APAC Polyvinyl Chloride (PVC) Market Size 2026-2030

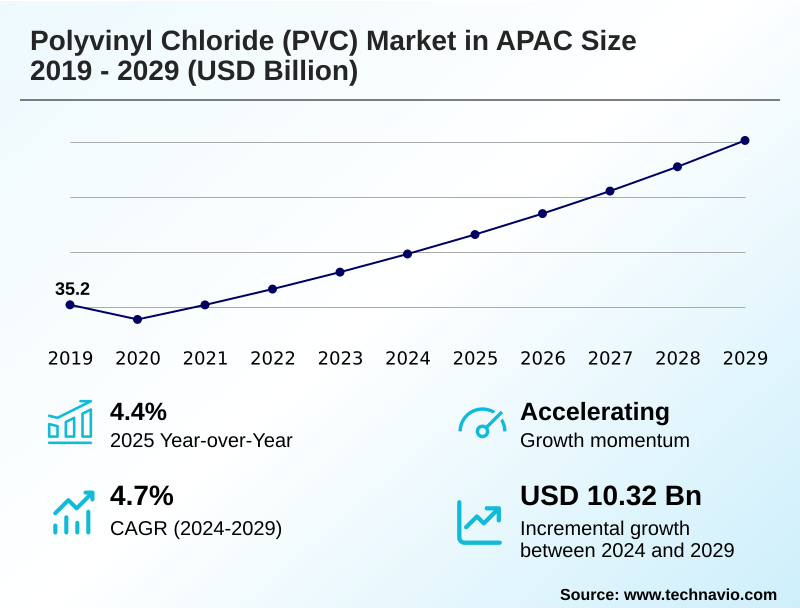

The apac polyvinyl chloride (pvc) market size is valued to increase by USD 10.88 billion, at a CAGR of 4.8% from 2025 to 2030. Growing infrastructure expansion and public housing initiatives will drive the apac polyvinyl chloride (pvc) market.

Major Market Trends & Insights

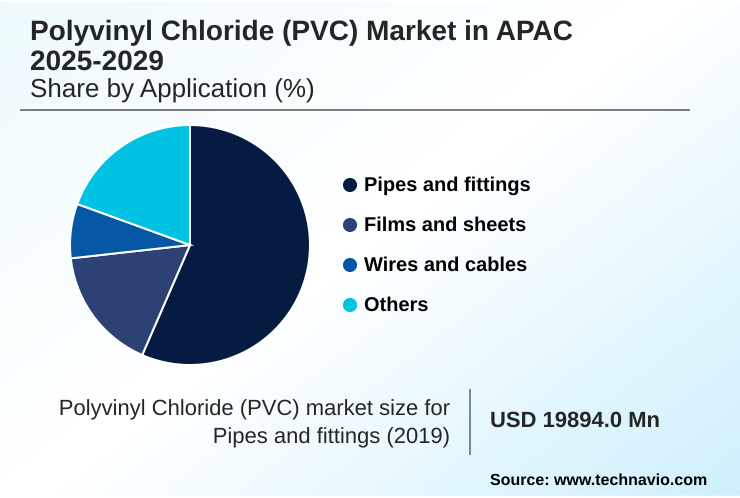

- By Application - Pipes and fittings segment was valued at USD 22.51 billion in 2024

- By Product - Rigid PVC segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 18.60 billion

- Market Future Opportunities: USD 10.88 billion

- CAGR from 2025 to 2030 : 4.8%

Market Summary

- The polyvinyl chloride (pvc) market in apac is experiencing sustained momentum, driven by expansive infrastructure development and rapid urbanization. Demand is centered on construction, electrical, and packaging applications, where the material's durability, corrosion resistance, and cost-efficiency are highly valued. A key trend shaping the industry is the strategic shift toward sustainability, which involves innovations in both production and end-of-life management.

- This includes the development of bio-attributed pvc grades and advanced chemical recycling technologies designed to create a more circular economy. For instance, a large-scale water infrastructure project might specify pvc pipes that incorporate 25% recycled content, aligning with government sustainability mandates while ensuring long-term performance.

- This scenario highlights the industry's dual focus: meeting the high-volume demand from growing economies while navigating increasing environmental scrutiny. Challenges persist, including volatility in feedstock pricing and competition from alternative polymers. However, ongoing investment in high-performance formulations like chlorinated pvc and low-smoke variants, alongside process optimizations in integrated chlor-vinyl manufacturing, positions the market for resilient growth.

- The industry's ability to innovate around material circularity goals and feedstock recovery will be critical for long-term success.

What will be the Size of the APAC Polyvinyl Chloride (PVC) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the APAC Polyvinyl Chloride (PVC) Market Segmented?

The apac polyvinyl chloride (pvc) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

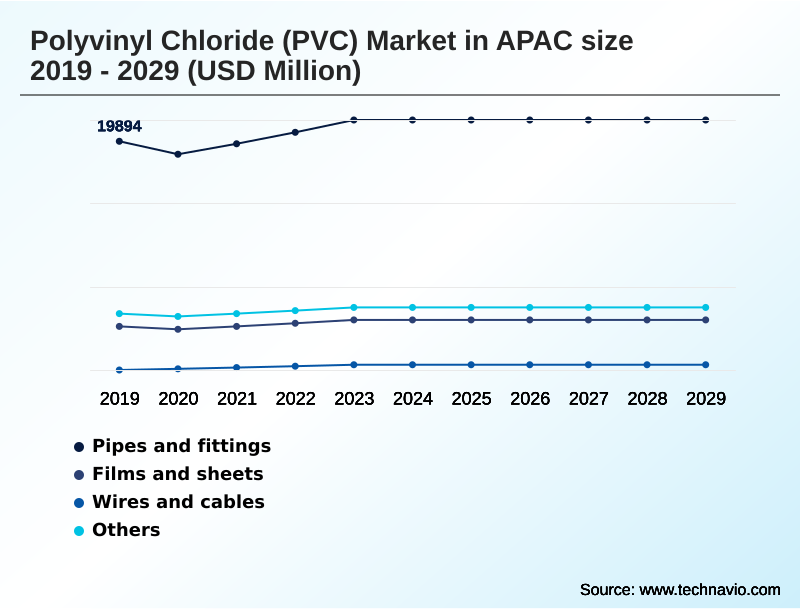

- Pipes and fittings

- Films and sheets

- Wires and cables

- Others

- Product

- Rigid PVC

- Flexible PVC

- Chlorinated PVC

- Low-smoke PVC

- End-user

- Building and construction

- Electrical and electronics

- Packaging

- Others

- Geography

- APAC

- China

- India

- Japan

- APAC

By Application Insights

The pipes and fittings segment is estimated to witness significant growth during the forecast period.

The pipes and fittings segment remains foundational, driven by infrastructure projects that prioritize long-term durability. Growth is supported by advancements in suspension polymerization, which improves the consistency of vinyl polymer chains.

Innovations in rigid pvc extrusion technology are enabling the production of more complex profiles, while new low-smoke pvc formulation techniques enhance fire safety in building applications.

The use of unplasticized polyvinyl chloride continues to be a standard for its structural integrity.

As the industry shifts, a focus on material circularity goals is evident, with some manufacturers achieving a 15% incorporation rate of post-consumer waste stream materials into non-critical applications.

This shift is increasingly supported by comprehensive life cycle assessment and positive technoeconomic evaluation.

The Pipes and fittings segment was valued at USD 22.51 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the Polyvinyl Chloride (PVC) Market in APAC requires a deep understanding of its application segments. The use of polyvinyl chloride pipe and fitting applications continues to dominate, driven by public infrastructure projects. In parallel, flexible pvc for wire and cable insulation is crucial for the expanding electrical and electronics sectors.

- For the building sector, rigid pvc profiles for construction industry applications offer a cost-effective alternative to traditional materials, while chlorinated pvc for hot water systems meets higher performance requirements. Fire safety compliance is addressed by low-smoke pvc for fire safety compliance. In packaging, pvc films and sheets for packaging provide durability and clarity.

- A significant trend is the adoption of bio-attributed pvc in sustainable products, supported by advanced chemical recycling of pvc waste streams. This involves new techniques like the catalytic conversion of post-consumer pvc and developing methods for managing chlorine content in pvc recycling. Processes such as thermal pretreatment for pvc waste are enabling new pathways for upcycling pvc waste into hydrocarbons.

- Producers are also focused on optimizing material performance through high-performance additives for rigid pvc and developing specialized pvc formulations for medical devices. Enhancing durability with pvc stabilizers remains a key R&D focus. The sustained cost-efficiency of pvc in infrastructure, with projects seeing up to 10% lower lifetime costs compared to metal alternatives, ensures its continued relevance.

- However, operations must adhere to strict compliance with pvc quality control orders, manage efforts to be reducing emissions from pvc production, and optimize integrated pvc and chlor-alkali production. Ultimately, success hinges on the ability to be optimizing pvc resin for extrusion processes.

What are the key market drivers leading to the rise in the adoption of APAC Polyvinyl Chloride (PVC) Industry?

- Growing infrastructure expansion and public housing initiatives are the primary drivers for the market.

- Market growth is fundamentally driven by demand from downstream processing applications, particularly in construction and electronics. The optimization of pvc resin viscosity is critical for fabricators, enabling faster processing speeds and reducing cycle times by up to 10%.

- Ensuring plasticizer compatibility is crucial for flexible applications to prevent material degradation. While mechanical recycling limitations persist, they are driving innovation in other areas. The development of specialized bio-attributed pvc grades is opening new market segments.

- Adherence to pvc homopolymer standards is non-negotiable for quality assurance. Performance is validated through metrics such as melt flow index and heat distortion temperature, with top-tier products achieving a 5% tighter tolerance, and tensile strength testing confirming durability.

What are the market trends shaping the APAC Polyvinyl Chloride (PVC) Industry?

- The proliferation of chemical recycling and material circularity is an emerging trend. This reflects a strategic industry shift toward advanced technologies that convert polyvinyl chloride waste into reusable feedstocks.

- Key trends are reshaping the competitive landscape, with a strong focus on high-performance and sustainable materials. The adoption of chlorinated polyvinyl chloride for applications requiring higher temperature resistance is growing, with some formulations showing a 20% improvement in thermal stability. For flexible pvc compounds, the emphasis is on developing non-phthalate plasticizers. Innovations in thermal stabilizer additives are extending product lifecycles.

- The most transformative trend is the move toward circularity through catalytic depolymerization and thermal dechlorination, enabling a monomer recovery process from post-industrial waste stream materials. This shift requires significant investment in new emissions control system technologies and a commitment to meeting stringent environmental compliance obligations, which can increase operational expenditures by 5-8%.

What challenges does the APAC Polyvinyl Chloride (PVC) Industry face during its growth?

- Stringent environmental regulations and sustainability mandates present a significant challenge to market growth.

- Key challenges stem from raw material production and environmental pressures. The synthesis of vinyl chloride monomer is energy-intensive, and producers are under pressure to innovate. The coal-based production route, prevalent in some regions, faces scrutiny, with lifecycle emissions being up to 50% higher than alternatives. The industry-standard chlor-alkali process also requires significant energy input.

- Developing high molecular weight pvc and incorporating vinyl acetate monomer adds complexity and cost. A primary focus is ensuring polymer chain durability and chemical resistance properties to guarantee long service life, a key value proposition.

- This is especially true for infrastructure applications where the inherent corrosion resistance benefit of PVC is a major selling point, with some systems demonstrating zero degradation after 40 years of service.

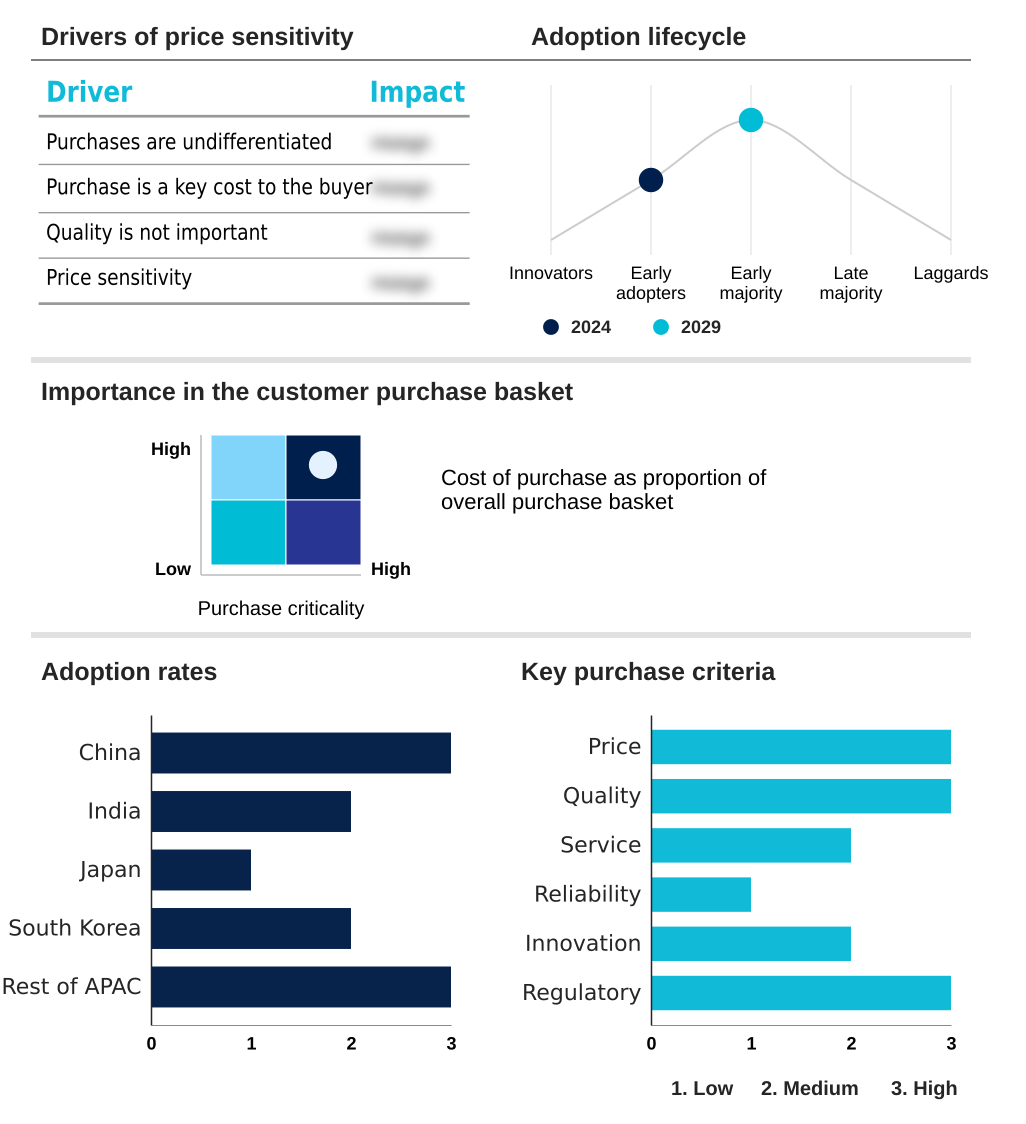

Exclusive Technavio Analysis on Customer Landscape

The apac polyvinyl chloride (pvc) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the apac polyvinyl chloride (pvc) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of APAC Polyvinyl Chloride (PVC) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, apac polyvinyl chloride (pvc) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Astral Ltd. - Delivering certified polyvinyl chloride resins and integrated piping systems engineered for critical infrastructure, plumbing, and agricultural applications, ensuring performance and material integrity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Astral Ltd.

- Avient Corp.

- Chemball HangZhou Chemicals

- Covestro AG

- DCM Shriram Ltd.

- DCW Ltd.

- Ercros SA

- Finolex Industries Ltd.

- Formosa Plastics Corp.

- Hanwha Solutions Corporation

- JM Eagle Inc.

- LG Chem Ltd.

- Occidental Petroleum Corp.

- Reliance Industries Ltd.

- Saudi Basic Industries

- Shin Etsu Chemical Co. Ltd.

- The Supreme Industries Ltd.

- Westlake Corp.

- Xinjiang Zhongtai Chemical

- Zhengzhou Sino Chemical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Apac polyvinyl chloride (pvc) market

- In August 2024, Reliance Industries outlined a strategic plan to significantly expand its integrated polyvinyl chloride production facilities, strengthening the regional supply chain for construction end uses.

- In January 2025, China's Ministry of Finance confirmed the elimination of the value-added tax rebate for polyvinyl chloride exports, effective April 2025, to manage overcapacity and bolster domestic utilization.

- In April 2025, LG Chem introduced new automotive interior materials and electric vehicle charging cables formulated with ultra-high molecular weight polyvinyl chloride at the CHINAPLAS exhibition.

- In May 2025, Orbia launched its global 'Vinyl in Motion' program, a comprehensive recycling initiative designed to advance material circularity for polyvinyl chloride products.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled APAC Polyvinyl Chloride (PVC) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 212 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2026-2030 | USD 10883.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | China, India, Japan, South Korea and Rest of APAC |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Polyvinyl Chloride (PVC) Market in APAC is defined by complex production dynamics, from the polymerization of vinyl chloride monomer to the formulation of end-products. The market leverages both the chlor-alkali process and coal-based production routes for integrated chlor-vinyl manufacturing.

- Core materials include suspension grade pvc resin, emulsion grade pvc, and specialized high molecular weight pvc, often combined with vinyl acetate monomer. Formulations vary from unplasticized polyvinyl chloride, known for its rigidity, to flexible pvc compounds, which require plasticizer compatibility. Innovations in chlorinated polyvinyl chloride and low-smoke pvc formulation are addressing niche performance demands.

- The supply chain relies on ethylene dichloride feedstock and is managed through pvc resin viscosity and homopolymer standards. A major focus is managing sustainability through advances in chemical recycling processes, including catalytic depolymerization and thermal dechlorination, which outperform mechanical recycling limitations.

- This push includes the development of bio-attributed pvc grades and the use of thermal stabilizer additives, signaling a shift in boardroom strategy toward materials with a 15% lower carbon footprint.

What are the Key Data Covered in this APAC Polyvinyl Chloride (PVC) Market Research and Growth Report?

-

What is the expected growth of the APAC Polyvinyl Chloride (PVC) Market between 2026 and 2030?

-

USD 10.88 billion, at a CAGR of 4.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Pipes and fittings, Films and sheets, Wires and cables, and Others), Product (Rigid PVC, Flexible PVC, Chlorinated PVC, and Low-smoke PVC), End-user (Building and construction, Electrical and electronics, Packaging, and Others) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Growing infrastructure expansion and public housing initiatives, Stringent environmental regulations and sustainability mandates

-

-

Who are the major players in the APAC Polyvinyl Chloride (PVC) Market?

-

Astral Ltd., Avient Corp., Chemball HangZhou Chemicals, Covestro AG, DCM Shriram Ltd., DCW Ltd., Ercros SA, Finolex Industries Ltd., Formosa Plastics Corp., Hanwha Solutions Corporation, JM Eagle Inc., LG Chem Ltd., Occidental Petroleum Corp., Reliance Industries Ltd., Saudi Basic Industries, Shin Etsu Chemical Co. Ltd., The Supreme Industries Ltd., Westlake Corp., Xinjiang Zhongtai Chemical and Zhengzhou Sino Chemical

-

Market Research Insights

- Market dynamics are shaped by the need to balance polymer chain durability with material circularity goals. Companies demonstrating superior chemical resistance properties and long service life see a 10% higher customer retention. A core challenge is managing post-consumer and post-industrial waste streams through efficient feedstock recovery and monomer recovery processes.

- Implementing backward integration strategy and improving downstream processing applications can reduce supply chain vulnerabilities by over 20%. The emphasis on life cycle assessment and technoeconomic evaluation is driving investment in advanced emissions control systems. Achieving regulatory compliance certification is non-negotiable, as failure to meet environmental compliance obligations can halt operations.

- Performance metrics like melt flow index, heat distortion temperature, tensile strength testing, and impact resistance measurement are critical for quality assurance and securing a corrosion resistance benefit in end-products.

We can help! Our analysts can customize this apac polyvinyl chloride (pvc) market research report to meet your requirements.

RIA -

RIA -