma protease c1 inhibitor market growth of industry companies

We can help! Our analysts can customize this plasma protease c1 inhibitor market research report to meet your requirements.

RIA -

RIA -