Mexico Plastic Packaging Market Size 2025-2029

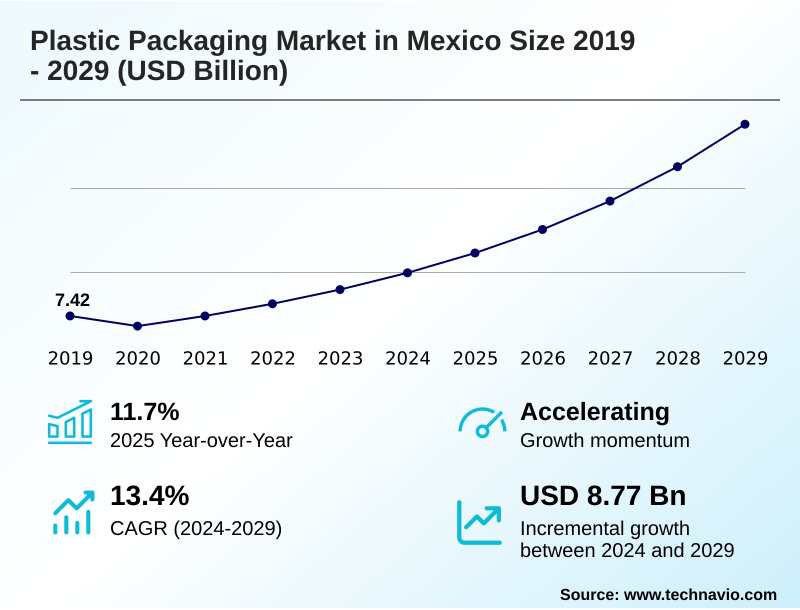

The mexico plastic packaging market size is valued to increase by USD 8.77 billion, at a CAGR of 13.4% from 2024 to 2029. Rising focus on improving shelf life of products will drive the mexico plastic packaging market.

Major Market Trends & Insights

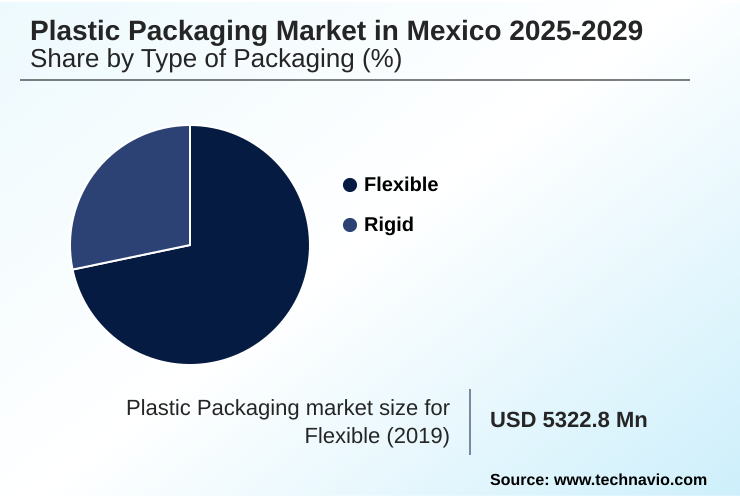

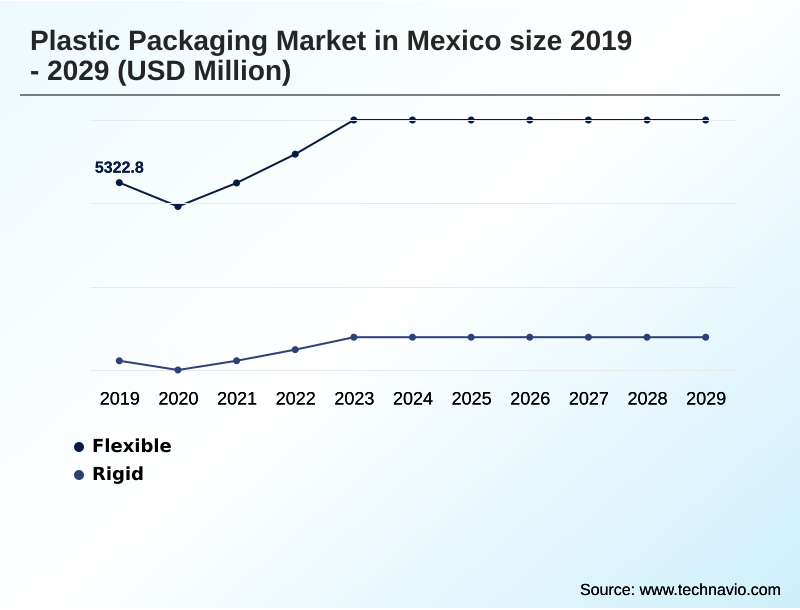

- By Type of Packaging - Flexible segment was valued at USD 6.46 billion in 2023

- By End-user - Food and beverages segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 11.32 billion

- Market Future Opportunities: USD 8.77 billion

- CAGR from 2024 to 2029 : 13.4%

Market Summary

- The plastic packaging market in Mexico is defined by a dynamic interplay between robust industrial demand, evolving consumer preferences, and a significant shift toward sustainability. A primary growth engine is the country's strengthening position as a manufacturing hub, amplified by nearshoring, which creates sustained demand for a wide array of plastic packaging solutions.

- The food and beverage sector remains the bedrock of this demand, where flexible packaging and rigid packaging formats are essential for safety and convenience. Innovations in materials like polyethylene terephthalate and high-density polyethylene are critical.

- For instance, a multinational CPG firm leverages advanced barrier films and resealable packaging to extend the shelf life of perishable goods, reducing spoilage-related losses by over 15% while meeting consumer demand. However, the industry also navigates challenges from environmental regulations and the push for alternatives, driving the adoption of post-consumer recycled resin and designs that facilitate a circular economy.

- End-user segments, including pharmaceutical and personal care, further contribute to the market's complexity, requiring specialized solutions that balance performance, cost, and environmental responsibility.

What will be the Size of the Mexico Plastic Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Mexico Plastic Packaging Market Segmented?

The mexico plastic packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type of packaging

- Flexible

- Rigid

- End-user

- Food and beverages

- Healthcare

- Retail

- Others

- Application

- Primary packaging

- Secondary packaging

- Tertiary packaging

- Geography

- North America

- Mexico

- North America

By Type of Packaging Insights

The flexible segment is estimated to witness significant growth during the forecast period.

The flexible packaging segment is characterized by its adaptability, encompassing formats whose shape can be readily changed, including pouches, wraps, and films.

This category's growth is driven by its widespread use in the food and beverage, pharmaceutical, and retail industries, where it offers significant advantages in product preservation and consumer convenience through features like resealable packaging.

The adoption of advanced materials like bioriented polypropylene films and other recyclable polymers supports the development of sustainable packaging solutions. Innovations in lightweight packaging formats, such as stand-up pouches, reduce transportation-related emissions by up to 25% compared to rigid alternatives.

The use of coextruded films enhances barrier properties, making flexible options a preferred choice for applications demanding both product protection and packaging design innovation, aligning with modern supply chain efficiency goals.

The Flexible segment was valued at USD 6.46 billion in 2023 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic application of plastic packaging is evolving beyond simple containment, with innovations targeting specific performance and sustainability goals. For instance, HDPE bottles for chemical storage provide critical durability, while PET containers for carbonated drinks are engineered for barrier integrity.

- In the food sector, flexible packaging for frozen foods ensures protection against freezer burn, and improving shelf life with MAP is a standard practice for fresh produce. The push for efficiency drives lightweighting in plastic bottle design, which can reduce material usage by more than 10% per unit compared to older designs.

- Advancements in recyclable polymer films are crucial to meeting corporate responsibility targets, directly addressing the challenges of multilayer film recycling. The role of plastic packaging in e-commerce has expanded, demanding robust yet lightweight solutions. The industry is exploring bio-based plastics for food contact, though regulatory compliance for food-grade plastics remains a complex hurdle.

- Meanwhile, trends in smart packaging for pharmaceuticals are enhancing patient safety and tracking. The cost-benefit of post-consumer recycled resin is increasingly favorable, prompting its wider adoption. Other key areas of development include thermoformed trays for medical devices, aseptic packaging solutions for dairy, and designing the optimal stand-up pouch design for shelf appeal.

- The performance of materials is also under scrutiny, from the barrier properties of coextruded films to the ongoing debate over the sustainability of rigid vs flexible packaging. Finally, consumer preference for transparent packaging continues to influence product marketing and design choices.

What are the key market drivers leading to the rise in the adoption of Mexico Plastic Packaging Industry?

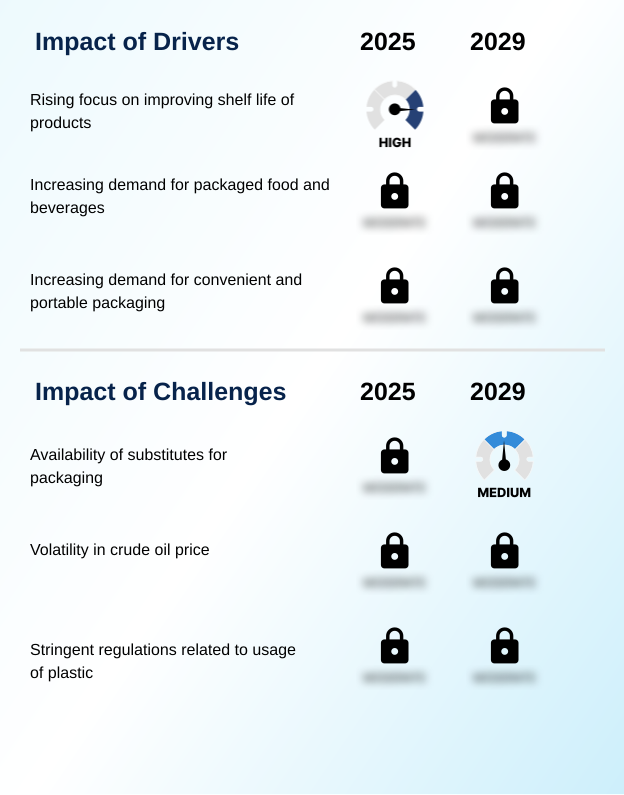

- A rising focus on improving the shelf life of products is a key driver for the market.

- A primary market driver is the intensified focus on product shelf life extension, which is crucial for reducing waste and enhancing supply chain efficiency, particularly in the food and beverage packaging and pharmaceutical packaging sectors.

- Technologies such as modified atmosphere packaging and the use of advanced barrier films are instrumental in protecting products from spoilage.

- These methods have been shown to extend the viability of perishable goods by up to 50% and reduce in-transit spoilage by 25%. Innovations like resealable packaging and aseptic packaging further contribute to this trend by preserving freshness after opening.

- The development of specialized laminates and coextruded films with superior protective properties is enabling manufacturers to meet stringent food safety standards while delivering longer-lasting products to consumers.

What are the market trends shaping the Mexico Plastic Packaging Industry?

- The growing popularity of lightweight packaging is a key upcoming market trend. This shift is driven by cost-effectiveness and enhanced recyclability.

- A prominent trend is the growing popularity of lightweight packaging, a strategy that delivers both economic and environmental benefits. By reducing material mass through advanced engineering and the use of high-performance recyclable polymers, manufacturers can lower production expenses and shipping costs. This approach has enabled some companies to achieve a 15% reduction in logistics-related expenditures.

- The development of thinner yet stronger extruded tubes and films, facilitated by innovations in injection molding and blow molding, allows for significant material savings without compromising product integrity.

- This focus on lightweighting directly supports packaging waste reduction goals and improves overall packaging machinery integration, making it a critical area of innovation for both flexible packaging and rigid packaging applications in a competitive marketplace.

What challenges does the Mexico Plastic Packaging Industry face during its growth?

- The availability of packaging substitutes presents a key challenge affecting industry growth.

- A significant challenge facing the market is the increasing availability and consumer acceptance of substitute materials, driven by environmental concerns. Alternatives such as paper, glass, and metal are gaining traction, with paper-based options capturing a 10% share in certain consumer goods segments. This trend pressures plastic packaging manufacturers to innovate, particularly in areas like blister packaging and doypacks.

- While plastic often maintains a 30% cost advantage in high-volume applications and offers superior performance in formats like shrink films, the industry must address perceptions related to sustainability.

- This involves advancing the use of compostable packaging and enhancing the recyclability of materials like those used in stand-up pouches, ensuring plastic remains a competitive choice for industrial packaging and personal care packaging.

Exclusive Technavio Analysis on Customer Landscape

The mexico plastic packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mexico plastic packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Mexico Plastic Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, mexico plastic packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALPLA Werke Alwin Lehner - Vendors provide specialized plastic packaging, including bottles, films, and containers, engineered for diverse applications in food, healthcare, and consumer goods sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALPLA Werke Alwin Lehner

- Altopro SA de CV

- Amcor Plc

- AptarGroup Inc.

- Berry Global Inc.

- CCL Industries Inc.

- Clifton Packaging Group Ltd.

- Constantia Flexibles GmbH

- FLAIR Flexible Packaging Corp

- Flexitek de Mexico SA de CV

- Mondi Plc

- Plastipak Holdings Inc.

- PO Empaques Flexibles SA de CV

- Printpack Inc.

- Sealed Air Corp.

- SigmaQ Packaging, S.A.

- Transcontinental Inc.

- Winpak Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mexico plastic packaging market

- In September 2024, Amcor Plc announced the commercial launch of its new recyclable, high-barrier mono-material pouch designed for sensitive food products, reducing plastic waste by 30% compared to traditional multi-layer laminates.

- In November 2024, Berry Global Inc. completed the acquisition of a leading Mexican flexible packaging manufacturer, enhancing its regional production capacity for food and healthcare applications and strengthening its supply chain in North America.

- In February 2025, Mondi Plc entered into a strategic partnership with a major chemical company to integrate certified circular polymers into its flexible packaging portfolio for the consumer goods sector in Mexico.

- In April 2025, a consortium of major CPG companies and packaging vendors, including Sealed Air Corp., launched a multi-year initiative in Mexico to standardize post-consumer recycled (PCR) resin specifications, aiming to boost the circular economy for plastics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mexico Plastic Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 181 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.4% |

| Market growth 2025-2029 | USD 8770.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 11.7% |

| Key countries | Mexico |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The plastic packaging sector is undergoing a significant transformation, driven by material innovation and sustainability mandates. Core materials like polyethylene terephthalate and high-density polyethylene are being re-engineered for enhanced performance and recyclability. The adoption of modified atmosphere packaging and advanced barrier films is critical for extending product viability.

- Boardroom decisions are increasingly influenced by the shift toward sustainable packaging solutions, as evidenced by the integration of post-consumer recycled resin, which can lower a company's carbon footprint by up to 20% compared to virgin plastics. This transition impacts both flexible packaging and rigid packaging formats.

- Innovations in bioriented polypropylene films and thermoforming processes are enabling the creation of lightweight packaging. Formats like stand-up pouches, doypacks, and blister packaging made from coextruded films are gaining market share.

- Meanwhile, the use of extruded tubes, laminates, and shrink films continues across various applications, with processes like blow molding and injection molding defining manufacturing capabilities for both aseptic packaging and resealable packaging.

What are the Key Data Covered in this Mexico Plastic Packaging Market Research and Growth Report?

-

What is the expected growth of the Mexico Plastic Packaging Market between 2025 and 2029?

-

USD 8.77 billion, at a CAGR of 13.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type of Packaging (Flexible, and Rigid), End-user (Food and beverages, Healthcare, Retail, and Others), Application (Primary packaging, Secondary packaging, and Tertiary packaging) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Rising focus on improving shelf life of products, Availability of substitutes for packaging

-

-

Who are the major players in the Mexico Plastic Packaging Market?

-

ALPLA Werke Alwin Lehner, Altopro SA de CV, Amcor Plc, AptarGroup Inc., Berry Global Inc., CCL Industries Inc., Clifton Packaging Group Ltd., Constantia Flexibles GmbH, FLAIR Flexible Packaging Corp, Flexitek de Mexico SA de CV, Mondi Plc, Plastipak Holdings Inc., PO Empaques Flexibles SA de CV, Printpack Inc., Sealed Air Corp., SigmaQ Packaging, S.A., Transcontinental Inc. and Winpak Ltd.

-

Market Research Insights

- The market is characterized by rapid evolution, driven by technological advancements and shifting consumer demands for sustainability. The adoption of smart packaging, which enhances traceability, has led to a 20% reduction in supply chain losses for high-value goods in the pharmaceutical packaging sector.

- Firms actively implementing circular economy principles are improving their packaging sustainability metrics by up to 35% compared to those using linear models. Furthermore, innovations in packaging material science are enabling retail-ready packaging designs that reduce shelf-stocking time by more than half, directly impacting operational efficiency for consumer packaged goods (CPG).

- This focus on functional and eco-conscious design underscores the industry's response to both regulatory pressures and market opportunities.

We can help! Our analysts can customize this mexico plastic packaging market research report to meet your requirements.

RIA -

RIA -