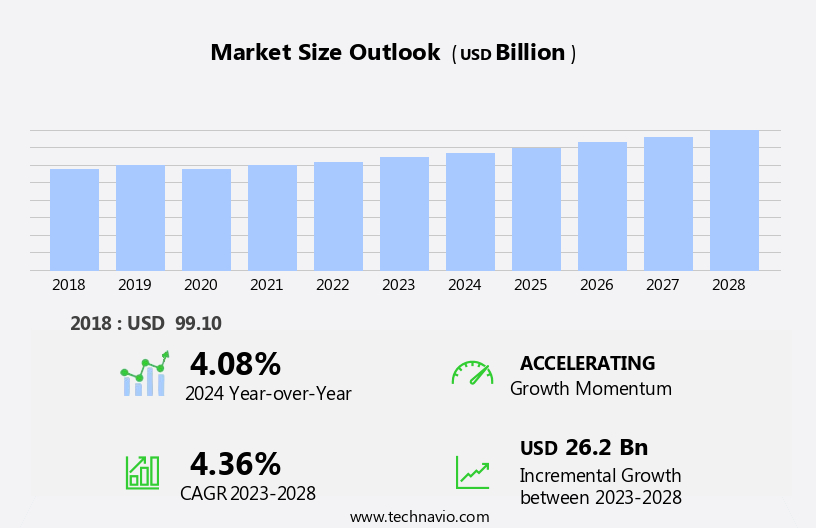

Polymer Foam Market Size 2024-2028

The polymer foam market size is forecast to increase by USD 26.2 billion, at a CAGR of 4.36% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the expanding bedding and furniture industries. These sectors are increasingly adopting polyurethane (PU) foams due to their superior comfort and durability properties. Market expansion hinges on various elements, notably the burgeoning bedding and furniture sector, the thriving building and construction industry, and surging demand for rigid foams. The rise in the bedding and home furniture industry acts as a catalyst, propelling market growth alongside the dynamic building and construction sector. However, this market faces challenges related to the environmental hazards associated with the manufacture and application of PU foams. The burgeoning bedding and furniture industries serve as a key growth driver for the market. PU foams are increasingly preferred for their ability to provide excellent comfort and support, making them an ideal choice for mattresses, pillows, and furniture cushions. This trend is expected to continue, fueling the demand for PU foams.

- Despite this growth, the market encounters challenges due to the environmental concerns surrounding PU foam production and usage. The manufacture of PU foams involves the emission of volatile organic compounds (VOCs), contributing to air pollution and potential health risks. Additionally, the disposal of PU foam waste poses environmental challenges due to its non-biodegradable nature. Companies must address these challenges by investing in research and development of eco-friendly alternatives or implementing sustainable production methods to mitigate their environmental impact and maintain market competitiveness.

What will be the Size of the Polymer Foam Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market showcases a dynamic and evolving landscape, driven by continuous advancements in technology and expanding applications across various sectors. Foam molding, laminating, elasticity, cutting, and resilience are integral processes shaping the industry, with each technique contributing to the development of diverse foam types. Polyurethane foam, sandwich panels, rigid foam, polyethylene foam, polystyrene foam, low-resilience foam, and foam assembly are just a few examples of the numerous foam varieties. Each foam type offers unique properties, such as buoyancy, compressive strength, thermal conductivity, and sound absorption, catering to specific industry requirements. Foam filtration, degradation, and regulations are essential aspects of the market, ensuring product quality and safety.

Standards and certifications play a crucial role in maintaining industry benchmarks, while foam recycling and sustainability initiatives drive innovation. Foam composites, laminates, and bonding techniques expand the potential applications of foam, enabling the creation of high-performance materials for various industries. Memory foam, microcellular foam, and cross-linked polymer foam are just a few examples of the advanced foam technologies emerging in the market. Foam machining, die cutting, and shaping processes enable the customization of foam products, catering to the unique needs of various industries. The ongoing evolution of foam technology and its diverse applications ensure a dynamic and ever-changing market landscape.

How is this Polymer Foam Industry segmented?

The polymer foam industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- PU

- PS

- PVC

- Phenolic

- Others

- Application

- Packaging

- Building and construction

- Furniture and bedding

- Transportation

- Others

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- India

- Japan

- South Korea

- South America

- Argentina

- Brazil

- Middle East and Africa

- UAE

- Rest of World (ROW)

- North America

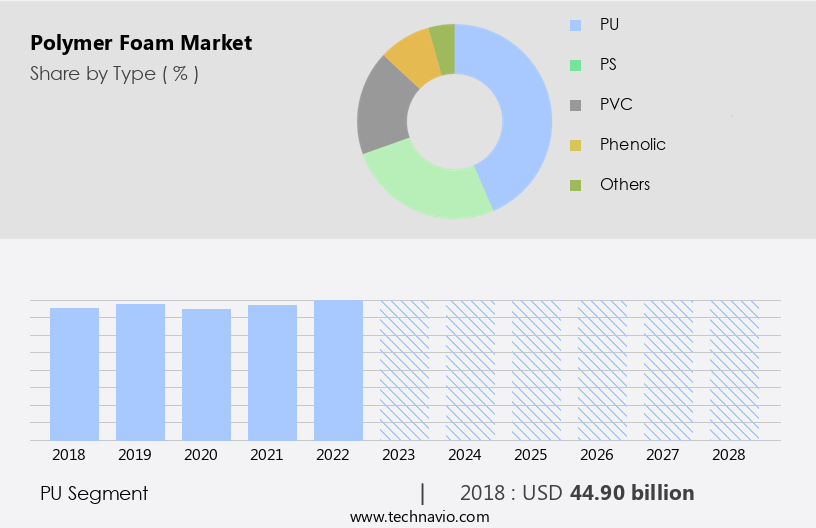

By Type Insights

The PU segment is estimated to witness significant growth during the forecast period.

Polymer foam, specifically polyurethane foam (PU), is a type of foam derived from the reaction of isocyanates with diols in the presence of a catalyst. The resulting product offers various applications due to the use of diverse isocyanates and diols. The global PU foam market experiences growth due to the expansion of the construction and infrastructure industries and the automotive sector. Population growth and increasing disposable incomes, particularly in countries like India, further fuel market demand. PU foam is produced through three primary stages: isocyanate production, polyol production, and PU foam manufacturing. Various types of PU foam include expanded polypropylene foam, high-resilience foam, polyvinyl chloride foam, anti-microbial foam, and more.

These foams cater to numerous industries, such as packaging, automotive, construction, and more. Foam processing techniques, like foam extrusion, foam lamination, foam molding, and foam machining, contribute to the versatility of PU foam. Additionally, foam regulations ensure product safety and quality. Foam properties, such as tensile strength, compressive strength, elasticity, and thermal conductivity, vary depending on the foam type. Foam insulation, foam cushioning, foam bonding, and foam gasket applications are essential in various industries. Foam recycling and the development of eco-friendly foam alternatives are current market trends, addressing environmental concerns. UV-resistant foam, flame retardant foam, and water-resistant foam cater to specific industry needs.

The global PU foam market's future looks promising, with ongoing research and innovation in foam technology. Cross-linked polymer foam, microcellular foam, and reticulated foam are some emerging foam types. Foam vibration damping, foam shaping, and foam seal applications are also gaining traction.

The PU segment was valued at USD 44.90 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

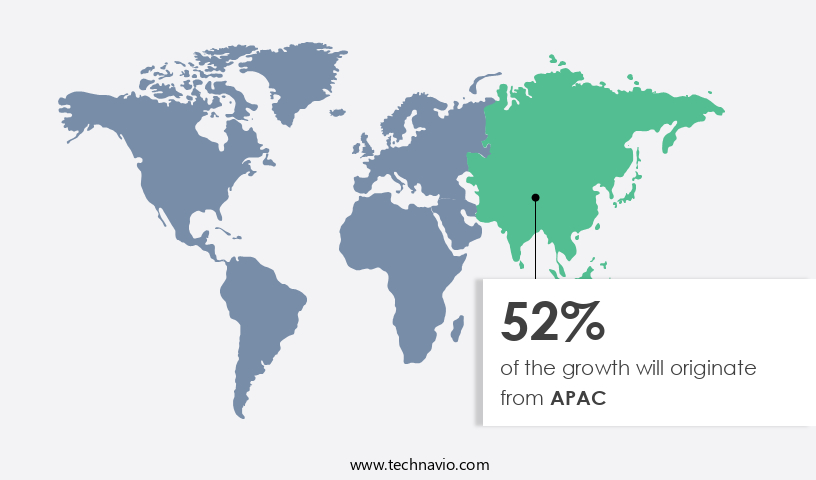

APAC is estimated to contribute 52% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific (APAC) is experiencing significant growth due to population and economic expansion, resulting in increased disposable income for consumers in countries like India, the Philippines, Malaysia, and China. This trend is anticipated to continue during the forecast period. The automotive industry, which is a major consumer of polymer foams, is expected to drive market growth in APAC, as China, Japan, India, and South Korea are among the top ten automotive producers globally. Furthermore, the demand for polymer foams is increasing in the food and beverage, alcoholic beverages, and pharmaceutical industries in APAC, contributing to market expansion during the forecast period.

Polymer foam applications include foam sound absorption, extrusion, filtration, degradation, standards, expanded polypropylene foam, die cutting, tensile strength, packaging, lamination, composites, compressive strength, high-resilience foam, polyvinyl chloride foam, anti-microbial foam, seal, recycling, thermal conductivity, uv-resistant foam, cushioning, bonding, buoyancy, closed-cell foam structure, shaping, microcellular foam, cross-linked polymer foam, vibration damping, regulations, molding, laminating, elasticity, cutting, resilience, polyurethane foam, sandwich panel, rigid foam, polyethylene foam, polystyrene foam, low-resilience foam, assembly, core, flame retardant foam, padding, certification, memory foam, machining, reticulated foam, flexible foam, water-resistant foam, density, cellular foam, insulation, open-cell foam structure, compounding, lining, gasket, and testing. These applications are witnessing growth due to various factors, including advancements in technology, increasing demand for lightweight materials, and stringent regulations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Polymer Foam Industry?

- The bedding and furniture industry's growth serves as the primary catalyst for market expansion.

- The global foam market encompasses various applications, including foam sound absorption, filtration, and packaging. Foam is produced through processes such as foam extrusion and die cutting, resulting in products with diverse properties, including high tensile and compressive strength. Expanded polypropylene foam and polyvinyl chloride foam are commonly used due to their durability and versatility. Foam's demand is driven by population growth and increasing consumer awareness of its benefits. With the global population projected to reach 9 billion by 2050, the need for insulation, cushioning, and filtration solutions is on the rise. In response, the market continues to innovate, with advancements in high-resilience foam and foam composites.

- However, foam degradation and adherence to industry standards remain critical challenges. Stringent regulations and certifications, such as those related to health and safety, are essential to ensure product quality and consumer trust. As the market evolves, it is crucial to stay informed of the latest research and developments to maintain a competitive edge.

What are the market trends shaping the Polymer Foam Industry?

- The investment in research and development for producing advanced PU foams is a mandatory trend in the upcoming market. This sector's growth is predicated on continuous innovation and improvement.

- The Polyurethane (PU) foam market experiences significant growth due to its increasing demand from various industries, including automotive. To cater to this rising demand, market participants are investing heavily in research and development (R&D). For instance, the exploration of bio-based PU, such as those synthesized from lignin polyols, is gaining traction. The integration of lignin during the manufacturing process enhances the mechanical properties of the resulting flexible PU foam, offering a unique open pore structure with numerous edges. Moreover, ongoing R&D efforts are anticipated to yield new applications for thermoplastic PU, thereby opening new market opportunities.

- PU foam's versatility extends to various applications, including anti-microbial foam for healthcare, foam seal for construction, foam cushioning for furniture, foam bonding for adhesives, foam buoyancy for marine applications, foam shaping for artistic creations, microcellular foam for electronics, cross-linked polymer foam for insulation, foam vibration damping for automotive components, and uv-resistant foam for outdoor applications. The market's growth is driven by factors such as the increasing demand for energy-efficient insulation, the growing automotive industry, and the expanding construction sector. However, regulations governing the production and disposal of foam waste, including foam recycling, pose challenges to market growth.

- Despite these challenges, the market's future looks promising, with continued innovation and advancements in foam technology.

What challenges does the Polymer Foam Industry face during its growth?

- The growth of the polyurethane industry is significantly impacted by the environmental challenges posed by its manufacturing and usage, which necessitates continuous research and implementation of sustainable practices to mitigate these hazards.

- The market encompasses various types of foam, such as polyurethane foam, polyethylene foam, and polystyrene foam, which are utilized in various applications including foam molding, foam laminating, and foam assembly. Foam elasticity and resilience are key attributes that make these materials popular in industries like automotive, construction, and packaging. However, the environmental concerns surrounding the production and disposal of polymer foams, particularly polyurethane foam, pose a significant challenge to the market's growth. Government regulations limiting the use of plastics, including foam, in developed nations like the US, Japan, and EU, are expected to adversely impact the market's growth during the forecast period.

- Additionally, the production of flexible polyurethane foam contributes to CO2 emissions, which is detrimental to the environment. Despite these challenges, the demand for rigid foam, such as foam sandwich panels, remains strong due to their insulation properties. Furthermore, the development of flame retardant foams is expected to mitigate some of the environmental concerns, providing opportunities for growth in the market. Overall, the market requires a balanced approach towards sustainable production and utilization to meet the growing demand while minimizing its environmental impact.

Exclusive Customer Landscape

The polymer foam market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polymer foam market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, polymer foam market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema SA - This company specializes in providing high-performing polymer foam solutions for various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema SA

- Armacell International SA

- BASF SE

- Borealis AG

- Boyd Corp.

- Dow Inc.

- FXI

- Huntsman Corp.

- Lanxess AG

- Mitsubishi Gas Chemical Co. Inc.

- Mitsui Chemicals Inc.

- Polymer Technologies Inc.

- RAG Stiftung

- Recticel Group

- Rogers Foam Corp.

- Saudi Basic Industries Corp.

- Toray Industries Inc.

- Tosoh Corp.

- Woodbridge Foam Corp.

- Zotefoams plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polymer Foam Market

- In March 2024, BASF, a leading chemical producer, introduced a new line of expanded polypropylene (EPP) foams under the brand name, Neopolen. These high-performance foams offer improved thermal insulation and are designed for use in automotive applications, appliances, and construction industries (BASF press release, 2024).

- In June 2025, Arkema, a major specialty chemicals company, announced a strategic partnership with LG Chem to develop and commercialize polymeric insulation materials for the building and construction sector. The collaboration aims to combine Arkema's expertise in high-performance polymers with LG Chem's advanced battery technology, leading to innovative insulation solutions (Arkema press release, 2025).

- In August 2024, Covestro, a global polymer manufacturer, completed the acquisition of the US-based foam manufacturer, Icynene-Lapolla. This acquisition expanded Covestro's presence in the spray foam insulation market and strengthened its position as a leading provider of insulation materials for the construction industry (Covestro press release, 2024).

- In January 2025, the European Union (EU) adopted new regulations on insulation materials, including expanded polystyrene (EPS) and extruded polystyrene (XPS) foams. The regulations set stricter emission limits for these foams, aiming to reduce greenhouse gas emissions and improve energy efficiency in the construction sector (European Commission press release, 2025).

Research Analyst Overview

- The market encompasses a diverse range of applications, from insulation and packaging to automotive and construction industries. Key components of this market include foam additives, which enhance foam properties, and foam supply chain management. Sustainability is a significant trend, with a focus on biodegradability and recycling technologies. Foam testing equipment ensures product quality, while industry associations foster collaboration and knowledge sharing. Innovation trends include advancements in foam mold design, extrusion process, and surface treatment.

- Regulatory agencies oversee foam manufacturing and use of blowing agents, while foam design software streamlines production. The competitive landscape is shaped by ongoing innovation and market segmentation. Foam colorants offer customization opportunities, and foam regulatory compliance is crucial for market success.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polymer Foam Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

197 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.36% |

|

Market growth 2024-2028 |

USD 26.2 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.08 |

|

Key countries |

China, US, Japan, Germany, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Polymer Foam Market Research and Growth Report?

- CAGR of the Polymer Foam industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the polymer foam market growth of industry companies

We can help! Our analysts can customize this polymer foam market research report to meet your requirements.

RIA -

RIA -