Polyethylene Terephthalate Market Size 2025-2029

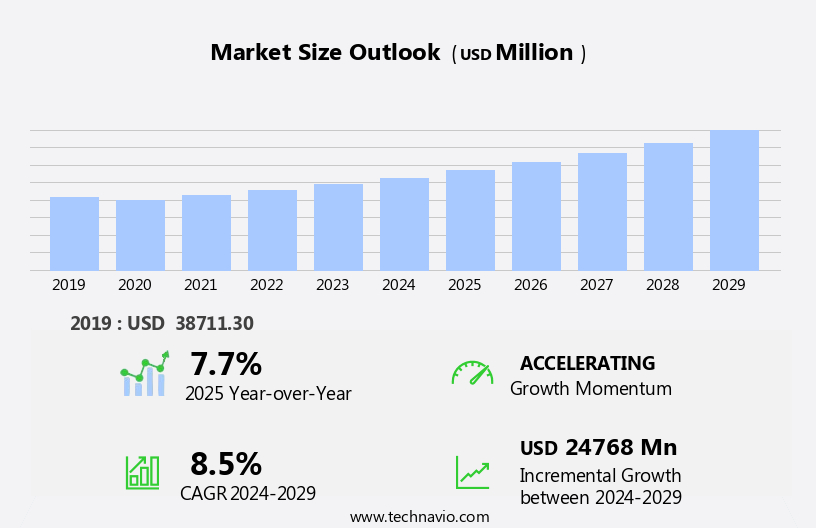

The polyethylene terephthalate market size is forecast to increase by USD 24.77 billion at a CAGR of 8.5% between 2024 and 2029.

- The Polyethylene Terephthalate (PET) market is experiencing significant growth, driven by the increasing consumption of packaging materials. The demand for PET in the packaging sector is on the rise due to its versatility, durability, and recyclability. Furthermore, the adoption of bio-based PET products is gaining momentum as companies seek sustainable alternatives to traditional fossil fuel-derived PET. However, the market faces challenges, most notably the volatility in crude oil prices.

- Additionally, investing in research and development to improve the production efficiency and sustainability of PET could provide a competitive edge. Consumer preferences for non-biodegradable plastic packaging drive the demand for PET bottles, thermoformed packaging, and personal care products. Navigating these dynamics requires a deep understanding of market trends and the ability to adapt quickly to changing conditions. This price instability can impact the production costs of PET, making it a critical factor for manufacturers to consider in their operational planning. To capitalize on the market's opportunities, companies must stay agile and responsive to shifting consumer preferences and price fluctuations.

What will be the Size of the Polyethylene Terephthalate Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The Polyethylene Terephthalate (PET) market witnesses significant activity as beverage producers adopt circular economy strategies to reduce waste and minimize material losses. Government environmental policies drive the shift towards sustainable manufacturing techniques, including those used in the rail industry's resin production. The coronavirus period disrupted crude oil prices, impacting the cost structure of PET production. In marine applications, PET's lightweight and durable properties continue to gain traction. In the medical field, PET is used for medical devices, while in the industrial sector, it is employed for cable sheathing, thermal insulation products, and engineering resins. Machinery suppliers invest in fusion technology to enhance manufacturing efficiency, while R&D efforts focus on circular innovations for the furniture industry.

Fusion technology and circular economy initiatives contribute to the production of recycled PET foam, insulation products, and flexible packaging. Woven plastic packaging remains a growing sector due to its versatility and cost-effectiveness. Technical limitations and stringent regulations pose challenges to market expansion. Despite these hurdles, the PET industry remains dynamic, with innovation and sustainability at its core.

How is this Polyethylene Terephthalate Industry segmented?

The polyethylene terephthalate industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Fibers

- Resins

- Others

- Type

- Virgin

- Recycled

- End-user

- Food and beverage

- Textiles

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Russia

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

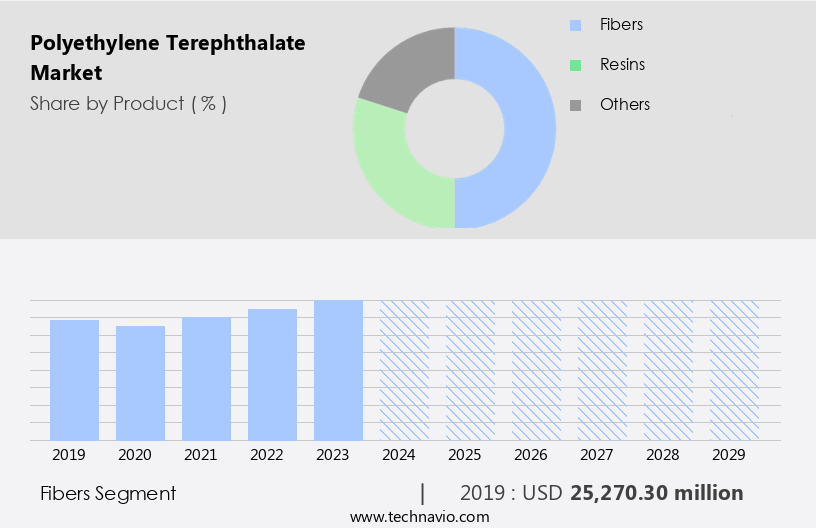

By Product Insights

The Fibers segment is estimated to witness significant growth during the forecast period. In the dynamic polyethylene terephthalate (PET) industry, various entities play pivotal roles. Dimethyl terephthalate (DMT) serves as a crucial raw material for PET production, while plastic recycling facilitates the reuse of PET fines and rPET pellets. Purified terephthalic acid and monoethylene glycol (MEG) are essential intermediates. PET preform machines produce containers for fresh produce, household products, and insulating tapes, showcasing PET's barrier properties. Virgin plastics coexist with recycled plastics, with the latter gaining traction due to environmental concerns and stringent regulations. Crude oil prices influence the cost dynamics of the industry, as PET is derived from crude oil. The PET recycling facility plays a vital role in reducing plastic waste and producing rPET flakes.

The rail industry uses PET for various applications, including printed designs on trains and antimicrobial property coatings for passenger safety. The mechanical properties of PET make it suitable for various applications, including beverage producers, marine applications, and industrial packaging. Technical limitations, such as material losses due to alcoholysis depolymerization, are being addressed through R&D efforts. Machinery suppliers provide equipment for PET production, while trade associations release reports on industry trends. In the Coronavirus period, the PET industry has shown resilience, with demand for PET bottles, packaging, and insulation products remaining robust. The polyester family, including PET, continues to evolve with innovations such as circular innovations and new applications in shipping facilities, rubber sheets, and electrical properties.

The Fibers segment was valued at USD 25.27 billion in 2019 and showed a gradual increase during the forecast period.

The Polyethylene Terephthalate (PET) Market is expanding across diverse sectors, from nonfood items to food packaging, including jars for peanut butter and bottles for flavored milk. Its compatibility with additives like polymeric plasticizer enhances durability and performance. PET composites reinforced with glass fiber are gaining traction in industrial applications, though inferior application methods can affect quality. Innovations in nitrile rubber blends improve PET flexibility for specialized uses. Key performance attributes like dielectric constant make PET valuable in electrical insulation. Insights from trade associations releases continue to steer sustainable manufacturing practices and standardization across the industry.

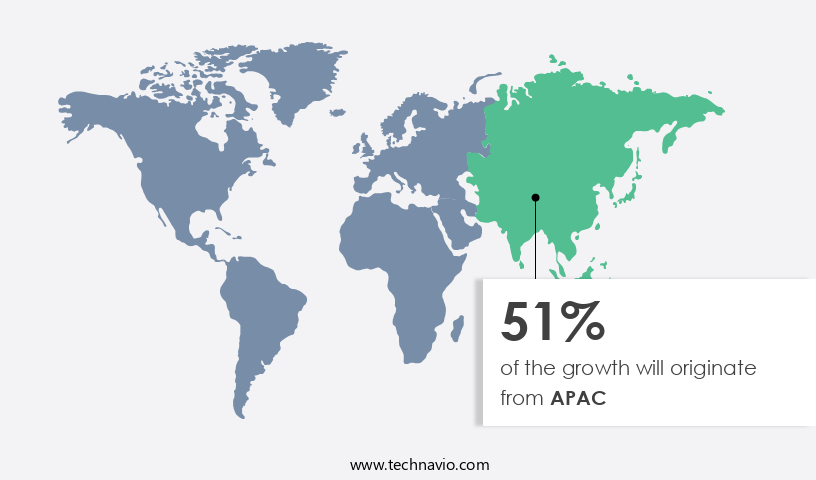

Regional Analysis

APAC is estimated to contribute 51% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The polyethylene terephthalate (PET) market is driven by the robust demand in Asia Pacific (APAC), particularly from China and India, which accounted for the largest market share in 2024. PET's popularity is attributed to its versatile applications, including fresh produce packaging, household products, insulating tapes, and personal care items. In the APAC region, Japan and South Korea maintain a consistent demand for PET due to their industrial sectors and high consumer preferences for non-biodegradable plastic packaging. China, as a major manufacturing hub, produces a significant amount of low-value PET, contributing to its dominance in the market. Despite stringent regulations on plastic waste and increasing crude oil prices, the circular economy and circular innovations, such as recycled PET foam and rPET pellets, are gaining traction.

The PET industry also benefits from advancements in technology, including fusion technology, thermal lamination, and machinery suppliers. In the medical field, PET's barrier properties and antimicrobial property coatings make it a preferred choice for medical devices and packaging. The Coronavirus period has led to an increased demand for PET bottles and thermoformed packaging for various industries, including beverage producers, industrial packaging, and rail industry. Additionally, the use of PET in marine applications, cable sheathing, and thermal insulation products further expands its market reach.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Polyethylene Terephthalate market drivers leading to the rise in the adoption of Industry?

- The significant rise in the consumption of packaging materials serves as the primary catalyst for market growth. The Polyethylene Terephthalate (PET) market is driven by the increasing demand for packaging applications. Packaging is the primary end-user segment, accounting for a significant market share. The appeal of PET packaging lies in its ability to showcase printed designs, which influence consumer preferences. PET is widely used in various industries, including food and beverages, for packaging salad dressings, cooking oil, and other liquid products. Flexible packaging, such as thermoplastic polymer resin, is also gaining popularity due to its lightweight and cost-effective nature.

- R&D efforts are underway to improve the durability and sustainability of PET, addressing concerns related to plastic waste. The Coronavirus period has accelerated the demand for non-biodegradable plastic packaging due to its ability to maintain product integrity during transportation and storage. Industries like medical devices and the rail industry also rely on PET for its strength and versatility. Despite material losses due to alcoholysis depolymerization, the potential applications of PET continue to expand, making it a valuable investment for businesses. Moreover, the recycling of plastics, particularly rPET flakes, is a growing trend. The antimicrobial property coatings applied to PET bottles and woven plastic packaging add an extra layer of protection, enhancing their appeal.

What are the Polyethylene Terephthalate market trends shaping the Industry?

- The use of bio-based PET products is gaining popularity as the latest market trend. This eco-friendly alternative to traditional petrochemical-based PET is increasingly being adopted due to its sustainable production process and reduced carbon footprint. As the global consciousness towards environmental sustainability grows, there is a rising demand for eco-friendly packaging materials among consumer product manufacturers. This trend is particularly significant in the plastic and resin industry, where Polyethylene Terephthalate (PET) is a widely used material. The increased focus on sustainability has led to more emphasis on the circular economy and the use of renewable resources in manufacturing. PET, derived from ethylene glycol and terephthalic acid, is a popular choice due to its versatility and durability.

- Fusion technology, a recycling process that combines PET with other polymers, is gaining popularity as it produces high-quality recycled plastic. Moreover, the use of PET in various applications, such as blister packaging for baked goods, cable sheathing, thermal insulation products, plastic bottles, and thermoformed packaging for personal care products and hair care, is increasing. The medical field also extensively uses PET as a flexible substrate material for various applications due to its excellent barrier properties. The circular economy approach to PET manufacturing and usage is expected to gain momentum as it reduces the need for virgin raw materials and minimizes waste. However, the production of PET from non-renewable resources contributes to environmental pollution. To address this concern, there is a growing interest in using recycled PET as a raw material.

How does Polyethylene Terephthalate market face challenges during its growth?

- The volatility in crude oil prices poses a significant challenge to the growth of the industry, requiring professionals to closely monitor and adapt to market fluctuations. The Polyethylene Terephthalate (PET) market has been experiencing price volatility due to the fluctuating prices of raw materials, primarily terephthalic acid and monoethylene glycol. The recent geopolitical tensions, such as the Russia-Ukraine war, have caused concerns over the supply of Russian oil, leading to a rise in oil prices, which in turn impacts the cost of PET production. As a petroleum and natural gas derivative, PET's price is closely linked to the prices of these commodities. Moreover, the oil and gas industry's efforts to reduce costs due to the decline in oil prices have resulted in workforce reductions among machinery suppliers, potentially impacting the availability and cost of engineering resins and dielectric strength components essential for PET production.

- Despite these challenges, the PET market continues to gain traction due to its versatile applications in various industries, including the furniture industry for its durability and mechanical properties, beverage producers for its use in industrial packaging, and marine applications for its electrical insulation components. Additionally, circular innovations in PET recycling and reuse have gained significant attention, providing opportunities for growth in the market. The PET market's growth dynamics are influenced by the price fluctuations of raw materials, primarily terephthalic acid and monoethylene glycol, and the impact of geopolitical events on the oil industry.

Exclusive Customer Landscape

The polyethylene terephthalate market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polyethylene terephthalate market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, polyethylene terephthalate market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpek SAB de CV - The company specializes in polyethylene terephthalate (PET), offering solutions for diverse applications such as food packaging, beverage bottles, and a wide range of consumer products.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpek SAB de CV

- BASF SE

- Covestro AG

- Dhunseri Tea and Industries Ltd.

- DSM-Firmenich AG

- DuPont de Nemours Inc.

- Eastman Chemical Co.

- EasyPak LLC

- Far Eastern New Century Corp.

- Formosa Plastics Corp.

- Indorama Ventures Public Co. Ltd.

- Jiangsu Sanfangxiang Group Co. Ltd.

- Lanxess AG

- Mitsubishi Chemical Corp.

- NEO GROUP UAB

- Plastipak Holdings Inc.

- Reliance Industries Ltd.

- Saudi Arabian Oil Co.

- Toray Industries Inc.

- Verdeco Recycling Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polyethylene Terephthalate Market

- In January 2024, LG Chem and TotalEnergies announced a strategic collaboration to jointly produce and commercialize polyethylene terephthalate (PET) resin using 100% renewable feedstock (Reuters). This initiative is expected to reduce the carbon footprint of PET production and cater to the growing demand for sustainable plastics.

- In March 2024, SABIC and Covestro signed a memorandum of understanding to explore the production of circular PET from post-consumer recycled materials (Wall Street Journal). This partnership aims to address the challenge of recycling PET and contribute to the circular economy in the plastics industry.

- In May 2024, Indorama Ventures, a leading PET producer, announced the acquisition of Borealis AG's polyolefins business for â¬4.3 billion (Bloomberg). This acquisition expanded Indorama Ventures' polyolefin capacity and strengthened its position as a global leader in the PET market.

- In April 2025, Daicel Corporation and Teijin Limited jointly announced the completion of their PET production plant in Thailand, with an annual capacity of 600,000 tons (Reuters). This expansion will enable both companies to cater to the increasing demand for PET in the Asia Pacific region and strengthen their market presence.

Research Analyst Overview

The polyethylene terephthalate (PET) industry continues to evolve, driven by dynamic market forces and diverse applications. Raw material prices, influenced by crude oil and purified terephthalic acid, impact production costs. The circular economy gains momentum with the increased use of recycled PET pellets and flakes in various sectors. Fusion technology and polymeric plasticizers enhance the barrier properties of PET, expanding its reach in household products, medical devices, and industrial packaging. In the food industry, PET's applications span from baked goods and blister packaging to fresh produce and salad dressings. The medical field leverages its antimicrobial property coatings to combat drug-resisting bacteria and create nosocomial infection-resistant products.

R&D efforts focus on improving mechanical properties and developing circular innovations for applications in the rail industry, cable sheathing, and thermal insulation products. PET's versatility extends to personal care products, where it is used in cosmetics, shampoo bottles, and packaging for various hair care products. The recycling sector sees advancements in PET recycling facilities, processing PET fines and producing recycled PET foam and woven plastic packaging. In the beverage industry, PET bottles and thermoformed packaging cater to consumer preferences for non-biodegradable plastic packaging. Government environmental policies and industry releases from trade associations shape the market landscape, pushing for more sustainable practices and technical limitations.

The polyester family, including PET, continues to unfold in various applications, from engineering resins and electrical insulation components to marine applications and printed designs. The ongoing coronavirus period underscores the importance of PET's role in essential industries, such as the production of essential goods and medical supplies. Despite these challenges, the market continues to expand due to its diverse applications and the increasing focus on circular innovations. The development of new resin manufacturing techniques and the establishment of PET recycling facilities are expected to further boost the market growth. However, challenges such as the high cost of raw materials and the presence of nosocomial infections in recycled PET remain. Authentic industry journals provide valuable insights into the latest trends, challenges, and opportunities in the PET market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polyethylene Terephthalate Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.5% |

|

Market growth 2025-2029 |

USD 24.77 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.7 |

|

Key countries |

China, US, India, Russia, Japan, Canada, Germany, Brazil, France, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Polyethylene Terephthalate Market Research and Growth Report?

- CAGR of the Polyethylene Terephthalate industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the polyethylene terephthalate market growth of industry companies

We can help! Our analysts can customize this polyethylene terephthalate market research report to meet your requirements.

RIA -

RIA -